TL;DR:

- In 2026, small business owners face a diverse lending landscape that emphasizes speed, flexibility, and approval likelihood over just low rates. Alternative lenders, fintech platforms, and SBA microloans now provide faster decisions, tailored loan structures, and valuable support compared to traditional banks. Success depends on understanding all available options, matching funding needs to the right lender, and prioritizing full funding and suitability over solely seeking the lowest interest rate.

Small business owners in 2026 are facing a lending market that looks almost nothing like it did a decade ago. The assumption that walking into a bank branch is the natural first step for business funding is outdated, and in many cases, it is actively working against growth. Alternative lenders, fintech platforms, and specialized programs like SBA microloans are now capturing a significant portion of the market, offering faster decisions, more flexible requirements, and products designed around how real businesses actually operate. This article breaks down your best options, how they compare, and how to choose the right path for your specific situation.

Table of Contents

- How the small business lending landscape has evolved by 2026

- Comparing lending options: Banks, fintechs, and alternative lenders

- SBA microloans and intermediary models: Small-dollar funding with support

- Choosing the right lending option for your business needs

- Avoiding common pitfalls when seeking funding in 2026

- A smarter take: Why your business needs more than the lowest rate

- Explore funding solutions tailored for your business

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Alternative lenders lead | Fintech and online lenders now account for a major share of small business loans due to faster approval and funding. |

| Approval odds matter | Choosing a loan based solely on rate can backfire if your chances of full approval are low. |

| SBA microloans support growth | For smaller, targeted needs, SBA microloans combine funding with training and flexible requirements. |

| Match lender to your needs | Start with your timeline, cash flow, and amount when selecting between banks, fintechs, or other options. |

| Preparation is key | Proper documentation and understanding lender-specific requirements greatly boost approval odds. |

How the small business lending landscape has evolved by 2026

The lending world has shifted in ways that genuinely surprise many business owners, especially those who have not sought funding in a few years. Not long ago, your local bank was the obvious starting point. Today, that assumption deserves a serious second look.

Fintech lenders now originate 28% of new small business loans, up from single digits just a few years ago. That is not a minor shift. It represents a fundamental change in how capital flows to businesses like yours. Fintech and online alternative lenders have built platforms that remove friction from the borrowing process, and business owners have responded by embracing them in large numbers.

Understanding the current 2026 lending trends matters because the market is no longer one-size-fits-all. You now have a genuine menu of options, and selecting wisely depends on knowing what has changed and why.

Here is what is driving the evolution:

- Speed expectations have risen sharply. Business owners now expect decisions in hours or days, not weeks. Fintech platforms have set a new benchmark that traditional banks are struggling to match.

- Documentation burdens differ widely. Banks still require extensive paperwork, financials, and collateral in most cases. Online lenders often work with streamlined applications that pull data directly from business accounts.

- Flexibility in loan structure is more available. Alternative lenders offer short-term options, revenue-based repayment, and merchant cash advances that banks typically do not provide.

- Approval rates vary significantly by lender type. Traditional banks approve a smaller percentage of small business applications compared to online and alternative lenders.

- Support services are bundled into some programs. Certain loan types, particularly SBA-linked options, come with business training and advisory support built into the process.

"The question is no longer just what rate can I get, but which lender is actually likely to approve me and fund my business on the timeline I need." This shift in thinking is what separates business owners who secure funding from those who waste weeks pursuing the wrong source.

Tracking the broader financing trends for 2026 makes clear that the smartest borrowers are the ones who enter the process understanding all available channels, not just the most familiar ones.

With old assumptions around bank lending out of the way, let's dig into what options are truly available today.

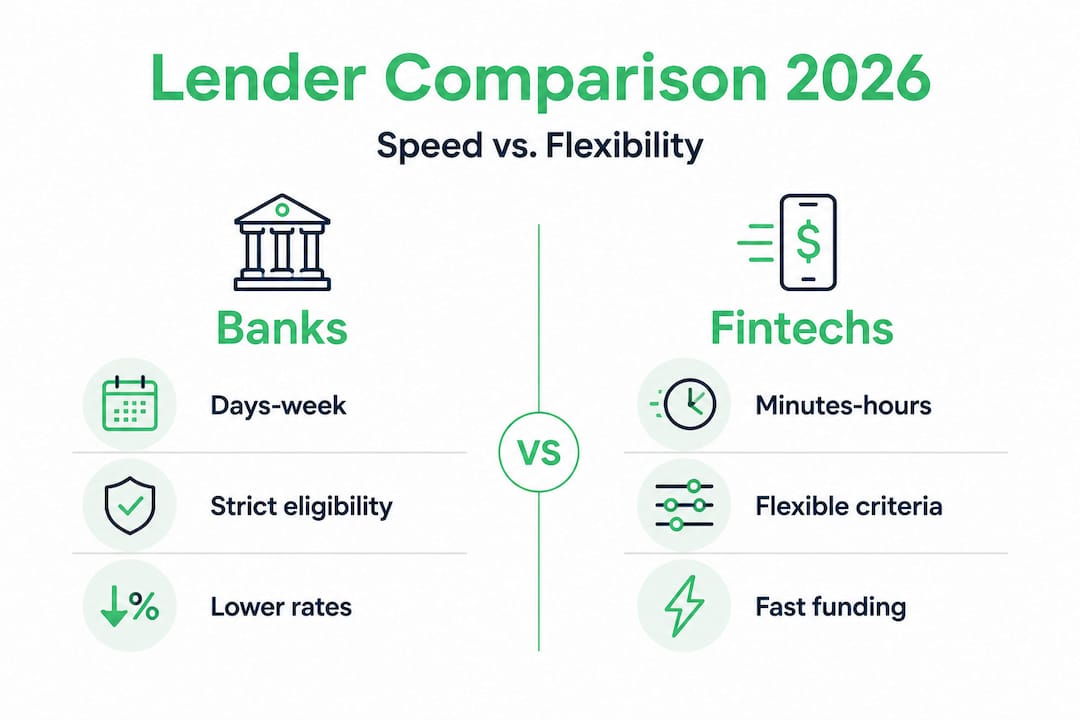

Comparing lending options: Banks, fintechs, and alternative lenders

Now that you recognize the players, see exactly how each compares in 2026 when it comes to what matters for small businesses.

Fintech lenders offer approval in minutes and funds in 24 to 48 hours, while traditional banks have slower, more document-heavy processes. But speed is just one dimension. Use the comparison below to see where each lending type stands across the factors that actually drive your decision.

| Factor | Traditional banks | Fintech lenders | Alternative lenders |

|---|---|---|---|

| Approval speed | Days to weeks | Minutes to hours | Hours to days |

| Time to funding | 1 to 4 weeks | 24 to 48 hours | 1 to 5 days |

| Application complexity | High | Low to moderate | Low to moderate |

| Credit requirements | Strict | Moderate | Flexible |

| Loan amounts | $50,000 to $5M+ | $5,000 to $500,000 | $5,000 to $1M+ |

| Collateral required | Often yes | Sometimes | Varies |

| Interest rates | Lower (qualified applicants) | Moderate to higher | Moderate to higher |

| Best for | Established, well-documented businesses | Fast-moving needs, early-stage | Revenue-based, non-traditional needs |

Each of these lending types serves a distinct niche. A restaurant owner who needs $30,000 to replace kitchen equipment before the summer season opens has a very different profile from a manufacturing company seeking $800,000 to expand its production floor. Matching the lender type to the situation is more important than optimizing for the lowest rate alone.

Key factors to weigh when comparing your alternative financing choices:

- Your timeline. How quickly do you need funds? If a supplier deal closes in five days, a bank loan is not a realistic option regardless of its rate.

- Your documentation readiness. Do you have audited financials, tax returns, and detailed business plans ready? If not, fintech or alternative lenders will be far less demanding.

- Your approval probability. A lower rate means nothing if you get denied. Consider which lender type is realistically likely to approve a business at your stage.

- Loan structure fit. Does your business have predictable monthly revenue, or does it run on seasonal cash flow? Some loan products are built for irregular income patterns; banks generally are not.

Pro Tip: Pull your last 12 months of business bank statements before approaching any lender. This single action speeds up the application process with almost every lender type and lets you spot cash flow patterns that affect which loan structure actually fits your business.

SBA microloans and intermediary models: Small-dollar funding with support

Beyond big sums and flashy fintech speed, the smallest businesses have an often-overlooked option: the SBA's microloan model.

SBA microloans under $50,000 are funded through nonprofit intermediaries, who may also require business training or planning support as part of the process. This model is meaningfully different from walking into a bank or applying online. The intermediary relationship adds a layer of accountability and support that many small business owners actually find valuable, especially if they are early in their business journey.

Here is how the SBA microloan program is structured in practice:

| Feature | Details |

|---|---|

| Maximum loan amount | $50,000 |

| Average loan size | Approximately $13,000 |

| Loan term | Up to 6 years |

| Interest rate range | Typically 8% to 13% |

| Who administers loans | Nonprofit intermediary organizations |

| Technical assistance | Often required or available |

| Eligible uses | Working capital, inventory, equipment, supplies |

| Ineligible uses | Real estate purchases, paying existing debt |

To make the most of an SBA microloan, follow this process:

- Identify an approved intermediary in your area. The SBA maintains a directory of approved intermediaries by state and region. Each has its own lending criteria within SBA guidelines, so your experience will vary depending on which organization you work with.

- Review their specific requirements. Some intermediaries require a business plan, personal financial statements, and participation in a business training course. Others may have additional documentation requirements.

- Complete the required training or support components. This is not just a box to check. Many business owners report that the technical assistance tied to these programs genuinely improved how they managed their finances and planned growth.

- Submit a complete application. Incomplete applications are one of the most common reasons for delays. Having all documents ready before you start the process saves significant time.

- Understand the timeline. SBA microloans take longer than fintech options, but they also come with lower rates and added support. Expect a process of several weeks from application to funding.

Pro Tip: If you are a newer business or a startup with limited credit history, the SBA microloan path through a nonprofit intermediary is worth exploring before automatically assuming you need a larger or more expensive loan. The added business support can provide value well beyond the funding itself.

Staying current on SBA loan updates helps you understand recent changes to eligibility and program availability that could affect your decision.

Choosing the right lending option for your business needs

Knowing what each lender offers, here's how to confidently pick the best fit for your next stage of growth.

Full funding approval and fit for your needs impacts the effectiveness of a loan far more than just price. This is a critical insight that many business owners overlook when they start the funding search focused only on advertised interest rates.

Follow these steps to make a clear-headed decision:

- Map your cash flow timing before anything else. Know exactly when you need funds, when you can start repaying, and what your monthly cash position looks like over the next 12 months. This determines which loan structures are actually viable for your business.

- Define your funding purpose precisely. Are you buying equipment with a multi-year useful life, covering a short-term inventory gap, or funding a six-month marketing push? Each purpose maps to a different product type. Equipment financing, working capital loans, and merchant cash advances each have a different cost and structure profile.

- Assess your approval likelihood honestly. Check your business credit score, personal credit, time in business, and annual revenue. Then compare these against the typical approval thresholds for each lender type. Apply where your profile is strongest, not just where the rate looks best.

- Factor in your timeline to funds. If your need is urgent, a traditional bank or SBA loan is almost never the right first call. If you have three to four months of runway, you have more options and more negotiating room.

- Evaluate total cost, not just rate. Factor fees, prepayment penalties, and origination costs into your comparison. A fintech loan at a higher rate with no origination fee may cost less in total than a bank loan at a lower rate with substantial closing costs.

- Consider what support comes with the product. For very small businesses or newer owners, the technical assistance tied to SBA microloan programs or the advisory relationships at some community development financial institutions can provide real value beyond the dollar amount.

Prioritizing access to funds over theoretical optimization is what separates business owners who move forward from those who stay stuck in analysis. A loan you can actually get and use is worth more than a perfect loan you do not qualify for.

Resources like navigating loan approvals and a clear understanding of your available funding options for 2026 will help you enter any lender conversation with confidence.

Avoiding common pitfalls when seeking funding in 2026

To keep your lending experience smooth, let's explore the critical mistakes and hidden success habits business owners need to know.

Technical assistance, required documents, and realistic expectations about speed and flexibility are all part of a successful loan application today. Skipping any one of these elements is where applications fall apart.

Here are the most common mistakes to avoid:

- Applying without knowing your numbers. Lenders will ask about revenue, expenses, outstanding debts, and cash reserves. Business owners who cannot answer these questions clearly raise immediate red flags.

- Chasing the lowest rate to the wrong lender. A bank with a 7% rate that denies your application does nothing for your business. An alternative lender at 14% that funds you in three days and fits your repayment cycle might be the far better choice.

- Submitting incomplete applications. Missing tax returns, unsigned documents, or outdated financials are among the top reasons for delays and denials. Review every checklist twice before submitting.

- Ignoring smaller loan options. Many business owners assume they need large loans when a targeted $15,000 to $30,000 microloan would cover the actual need. Borrowing more than you need increases costs and repayment burden.

- Overlooking the value of intermediary support. For business owners newer to managing credit and debt, the training and advisory support tied to programs like SBA microloans has real long-term value. Treating it as an obstacle misses the point.

- Not shopping across multiple lender types. Getting quotes from only one type of lender limits your ability to compare total cost of capital across the full market.

- Underestimating the time involved. Even fast fintech lenders require accurate, complete information. Rushing an application without preparing documentation leads to delays or denied requests.

Pro Tip: Build a simple funding file that stays updated year-round. Keep your last two years of tax returns, three to six months of bank statements, a current profit and loss statement, and a one-page summary of how you plan to use any loan proceeds. This single preparation habit puts you ahead of most business owners the moment a funding need arises.

Applying the smart financing tips that experienced borrowers use consistently improves both approval rates and the quality of loan terms you receive.

A smarter take: Why your business needs more than the lowest rate

Here is an opinion that runs against a lot of conventional advice: the interest rate on your small business loan is often one of the least important factors in deciding whether that loan helps or hurts your business.

Business owners spend an enormous amount of time comparing rates. Rate comparison tools, loan calculators, and advertised APR figures dominate the conversation. But approval likelihood and full funding are just as important as price and rate, since getting denied or only partially funded genuinely harms growth plans.

Think about what a partial approval actually means in practice. You budgeted $80,000 to upgrade equipment and hire two staff members. A lender approves $40,000. Now you can do one or the other, but not both, and the growth plan you built falls apart. A different lender at a slightly higher rate might have approved the full amount and made the whole plan work. The rate difference costs you a few hundred dollars per month. The funding gap costs you the entire growth initiative.

The same logic applies to timing. A loan that arrives six weeks after your opportunity has closed does nothing for you regardless of how competitive the rate was. Speed and timing are not soft factors. They are central to whether a loan creates value for your business.

We have worked with business owners across hundreds of industries since 2009, and the pattern is consistent: the owners who grow the most reliably are the ones who think about fit and access first, then cost. They ask: will I get approved? Will I get the full amount? Will the funds arrive when I need them? Can I actually service this repayment schedule given my cash flow? Only after those questions are answered do they turn to rate comparison.

The smarter business financing strategies that lead to sustainable growth treat lending as a strategic tool, not a commodity to be price-shopped. The right loan at the right time for the right purpose will always outperform the cheapest loan that arrives late, covers only part of your need, or comes with a repayment structure that strains your cash flow every month.

Rate matters. It is not irrelevant. But in 2026, with more lender types and more product structures available than ever before, the business owners who win are those who evaluate the full picture.

Explore funding solutions tailored for your business

Understanding your options is the first step. Taking action on that understanding is what actually moves your business forward.

At Capital for Business, we have spent over 15 years helping small business owners find the right funding product for their specific situation, not just the most convenient one. Whether you need a fast working capital solution, equipment financing, a merchant cash advance, or a structured business loan, we match you with the product that fits your business timeline, approval profile, and growth goals. Explore the full range of easy business loan types available to you, browse our business funding solutions page to see what fits your current stage, or connect with our team through our fast business loans portal to get started today.

Frequently asked questions

What are the fastest business loan options available in 2026?

In 2026, fintech and online lenders offer approvals in minutes and funding within 24 to 48 hours, making them the fastest business loan providers available to small business owners.

How do SBA microloans differ from other small business loans?

SBA microloans up to $50,000 are made through nonprofit intermediaries and often include required business training or advisory support, which conventional bank loans and fintech products do not typically offer.

What should I consider first when picking a lender in 2026?

Match your business's cash-flow timing, realistic approval likelihood, and funding speed to the loan offer before comparing rates, since getting the right product match determines whether funding actually serves your growth plan.

Is the lowest loan rate always the best choice?

No. Full approval and funding likelihood are just as important as the interest rate, since a partial approval or denial at a low rate does far less for your business than full funding at a slightly higher one.

Can I use an SBA microloan for any business expense?

SBA microloans can be used for working capital, inventory, equipment, and supplies, but allowable uses exclude purchasing real estate or paying off existing business debts.