TL;DR:

- Alternative financing offers faster, more accessible funding options compared to traditional banks.

- It includes diverse products like term loans, MCAs, invoice factoring, and revenue-based financing.

- Using these tools strategically for short-term needs helps avoid long-term financial pitfalls.

Many small business owners still assume the bank is their only option when they need capital. That assumption is increasingly outdated. Small businesses are approved more frequently by online lenders than large banks, according to the Federal Reserve's 2025 Small Business Credit Survey. This shift reflects a broader change in how capital flows to growing businesses across the U.S. and Canada. Alternative financing, meaning business funding from non-bank sources, now covers a wide range of products built around the actual needs of small business owners. This article defines what alternative financing is, compares it to traditional lending, breaks down the main product types, and helps you figure out which option fits your business.

Table of Contents

- What is alternative financing?

- How alternative financing compares to traditional lending

- Types of alternative financing options for small businesses

- Expert nuances and practical considerations

- A realistic perspective: What most experts miss about alternative financing

- Explore tailored funding solutions with Capital for Business

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Alternative financing basics | Business loans outside banks can offer faster, more flexible solutions. |

| Diverse product options | Choose from term loans, merchant cash advances, invoice factoring, and more. |

| Higher approval rates | Online lenders generally approve more small business applications than banks. |

| Evaluate risks carefully | Understand terms, avoid stacking MCAs, and match repayment to revenue. |

What is alternative financing?

Alternative financing refers to any business funding that comes from sources outside traditional banks and credit unions. It is not a single product. It is a category that includes many different structures, each designed for a specific type of business need or repayment capacity.

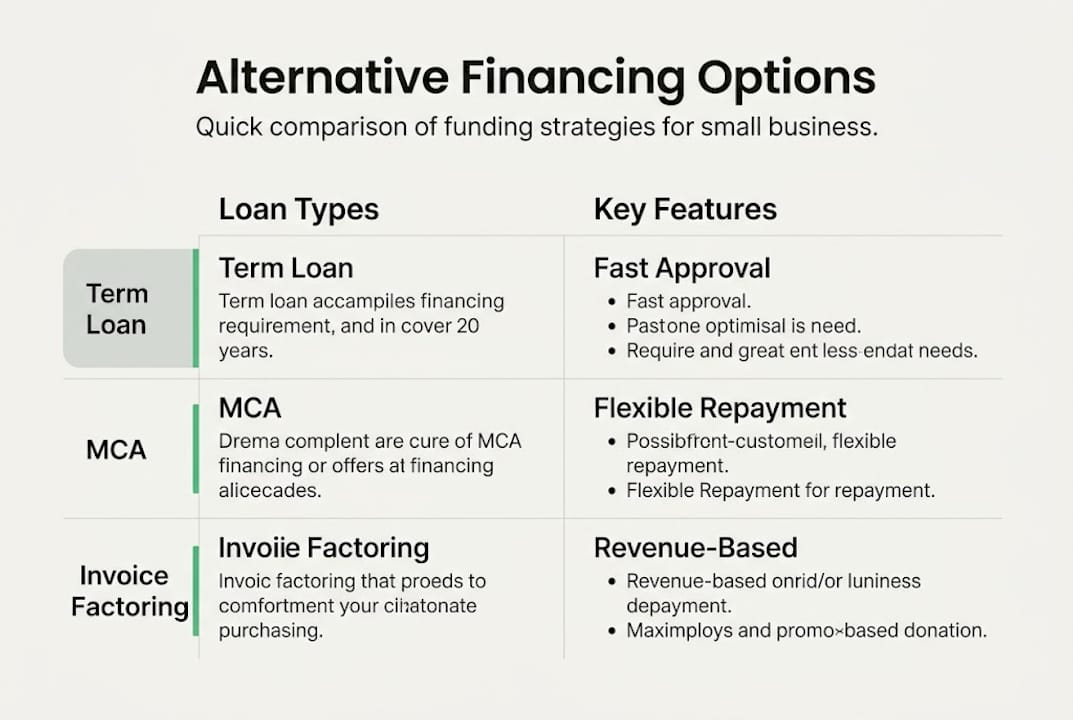

According to a range of products that fall under this label, alternative financing includes merchant cash advances (MCAs), term loans, invoice factoring, revenue-based financing (RBF), equipment financing, and business lines of credit. Each works differently, and each suits a different type of business situation.

Here is a quick overview of the main types:

- Term loans: A lump sum repaid over a fixed period with scheduled payments. Good for predictable expenses like expansion or renovation.

- Merchant cash advances: Funding based on future sales, repaid as a percentage of daily card transactions. Suited for businesses with consistent card revenue.

- Invoice factoring: Selling unpaid invoices to a lender for immediate cash. Useful when customers pay slowly but work is already complete.

- Revenue-based financing: Repayment fluctuates with monthly revenue. Useful for seasonal or variable-income businesses.

- Equipment financing: Funds tied directly to purchasing specific equipment, with the equipment acting as collateral.

- Business line of credit: A revolving credit limit you draw from as needed. Ideal for managing cash flow gaps.

What separates these products from traditional bank loans is the application process, underwriting criteria, and repayment structure. Banks evaluate your personal credit score, years in business, collateral, and financial history in detail. Alternative lenders focus more on current cash flow, business performance, and revenue trends. The application is usually faster, often completed online, and decisions can come within hours rather than weeks.

| Feature | Traditional bank | Alternative lender |

|---|---|---|

| Application time | Days to weeks | Hours to days |

| Approval criteria | Credit score, collateral, history | Cash flow, revenue, performance |

| Repayment flexibility | Fixed monthly payments | Daily, weekly, or revenue-linked |

| Funding speed | Weeks to months | 24 to 72 hours |

| Eligibility for startups | Low | Moderate to high |

Businesses that explore fast-track growth solutions for the first time often find alternative lending far more accessible than expected. Understanding why banks reject funding is also useful context before you apply anywhere.

Pro Tip: Match your lender type to your cash flow pattern. If your income is daily and card-based, an MCA may fit better than a term loan. If you invoice large clients on net-60 terms, invoice factoring solves the problem a line of credit only partially addresses.

How alternative financing compares to traditional lending

Traditional bank lending has long been the default for small business owners seeking capital. But that model has shifted noticeably over the last several years. Banks have tightened their approval standards, particularly for businesses under three years old or those without significant collateral. The process is slow, documentation-heavy, and often ends in rejection for the businesses that need funding most.

Alternative lenders have stepped in to fill that gap. Approval rates are higher at online lenders than at large banks, and the turnaround from application to funding is dramatically shorter. For a business owner facing a payroll crunch or a time-sensitive supplier opportunity, this difference is not just convenient. It can be decisive.

"The alternative capital surge is not a trend. It is a structural response to a gap that traditional banks have not been able to close for small businesses."

In Canada, the growth of alternative lending is equally significant. The Canadian market for alternative small business financing is projected to reach $4.2B by 2028, reflecting strong demand from business owners who cannot meet bank requirements or who simply need faster access to capital.

Here is how the two models compare across key dimensions:

| Category | Traditional bank | Alternative lender |

|---|---|---|

| Average approval rate | 13 to 20% (large banks) | 40 to 60% (online lenders) |

| Time to funding | 30 to 90 days | 1 to 5 business days |

| Credit score requirement | 680 or higher | Often 550 or higher |

| Collateral required | Frequently required | Often not required |

| Loan size range | $50,000 and up | $5,000 to $500,000+ |

Some of the specific advantages of alternative lending include:

- Flexible qualification: Revenue and cash flow matter more than credit history alone.

- Faster decisions: Many lenders use automated underwriting, so approvals arrive in hours.

- Smaller loan amounts: Many alternative products start at $5,000, which banks rarely offer.

- Variety of products: From fast, flexible funding to specialized equipment loans, the range of choices is broad.

- Accessible for newer businesses: Businesses with less than two years of history still have options.

For business owners researching online business loans, the contrast with bank timelines becomes especially clear. What takes a bank two months often takes an alternative lender two days. That speed can change outcomes for businesses operating in competitive or seasonal markets.

Types of alternative financing options for small businesses

Term loans, MCAs, invoice factoring, and RBF are among the most commonly used alternative financing products, and each serves a distinct business profile. Knowing which one fits your situation is more important than chasing the lowest rate.

Here is a practical breakdown:

1. Term loans A fixed amount repaid over a set period, usually 3 to 36 months. These work well for planned investments like new staff, location expansion, or rebranding. The cost is predictable, and the structure is straightforward.

2. Merchant cash advances An advance on future sales, repaid daily as a percentage of card receipts. Speed is the main advantage; merchant cash advance products can fund within 24 hours. The cost can be high if the repayment period extends unexpectedly.

3. Invoice factoring You sell outstanding invoices to a lender at a discount in exchange for immediate cash. Invoice factoring explained simply: you get 80 to 95 cents on the dollar now instead of waiting 30 to 90 days for payment. Best suited for B2B businesses with reliable clients.

4. Revenue-based financing Repayment is tied to a fixed percentage of monthly revenue. When revenue dips, so does the payment. Revenue-based financing suits seasonal businesses or those with variable monthly income.

5. Equipment financing Funds are used exclusively to purchase equipment, and the equipment secures the loan. This keeps your cash free for operations. See equipment financing basics for a practical intro.

Experts recommend hybrid stacks and matching products to specific business needs rather than relying on a single funding source. For example, a seasonal retailer might combine a line of credit for inventory with RBF for year-round flexibility.

Key things to consider when evaluating any option:

- Total cost of capital: Compare factor rates and APRs, not just monthly payments.

- Repayment frequency: Daily deductions from a bank account affect cash flow differently than monthly payments.

- Prepayment terms: Some products have penalties for early payoff; others reward it.

- Impact on credit: Business credit factors vary by product, so ask how each lender reports to credit bureaus.

- Renewability: Some products can be renewed before payoff; others require full repayment first.

Pro Tip: Avoid stacking multiple MCAs without a clear exit plan. Each advance adds a layer of daily repayment that compounds quickly. If you find yourself taking a second MCA to service the first, that is a warning sign to pause and reassess.

Expert nuances and practical considerations

Knowing what products exist is only part of the equation. The more important skill is knowing how to evaluate them against your business's actual repayment capacity and risk tolerance.

One area where many business owners make costly mistakes is repayment structure. Daily repayment products work well when revenue is consistent, but they become a problem during slow periods. Weekly or monthly repayment schedules are gentler on cash flow and give you more room to manage unexpected expenses. Revenue-driven structures, where payments scale with income, are often the most sustainable choice for businesses with seasonal or unpredictable revenue.

AI underwriting is changing the speed and scope of eligibility decisions significantly. Lenders now use machine learning to assess risk based on bank transaction patterns, sales data, and even platform reviews, rather than relying solely on credit scores. This means more businesses qualify than ever before, including those that traditional banks would have turned away. It also means decisions arrive faster and with less paperwork.

The role of technology in lending has also expanded the range of products available in smaller markets and rural areas. Businesses that once had no realistic access to capital beyond a local bank now have dozens of lenders competing for their application.

That said, there are genuine risks. The regulatory environment for alternative lending is less standardized than banking, which means terms and disclosures vary widely. Some lenders are transparent and fair; others bury fees in complex agreement language. Before accepting any offer, read the full agreement and understand:

- What the total repayment amount will be

- Whether there are origination fees, late fees, or renewal penalties

- How the lender handles prepayment

- Whether the agreement requires a personal guarantee

Businesses that have used alternative financing to bridge funding gaps successfully tend to share one habit: they treated each product as a bridge to a specific goal, not as ongoing income.

Use this credit checklist to evaluate your business credit profile before applying anywhere. Strong credit gives you negotiating power even with alternative lenders.

Pro Tip: Before you accept any fast-cash offer, identify your exit ramp. What revenue milestone or event will allow you to pay it off early or transition to cheaper long-term financing? Without that answer, short-term products can become long-term obligations.

A realistic perspective: What most experts miss about alternative financing

Most guides on alternative financing focus on product types and approval odds. What they often miss is the deeper question of whether any given product actually fits the problem a business owner is trying to solve.

Alternative financing is excellent at solving urgent, short-term capital needs. It is not designed to fix structural business problems like weak margins, poor pricing, or over-reliance on a single client. A business that needs capital because its model is not profitable will not become profitable by taking on more debt, regardless of how fast the money arrives.

The businesses that use alternative financing well treat it as a tool with a specific job. They use it to bridge a seasonal gap, fund a growth opportunity, or cover an unexpected expense while waiting on receivables. They do not use it as a substitute for revenue.

Use alternative financing for bridge or growth scenarios, and actively avoid cycles where one advance funds the repayment of another. That pattern traps businesses in a loop that is difficult to exit without disrupting operations.

Hybrid approaches work well here. A business might use MCA for growth during a strong sales quarter and shift to a line of credit during slower months. The key is staying intentional about which product serves which purpose, and reviewing that alignment regularly.

Our perspective at Capital for Business is straightforward: the best financing product is the one that fits your cash flow, supports your goals, and has a clear payoff path. Approval is the starting line, not the finish line.

Explore tailored funding solutions with Capital for Business

If you have read this far, you are already thinking more strategically about financing than most small business owners do. The next step is finding the right product for your specific situation, not just the first one that approves you.

At Capital for Business, we have been matching small business owners with the right funding since 2009. Whether you need working capital, equipment financing, or a merchant cash advance, we offer fast, transparent options built for real businesses. Explore easy small business loans to compare what fits your needs, or take a closer look at equipment financing if you are ready to invest in assets that grow your capacity. We work quickly, explain our terms clearly, and focus on solutions that actually serve your business, not just your approval odds.

Frequently asked questions

What is the main difference between alternative and traditional financing?

Alternative financing uses non-bank lenders with faster processes and often higher approval rates, while traditional financing relies on banks and credit unions with stricter criteria. Approval rates are higher at online lenders than at large banks, making alternative options more accessible for many small businesses.

Are alternative financing options safe for my business?

Most options are safe if you understand the terms and avoid high-cost, short-term products without a clear repayment plan. Experts warn against cycles where one advance is used to repay another, as this creates compounding cost risk.

How quickly can I access funding from alternative lenders?

Alternative options offer faster turnaround than traditional banks, with funding often available within 24 to 72 hours of approval, and some products funding the same day.

Will alternative financing impact my business credit score?

It depends on the product and lender. Alternative options affect credit differently depending on how the lender reports to business credit bureaus, so always ask about reporting practices before signing.