TL;DR:

- SBA loans are accessible to a wide range of small businesses, not just large or perfect-credit companies.

- The main SBA loan types are 7(a), 504, and microloans, each suited for different needs and stages.

- Proper planning, documentation, and timing are crucial for successful SBA loan applications.

Many small business owners assume SBA loans are reserved for large, established companies with perfect credit scores and years of financial records. That assumption keeps a lot of capable entrepreneurs from funding they could realistically access. The truth is, SBA loans are designed specifically for businesses like yours, whether you're expanding a retail location, buying equipment, or managing cash flow gaps. This guide breaks down what SBA loans are, the main types available, how to qualify, how they compare to other funding options, and what most guides leave out. By the end, you'll have a clear picture of whether an SBA loan is the right move for your next stage of growth.

Table of Contents

- Understanding SBA loans: What they are and who they help

- The main types of SBA loans for small businesses

- Eligibility, application process, and common pitfalls

- Comparing SBA loans with alternative funding options

- What most articles get wrong about SBA loans for small businesses

- Ready to grow? Explore the right financing solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| SBA loans are accessible | Small business owners often qualify for more flexible funding than they expect with SBA-backed loans. |

| Several loan types exist | There are SBA loan options for various purposes like working capital, real estate, and startups. |

| Compare before you apply | Understand the differences between SBA loans and alternatives to choose the right financing for your needs. |

| Canadian owners use CSBFP | Canadian businesses have support similar to the SBA through the CSBFP, but cannot access U.S. SBA loans. |

| Preparation boosts approval odds | Organizing documents and understanding requirements significantly increases your chance of getting approved. |

Understanding SBA loans: What they are and who they help

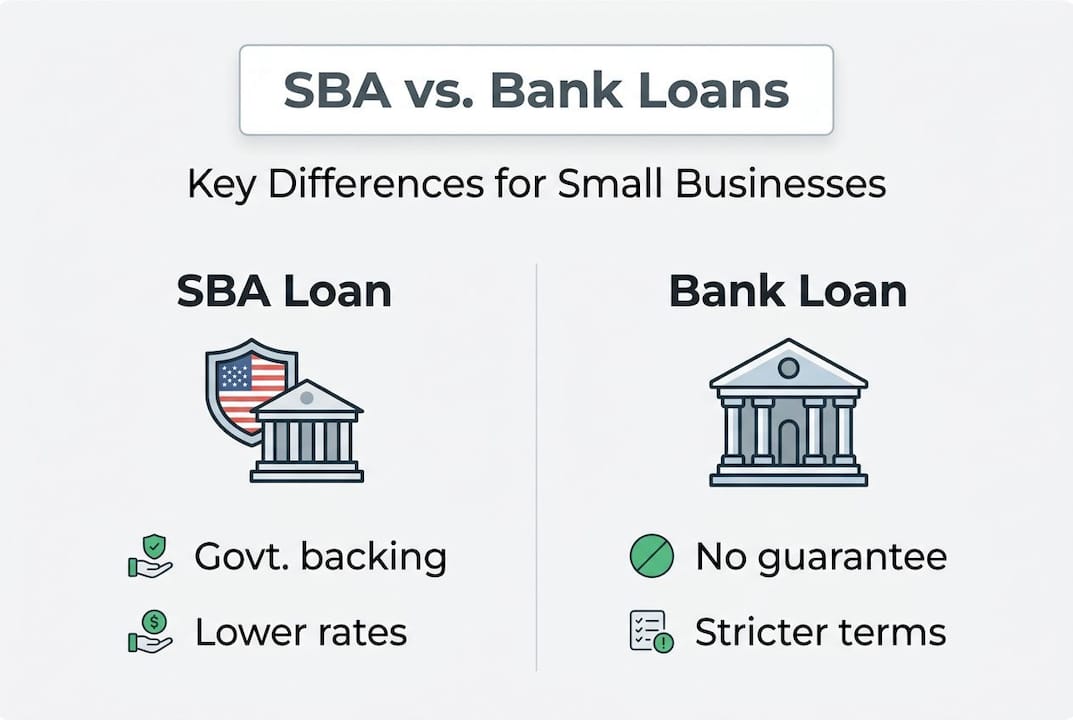

An SBA loan is not a direct loan from the government. The U.S. Small Business Administration guarantees a portion of the loan, which reduces the risk for approved lenders. That guarantee is what makes banks and credit unions more willing to lend to small businesses that might not qualify for conventional financing. You still borrow from a bank or approved lender, but the SBA's backing changes the terms significantly, often resulting in lower interest rates, longer repayment periods, and more flexible qualification standards.

The difference between an SBA loan and a traditional bank loan comes down to risk and access. Traditional bank loans rely entirely on the lender's confidence in your creditworthiness. SBA loans spread that risk, which is why government-backed SBA loans can reach businesses that banks would otherwise turn away. You still need to meet certain criteria, but the bar is more realistic for growing small businesses.

Here's a quick comparison of SBA loans versus traditional bank loans:

| Feature | SBA loan | Traditional bank loan |

|---|---|---|

| Government backing | Yes | No |

| Interest rates | Generally lower | Varies, often higher |

| Repayment terms | Up to 25 years | Typically 1 to 10 years |

| Qualification flexibility | Higher | Lower |

| Processing time | Weeks to months | Weeks |

| Loan amounts | Up to $5 million | Varies widely |

The three most common SBA loan types are the 7(a), the 504, and the microloan. Each serves a different purpose and a different type of borrower. Staying current on SBA loan updates helps you understand which programs are active and what terms are currently available.

For Canadian business owners, the closest equivalent is the Canadian small business loans program known as the Canada Small Business Financing Program (CSBFP). It operates on a similar guarantee model but is administered through the Canadian government and has its own eligibility rules.

Some common myths worth clearing up:

- Myth: SBA loans are only for businesses with perfect credit. Reality: Many SBA programs accept credit scores in the mid-600s.

- Myth: You need years of business history to qualify. Reality: Startups can access SBA microloans with limited operating history.

- Myth: SBA loans are a last resort. Reality: Many savvy business owners use them as a first-choice strategic tool.

- Myth: The process is too slow to be useful. Reality: SBA Express loans can be approved in as little as 36 hours.

With this foundation, let's look deeper at how SBA loans actually work, the main options available, and who benefits most.

The main types of SBA loans for small businesses

Now that we understand the basic loans available, let's dig into the specifics of each kind and who they're really meant for.

Here's a side-by-side overview of the three primary SBA loan types:

| Loan type | Max amount | Best for | Interest rates | Max term |

|---|---|---|---|---|

| SBA 7(a) | $5 million | Working capital, expansion | Prime + 2.25-4.75% | 10 to 25 years |

| SBA 504 | $5.5 million | Real estate, heavy equipment | Fixed, below market | 10 to 25 years |

| SBA microloan | $50,000 | Startups, underserved businesses | 8% to 13% | 6 years |

Choosing the right loan type depends on what your business actually needs. Here's a step-by-step approach to matching your goals with the right product:

- Identify your primary need. Are you buying property, covering payroll, or purchasing equipment? Your need determines your loan type.

- Assess your business stage. Newer businesses with limited history are better suited for microloans. Established businesses with real estate goals should look at 504 loans.

- Review your credit profile. Higher credit scores open up 7(a) and 504 options. If your score is still building, a microloan may be the most realistic starting point.

- Estimate your funding amount. If you need under $50,000, a microloan fits. Larger capital needs point toward 7(a) or 504 programs.

- Consider your collateral. 504 loans are secured by the asset being purchased. 7(a) loans may require additional collateral depending on the amount.

The SBA 7(a) loan is the most widely used option. It works well for working capital, refinancing existing debt, purchasing inventory, or funding business expansion. The flexibility of the 7(a) makes it the go-to choice for businesses with varied needs. You can explore easy small business loan types to see how these programs compare across lenders.

The SBA 504 loan is purpose-built for major fixed assets. If you're buying a building, renovating a facility, or purchasing heavy machinery, this is the loan designed for that. It's structured as two loans: one from a lender and one from a Certified Development Company (CDC). The fixed interest rate and long repayment term make it attractive for loan options for property investors and business owners making long-term capital commitments.

The SBA microloan is the most underrated option in the lineup. Microloans provide up to $50,000 through nonprofit intermediary lenders, with interest rates between 8% and 13% and repayment terms up to six years. They're specifically designed for startups, minority-owned businesses, and underserved entrepreneurs who may not yet qualify for larger programs.

Pro Tip: If you're a startup owner who keeps dismissing microloans because the amounts seem small, reconsider. A $30,000 microloan used strategically for equipment or inventory can generate enough revenue to qualify you for a 7(a) loan within 12 to 18 months. Think of it as a stepping stone, not a ceiling.

Eligibility, application process, and common pitfalls

Armed with the main loan options, let's move to the nuts and bolts of qualifying, applying, and steering clear of costly missteps.

To qualify for an SBA loan in the U.S., your business generally needs to meet these core requirements:

- Operate as a for-profit business

- Be physically located and operating in the United States

- Meet the SBA's size standards for your industry

- Demonstrate a reasonable ability to repay the loan

- Have invested some equity in the business

- Not be delinquent on any existing government debt

For Canadian business owners, the CSBFP mirrors SBA structure but operates at a smaller scale and under Canadian federal guidelines. U.S. business owners operating in Canada are not eligible for SBA loans. Canadians should apply through their chartered banks using the CSBFP framework instead.

Here's a step-by-step breakdown of the SBA loan application process:

- Determine the right loan type based on your funding need and business profile.

- Gather your financial documents. This includes two to three years of tax returns, current financial statements, a profit and loss statement, and a balance sheet.

- Prepare your business plan. Lenders want to see how you'll use the funds and how you plan to repay them.

- Check and improve your credit score. Both personal and business credit scores matter. Aim for at least 650 before applying.

- Find an SBA-approved lender. Use the SBA's lender match tool or work with a financing partner who already has established relationships.

- Submit your application. Complete all required SBA forms along with your supporting documents.

- Respond promptly to lender requests. Delays in providing additional information are one of the most common reasons approvals stall.

"Incomplete applications and poor documentation are among the top reasons SBA loan applications are delayed or denied. Preparation is not optional; it's the difference between approval and rejection."

Pro Tip: Before you apply, review your personal credit report and dispute any errors. Even a 20-point improvement in your credit score can shift you from a borderline application to a strong one. Review the SBA loan application tips to make sure you're not missing any key preparation steps. Once approved, knowing how to use loan funds strategically is just as important as getting them.

Common pitfalls to avoid include applying for the wrong loan type, underestimating the documentation required, and failing to clearly explain how the funds will generate revenue or support repayment.

Comparing SBA loans with alternative funding options

Finally, it's essential to compare SBA loans to other funding sources so you can make the most strategic choice for your business.

Not every business situation calls for an SBA loan. Sometimes a faster or more flexible option is the better fit. Here's a direct comparison:

| Funding type | Approval speed | Rates | Loan amounts | Best for |

|---|---|---|---|---|

| SBA 7(a) loan | Weeks to months | 7% to 10%+ | Up to $5 million | Growth, working capital |

| Traditional bank loan | Weeks | 5% to 12% | Varies | Established businesses |

| Online lender | 24 to 72 hours | 10% to 40%+ | $5k to $500k | Speed, flexibility |

| CSBFP (Canada) | Weeks | Prime + 3% | Up to CAD $1.15M | Canadian businesses |

| Merchant cash advance | 24 to 48 hours | Factor rate 1.1 to 1.5 | $5k to $250k | Revenue-based needs |

SBA loans offer some of the lowest rates and longest terms available to small businesses. But they're not always the fastest solution. If your business needs capital within a week, an online lender or bridge loan options may be a better short-term answer while you prepare a stronger SBA application.

Here are specific scenarios where each option makes the most sense:

- SBA loan: You need $200,000 to buy equipment and want the lowest possible interest rate with a long repayment term.

- Online lender: You have a cash flow gap and need $30,000 within 48 hours to cover payroll.

- Traditional bank loan: You have excellent credit, strong financials, and want a straightforward lending relationship.

- CSBFP: You're a Canadian business owner looking to finance equipment or leasehold improvements.

- Merchant cash advance: Your business has strong daily revenue and you need capital tied to sales volume rather than fixed payments.

Hidden costs are worth noting. SBA loans carry guarantee fees that can range from 0.5% to 3.75% of the guaranteed portion. Online lenders often have origination fees and higher effective rates. Technology-powered loans have made alternative lending faster and more transparent, but always read the full cost of capital before committing.

For a deeper look at microloan specifics and how they stack up, SBA microloan info provides detailed program breakdowns directly from the source.

What most articles get wrong about SBA loans for small businesses

Most guides treat SBA loans like a checkbox exercise: gather documents, submit application, wait. That framing misses the bigger picture entirely.

The business owners who get the most from SBA loans are the ones who approach them as a strategic tool, not a fallback. Timing your loan matters more than most applicants realize. Applying when your financials are trending upward, even if you don't urgently need the funds yet, puts you in a far stronger position than applying in a crisis.

Another overlooked reality: pairing an SBA loan with alternative funding often produces better outcomes than relying on one source alone. For example, using a microloan to cover startup costs while maintaining a business line of credit for operational flexibility gives you both structure and agility.

We've also seen business owners focus too heavily on their current financial snapshot when lenders actually want to see future growth projections. A well-constructed three-year revenue forecast, backed by realistic market data, can carry more weight than a solid current balance sheet. Show lenders where you're going, not just where you've been. That shift in perspective changes how your application reads and often changes the outcome.

Ready to grow? Explore the right financing solutions

Understanding SBA loans is a strong first step. Taking action on that knowledge is what actually moves your business forward.

At Capital for Business, we've helped small business owners across the U.S. and Canada find the right funding since 2009. Whether you're looking to explore SBA and business loan options or need a broader look at what's available, we make the process straightforward. Our team works with businesses in hundreds of industries, connecting owners to the programs that actually fit their situation. From Business Funding up to $500k to specialized programs for growth and equipment, we're here to help you move quickly and confidently. Visit our business funding solutions page to see what's available for your business right now.

Frequently asked questions

Who qualifies for an SBA loan as a small business owner?

Most U.S.-based small businesses may qualify if they meet SBA size standards, demonstrate repayment ability, and have invested some equity. A solid business plan and a credit eligibility review are also key factors lenders evaluate.

Can Canadian small business owners apply for SBA loans?

No, SBA loans are exclusively available to U.S.-based businesses. Canadian owners should look into the CSBFP program, which offers a similar government-backed lending structure through Canadian financial institutions.

What is the maximum amount for an SBA microloan?

SBA microloans provide up to $50,000 through nonprofit intermediary lenders, making them ideal for startups and underserved businesses that need smaller amounts of capital.

How long does SBA loan approval usually take?

Approval timelines vary by loan type and lender. Standard SBA 7(a) loans can take several weeks to a few months, while SBA Express loans are designed for faster turnaround, sometimes within 36 hours.

What can SBA loan funds be used for?

SBA loan funds can be applied to working capital, equipment purchases, real estate acquisition, inventory, debt refinancing, and general business expansion depending on the loan type you choose.