TL;DR:

- UCC filings publicly notify lenders of secured interests in business assets and influence future financing options. They do not create debt or security interests, but proper management ensures clear asset control and credit standing. Regularly monitoring and promptly terminating outdated filings can protect your business’s growth potential and borrowing capacity.

If you have ever applied for a small business loan, a lender may have placed a UCC filing on your assets without fully explaining what it means. Understanding what is a UCC filing is not just useful legal knowledge. It directly affects your ability to secure future financing, manage your business credit, and protect your assets. Many business owners sign loan documents that include UCC filings without realizing the long-term implications. This guide breaks down the UCC filing definition, explains how it works in practice, and shows you how to use it to your advantage when growing your business.

Table of Contents

- Key takeaways

- What is a UCC filing and how does it work

- Why UCC filings matter when you seek financing

- How to file, amend, or terminate a UCC filing

- Common misconceptions about UCC filings

- How UCC filings affect your credit and future borrowing

- My perspective on UCC filings and business growth

- How Capitalforbusiness can support your financing needs

- FAQ

Key takeaways

| Point | Details |

|---|---|

| UCC filings are public notice | A UCC-1 form tells the public a lender has a secured interest in your business assets. |

| Filing perfects, not creates, a lien | The security agreement creates the lien; the UCC filing makes it legally enforceable against others. |

| Lingering filings block new loans | Unpaid or unterminated UCC filings can prevent you from getting additional financing. |

| Digital filing is now standard | Most states process UCC-1 forms through online portals, with some eliminating paper submissions entirely. |

| Monitor your UCC filings actively | Regularly reviewing your filings helps you catch errors and remove outdated liens before they hurt your credit. |

What is a UCC filing and how does it work

A UCC-1 financing statement is a standardized legal form filed with a state's Secretary of State office. Its purpose is to publicly announce that a creditor holds a security interest in a borrower's personal property. Think of it as the lender placing a formal flag on your business assets so that anyone searching the public record can see the claim exists.

Here is what the UCC filing does not do: it does not create the debt, and it does not create the security interest itself. The security interest is created by a separate, private security agreement signed between the lender and the borrower. The UCC-1 simply perfects that security interest, which means it makes the lender's claim legally superior to other creditors who might file later.

This distinction matters more than most business owners realize. If a lender fails to file a UCC-1 after you sign a security agreement, their claim on your collateral may be subordinate to any other secured party that files first. The filing race is real. Lenders know this, which is why they typically file the UCC-1 within days of closing a loan.

Common types of collateral covered by UCC filings include:

- Accounts receivable and future invoices

- Inventory and raw materials

- Equipment, machinery, and vehicles

- Furniture and fixtures

- Intellectual property in some cases

- Business bank account balances

Pro Tip: Before signing any loan agreement, ask the lender to walk you through exactly what assets they intend to list as collateral. A specific collateral description protects your other assets, while a blanket lien covers everything your business owns.

Understanding collateral types and descriptions is one of the most practical things you can do before entering any secured loan agreement.

Why UCC filings matter when you seek financing

The importance of UCC filings goes beyond the moment you sign a loan. Every active UCC filing on your business is visible to every lender who searches your name. That visibility shapes how lenders view your creditworthiness and your ability to offer assets as security for future loans.

Here is the priority system lenders rely on:

- First to file wins. When multiple lenders hold security interests in the same collateral, the one who filed first has the highest priority claim. If you default, that lender gets paid before the others. This is why lenders move fast to file after closing.

- Blanket liens limit your options. Some lenders file UCC liens that cover all of your business assets. If that happens, a future lender may refuse to extend credit because your assets are already encumbered. You have less collateral left to offer.

- Your credit report tells the story. UCC filings appear on business credit reports. While they generally do not lower your business credit score directly, having too many active filings signals to lenders that your assets are heavily pledged.

- Targeted collateral descriptions preserve flexibility. When a lender agrees to list only specific assets as collateral rather than your entire business, your remaining assets stay available for future financing. This is a negotiable point worth fighting for.

Pro Tip: Read the collateral description in any UCC filing before you agree to it. Ask your lender to narrow it to the specific assets tied to the loan rather than accepting a blanket lien covering all assets now owned or hereafter acquired.

Before signing a secured loan, reviewing the considerations for small business loans can help you spot terms that might limit your financing options down the road.

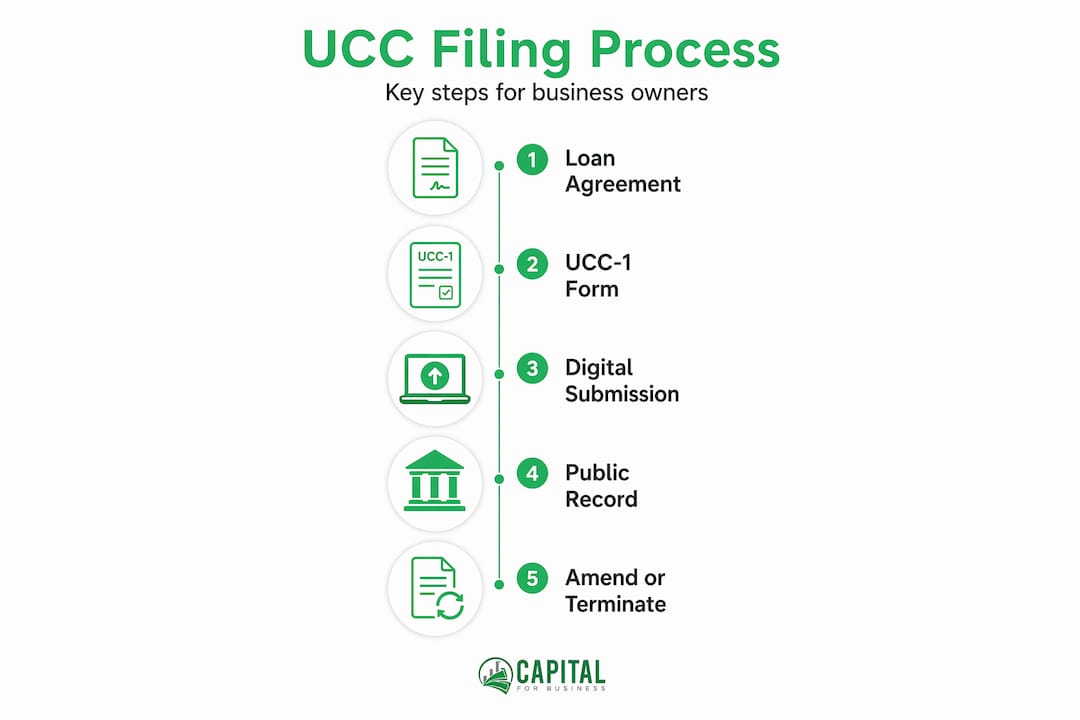

How to file, amend, or terminate a UCC filing

The UCC filing process is straightforward once you understand the forms involved and where to send them. Whether you are a lender handling this on behalf of a borrower or a business owner who needs to terminate an old filing, the steps below apply.

The UCC-1 filing process

The UCC-1 form is the initial filing that creates the public record. It must be filed with the Secretary of State in the state where the debtor is located, which is typically where the business is registered. The form requires the full legal names of the debtor and the secured party, along with a description of the collateral being pledged.

The filing process has shifted heavily toward digital portals. Texas, for example, discontinued paper filings as of August 29, 2025, and now requires submission through the Secretary of State's online portal. Most other states have followed a similar path. Filing fees vary by state but are typically modest, ranging from $10 to $25 per filing.

For business owners navigating digital submissions for the first time, understanding business contract notarization online can provide helpful context on how legal documents are now processed through digital channels.

UCC-3 amendments and terminations

Once a UCC-1 is filed, a UCC-3 form handles all subsequent changes. This includes:

- Amendments to update collateral descriptions or change party information

- Continuations to extend the filing beyond its standard five-year term

- Terminations to remove the filing after the loan is repaid

| Form | Purpose | Who Files It |

|---|---|---|

| UCC-1 | Initial financing statement | Secured party (lender) |

| UCC-3 Amendment | Updates to existing filing | Secured party or authorized debtor |

| UCC-3 Continuation | Extends filing past 5 years | Secured party |

| UCC-3 Termination | Removes filing after payoff | Secured party or debtor with authorization |

Common mistakes to avoid during the filing process include misspelling the debtor's legal name (which can render the filing legally ineffective), filing in the wrong jurisdiction, and failing to file a termination after payoff.

Common misconceptions about UCC filings

Several misunderstandings about UCC filings cost business owners time, money, and financing opportunities. Addressing them directly can save you real problems.

The filing creates the lien. This is the most common mistake. Most business owners believe the UCC filing creates the lien. It does not. The security agreement you sign with your lender creates the legal right. The UCC-1 simply puts the public on notice that the right exists. Without the security agreement, the filing has no legal force.

Paying off the loan removes the filing automatically. It does not. Once a UCC-1 is filed, it stays on public record until someone actively files a termination statement. Creditors often fail to file terminations after loans are repaid, leaving ghost liens on your assets. Those ghost liens can mislead future lenders into thinking your assets are still encumbered.

Common pitfalls to watch for include:

- Assuming your lender will automatically terminate the filing after payoff. They might not.

- Failing to check your business credit report for outdated UCC liens before applying for new financing.

- Accepting a blanket lien when a specific collateral description would have protected your other assets.

- Including personal identifying information such as a Social Security number in UCC filings. These are public documents, and including sensitive data creates identity theft risks.

Pro Tip: After you repay any secured loan, send a written request to your lender asking them to file a UCC-3 termination statement within 30 days. If they do not, you can file one yourself if you have written authorization or follow your state's process for debtor-initiated terminations.

How UCC filings affect your credit and future borrowing

Many business owners are surprised to learn that UCC filings appear on their business credit reports. The impact is more nuanced than a simple score reduction, but it is still worth managing carefully.

Here is how lenders actually use UCC information when evaluating your business:

- They run a UCC search before approving your application. UCC searches allow lenders to assess which of your assets already have claims against them. If your equipment, receivables, and inventory are all listed in existing UCC filings, a new lender has little to secure their loan against.

- Multiple active filings signal overleveraged assets. Even if your credit score is strong, seeing five active UCC liens can make a lender hesitant. It suggests your business has borrowed heavily against its assets, which raises the risk profile of any new loan.

- Outdated filings hurt more than you think. A lender looking at your report does not automatically know a UCC filing is from a loan you already paid off. They see an active lien and treat it as current until a termination is filed. Regularly reviewing your business credit reports for UCC filings can prevent surprises during new financing attempts.

- Your leverage capacity depends on clean records. Understanding how lenders evaluate your 5 Cs of credit, particularly collateral and capital, helps you see why clean UCC records matter. A business with no unnecessary liens has more asset leverage available for future financing.

Reviewing your standing against the 5 Cs of credit before applying for any loan puts you in a much stronger negotiating position when UCC filings come up.

My perspective on UCC filings and business growth

I have worked with thousands of business owners over the years, and the pattern I keep seeing is the same. They sign loan documents in good faith, get the capital they need, and then completely forget about the UCC filing sitting on their assets. Years later, when they need new financing, they run into problems they never anticipated.

What I have learned from this is that the UCC filing process rewards the business owners who pay attention to it. The gap between the security agreement and the UCC-1 filing is not just a legal technicality. It is the difference between thinking you understand your obligations and actually knowing what is on public record about your business.

The hidden cost of lingering UCC liens is something I want business owners to take seriously. I have seen situations where a lender repaid the original loan, refused to file a termination, and left the borrower scrambling to get authorization to do it themselves. That delay cost the business owner a favorable loan offer from another lender who moved on to the next applicant.

My strongest advice is this: negotiate the collateral description before you sign, not after. Effective UCC filings use targeted collateral descriptions rather than blanket liens. Lenders will often push for blanket coverage because it protects them more. But you have the right to negotiate, and a good lender will work with you on this.

Work with lenders who explain your UCC filings clearly. Work with lenders who file terminations promptly. And always monitor your business credit for UCC activity. It is one of the few areas of business finance where staying proactive costs very little and can save you a great deal.

— Capital

How Capitalforbusiness can support your financing needs

At Capitalforbusiness, every loan product we offer comes with clear, transparent terms about how UCC filings work and what collateral is being secured. Since 2009, we have helped business owners across hundreds of industries access working capital, equipment financing, and business lines of credit without the runaround they get from traditional banks.

Whether you are exploring small business loan options for the first time or looking for business funding solutions to fuel your next growth phase, Capitalforbusiness guides you through every step of the process. That includes explaining any UCC filings attached to your loan and making sure terminations are handled properly when your loan is paid off.

Our application process is fast, our team is knowledgeable, and our goal is to get you funded with terms you understand. If your credit is not perfect, we offer products designed for that situation too. Reach out to Capitalforbusiness today and find out which financing option fits where your business is right now.

FAQ

What does a UCC filing mean for my business?

A UCC filing is a public record showing that a lender has a secured interest in your business assets. It does not create debt but tells other lenders and creditors that specific collateral is already pledged.

How long does a UCC filing stay on record?

A UCC-1 filing stays on public record for five years. After that, it lapses unless the secured party files a UCC-3 continuation. A termination statement can remove it earlier once the loan is repaid.

Does a UCC filing lower my business credit score?

UCC filings appear on business credit reports but generally do not lower your score directly. However, too many active filings can make lenders reluctant to extend new credit based on perceived asset encumbrance.

What is the UCC filing process for a small business loan?

After the loan closes, the lender files a UCC-1 form with the Secretary of State in your state. Most states now process these through digital portals. The filing lists the debtor, the secured party, and the collateral description.

Can I remove a UCC lien after paying off my loan?

Yes. Once your loan is repaid, the lender should file a UCC-3 termination statement. If they do not act within a reasonable time, you can request written authorization and file one yourself following your state's process for debtor-initiated terminations.