TL;DR:

- Securing HVAC financing involves thorough preparation, choosing the right structure, and prompt responses.

- Complete documentation and demonstrating strong cash flow significantly accelerate approval and funding.

The HVAC equipment financing process is the series of steps a small business owner takes to secure funds for purchasing or upgrading heating, ventilation, and air conditioning equipment, covering application, documentation, underwriting, approval, and funding. For most small businesses, HVAC systems represent one of the largest capital expenditures on the books, with commercial rooftop units, chillers, and VRF systems routinely running from $15,000 to well over $150,000. Financing spreads that cost across manageable monthly payments while preserving working capital for payroll, inventory, and operations. Lenders evaluate three core factors throughout this process: the equipment's value as collateral, your business's cash flow capacity, and the completeness of your documentation package. Understanding each stage before you apply puts you in control of the timeline and the outcome.

What types of HVAC financing options are available?

Four main financing structures cover the majority of HVAC purchases for small businesses: equipment loans, equipment leases, SBA-backed loans, and vendor financing programs. Each carries different tradeoffs in ownership, approval speed, cost, and collateral treatment. Choosing the wrong structure for your situation adds cost and complexity, so the comparison below matters.

Equipment loans vs. leases

An equipment loan grants immediate ownership with the lender holding a security interest in the equipment until the balance is paid. This works well when you want to build equity in a long-lived asset, take advantage of Section 179 tax deductions, or when the equipment has strong resale value. Equipment leases, by contrast, keep the equipment on the lessor's books, which lowers your upfront cost and can simplify balance sheet treatment. Leases suit businesses that upgrade systems frequently or want to avoid obsolescence risk on technology-heavy HVAC controls.

SBA 7(a) and SBA 504 loans

SBA 7(a) financing covers purchasing and installation of machinery and equipment, while SBA 504 financing targets long-life, major fixed assets with typical approval times of 30 to 90 days. The SBA 504 program requires the equipment to carry a useful life of at least 10 years, which most commercial HVAC systems satisfy. The structure splits funding: a bank covers 50%, a Certified Development Company covers 40%, and you contribute 10% as a down payment. Rates are below conventional market rates, but the longer approval timeline makes SBA 504 a poor fit when you need equipment installed within weeks.

Vendor financing and conventional loans

Many HVAC manufacturers and distributors, including Carrier, Trane, and Lennox, offer point-of-sale financing through captive finance arms or third-party lenders. These programs can approve in 24 to 48 hours and sometimes include promotional periods, but rates are often higher than bank alternatives. Conventional equipment loans typically fund in 2 to 4 weeks with advance rates of 80 to 100% on new equipment, making them the practical middle ground for most small businesses.

| Financing type | Approval speed | Best for | Down payment |

|---|---|---|---|

| Equipment loan | 2 to 4 weeks | Ownership, tax deductions | 10 to 20% |

| Equipment lease | 1 to 5 days | Frequent upgrades, lower upfront cost | Often $0 |

| SBA 504 | 60 to 90 days | Long-life assets, lowest rates | 10% |

| Vendor financing | 24 to 48 hours | Speed, convenience | Varies |

Pro Tip: If your HVAC replacement is urgent due to equipment failure, vendor financing or a conventional equipment loan from a lender like Capitalforbusiness will get you funded faster than any SBA program. Reserve SBA 504 for planned capital projects with a 60-day runway.

You can also review a detailed breakdown of HVAC financing options to compare structures side by side before committing to an application.

What documentation do you need for HVAC financing approval?

Equipment financing underwriting heavily weighs the equipment as collateral and your cash-flow capacity, requiring a financial package of 3 to 6 months of business bank statements, tax returns, and the equipment invoice or quote. Submitting an incomplete package is the single most common reason for delays. Lenders cannot move to underwriting until every required item is in hand, so a missing document adds days or weeks to your timeline.

Business identity and ownership documents

- Government-issued photo ID for all owners with 20% or more ownership stake

- Business formation documents: articles of incorporation, operating agreement, or DBA filing

- Employer Identification Number (EIN) confirmation letter from the IRS

- Business license or operating permit relevant to your state and industry

Financial documents

- 3 to 6 months of complete business bank statements (all pages, all accounts)

- 2 years of business tax returns, signed and dated

- Most recent year-to-date profit and loss statement

- Debt schedule listing all current business obligations and monthly payments

Equipment-specific documents

- Formal vendor quote or invoice showing make, model, serial number, and total installed cost

- Vendor contact information and delivery timeline confirmation

- For used HVAC equipment: independent appraisal and inspection report

- Proof of insurance naming the lender as loss payee

Collateral and lien documents

Lenders file a UCC-1 financing statement to perfect their security interest in the equipment. If you have existing UCC liens from other lenders, your new lender will require a lien search and may need subordination agreements before proceeding. Coordinating lien priorities is critical when layering SBA loans with equipment financing, since conflicting security interests can stall underwriting entirely.

Pro Tip: Organize your submission package in this exact order: application and ownership docs, IDs, formation documents, bank statements, tax returns, debt schedule, equipment quote, insurance proof, and any used equipment appraisals. A well-organized application package speeds approval dramatically because underwriters can process it without back-and-forth requests.

| Document category | Specific items required |

|---|---|

| Identity | Photo ID, EIN letter, business license |

| Financial | Bank statements (3 to 6 months), tax returns (2 years), P&L |

| Equipment | Vendor quote with serial number, delivery confirmation |

| Collateral | UCC lien search, insurance with lender as loss payee |

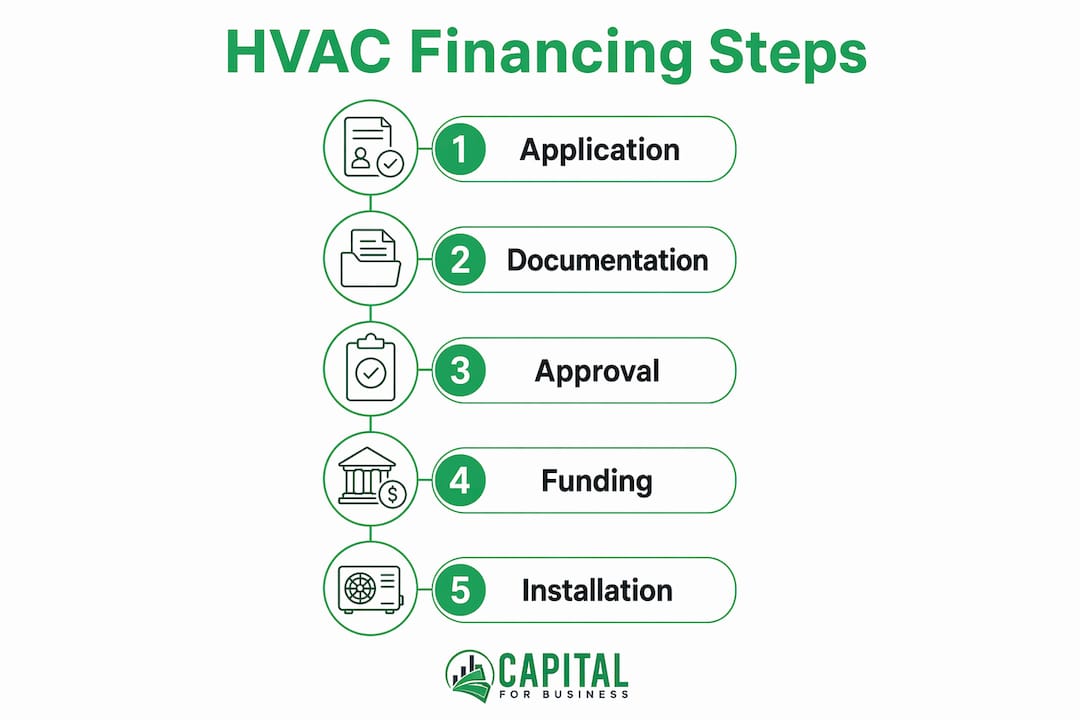

What does the step-by-step approval process look like?

The HVAC equipment financing process follows a predictable sequence from inquiry to funded account. Knowing what happens at each stage helps you prepare the right materials at the right time and respond to lender requests without delay.

-

Submit your inquiry and application. Provide basic business details, the equipment type and cost, and your requested loan amount. Most lenders, including Capitalforbusiness, accept online applications that take under 15 minutes to complete.

-

Initial screening and pre-review. The lender's credit team runs a soft or hard credit pull, confirms your time in business, and checks that the equipment type is eligible for their program. This stage typically takes 24 to 48 hours.

-

Document collection. You receive a checklist of required items and submit your full financial package. The speed of this stage is entirely within your control. Businesses that submit complete packages on day one move to underwriting immediately.

-

Underwriting evaluation. This is the most detailed stage. Underwriters assess:

- Credit score and credit history of the business and its owners

- Cash flow coverage: the monthly payment must fit comfortably within operating cash flow

- Time in business and industry stability

- Equipment value and condition as collateral

- Existing debt obligations and lien position

-

Decision outcome. Three outcomes are possible. An approval moves directly to final documentation. A conditional approval, sometimes called a "yes, if" decision, requires additional items such as a larger down payment, a co-signer, or clarification on a specific document. A decline typically comes with a reason code that tells you what to address before reapplying.

-

Final documentation and vendor coordination. Once approved, you sign loan documents, and the lender coordinates directly with your HVAC vendor to confirm the invoice, delivery date, and installation schedule. Funds are disbursed to the vendor, not to you, in most equipment financing structures.

-

Equipment delivery and lien filing. After delivery and installation confirmation, the lender files the UCC-1 statement. Your repayment schedule begins on the agreed start date.

Conventional loans complete this sequence in 2 to 4 weeks. SBA 504 loans run 60 to 90 days. Vendor financing programs can compress the entire process to 48 hours for straightforward applications.

How can you speed up the HVAC financing process?

Several specific actions reduce approval time and improve your odds of a clean approval on the first submission. These are not generic tips. They address the exact friction points that slow down HVAC equipment financing applications.

-

Match your documents to your application exactly. Document mismatches between the approved equipment description and the final invoice are a common hidden delay. The make, model, serial number, and total cost on your quote must match what appears on the final invoice. Any discrepancy triggers a re-review.

-

Respond to conditional approval requests the same day. Responding promptly to lender requests is disproportionately important to funding speed. Conditional approvals expire or lose priority in the lender's queue when borrowers take days to respond. Treat every lender request as urgent.

-

Demonstrate ROI on the equipment. Lenders want to see a strong business case for ROI and payment capacity. A one-page summary showing how the new HVAC system reduces energy costs, supports a lease renewal, or enables a new service contract gives underwriters a reason to approve beyond the numbers alone.

-

Address credit issues before applying. If your personal or business credit score is below 650, consider paying down revolving balances, resolving any collections, or adding a creditworthy co-signer before submitting. Applying with known credit problems without a mitigation strategy wastes time.

-

Choose terms that fit your cash flow. Extending the loan term from 36 to 60 months reduces the monthly payment and improves your debt service coverage ratio, which directly affects underwriting decisions. A lower monthly payment that fits your cash flow is better than a shorter term that strains it.

Pro Tip: Before you apply, pull your own business credit report from Dun & Bradstreet or Experian Business and check for errors. Disputing inaccuracies takes time, but catching them before a lender does prevents a surprise decline.

How to choose the best HVAC financing option for your business

Selecting the right financing structure depends on four variables: the equipment's cost and useful life, your business's cash position, how quickly you need the equipment, and your tax situation. No single option is best for every business.

For new commercial HVAC systems with a useful life of 15 to 25 years, SBA 504 financing delivers the lowest total cost of capital when your timeline allows 60 to 90 days. The lower interest rate and longer repayment term reduce monthly obligations significantly compared to conventional loans. However, SBA 504 loans require the asset to have a useful life of 10 years or more, which disqualifies some specialized HVAC control systems with shorter technology cycles.

For businesses that need equipment within 30 days, a conventional equipment loan from a lender like Capitalforbusiness is the practical choice. Advance rates of 80 to 100% on new equipment mean you may need only a 10 to 20% down payment, and funding in 2 to 4 weeks keeps your project on schedule.

Leasing makes sense when you operate in a sector where HVAC technology changes rapidly, such as data center cooling or medical facility climate control, or when your business is in an early growth phase and preserving cash matters more than ownership. You can also explore the loan vs. leasing tradeoffs in detail to see which structure fits your balance sheet.

Tax treatment is a meaningful factor. Section 179 of the IRS tax code allows businesses to deduct the full purchase price of qualifying equipment in the year of purchase rather than depreciating it over time. Bonus depreciation rules in 2026 allow additional first-year deductions on new equipment. These deductions apply to owned equipment, not leased equipment, which shifts the math in favor of loans for profitable businesses with a tax liability to offset.

Sale-leaseback financing is worth considering if you already own HVAC equipment outright. You sell the equipment to a finance company and lease it back, freeing up the equity as working capital while retaining use of the system. This structure suits businesses that need liquidity without taking on new debt.

| Scenario | Best financing fit | Key reason |

|---|---|---|

| New commercial system, 60-day timeline | SBA 504 | Lowest rate, long term |

| Emergency replacement, needed in 2 weeks | Conventional equipment loan | Fast funding |

| Frequent upgrades, technology-heavy | Equipment lease | Flexibility, no obsolescence risk |

| Early-stage business, limited cash | Vendor financing or lease | Low upfront cost |

| Profitable business, tax optimization | Equipment loan with Section 179 | Full deduction in year one |

What I've learned about HVAC financing after working with hundreds of businesses

Working with small business owners across HVAC, construction, and facilities management since 2009 has taught me one consistent lesson: the businesses that get approved quickly are not always the ones with the best credit. They are the ones who arrive prepared.

The most common mistake I see is treating the financing application as an afterthought. A business owner selects equipment, negotiates a price with a vendor, and then starts gathering documents. That sequence adds two to three weeks to the timeline because the financial package is never ready on day one. The businesses that move fastest start collecting bank statements, tax returns, and vendor quotes before they even contact a lender.

The second pattern I notice is underestimating how much lenders care about cash flow relative to credit score. A business with a 680 credit score and clean, consistent bank statements showing strong monthly revenue will often outperform a business with a 720 score and irregular cash flow. Underwriters are approving a monthly payment, not a credit number. Showing that the payment fits your operating reality is the most persuasive thing in your application.

I also want to address the fear that many small business owners carry into the financing process: the belief that if a bank has declined them, no one will approve them. Banks apply rigid criteria that exclude many creditworthy businesses. Lenders like Capitalforbusiness exist specifically to serve businesses that fall outside traditional bank parameters, and they evaluate applications with more flexibility and context. The HVAC equipment financing process is navigable for most businesses when you approach it with the right preparation and the right lender.

— Capital

Get your HVAC equipment financed with Capitalforbusiness

Capitalforbusiness has helped small business owners across hundreds of industries secure equipment financing since 2009, with approvals up to $250,000 and same-day funding available for qualified applicants. Whether you are replacing a failed rooftop unit, upgrading to a high-efficiency commercial system, or expanding your HVAC capacity to support a new location, the team at Capitalforbusiness structures financing around your cash flow and timeline.

Capitalforbusiness works with businesses that banks have turned away, offering flexible terms, fast underwriting, and a straightforward application process. Explore small business loan options or visit the HVAC financing page to see what your business qualifies for today.

FAQ

What credit score do you need for HVAC equipment financing?

Most equipment lenders look for a minimum personal credit score of 620 to 650, though some programs accept lower scores with stronger cash flow or a larger down payment. Lenders weigh cash flow coverage and time in business alongside credit score, so a lower score does not automatically mean a decline.

How long does the HVAC equipment financing process take?

Conventional equipment loans fund in 2 to 4 weeks, vendor financing programs can close in 24 to 48 hours, and SBA 504 loans take 60 to 90 days. Submitting a complete document package on day one is the single fastest way to shorten your timeline.

Can a startup qualify for HVAC equipment financing?

Startups with less than two years in business face stricter requirements, including higher down payments and stronger personal credit. Vendor financing and equipment leases are the most accessible options for early-stage businesses because they rely more on the equipment's value than on business history.

What documents are required for HVAC equipment financing?

Required documents include government-issued ID, business formation documents, 3 to 6 months of bank statements, two years of tax returns, and a vendor quote with the equipment's make, model, and serial number. Proof of insurance naming the lender as loss payee is also standard.

Is HVAC equipment financing tax deductible?

Owned HVAC equipment financed through a loan qualifies for Section 179 expensing, allowing you to deduct the full purchase price in the year of acquisition rather than depreciating it over time. Leased equipment does not qualify for Section 179, though lease payments may be deductible as a business operating expense.

Key takeaways

The HVAC equipment financing process requires complete documentation, the right financing structure, and fast responses to lender requests to move from application to funded in the shortest possible time.

| Point | Details |

|---|---|

| Match financing type to your timeline | Conventional loans fund in 2 to 4 weeks; SBA 504 takes 60 to 90 days but offers lower rates. |

| Documentation completeness drives speed | Submit bank statements, tax returns, and a vendor quote with serial numbers on day one to avoid delays. |

| Cash flow matters more than credit score | Underwriters approve a monthly payment, so showing consistent operating cash flow is the strongest part of your application. |

| Conditional approvals require same-day responses | Responding to lender requests immediately keeps your application at the front of the queue and speeds funding. |

| Section 179 favors loans over leases | Businesses with tax liability benefit from owning equipment through a loan to capture full first-year deductions. |