TL;DR:

- Most small business owners overestimate their assets' value for loan collateral, which can lead to reduced borrowing capacity. Lenders use haircut adjustments and loan-to-value ratios to mitigate risk, often discounting asset worth significantly before approving loans. Understanding legal procedures like UCC filings and comparing different loan programs helps entrepreneurs maximize borrowing and avoid costly pitfalls.

Most small business owners assume their assets are worth what the market says they are. They are wrong, and that misunderstanding can quietly sink a loan application before it even reaches underwriting. Lenders routinely discount collateral values by 20 to 40 percent below fair market value, sometimes more, depending on the asset type and how quickly they could sell it if your business defaulted. Knowing why this happens, how to prepare for it, and how different loan programs treat collateral differently gives you a real edge when you walk into a lender's office or fill out an online application.

Table of Contents

- What is collateral and how does it secure a business loan?

- How lenders value collateral: Haircuts, volatility, and loan-to-value ratios

- Securing your assets: UCC filings, liens, and avoiding common pitfalls

- Collateral requirements: Comparing SBA, conventional, and alternative business loans

- Applying collateral knowledge: Strategies for maximizing your loan and avoiding traps

- The uncomfortable truth about collateral: What small business owners need to hear

- Find the right financing solution with Capital For Business

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Collateral is discounted | Lenders rarely value collateral at full market price; expect significant haircuts. |

| Securing assets legally matters | Accurate UCC filings and liens are crucial to maintaining lending eligibility. |

| Loan requirements vary | SBA programs are often more flexible than banks, and unsecured loans are an option with higher costs. |

| Asset type influences value | Advance rates differ dramatically by asset type—know which assets maximize your borrowing power. |

| Preparation improves outcomes | Strategically presenting and documenting assets can increase loan amounts and reduce risks. |

What is collateral and how does it secure a business loan?

Collateral is an asset you pledge to a lender as security for a loan. If you stop making payments, the lender has the legal right to seize and sell that asset to recover what they are owed. It is a straightforward concept, but the rules governing which assets qualify and how they are valued are anything but simple.

Understanding business vs personal loans is a useful starting point because the collateral rules differ significantly. Business loans may accept commercial real estate, equipment, and inventory, while personal loans typically rely on home equity or vehicles. The commercial loan types available to you will also shape which assets are acceptable.

Here are the most common asset types lenders accept as collateral:

- Real estate: Commercial property and sometimes personal real estate are the most valued assets. Lenders can usually recover value quickly through a sale.

- Equipment: Machinery, vehicles, and technology hardware qualify, though older or highly specialized equipment loses value fast.

- Inventory: Finished goods and raw materials are accepted but heavily discounted because demand can be unpredictable.

- Accounts receivable (A/R): Outstanding invoices from creditworthy customers are solid collateral, especially for businesses with consistent billing cycles.

- Cash and cash equivalents: Savings accounts, certificates of deposit, and money market funds are the most liquid and least discounted assets.

- Public stock: Publicly traded shares can secure a loan, and public stock as collateral carries specific advantages and risks tied to market volatility.

Lenders assess collateral value through a process called the loan-to-value (LTV) ratio, which compares the loan amount to the appraised value of the pledged asset. According to typical LTV advance rates, lenders generally advance 60 to 90 percent on real estate, 40 to 80 percent on equipment, 25 to 60 percent on inventory, and 60 to 85 percent on accounts receivable. Understanding these ranges matters because they directly determine your maximum borrowing capacity.

Collateral plays a psychological and financial role in the loan process. It lowers the lender's risk, which usually translates into lower interest rates for you. It also gives lenders a reason to approve business loans for growth when other factors like credit score or time in business are not perfect. For startup loan options, collateral can be especially important because startups lack the operating history that banks prefer.

With these basics covered, let's dig into how lenders actually value collateral assets and why your real estate or inventory might be worth less to them than you think.

How lenders value collateral: Haircuts, volatility, and loan-to-value ratios

The term "haircut" in lending refers to the reduction lenders apply to an asset's market value before calculating how much they will loan against it. It is not a punishment. It is risk management. Lenders must account for the possibility that if they need to liquidate your asset quickly, they will not get full market price.

According to Investopedia's definition of haircut, liquidation value for equipment typically lands at 60 to 80 percent of fair market value (FMV), reflecting the reality that distressed sales rarely bring top dollar. The haircut grows larger for assets that are harder to sell, more volatile in value, or in poor condition.

Three primary factors drive how large a haircut a lender applies:

- Liquidity: How quickly and easily can the asset be sold? Real estate in a strong market sells reasonably fast. Custom manufacturing equipment in a niche industry might sit unsold for months.

- Volatility: Does the asset's value fluctuate? Public stock prices move daily. Commercial real estate is more stable but not immune to downturns.

- Condition: Well-maintained equipment, updated properties, and accurate inventory records all reduce the discount. Neglected assets get steeper haircuts.

Here is a practical table showing typical LTV advance rates by asset class, based on standard lender benchmarks:

| Asset type | Typical LTV / advance rate | Key driver of discount |

|---|---|---|

| Commercial real estate | 60 to 90% | Market conditions, location |

| Equipment | 40 to 80% | Age, condition, liquidity |

| Inventory | 25 to 60% | Turnover rate, perishability |

| Accounts receivable | 60 to 85% | Customer creditworthiness |

| Cash / CDs | 90 to 100% | Near-zero risk |

| Public stock | 50 to 70% | Price volatility |

"Lenders do not lend against what your assets are worth today. They lend against what those assets would realistically sell for under pressure, often in a matter of weeks. That number is almost always lower than you expect."

Pro Tip: Before your loan appointment, have equipment appraised by a third party and gather maintenance records. Clean, documented, well-maintained assets consistently earn higher advance rates because they signal lower liquidation risk to underwriters.

The practical implication here is significant. If you own a piece of equipment appraised at $200,000 but the lender applies a 50 percent haircut, they are working from a collateral value of $100,000. At an 80 percent LTV, your maximum loan against that asset is $80,000, not $200,000. Running these numbers before you apply prevents frustrating surprises at closing.

Once you know how collateral is valued, it is essential to understand the paperwork and legal steps that make your collateral count in the eyes of lenders.

Securing your assets: UCC filings, liens, and avoiding common pitfalls

Pledging collateral is not just a handshake agreement. It requires legal documentation that formally establishes the lender's claim on your assets. Without proper legal perfection, a lender's security interest may be unenforceable, which is a risk no serious lender will accept.

The primary legal tool in the United States is the UCC-1 financing statement, filed under the Uniform Commercial Code. A UCC-1 filing publicly records that a lender holds a security interest in specific assets. According to guidance on UCC filing mistakes, the filing must include the exact legal debtor name, be filed in the correct state, and be renewed via a continuation statement every five years or it lapses automatically.

Common mistakes that can invalidate your collateral protection include:

- Incorrect debtor name: Even a minor variation from the legal business name on file with the state can render the UCC-1 ineffective against third-party creditors. This is the most frequent and costly error.

- Wrong filing state: UCC filings must be made in the state where the debtor is organized, not where the collateral is located. Many filers confuse these.

- Overly vague collateral descriptions: Descriptions like "all assets" may seem comprehensive but can be challenged. Specific descriptions reduce legal ambiguity.

- Missing the five-year renewal: A lapsed UCC filing means the lender loses priority to other creditors, even if the original loan is still active.

- Filing in the wrong office: Different states have different rules about which office handles UCC filings. Some require filings at the county level for real estate-related collateral.

Pro Tip: Set a calendar reminder the moment your UCC-1 is filed. Mark the date five years out and schedule a continuation filing at least 60 days before expiration. A lapsed filing can seriously complicate refinancing, selling your business, or taking on additional credit.

Liens are closely related to UCC filings but apply more broadly. A lien is a legal claim against an asset. It can be voluntary, as when you pledge property to secure a loan, or involuntary, as when a tax authority or contractor places a lien due to unpaid obligations. Existing liens on your assets can reduce or eliminate their value as collateral for a new loan because they signal that other creditors already have priority claims.

Before applying for any secured loan, pull a lien search on your primary assets. Unresolved liens from past debts, tax disputes, or contractor judgments can surface and block approvals even when the underlying asset has significant value. Addressing these issues before you apply saves time and prevents last-minute deal failures.

With your collateral secured, let's compare how different loan programs use assets and why SBA and bank loans treat collateral very differently.

Collateral requirements: Comparing SBA, conventional, and alternative business loans

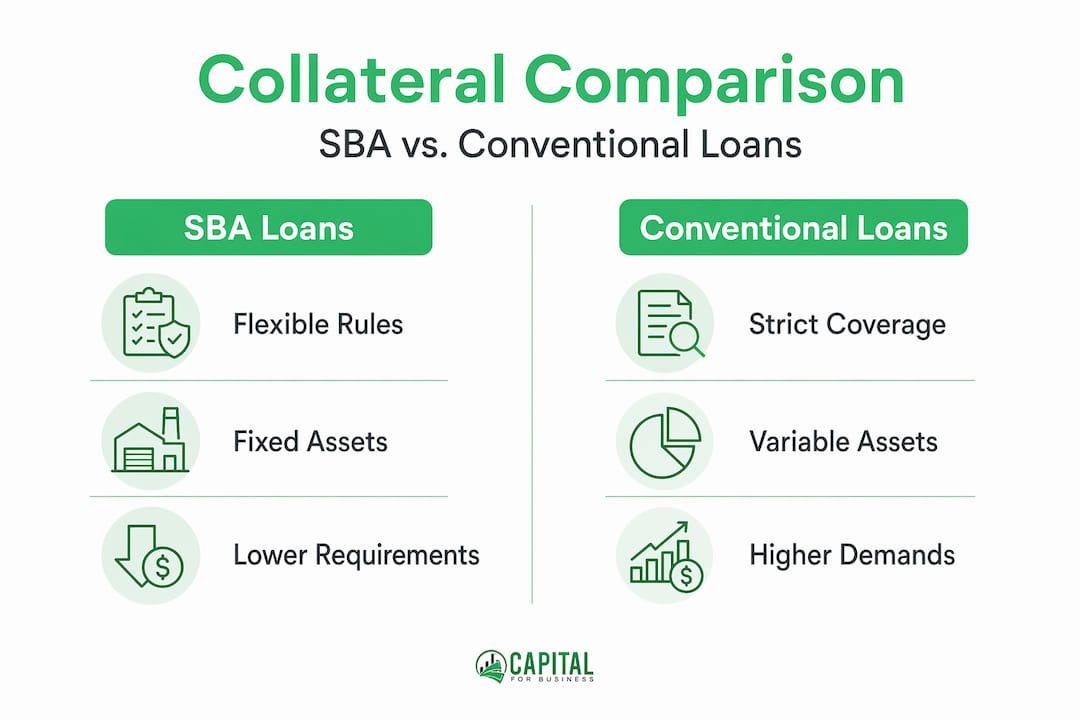

Not all business loan programs view collateral the same way. The rules vary considerably depending on whether you are applying for an SBA loan, a conventional bank loan, or an alternative financing product.

According to the SBA's 504 loan program, fixed assets like commercial real estate and equipment serve as the primary collateral, and the program is specifically designed to help businesses purchase long-term assets. SBA loans generally use cash flow as the primary repayment indicator and view collateral as a secondary support, which makes them more accessible for businesses with solid revenue but limited asset holdings.

Conventional banks, by contrast, often require stricter collateral coverage, sometimes demanding 100 to 120 percent of the loan amount in collateral value before advancing funds. This approach protects the bank heavily but can exclude businesses that have strong cash flow but limited hard assets.

Here is a comparison table of the three main lending categories:

| Loan type | Collateral requirement | Coverage ratio | Flexibility |

|---|---|---|---|

| SBA loans | Business and sometimes personal assets | Moderate (cash flow primary) | Higher flexibility |

| Conventional bank loans | Real estate, equipment, A/R | 100 to 120% of loan value | Lower flexibility |

| Alternative / online lenders | Varies; often a blanket lien or revenue-based | Flexible or none | Highest flexibility |

Pros and cons of each option:

- SBA loans: Lower rates and longer terms, but slower approval process and more documentation required. Check the latest SBA loan updates before applying.

- Conventional bank loans: Best rates for borrowers who qualify, but rigid collateral demands exclude many small businesses.

- Alternative loans and MCAs: Faster approval and more flexibility. Review the MARC loans vs bank loans comparison to understand when these products make sense. Interest rates are higher, but access is far easier.

- Unsecured loans: No collateral required, but they typically carry higher rates and shorter terms. The unsecured loan guide explains the qualifying criteria in detail, and the unsecured business credit line is worth evaluating for working capital needs.

Always review loan consideration tips before committing to any program. The lowest rate is not always the best deal when you factor in collateral risk, term length, and prepayment penalties.

Knowing the differences, the final step is applying this knowledge strategically to maximize your borrowing power and minimize risk.

Applying collateral knowledge: Strategies for maximizing your loan and avoiding traps

Understanding how collateral is valued is only useful if you apply that knowledge practically. Here is how to position your assets for the strongest possible loan terms.

Before you apply, do this:

- Get a professional appraisal for real estate and major equipment. Lender-ordered appraisals tend to be conservative. Having your own appraisal in hand gives you a starting point for negotiation.

- Organize maintenance logs, warranties, and purchase records for all equipment. Documented asset history consistently leads to better advance rates.

- Clean up your accounts receivable. Remove invoices older than 90 days because most lenders exclude them from eligible collateral. A tightly managed A/R ledger is far more attractive than a list padded with aging debt.

- Check for liens. Run lien searches on all assets you plan to pledge before the lender does. Surprises discovered late in the underwriting process can kill deals.

During negotiations:

- Ask the lender directly how they arrived at their collateral valuation. If they use an internal formula, knowing it helps you present assets in the most favorable light.

- Negotiate the haircut on equipment by providing evidence of high resale demand for your specific asset category. Industry-specific auction results and dealer quotes strengthen your case.

- Ask whether substitution of collateral is permitted. Some loan agreements allow you to swap one asset for another over the loan term, which gives you flexibility as your business evolves.

- According to haircut valuation standards, liquidation values typically run 60 to 80 percent of FMV, but well-documented and liquid assets can push toward the top of that range. Presentation matters.

Protecting yourself legally:

- Read the lien terms carefully. A blanket lien grants the lender a claim on all business assets, including future ones. This can restrict your ability to take on additional financing later.

- Understand what triggers default. Some agreements include clauses that declare default if your collateral value drops below a certain threshold, even if you are current on payments.

- Consider whether pledging personal real estate is necessary. Personal guarantees backed by your home carry serious risk. Explore whether business assets alone can satisfy the lender's requirements before agreeing to personal collateral.

When unsecured or hybrid options make sense:

- If your collateral falls short of what a bank requires but your revenue is strong, merchant cash advances or revenue-based financing may be faster and more practical.

- Hybrid loans that combine a smaller secured portion with an unsecured component can give you access to more capital without overexposing your assets.

- Lines of credit, especially unsecured business lines, are useful for covering short-term gaps without putting fixed assets at risk.

Now that you have a toolbox for navigating collateral, let's look at what most guides miss: practical realities, tough tradeoffs, and what actually works for small business owners.

The uncomfortable truth about collateral: What small business owners need to hear

Here is something most financing guides will not tell you plainly: collateral is not your strongest card. Cash flow is. Lenders care more about whether you can make your monthly payments than whether they could liquidate your warehouse if you default. Collateral is a backup plan for them. It should not be your primary pitch.

We have worked with thousands of business owners since 2009, and the pattern is consistent. Owners who walk in leading with their assets often do worse than owners who walk in leading with their revenue story. A profitable business with modest collateral frequently gets better terms than a cash-strapped business sitting on a pile of equipment. The numbers behind the business matter more than the stuff inside it.

The second hard truth is that most business owners significantly overestimate what their assets are worth to a lender. A $500,000 commercial property in a slow market with an existing mortgage does not translate to $500,000 in collateral. After the existing lien, the haircut, and the LTV ratio, you might be looking at $80,000 to $120,000 in usable collateral value. That gap between perceived value and actual borrowing power is where a lot of loan applications fall apart.

Negotiation is also more available than most people realize. Lenders present their initial LTV ratios as fixed, but they are often starting positions. If you come with documentation, clean asset history, and a clear business case, there is room to move. Most owners never ask. The ones who do often secure meaningfully better terms.

Finally, unsecured loans are not a last resort. For businesses with strong cash flow, an unsecured loan keeps your assets free from liens, preserves your flexibility, and avoids the documentation burden that comes with pledging collateral. Yes, the rate is higher. But the total cost of capital, when you factor in the time, legal fees, and risk of a blanket lien, can make an unsecured product the smarter choice for the right business at the right stage.

The businesses that navigate collateral best are the ones that treat it as one variable in a larger equation, not the whole answer. Know your numbers, know your options, and negotiate from a position of information rather than desperation.

Find the right financing solution with Capital For Business

Understanding collateral is a critical step, but knowledge alone does not fund your growth. You need a lending partner who works with your situation, not against it.

Capital For Business has helped business owners across North America access the financing they need since 2009, from secured loans backed by real estate and equipment to flexible unsecured options for businesses that need capital without pledging assets. Whether you are looking for a straightforward secured loan or something more customized, we have the product lineup and the experience to match you with the right solution. Explore your easy business loan options to see what fits your needs, browse our full business funding solutions, or go ahead and apply for funding today to start the conversation.

Frequently asked questions

What assets qualify as collateral for a small business loan?

Common collateral assets include real estate, equipment, inventory, accounts receivable, cash, and publicly traded stock. Typical advance rates vary by asset type based on liquidity and risk.

How much can I borrow against my collateral?

Most lenders advance different rates depending on the asset: roughly 60 to 90 percent for real estate, 40 to 80 percent for equipment, 25 to 60 percent for inventory, and 60 to 85 percent for accounts receivable.

What legal steps protect my collateral in a loan?

A UCC-1 perfects the lender's security interest in your assets; it must be accurately completed, filed in the correct state, and renewed every five years to remain enforceable.

Can I get approved without collateral?

Yes. Unsecured loans are available but typically carry higher interest rates and require stronger cash flow or a solid credit history to qualify.

How do SBA and bank loans differ in their collateral requirements?

SBA loans prioritize cash flow and are generally more flexible on collateral, while conventional banks often require stricter coverage ratios of 100 to 120 percent of the loan value.