Small business owners are entering 2026 with record-level confidence, with 94% projecting growth this year. But confidence alone does not secure a loan. The lending landscape is shifting fast, shaped by technology, tighter bank standards, and a growing preference for non-bank financing. Whether you are planning to expand, purchase equipment, or simply stabilize cash flow, understanding where lending is heading gives you a real advantage. This article breaks down the key trends, compares your options, and gives you practical steps to improve your chances of getting funded in 2026.

Table of Contents

- What's driving small business lending in 2026?

- Bank vs. non-bank loans: A 2026 comparison

- How technology and AI are transforming lending

- Key challenges: Approval odds, interest rates, and tighter standards

- Preparing to succeed: Steps for small business borrowers in 2026

- Explore the best small business lending solutions for your growth

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Non-bank lenders surge | In 2026, most small businesses favor non-bank and online lenders for speed and easier access. |

| AI speeds up approvals | AI and automation often cut funding decisions to less than two days, transforming how loans are approved. |

| Partial funding is common | Nearly half of applicants receive only part of the funds they request, so alternative strategies are essential. |

| Credit standards tightening | Banks and lenders have stricter requirements and fewer approvals as 2026 trends continue. |

| Preparation is key | Business owners should update financials and explore multiple funding options to boost loan success. |

What's driving small business lending in 2026?

With this optimism as a backdrop, it is critical to understand the factors stirring lending trends and shaping access in 2026. The mood among small business owners is genuinely positive, but the data tells a more layered story.

The Federal Reserve's Small Business Credit Survey shows a revenue index drop to 33, signaling that future expectations are softening even as current confidence holds strong. That gap between optimism and outlook is something lenders are watching closely. It affects how they assess risk and set terms.

At the same time, SBA 7(a) loan volume is down 18% year over year in early 2026, following a record peak in 2025. Higher purchase rates in the 3% to 4% range are cooling demand for government-backed loans. This is pushing more borrowers toward alternative funding options that offer faster decisions and fewer documentation requirements.

Here is what is shaping the 2026 lending environment:

- Record optimism among small business owners, with 94% expecting growth

- Softening revenue forecasts creating caution among traditional lenders

- SBA volume correction following the 2025 peak, driven by higher rates

- Surge in non-bank lending, fueled by speed, accessibility, and technology in lending

- AI-driven underwriting reducing friction and approval timelines significantly

"The gap between small business optimism and lender caution is the defining tension of 2026 financing. Knowing which side of that gap you fall on determines your strategy."

Bank vs. non-bank loans: A 2026 comparison

Now let's break down where small business owners actually turn for funding, and what approval looks like in 2026.

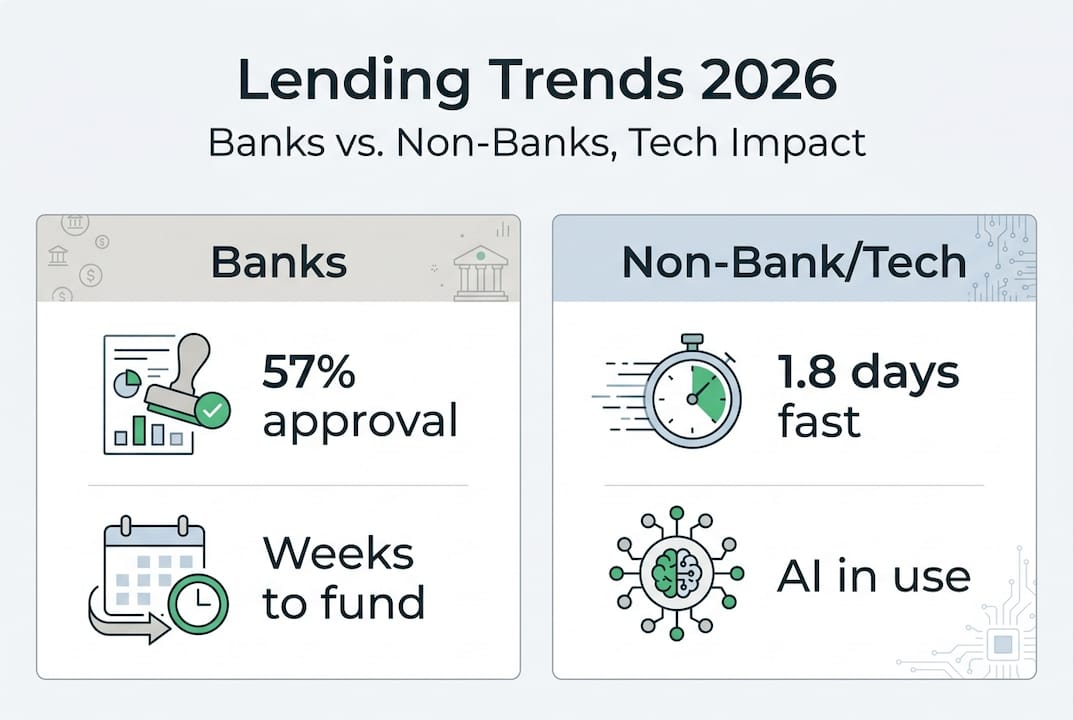

Approval rates vary significantly depending on where you apply. According to Federal Reserve data, small banks fully fund 57% of applications, large banks fund 43%, and online lenders fund 38%. Partial funding is common across all lender types, affecting roughly 48% of applicants.

| Lender type | Full funding rate | Speed | Best for |

|---|---|---|---|

| Small banks | 57% | Slow (weeks) | Established businesses with strong credit |

| Large banks | 43% | Slow (weeks) | High-revenue businesses with collateral |

| Online lenders | 38% | Fast (1 to 3 days) | Newer businesses needing quick capital |

| Non-bank lenders | Varies | Fast (24 to 72 hrs) | Flexible needs, lower credit thresholds |

Despite lower full-funding rates, 74% of small business owners now prefer non-bank lenders over traditional banks, citing speed and ease as the top reasons. That preference is reshaping the market. Understanding the types of small business loans available from each source helps you match your needs to the right lender.

Pro Tip: Do not assume the lender with the highest approval rate is your best option. A small bank may fund more applications, but if your business is under two years old or your credit score is below 680, an online lender may be your fastest and most realistic path to capital.

To improve your approval odds regardless of lender type, follow these steps:

- Pull your business credit report and resolve any errors before applying

- Prepare at least 12 months of bank statements and profit and loss statements

- Know your debt service coverage ratio before a lender calculates it for you

- Apply to multiple lender types simultaneously to compare offers

- Be ready to explain any revenue dips with context and a recovery plan

How technology and AI are transforming lending

Much of the rapid change in lending is being driven by technology. Here is what is new and why it matters for your next application.

AI-powered underwriting is now cutting time-to-fund to 1.8 days at many non-bank lenders, compared to weeks at traditional banks. By Q4 2026, automated underwriting is predicted to deliver decisions in under four hours. That is a fundamental shift in how quickly capital can move.

| AI adoption metric | Current figure |

|---|---|

| Small businesses using AI | 56% |

| Reporting positive impact | 87% |

| Avg. time-to-fund (AI lenders) | 1.8 days |

| Predicted underwriting time by Q4 2026 | Under 4 hours |

With 56% of small businesses now using AI in some capacity, and 87% reporting a positive impact, the technology is no longer a novelty. It is a competitive tool. Lenders using AI can analyze cash flow patterns, transaction history, and business performance data in minutes, giving borrowers with strong fundamentals a real edge even if their credit score is not perfect.

Here is how AI is changing the borrower experience:

- Faster pre-qualification with minimal paperwork

- Real-time cash flow analysis replacing manual document review

- Personalized loan offers based on actual business performance

- Reduced bias in underwriting through data-driven decisions

- Instant alerts if additional documentation is needed

Pro Tip: When applying through an AI-powered platform, connect your business bank account directly if the option is available. Lenders using technology in small business loans can pull live data, which often speeds up approval and may result in better terms than a static document submission.

Key challenges: Approval odds, interest rates, and tighter standards

Technology brings speed, but it is not all smooth sailing. Let us look at the challenges that can catch borrowers off guard.

Credit standards are tightening. The Senior Loan Officer Opinion Survey (SLOOS) recorded net tightening of 8.9% among banks in Q4 2025, meaning more banks are raising the bar for approval. Outstanding small business loans now exceed $71 billion, and while lending volume is growing, demand is slightly weaker as borrowers weigh higher costs.

"Tighter standards do not mean no access. They mean you need to show up better prepared than you did two years ago."

Only 52% of applicants received the full amount they requested in the most recent Federal Reserve survey, with rising costs cited as the top challenge. That means nearly half of all applicants either received partial funding or were declined. Understanding why banks decline loans is the first step to avoiding that outcome.

Three mistakes to avoid when applying in a tighter market:

- Applying without reviewing your credit profile. Lenders are scrutinizing credit more carefully. A score below 650 will limit your options significantly at traditional banks.

- Underestimating the importance of cash flow documentation. Even profitable businesses get declined when cash flow statements are incomplete or inconsistent. Review SBA lending updates to understand current documentation expectations.

- Ignoring partial funding as an option. If you need $200,000 and are offered $120,000, that partial offer may still be worth taking. Understand how small business loan accounting works before you decline a partial offer.

Preparing to succeed: Steps for small business borrowers in 2026

Success in this market means taking proactive steps. As banks and lenders change, so should your application strategy.

Online lender applications have grown for the fifth consecutive year, according to Federal Reserve survey data, with rising costs remaining the top challenge for applicants. That growth reflects a real shift in borrower behavior. More business owners are skipping the bank line entirely and going straight to digital platforms.

Here is a practical checklist to prepare your business for a 2026 loan application:

- Financial statements: Have at least two years of profit and loss statements and balance sheets ready

- Bank statements: Provide 12 months minimum, with clear explanations for any unusual activity

- Business plan: Update your plan to reflect current market conditions and 2026 revenue projections

- Credit profile: Check both personal and business credit scores and dispute any inaccuracies

- Collateral inventory: Know what assets you can offer if a lender requires security

- Alternative lender research: Identify at least two non-bank options before you apply anywhere

Pro Tip: Get quotes from at least three lenders before committing. Rates and terms vary widely in 2026, and a few hours of comparison shopping can save you thousands over the life of a loan. Explore your funding options in 2026 before locking in with the first offer you receive.

Understanding the trade-off between speed and cost is also essential. A fast online lender may charge a higher factor rate than a bank, but if you need capital in 48 hours to fulfill a contract, that cost may be justified. Match the financing tool to the actual business need, not just the lowest rate.

Explore the best small business lending solutions for your growth

With these tips and trends in mind, partnering with a forward-thinking provider can give your business the competitive financing edge it needs in 2026.

At Capital for Business, we have been helping small business owners access the right financing since 2009. Whether you need to understand the easy loan types available to you, explore our full range of funding solutions, or find out if a merchant cash advance fits your cash flow situation, we are ready to help. We work fast, keep costs transparent, and specialize in the situations where banks say no. Reach out today and let us match you with the financing option that fits your 2026 growth plan.

Frequently asked questions

What types of lenders are most popular for small business loans in 2026?

Non-bank and online lenders lead borrower preference in 2026, with 74% of small business owners choosing them over traditional banks for their speed and simpler application process.

Are approval rates for business loans increasing or decreasing in 2026?

Full approvals remain competitive, with small banks funding 57% of applications fully while partial funding affects nearly half of all applicants across lender types.

How is AI changing the loan application process?

AI now cuts time-to-fund to 1.8 days on average, with automated underwriting expected to deliver decisions in under four hours by Q4 2026.

What is the outlook for SBA 7(a) lending in 2026?

After a record $45 billion funded in fiscal year 2025, SBA 7(a) volume is down 18% in early 2026, with more than half of approved loans under $150,000.

What's the main challenge for small business borrowers in 2026?

Rising operating costs and tighter credit standards are the top barriers, with only 52% of applicants receiving the full loan amount they requested.