TL;DR:

- SBA interest rates are variable and depend on factors like loan type, size, lender, and economic conditions. Prime Rate at 6.75% in May 2026 drives most SBA 7(a) loans, with lenders adding caps and spreads for pricing. Borrowers should actively compare quotes, negotiate spreads, and consider fixed options or alternative SBA loans based on their long-term plans.

If you're planning to borrow through a Small Business Administration loan this year, understanding SBA interest rates May 2026 is one of the most practical things you can do before signing anything. Most business owners assume SBA rates are fixed and government-set. They aren't. What you actually pay depends on your loan type, your loan size, your lender's appetite, and a base rate that moves with the economy. This guide breaks down exactly what rates look like right now, how they're structured, and what you can do to make sure you're not paying more than you should.

Table of Contents

- Key Takeaways

- SBA 7(a) Interest Rates in May 2026

- SBA 504 and Microloan Rates Compared

- Factors that affect your SBA rate in 2026

- How to check SBA rates and choose the right loan

- My take on SBA rates and smarter borrowing

- Ready to explore your funding options?

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Prime Rate drives most SBA loans | The WSJ Prime Rate at 6.75% sets the floor for most SBA 7(a) variable-rate loans in May 2026. |

| Spreads are capped, not fixed | Lenders can charge less than the SBA maximum spread, which means negotiation is both allowed and worth pursuing. |

| Loan type determines rate structure | SBA 504 loans offer lower fixed rates than 7(a) loans, making them better suited for long-term asset purchases. |

| Rate adjustments happen quarterly | Variable-rate SBA loans reprice every quarter, so your payment can change as the Prime Rate moves. |

| Checking rates takes active effort | You need to gather lender quotes and monitor the Prime Rate yourself. No single official dashboard shows your actual rate. |

SBA 7(a) Interest Rates in May 2026

The SBA 7(a) loan is the most widely used SBA program, and its interest rate structure is more layered than most borrowers expect. Understanding the mechanics will help you compare quotes accurately and recognize when a lender is pricing you fairly.

How the base rate works

Most SBA 7(a) variable rates are built on top of the Wall Street Journal Prime Rate. As of May 2026, that rate sits at 6.75%. The lender then adds a spread on top of that base. The SBA caps how large that spread can be, and the cap depends on your loan size and term length.

Here's what those caps look like in practice:

| Loan Size | Term | Max Spread Above Prime | Approximate Max Rate |

|---|---|---|---|

| Over $50,000 | Under 7 years | Prime + 2.25% | 9.00% |

| Over $50,000 | 7 years or more | Prime + 2.75% | 9.50% |

| $50,000 or less | Any term | Prime + 6.50% | 13.25% |

These are ceiling numbers. Most lenders working with well-qualified borrowers price below the cap. A business with strong revenue, good credit, and solid collateral might land closer to Prime plus 1.5% on a larger loan, which at current rates would put you around 8.25%.

Variable vs. fixed rate options

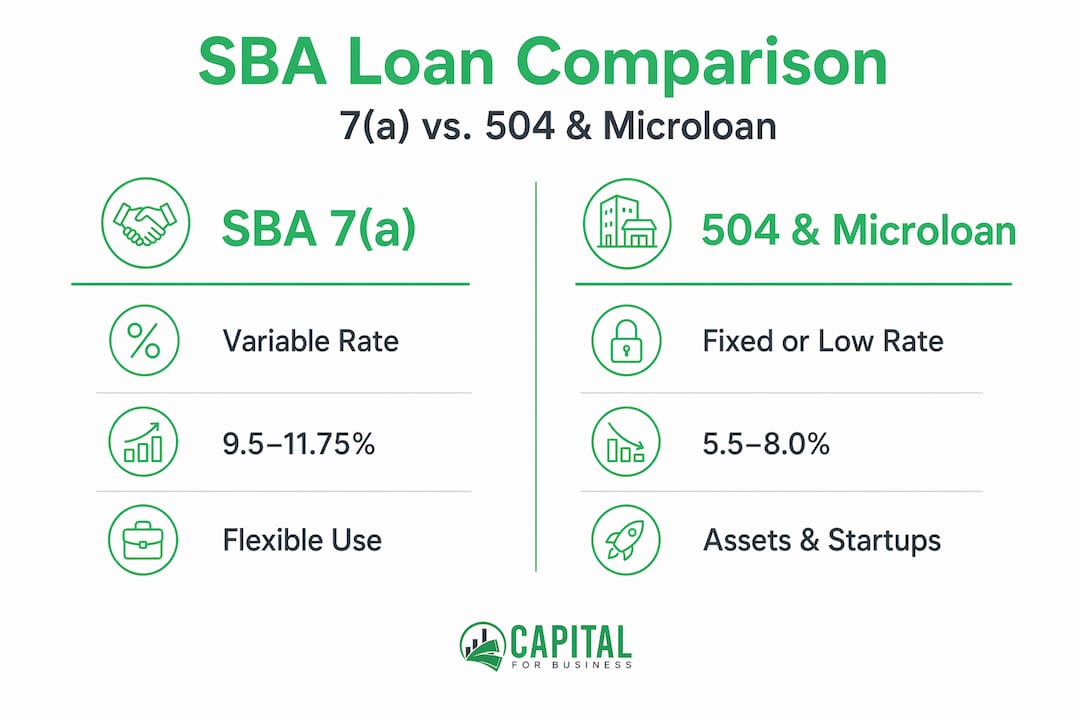

The majority of SBA 7(a) loans carry variable rates that adjust quarterly as Prime moves. If you prefer predictable payments, fixed-rate 7(a) loans are available, but they come at a cost. Fixed-rate 7(a) loans currently run approximately 9.75% to 12.25%, compared to variable options ranging from 9.50% to 11.75%. That premium reflects the lender's risk in locking your rate over the long term.

Fixed rates work well when you expect the Prime Rate to rise and you want to protect your cash flow. Variable rates make more sense when rates are trending down or when your loan term is short enough that the risk of adjustment is manageable.

Pro Tip: A 2-point reduction in your spread on a $500,000 loan over ten years saves over $60,000 in total interest. Always ask the lender what spread they're applying, not just what the final rate is. That distinction tells you how much room exists to negotiate.

SBA 504 and Microloan Rates Compared

Not every business needs a 7(a) loan. The SBA also offers 504 loans and microloans, each designed for specific purposes and priced very differently from 7(a) products.

SBA 504 loan rates

The 504 program finances major fixed assets like commercial real estate or heavy equipment. It's structured in two parts: a portion funded by a bank (typically 50% of the project), and a portion funded by a Certified Development Company or CDC (usually 40%). The CDC portion carries a government-backed fixed rate, and that's where the pricing advantage shows up.

504 CDC fixed rates currently range from 5.50% to 6.50% for terms of 20 to 25 years. That's meaningfully lower than what you'd pay on a long-term 7(a) loan at maximum spread. The reason is structural. CDC funding comes from bond markets backed by the SBA guarantee, which allows for lower rates than bank-originated products.

If you're buying a building or investing in major equipment with a 20-year horizon, the 504 program deserves serious consideration over a 7(a) loan strictly on rate grounds.

Microloan rates and use cases

SBA microloans serve businesses that need smaller amounts, typically under $50,000, and often newer businesses that don't yet qualify for standard bank terms. The trade-off is rate. Microloan rates typically run from 8% to 13%, reflecting the higher risk and smaller scale of these loans.

Microloans are administered through nonprofit intermediaries rather than traditional banks, and they often come with technical assistance and mentoring. If your funding need is small and your business is still building credit history, the rate is the cost of access, not a penalty.

Side-by-side comparison

| Loan Type | Rate Range | Terms | Loan Size | Best Used For |

|---|---|---|---|---|

| SBA 7(a) Variable | 9.50%–11.75% | Up to 25 years | Up to $5M | Working capital, expansion, equipment |

| SBA 7(a) Fixed | 9.75%–12.25% | Up to 25 years | Up to $5M | Predictable payments, rate lock |

| SBA 504 (CDC portion) | 5.50%–6.50% | 20–25 years | Up to $5.5M | Real estate, major fixed assets |

| SBA Microloan | 8.00%–13.00% | Up to 6 years | Up to $50,000 | Startups, small capital needs |

| SBA Express | 11.00%–13.50% | Up to 10 years | Up to $500K | Fast funding, smaller amounts |

Note that SBA Express loans currently range from 11.00% to 13.50%, reflecting the speed premium and reduced lender review requirements for that program.

Factors that affect your SBA rate in 2026

The rate you're quoted isn't arbitrary, but it also isn't purely mechanical. Several forces shape what you'll actually pay.

The Federal Reserve's role

Fed policy changes flow directly into SBA loan pricing through their effect on the Prime Rate. When the Fed raises the federal funds target rate, Prime follows within days, and your variable-rate SBA loan adjusts at the next quarterly repricing. The same works in reverse. A Fed rate cut eventually means lower SBA loan payments, though the benefit is delayed until your loan's next adjustment date.

This is why tracking Federal Reserve meeting outcomes matters if you carry or plan to take on variable-rate SBA debt.

Key factors lenders weigh when pricing your loan

- Credit score and history. Borrowers with scores above 700 consistently receive spreads below the SBA cap. Lower scores push lenders toward the maximum.

- Business revenue and cash flow. Lenders want to see consistent income. Strong debt service coverage ratios give you pricing leverage.

- Collateral quality. Real estate collateral is valued differently than equipment. Better collateral lowers lender risk and can lower your spread.

- Loan size. Larger loans carry lower maximum spreads by SBA rules. A $500,000 loan will almost always be priced lower than a $40,000 loan on a percentage basis.

- Lender competition. Getting quotes from multiple SBA-approved lenders creates real pricing pressure. Don't treat the first quote as your only option.

The SBA Optional Peg Rate

The SBA Optional Peg Rate sits at approximately 4.875% as of Q2 2026. This is an alternative base rate that some lenders use, particularly for fixed-rate SBA loans. It's set by the SBA itself rather than tracking the Prime Rate, and it can produce different pricing outcomes depending on market conditions. When you're comparing loan quotes, ask each lender which base rate they're using. That single question can reveal meaningful pricing differences across identical loan structures.

Pro Tip: Quarterly rate adjustments on variable loans can shift your monthly payment by hundreds of dollars if Prime moves significantly. Build a buffer of at least one to two months of projected higher payments into your operating reserves before drawing down a variable-rate SBA loan.

How to check SBA rates and choose the right loan

Knowing the rate structure is useful. Knowing how to apply that knowledge when you're actually shopping for a loan is what moves the needle for your business.

Here's a practical checklist to use when evaluating SBA loan options:

-

Look up the current WSJ Prime Rate. This is published daily by the Wall Street Journal and widely available online. It's your starting point for any variable-rate calculation.

-

Identify which SBA loan type fits your purpose. Real estate purchase points toward a 504. Working capital or equipment under a longer term points toward 7(a). Small amounts with limited credit history points toward a microloan.

-

Request quotes from at least three SBA-approved lenders. Rates vary by institution. Some lenders compete aggressively on spread; others don't. You won't know until you ask.

-

Ask each lender to itemize the spread and the base rate separately. Don't accept "your rate is 10.25%" without knowing if that's Prime plus 3.5% or Prime plus 2.75% plus fees buried elsewhere.

-

Ask about fees beyond interest. SBA guarantee fees, origination fees, and prepayment penalties all affect the true cost of borrowing. A lower rate with high fees can be more expensive than a higher rate with none.

-

Evaluate fixed vs. variable based on your business plan horizon. If you'll pay the loan off in three years, variable rate risk is limited. If you're locking into a 20-year real estate purchase, fixed-rate stability has real value.

-

Check for rate adjustment frequency and caps. Some variable-rate products include annual or lifetime rate caps. Those caps limit your worst-case payment scenario and are worth paying a small premium to secure.

For a broader view of your options beyond SBA programs, the best lending options for 2026 resource covers alternative structures worth comparing before you commit.

You can also review why banks decline small business loans if you're concerned about qualification, since understanding common rejection reasons helps you prepare a stronger application from the start.

My take on SBA rates and smarter borrowing

I've seen business owners walk into the SBA loan process thinking the rate is set in stone by the government. By the time they realize their lender priced them at the maximum allowable spread, they've already signed. That's an expensive lesson.

What I've learned from years of working with small business borrowers is that the published rate caps are starting points for lenders, not final numbers. The cap protects you from being overcharged beyond a certain point, but everything below that cap is negotiable. If your business financials are in good shape, bring them to every lender conversation. A clean balance sheet is your best negotiating tool.

I also think people underestimate the timing element. Borrowers who took variable-rate SBA loans when Prime was near its recent peak are now sitting on debt that adjusts down as the Fed holds or cuts. That's a good position to be in. If you're borrowing now with Prime at 6.75%, a variable-rate loan still makes sense if your business plan doesn't depend on a fixed monthly number and you expect rates to trend lower over the next few years.

The borrowers who consistently get the best SBA loan rates 2026 has to offer are the ones who come prepared with financial documentation, solicit multiple quotes, and ask specific questions about spreads rather than just rates. Lenders respond to informed borrowers differently than to those who simply accept the first offer. Arm yourself with the current data, understand what drives the number you're being quoted, and negotiate accordingly.

— Capital

Ready to explore your funding options?

At Capitalforbusiness, we've been helping small business owners access the right funding since 2009. Whether you're evaluating SBA loan rates 2026 offers or looking for a faster path to capital that doesn't require months of paperwork, we can match you with the right product for your situation. Our team understands SBA pricing structures, and we work with borrowers across hundreds of industries to find financing that fits both their budget and their growth plans.

Explore the full range of small business loan types we support, review our business funding solutions up to $500,000, or check out working capital loan options if you need fast operating funds. When banks say no, Capitalforbusiness finds a way forward.

FAQ

What are the current SBA 7(a) loan interest rates in May 2026?

SBA 7(a) variable rates currently range from 9.50% to 11.75%, based on the WSJ Prime Rate of 6.75% plus lender spreads. Fixed-rate 7(a) loans run slightly higher at 9.75% to 12.25%.

How do I find out what SBA interest rate I'll actually be offered?

You need to request quotes directly from SBA-approved lenders, since rates vary by institution. Ask each lender to break out the base rate and spread separately so you can make a true comparison across offers.

What is the difference between SBA 7(a) and SBA 504 loan rates?

SBA 7(a) loans carry higher variable rates in the 9.50% to 11.75% range, while SBA 504 CDC fixed rates run 5.50% to 6.50%. The 504 program is designed for real estate and major equipment purchases with longer terms.

Can I negotiate my SBA loan interest rate?

Yes. Lenders can and do price below the SBA maximum spread, especially for borrowers with strong credit and cash flow. Negotiating your spread on a large loan can reduce total interest costs by tens of thousands of dollars over the loan term.

How often do variable SBA loan rates change?

Most variable SBA 7(a) loans adjust quarterly based on Prime Rate movements. If the Federal Reserve changes rates, your loan payment will reflect that shift at the next quarterly adjustment date.