TL;DR:

- Commercial lending is accessible to small businesses, not just large corporations.

- Lenders evaluate applications using the 5 Cs: character, capacity, capital, collateral, and conditions.

- The market offers various options like bank loans, SBA loans, online lenders, and lines of credit.

Many small business owners assume commercial lending is reserved for large corporations with deep pockets and long credit histories. That assumption is costing them real growth. Small business lending continues to increase heading into 2026, and SBA 7(a) loan volume recently hit a record high, signaling that lenders are actively looking to fund businesses of all sizes. Whether you need working capital to cover payroll, equipment to take on bigger contracts, or a credit line to manage cash flow gaps, commercial lending offers a path forward. This guide breaks down what commercial lending is, what types of products exist, how lenders evaluate your application, and what pitfalls to avoid so you can walk into your next loan conversation with confidence.

Table of Contents

- What is commercial lending: Basics every business owner needs to know

- Types of commercial lending options for small businesses

- How lenders evaluate your business: Key criteria and approval process

- Common pitfalls, alternatives, and the future of commercial lending

- Our perspective: What most guides miss about commercial lending

- Next steps: Explore tailored business funding solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Broad lending options | Small businesses in the U.S. and Canada have access to a growing range of commercial loan types. |

| Approval factors matter | Lenders focus on cash flow, credit, collateral, and business purpose when evaluating applications. |

| Alternatives are rising | Fintech and online lenders are quickly expanding, offering faster and flexible loan options. |

| Avoid common mistakes | Preparing documents and understanding requirements can prevent loan application rejection. |

| Expert advice helps | Leverage insights from credible guides to make informed commercial lending decisions. |

What is commercial lending: Basics every business owner needs to know

Commercial lending refers to the process by which financial institutions, including banks, credit unions, and alternative lenders, provide financing to businesses rather than individuals. Unlike personal loans, which are tied to your individual credit and personal income, commercial loans are evaluated based on the financial health and purpose of your business. Understanding this distinction is foundational, and you can read more about business vs personal loans to see exactly how the two differ.

One of the most persistent myths is that commercial lending is only accessible to established corporations. In reality, small businesses represent a significant share of commercial loan activity across the U.S. and Canada. Community banks, online lenders, and government-backed programs all offer products specifically designed for smaller operations. The key is knowing what lenders look for and how to present your business accordingly.

Lenders evaluate borrowers based on financial statements, cash flow, and collateral, along with credit history and the stated purpose of the loan. These factors collectively determine your risk profile. A strong application addresses each one clearly and honestly.

The five most common evaluation criteria lenders use are often referred to as the 5 Cs of credit:

- Character: Your credit history and reputation as a borrower

- Capacity: Your ability to repay based on current cash flow

- Capital: The money you have already invested in your business

- Collateral: Assets that can secure the loan if you default

- Conditions: The purpose of the loan and broader economic context

Familiarizing yourself with the 5 Cs of credit before you apply gives you a significant advantage. You will know where your application is strong and where it needs work before a lender ever reviews it.

"Commercial lending is not just about getting approved. It is about presenting your business as a reliable, purposeful borrower. Lenders want to say yes. Your job is to make that easy for them."

Pro Tip: Pull your business credit report and review your most recent two years of financial statements before starting any loan application. Identifying gaps early gives you time to address them rather than scrambling after a rejection.

The commercial lending process also involves a formal underwriting review, where lenders verify the information you submit and assess overall risk. This stage can take anywhere from a few days with alternative lenders to several weeks with traditional banks. Knowing this timeline helps you plan your financing needs well in advance rather than applying under pressure.

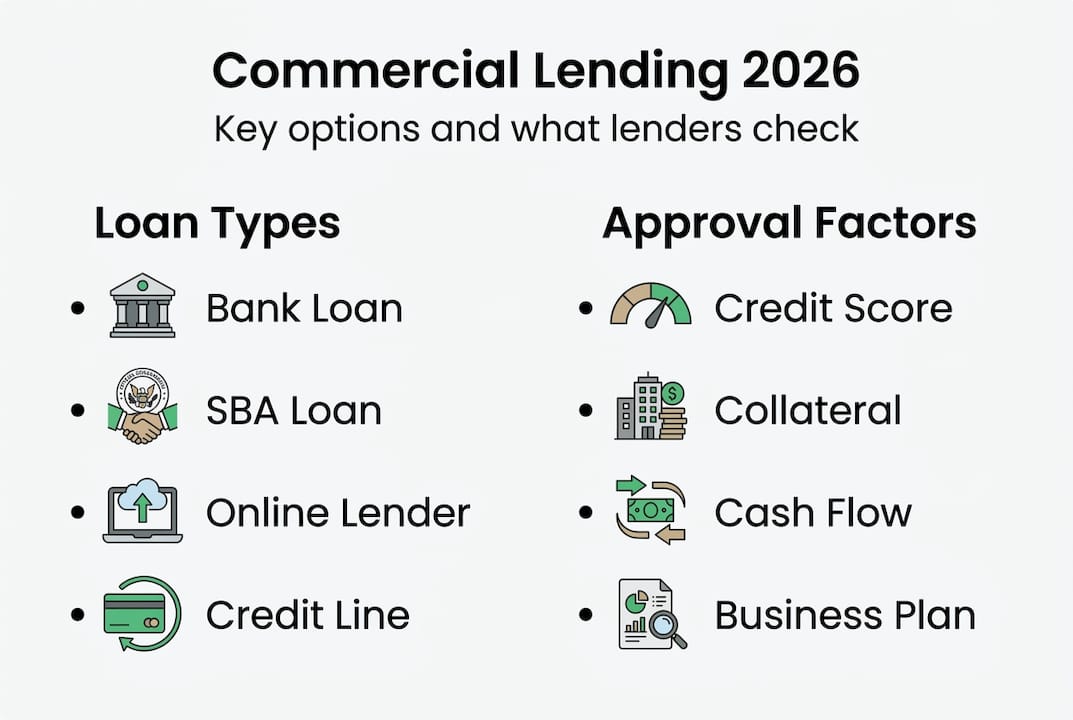

Types of commercial lending options for small businesses

With commercial lending defined, it is essential to know what types of loans and products are available to your business. The market offers far more variety than most owners realize, and the right product depends on your specific goals, timeline, and financial profile.

Here are the primary categories of commercial lending products available to small businesses:

- Traditional bank loans: Offered by large national banks and regional institutions. These typically come with competitive interest rates but stricter qualification requirements and longer processing times.

- SBA-backed loans: Loans partially guaranteed by the U.S. Small Business Administration. The SBA 7(a) program is the most popular, offering up to $5 million with flexible terms. These are well-suited for businesses that may not qualify for conventional bank financing.

- Community and small bank loans: Smaller institutions often have more flexibility and a stronger relationship-based approach to lending. They tend to understand local market conditions better.

- Alternative and online lenders: Fintech platforms and non-bank lenders offer faster approvals and more flexible criteria. They are especially useful for businesses that need capital quickly or have limited credit history.

- Business lines of credit: A revolving credit facility that lets you draw funds as needed, repay, and draw again. Ideal for managing cash flow or covering short-term expenses.

- Equipment financing: A loan or lease specifically for purchasing business equipment, where the equipment itself often serves as collateral.

Approval rates vary significantly depending on the lender type. Small banks approve 57% of small business loan applications, while big banks approve only 13.2%, and alternative lenders fall in between at 42%. These numbers highlight why exploring multiple channels matters.

| Lender type | Approval rate | Typical speed | Best for |

|---|---|---|---|

| Small/community banks | 57% | 2 to 4 weeks | Relationship-based borrowers |

| Big banks | 13.2% | 4 to 8 weeks | Established businesses with strong financials |

| Alternative lenders | 42% | 1 to 5 days | Fast capital, flexible criteria |

| SBA-backed programs | Varies | 3 to 10 weeks | Underserved or growing businesses |

For Canadian business owners, the landscape is evolving quickly. Alternative lending in Canada now accounts for $2.17 billion and is growing at 26% year-over-year, reflecting rising demand for faster and more flexible financing outside traditional banks. You can explore business financing trends for a broader view of how the market is shifting in both countries.

For U.S. businesses, SBA and bank term loan programs remain strong options, particularly for businesses in growth phases or those recovering from economic disruption.

Pro Tip: If time is a factor, consider starting with a tech-driven or online lender while simultaneously building a relationship with a local community bank. This two-track approach gives you speed now and better terms later.

Understanding how technology in lending is reshaping the approval process can also help you choose the right platform and submit a stronger application.

How lenders evaluate your business: Key criteria and approval process

Once you have identified the right lending options, it is crucial to understand how lenders assess your application. The evaluation process is more structured than most people expect, and knowing what happens behind the scenes helps you prepare a stronger submission.

Lenders begin by reviewing your core financial documents. According to standard commercial loan criteria, the evaluation covers financial statements, cash flow records, credit history, collateral, and the stated business purpose. Each element tells a different part of your story as a borrower.

Here is what lenders typically request during the application process:

- Business and personal tax returns (last 2 to 3 years)

- Profit and loss statements

- Balance sheets

- Bank statements (last 3 to 6 months)

- Business plan or loan purpose statement

- Collateral documentation

- Legal documents such as business licenses, articles of incorporation, or lease agreements

The underwriting stage is where lenders verify all submitted information and calculate your debt service coverage ratio (DSCR). This ratio compares your net operating income to your total debt obligations. Most lenders want to see a DSCR of at least 1.25, meaning your business earns 25% more than it needs to cover its debt payments.

| Evaluation factor | What lenders look for | Minimum benchmark |

|---|---|---|

| Credit score | Personal and business credit | 650 or higher (varies) |

| DSCR | Net income vs. debt payments | 1.25 or above |

| Time in business | Operational history | 1 to 2 years minimum |

| Annual revenue | Demonstrated income | Varies by lender |

| Collateral value | Assets to secure the loan | Typically 80 to 100% of loan |

Collateral plays a significant role in commercial lending. Real estate, equipment, inventory, and accounts receivable are common forms of collateral. For small businesses without significant assets, personal guarantees are common, meaning you agree to be personally liable if the business cannot repay. This is a serious commitment and worth reviewing carefully before you sign.

Before committing to any loan agreement, review the loan signing considerations that often get overlooked. It is also worth understanding how accounting standards treat small business loans so you can manage your books accurately after funding.

Pro Tip: Prepare a one-page loan summary that outlines your business purpose, requested amount, repayment plan, and how the funds will generate revenue. Lenders see hundreds of applications. A clear, concise summary makes yours easier to approve.

Addressing common approval hurdles early is smart. If your credit score is below the threshold, spend three to six months improving it before applying. If your cash flow is inconsistent, consider a line of credit instead of a term loan, since it aligns better with variable income patterns.

Common pitfalls, alternatives, and the future of commercial lending

After mastering the approval process, it is equally important to avoid common errors and stay updated on industry changes. Even well-prepared business owners make avoidable mistakes that delay or derail their applications.

The most frequent mistakes include:

- Applying without reviewing your credit first: Surprises in your credit report can kill an application that would otherwise succeed.

- Borrowing more than you need: Overleveraging increases your monthly obligations and reduces financial flexibility.

- Ignoring loan terms in favor of speed: A fast approval with unfavorable terms can cost more in the long run than waiting for a better offer.

- Failing to compare lenders: Many business owners apply to one lender and accept the first offer without shopping around.

- Neglecting to update financial documents: Outdated financials raise red flags and slow the underwriting process.

"The alternative lending market is no longer a last resort. In many cases, it is the first choice for business owners who value speed, flexibility, and transparency over brand recognition."

Alternative lending is expanding rapidly in both Canada and the U.S., with Canada's market growing 26% year-over-year. This growth reflects a real shift in how business owners think about financing. Fintech platforms now offer AI-driven underwriting, same-day decisions, and products tailored to specific industries. For Canadian businesses, understanding Canadian SME credit options is increasingly important as the alternative market matures.

For startups or businesses with limited history, the startup loan guide outlines which products are realistically accessible and how to position your application effectively.

The future of commercial lending is being shaped by three key trends. First, automated underwriting is reducing approval times from weeks to hours. Second, open banking is allowing lenders to access real-time financial data with your permission, which speeds up verification. Third, alternative credit scoring models are giving businesses with thin credit files more access to capital than ever before. Staying informed about tech in small business lending helps you take advantage of these shifts rather than being caught off guard.

Pro Tip: Before applying anywhere, list your top three priorities: speed, cost, or flexibility. Use that list to filter your options. A business that needs cash in 48 hours should not be applying to a traditional bank.

Our perspective: What most guides miss about commercial lending

Most articles about commercial lending treat it as a checklist exercise. Gather documents, check your credit, submit an application. That framing misses something important: lending decisions are made by people and systems that operate within specific local and institutional contexts.

In our experience working with small businesses across the U.S. and Canada since 2009, we have seen that the local banking ecosystem matters enormously. A business in a rural community may find that a regional credit union offers better terms than any national bank or online platform, simply because that institution understands the local economy. Generic advice to "shop around" rarely captures this nuance.

We have also seen business owners dismiss alternative lenders too quickly, assuming higher rates mean worse deals. That is not always true. When you factor in the cost of waiting, lost contracts, and missed growth windows, a slightly higher rate from a fast lender can deliver better overall value than a lower rate that takes three months to materialize.

Conversely, we caution against treating alternative lending as a catch-all solution. Some platforms charge fees that are not immediately visible in the advertised rate. Reading the full loan agreement, not just the summary, is non-negotiable.

The 2026 financing trends show a market that is more accessible than ever, but also more complex. The best borrowers are not the ones with the highest credit scores. They are the ones who understand their options, know their numbers, and apply strategically.

Next steps: Explore tailored business funding solutions

Understanding commercial lending is only the first step. The real value comes from applying that knowledge to find the right funding for your specific situation.

At Capital for Business, we work with small business owners across the U.S. and Canada to match them with financing that fits their goals, not just their credit score. Whether you are exploring easy small business loans for the first time, need working capital to keep operations running smoothly, or are ready to invest in growth through an equipment financing guide, we have products designed for businesses at every stage. Since 2009, we have helped hundreds of businesses secure funding quickly and affordably. Reach out today to explore your options and take the next step toward your business goals.

Frequently asked questions

What documents do I need to apply for a commercial loan?

Most lenders require financial statements, tax returns, proof of cash flow, a business plan, and collateral details. Having these ready before you apply speeds up the underwriting process significantly.

Can startups qualify for commercial loans?

Startups can qualify, but lenders often require strong business plans, personal guarantees, or alternative products. SBA loans and fintech lenders offer startup-friendly options with varying approval requirements.

What are common reasons for loan application rejection?

Insufficient collateral, weak cash flow, poor credit history, and an unclear loan purpose are the most frequent reasons. Addressing these factors before applying, rather than after rejection, improves your odds considerably.

Is alternative lending safe for small businesses?

Alternative lending is safe when you vet the lender for legitimacy and review all terms carefully before signing. Canada's alternative market grew 26% year-over-year, reflecting strong and growing trust in these platforms.

How do approval rates differ for SBA loans compared to alternatives?

Small banks approve 57% of applications, big banks approve 13.2%, and alternative lenders approve 42%, making small banks and alternative lenders the stronger options for most small businesses.