TL;DR:

- Building a strong HVAC business credit profile requires establishing a separate legal entity, obtaining necessary identifiers, and managing timely payments. Consistent credit management and strategic application timing are crucial for accessing favorable financing options and expanding operations. Regular monitoring and proper operational practices help avoid common mistakes and enhance funding opportunities.

HVAC business credit essentials are the foundational financial practices, credit-building steps, and financing strategies that HVAC companies must implement to access funding and sustain operations. At their core, these essentials require a separate business credit profile built through an Employer Identification Number (EIN), a D-U-N-S number from Dun & Bradstreet, and a payment history reported to bureaus like Experian and Equifax. Without these building blocks in place, lenders treat your HVAC company as a financial unknown, regardless of how many service calls you run each week. Getting this right from the start separates contractors who grow from those who stay stuck.

What are HVAC business credit essentials?

Business credit, in the HVAC context, refers to your company's independent creditworthiness as a legal entity, separate from your personal finances. Lenders, suppliers, and equipment vendors all check this profile before extending terms or approving loans. A strong profile means better rates, higher limits, and faster approvals on the HVAC financing options that matter most to your operations.

Three credit bureaus track your business credit: Dun & Bradstreet, Experian Business, and Equifax Business. Each uses its own scoring model. Dun & Bradstreet uses the PAYDEX score, which runs from 0 to 100 and rewards early payment above all else. Experian Business uses the Intelliscore Plus, while Equifax Business issues its own commercial credit risk score.

Your business credit profile is not automatic. You must actively build it by registering your business, obtaining your EIN from the IRS, and applying for a D-U-N-S number through Dun & Bradstreet. From there, every vendor account, credit card, and loan you open either builds or damages the profile depending on how you manage payments.

How do you build a credible HVAC business credit profile?

Building business credit is a deliberate, step-by-step process that typically takes 6–12 months of consistent, on-time payments before lenders consider your profile fundable. That timeline is not a barrier. It is a roadmap. Follow these steps in order and you will reach fundable status faster than most contractors do.

-

Register your business as a legal entity. Form an LLC or corporation with your state. This separates your personal liability from business obligations and is the first signal to lenders that you are operating a real company.

-

Obtain your EIN from the IRS. Your EIN functions as your business's Social Security number. Every bank account, credit application, and tax filing uses it. Apply at IRS.gov at no cost.

-

Apply for a D-U-N-S number. Dun & Bradstreet issues this nine-digit identifier for free. Without it, your business does not exist in their database, and many lenders and vendors will not extend credit to you.

-

Open a dedicated business bank account. Use this account exclusively for business income and expenses. Mixing personal and business finances weakens your credit profile and removes liability protection. Keep them completely separate from day one.

-

Open Net-30 vendor accounts that report to bureaus. Suppliers like Uline, Grainger, and Quill offer Net-30 terms and report payment history to Dun & Bradstreet. These are your first tradelines. Pay them on time, every time.

-

Apply for a business credit card. Cards from issuers like American Express, Chase Ink, or Capital One Spark report to business credit bureaus and build your profile with every on-time payment. Use the card for recurring operational expenses and pay the balance in full monthly.

-

Monitor your credit reports regularly. Proactive credit monitoring at all three bureaus helps you catch reporting errors before they delay a loan application. Dispute inaccuracies immediately through each bureau's formal dispute process.

Pro Tip: Paying vendor invoices before their due date, not just on time, accelerates your PAYDEX score growth at Dun & Bradstreet. A score of 80 or above signals prompt payment and opens doors to better financing terms.

Which HVAC financing options fit your business best?

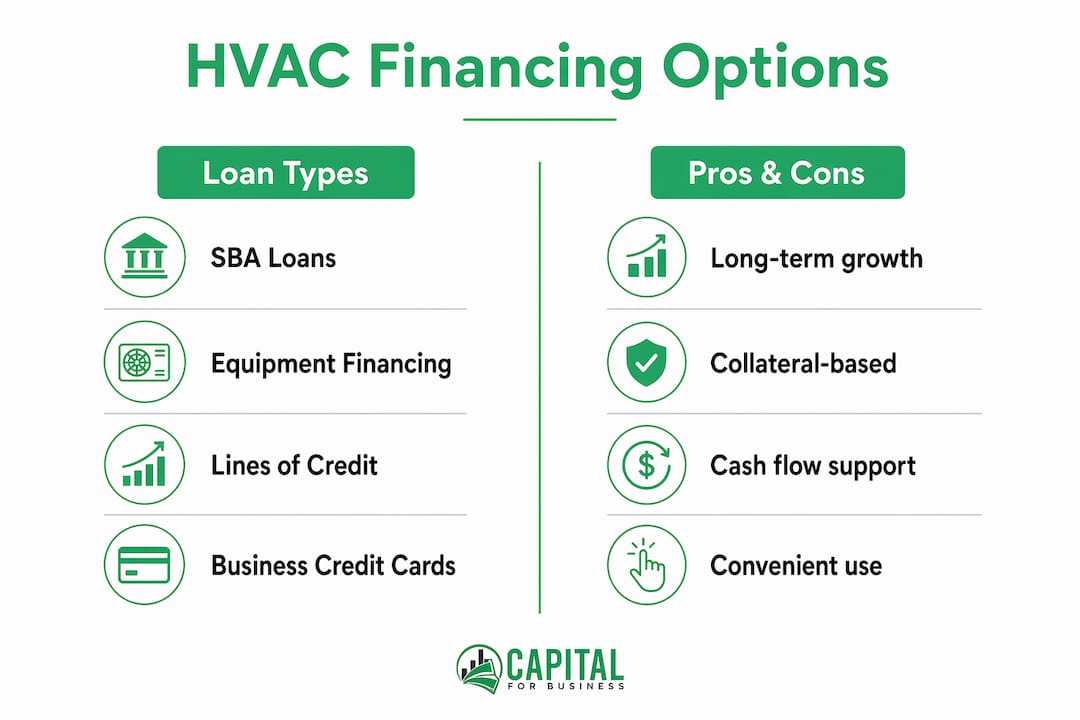

HVAC businesses have access to several distinct financing tools, and your business credit score directly influences which ones you qualify for and at what cost. Understanding each option helps you match the right product to the right need.

| Loan Type | Best Use | Key Advantage | Key Drawback |

|---|---|---|---|

| SBA Loans | Long-term growth, real estate | Low rates, long repayment terms | Slow approval, heavy documentation |

| Equipment Financing | HVAC units, vans, tools | Equipment serves as collateral | Tied to specific asset purchase |

| Working Capital Loans | Payroll, supplies, slow season | Fast funding, flexible use | Higher rates than SBA |

| Business Line of Credit | Seasonal cash gaps, emergencies | Revolving access, pay only what you use | Requires strong credit history |

| Business Credit Cards | Daily expenses, vendor purchases | Builds credit, rewards programs | Low limits early in credit history |

Equipment financing is the most common starting point for HVAC startups. The equipment itself serves as collateral, which means lenders take on less risk and often approve borrowers with shorter credit histories. A new HVAC van or a set of commercial refrigerant recovery machines can be financed this way through lenders like Capitalforbusiness, with the asset securing the loan.

A revolving business line of credit addresses the seasonal cash flow reality every HVAC contractor faces. Summer brings peak revenue from AC calls, while winter can slow residential service dramatically in some markets. A line of credit lets you draw funds during slow months and repay when revenue recovers, without reapplying each time.

Business credit card approvals generally require a personal FICO score of 670 or higher for the best options. Alternative lenders may accept scores as low as 500–550 with sufficient revenue and operational history. That flexibility matters for HVAC startups still building their profiles.

Applying during peak months like summer, when your financial statements show strong cash flow, significantly improves approval chances and the terms lenders offer. Lenders evaluate recent performance, so timing your application to coincide with your strongest revenue period is a practical advantage most contractors overlook.

Pro Tip: Do not apply for multiple loans simultaneously. Each hard inquiry can lower your personal credit score and signal financial stress to lenders. Space applications at least 90 days apart and apply for the product that best matches your current credit profile.

How should HVAC owners manage credit lines operationally?

Strong credit is only useful if you manage it well after you get it. HVAC businesses have specific operational patterns that require a structured approach to banking and credit use.

-

Maintain multiple business bank accounts. HVAC-specific banking works best with 8–10 separate accounts designated for seasonal reserves, equipment funds, payroll, and tax obligations. That structure gives you a clear picture of where money is at any moment and prevents you from accidentally spending equipment reserves on payroll.

-

Use equipment loans to preserve your credit line. When you finance a new van or HVAC unit through a dedicated equipment loan, you keep your line of credit free for operational expenses like parts, fuel, and subcontractor payments. Mixing these uses depletes your revolving credit and leaves you exposed during slow months.

-

Offer customer financing as a sales tool. Shops that offer customer financing close 50% of replacement projects compared to 38% for those that do not. Dealer fees for 0% APR promotions range from 3–12% depending on the promotion length and financing partner. That fee is a customer acquisition cost, not a penalty, and it pays for itself in closed jobs.

-

Integrate accounting software for cash flow clarity. Tools like QuickBooks or FreshBooks connect directly to your business bank accounts and give you real-time visibility into receivables, payables, and available credit. That visibility prevents the common mistake of drawing on credit when cash is actually available.

-

Review your credit utilization monthly. Keeping your business credit card balances below 30% of your credit limit protects your Experian Business and Equifax Business scores. High utilization signals financial stress even when you are paying on time.

Pro Tip: Adapt the Profit First method for your HVAC business by assigning a percentage of every deposit to separate accounts for taxes, owner pay, operating expenses, and equipment. This structure prevents cash flow crises and keeps your credit lines available for genuine emergencies.

What are the biggest mistakes in HVAC business credit?

Most HVAC business owners do not lose financing opportunities because of bad luck. They lose them because of specific, avoidable mistakes that compound over time.

-

Mixing personal and business finances. This is the single most common error. Using a personal card for business purchases or depositing business checks into a personal account blurs the line lenders need to see. It also removes the liability protection your LLC or corporation provides.

-

Ignoring credit monitoring. Errors on business credit reports are more common than most owners realize. A vendor who misreports a payment or a duplicate account can drag your score down for months. Regular monitoring at Dun & Bradstreet, Experian Business, and Equifax Business is the only way to catch these problems early.

-

Applying for credit without proper documentation. Lenders want to see two years of tax returns, recent bank statements, a current profit and loss statement, and a business plan. Walking into a loan application without these documents wastes time and results in unnecessary hard inquiries on your credit report. Review common financing mistakes before you apply.

-

Applying during your slowest revenue months. A loan application submitted in february, when your bank statements show minimal activity, tells a weak story. Wait until your financials reflect peak performance before approaching lenders.

-

Mismanaging credit lines. Drawing your entire line of credit for a single large purchase and then carrying that balance for months raises your utilization rate and signals poor cash management. Use your line for short-term gaps, not long-term financing needs.

The best practices that counter these mistakes are straightforward: pay every bill on time, keep business and personal finances completely separate, review your credit reports quarterly, and time your financing applications to align with your strongest financial periods. Consistently following these credit score improvement tips compounds into a fundable profile within 12 months.

Key takeaways

HVAC business credit essentials require a separate legal entity, consistent payment history across multiple tradelines, and strategic timing of financing applications to build a fundable credit profile.

| Point | Details |

|---|---|

| Start with legal structure | Register your business, get an EIN and D-U-N-S number before opening any credit accounts. |

| Build tradelines deliberately | Use Net-30 vendor accounts and business credit cards that report to Dun & Bradstreet, Experian, and Equifax. |

| Time your loan applications | Apply during peak revenue months when your financials show the strongest performance. |

| Separate finances completely | Never mix personal and business accounts; separation protects liability and builds credit faster. |

| Monitor and dispute errors | Check all three bureau reports quarterly and dispute inaccuracies before they delay financing. |

What i have learned after years of working with HVAC contractors

At Capitalforbusiness, we have worked with HVAC business owners since 2009, and the pattern we see most often is this: contractors who struggle to get financing are not struggling because their business is weak. They are struggling because their credit profile does not reflect the strength of their business.

The most common situation we encounter is an HVAC owner with five years of solid revenue who has never separated personal and business finances. Their personal credit score is decent, but their business credit profile is essentially blank. When they approach a bank for a $150,000 equipment loan, the bank sees a ghost. There is no business credit history to evaluate.

The fix is not complicated, but it requires patience. We tell every contractor the same thing: start building your business credit profile now, even if you do not need financing today. The 6–12 month timeline to a fundable profile means the best time to start was a year ago. The second best time is today.

We also see contractors underestimate the value of timing. Applying for a working capital loan in january after a slow winter quarter is a harder conversation than applying in august after three months of strong AC season revenue. Lenders look at recent performance. Give them your best months to evaluate.

One more thing worth saying directly: do not let a thin credit file stop you from exploring your options. Alternative lenders, including Capitalforbusiness, work with HVAC businesses at every stage of credit development. The goal is always to match you with the right product for where you are right now, while helping you build toward better terms in the future.

— Capital

HVAC financing solutions built for contractors like you

Capitalforbusiness has helped HVAC contractors across the country access the funding they need to buy equipment, cover slow-season payroll, and take on larger commercial projects. Whether you are building your credit profile from scratch or ready to apply for a substantial loan, we have products designed for your situation.

From equipment financing up to $250,000 with same-day funding to working capital loans and business lines of credit, Capitalforbusiness moves faster than traditional banks and works with a wider range of credit profiles. If your personal credit is not perfect, explore our bad credit business loan options to see what you qualify for today. You can also review the full range of small business loan types to find the product that fits your current stage of growth.

FAQ

What is a d-u-n-s number and do HVAC businesses need one?

A D-U-N-S number is a nine-digit identifier issued by Dun & Bradstreet that establishes your business in their credit database. HVAC businesses need one because many lenders and commercial vendors check Dun & Bradstreet before extending credit or Net-30 terms.

How long does it take to build HVAC business credit?

Building a fundable business credit profile typically takes 6–12 months of consistent, on-time payments reported to major bureaus. Paying vendor invoices early can accelerate your PAYDEX score growth at Dun & Bradstreet.

What credit score do i need for an HVAC business loan?

Business credit card approvals generally require a personal FICO score of 670 or higher for the best options, though alternative lenders may approve scores as low as 500–550 with sufficient revenue history. Equipment financing is often easier to qualify for because the equipment serves as collateral.

Should i separate personal and business finances right away?

Yes. Separating personal and business finances from the start protects your personal liability and is a required step for building a business credit profile that lenders can evaluate independently. Open a dedicated business bank account before making any business purchases.

When is the best time to apply for an HVAC business loan?

Apply during your peak revenue months, typically summer for most HVAC contractors, when your bank statements and financial records reflect strong cash flow. Lenders evaluate recent performance, and stronger financials at application time improve both approval odds and the terms you receive.