TL;DR:

- Equipment financing helps small businesses preserve cash and maximize tax deductions in 2026.

- Choosing between loans, leases, or hybrid strategies depends on asset lifespan, technology risk, and cash flow.

- Regular review and strategic planning of financing portfolios enhance growth and cost savings.

Many small business owners assume equipment financing is reserved for large corporations or for businesses that simply cannot afford to buy outright. That assumption is costing them real money. In 2026, new tax rules around accelerated depreciation and expanded deductions are making equipment financing one of the smartest financial moves a small business can make, regardless of size or industry. Whether you run a restaurant, a landscaping company, or a tech startup, the right financing structure can preserve your working capital, reduce your tax burden, and keep your operation competitive. This article walks you through the key benefits, the main structures available, and how to choose what fits your growth plans.

Table of Contents

- What is equipment financing and why it matters for 2026

- Top benefits of equipment financing for small businesses

- Comparing equipment loans, leases, and hybrid options

- How to maximize equipment financing benefits in 2026

- Real-world examples: How businesses use equipment financing to grow

- Our take: What most small business owners miss about equipment financing

- Explore your equipment financing options for 2026

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Flexible growth options | Equipment financing lets small businesses access new technology and assets without large upfront costs. |

| Major tax savings | New 2026 laws accelerate deductions, making equipment financing more profitable than ever. |

| Hybrid solutions work | Combining leasing for tech and loans for heavy assets provides maximum advantage. |

| Plan strategically | Consult your accountant and review financing annually to capture all possible savings and benefits. |

What is equipment financing and why it matters for 2026

Equipment financing is the practice of using a loan or lease to acquire machinery, vehicles, technology, or any physical asset your business needs to operate. Rather than paying the full purchase price upfront, you spread the cost over time while putting the equipment to work immediately. It is a tool that has been available for decades, but its value is sharpening in 2026 for specific reasons tied to tax policy and market conditions.

The businesses using equipment financing today span nearly every industry:

- Restaurants upgrading commercial ovens and refrigeration systems

- Construction companies modernizing their fleet of excavators and cranes

- Medical practices acquiring diagnostic and imaging equipment

- Retailers investing in point-of-sale and inventory management technology

- Trucking operators expanding their vehicle fleets

What makes 2026 different is that accelerated write-offs now make financing more attractive than straight cash purchases for many asset categories. When you finance equipment, you can often deduct a significant portion of its cost in the first year while keeping your cash available for payroll, inventory, and marketing. That changes the math considerably.

Understanding the leasing vs. financing differences is the starting point for making a smart decision. Leasing tends to work better for businesses that need flexibility or face rapid technology change. Financing, meaning taking an actual loan that builds ownership, works better for long-life assets that hold or gain value over time.

Pro Tip: Before choosing a structure, assess how long the equipment will remain productive for your specific operation. A piece of manufacturing equipment with a 15-year useful life justifies a different approach than a server system that will be outdated in four years.

You can explore the full range of equipment financing options available to small businesses to see which structures align with your industry and asset type.

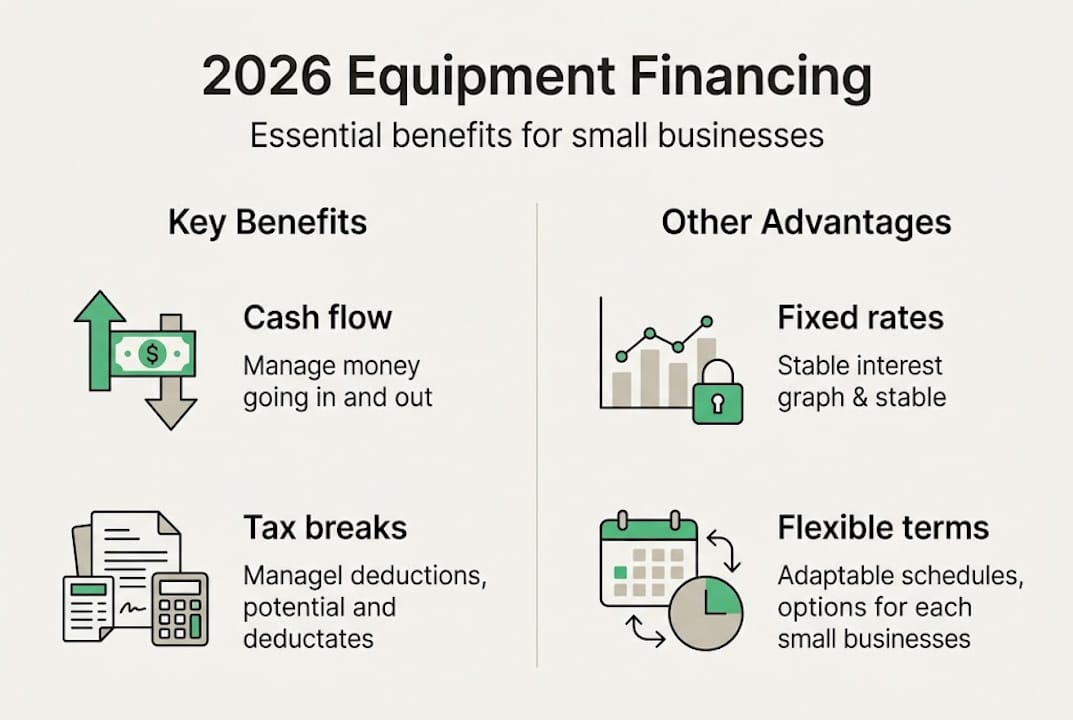

Top benefits of equipment financing for small businesses

With the basics covered, let's break down the powerful benefits equipment financing offers your business this year.

Preserve working capital. The most immediate benefit is straightforward: you do not drain your cash reserves. A single large equipment purchase can wipe out months of operating cushion. Financing keeps that money available for daily expenses, unexpected costs, and growth opportunities.

Tax advantages in 2026. Section 179 of the U.S. tax code allows businesses to deduct the full purchase price of qualifying equipment in the year it is placed in service. In Canada, accelerated depreciation rules are similarly favorable. These deductions are most powerful when combined with financing, because you gain the deduction without depleting cash.

Fixed-rate predictability. Unlike revolving credit lines that fluctuate with interest rate changes, equipment loans typically carry fixed rates. That means your monthly payment stays the same whether rates rise or fall, making budgeting far more reliable.

Building equity versus staying current. Financing a long-life asset builds equity that adds to your balance sheet. Leasing, on the other hand, lets you swap out equipment at the end of a term, keeping pace with technology changes without the risk of owning something obsolete.

The way you unlock growth and cash flow through financing depends heavily on matching the structure to the asset. The data backs this up clearly.

"Total cost matters more than the monthly payment. Match your financing structure to the asset's life and your cash flow cycle. A hybrid approach, leasing technology and buying heavy equipment, is often optimal. Always consult your accountant for tax optimization." Owning vs. leasing equipment

Many industries using equipment financing have found that the true financial advantage emerges over the full term of the agreement, not just in the first few months of lower payments. Reviewing equipment financing examples from similar businesses can help you visualize what the numbers look like in practice.

Pro Tip: Don't just compare monthly payments across lenders. Ask your accountant to calculate total cost of ownership for each option, including interest, maintenance obligations, and tax impact over the full term.

Comparing equipment loans, leases, and hybrid options

Once you know the benefits, the next step is choosing the right structure. Here is a clear comparison to guide your decision.

| Feature | Equipment loan | Equipment lease | Hybrid approach |

|---|---|---|---|

| Ownership | Yes, at end of term | No (option to buy varies) | Depends on asset type |

| Monthly payments | Higher | Lower | Mixed |

| Best for | Long-life, value-retaining assets | Frequently upgraded tech | Diverse asset portfolios |

| Tax advantage | Depreciation and Section 179 | Lease payments deductible | Combination of both |

| End-of-term flexibility | Own outright | Upgrade or return | Flexible by asset |

| Balance sheet impact | Asset + liability | Off-balance-sheet (in some cases) | Varies |

Here is a numbered framework for choosing the right option:

- Assess equipment lifespan. Equipment that lasts 10 or more years typically justifies financing. Assets with a 3 to 5 year useful life often suit a lease better.

- Evaluate technology risk. If the equipment is likely to become obsolete quickly, leasing reduces the risk of being stuck with outdated tools.

- Review your cash flow cycle. Businesses with seasonal revenue patterns often benefit from leases that allow for adjusted payment schedules.

- Map your tax position. Work with your accountant to determine whether depreciation deductions or deductible lease payments provide better relief for your specific situation.

- Consider a hybrid portfolio. Matching structure to asset life is what separates strategic financing from reactive borrowing.

You can use a hybrid finance calculator to model different scenarios before committing. The tool helps you see how payment structures affect total cost across different asset types.

For a deeper dive into how these options stack up, the guide on choosing between loan or leasing walks through specific scenarios by industry. The detailed comparison guide adds more context if you want to go further.

Pro Tip: Schedule a formal review of your equipment finance portfolio every 12 months. Rates change, business needs shift, and refinancing options may improve. A structured annual review keeps you from overpaying on outdated terms.

How to maximize equipment financing benefits in 2026

After understanding which structure fits, let's make sure you're capturing every possible advantage in 2026.

The strategies below are practical and actionable. Most businesses can implement them with the help of their accountant and a qualified lender.

- Optimize your tax position first. Before signing any financing agreement, confirm with your accountant how accelerated depreciation or Section 179 applies to the specific asset. The 2026 tax deduction changes favor financing over cash purchases in many scenarios.

- Map your upgrade cycles. Create a written timeline of when each major piece of equipment will need replacement. This exercise reveals which assets should be financed, which should be leased, and when to start the application process.

- Apply hybrid strategies intentionally. Finance your heavy equipment. Lease your technology. This combination gives you equity on durable assets while keeping your tech stack current without obsolescence risk.

- Research grants and incentives. Several 2026 government programs in both the U.S. and Canada offer grants or subsidized financing tied to green energy equipment, workforce development tools, and manufacturing modernization.

- Review and renegotiate existing terms. Rates and lender offerings have shifted. If you have existing agreements, check whether refinancing produces a better outcome.

| Strategy | Best for | Potential savings |

|---|---|---|

| Section 179 deduction | U.S. businesses buying qualifying equipment | Up to full purchase price in year one |

| Accelerated depreciation | Both U.S. and Canadian businesses | Significant first-year write-off |

| Lease payment deduction | Businesses with short asset cycles | Fully deductible lease payments |

| Hybrid portfolio | Businesses with mixed asset types | Optimized tax and cash flow outcome |

Staying on top of financing trends for 2026 ensures you are not leaving incentives on the table. Pairing that awareness with smart business financing strategies gives you a complete picture of where to focus your energy.

Real-world examples: How businesses use equipment financing to grow

Nothing brings a framework to life like real stories. Here is how your peers are applying these strategies.

The restaurant that expanded without draining cash. A mid-sized restaurant group wanted to open a second location but could not afford to equip it from operating funds. By leasing commercial ovens, refrigeration units, and prep stations, they kept their cash available for staffing, marketing, and lease deposits on the new space. Lower monthly payments preserved their operating margin during the critical first six months of the new location.

The construction firm that boosted project capacity. A regional construction company needed to take on larger contracts but lacked the heavy machinery to do so. By financing two excavators and a fleet of dump trucks at fixed rates, they locked in predictable costs and avoided the volatility of rental markets, which had surged significantly. The fixed payment structure let them bid projects with confidence because equipment costs were known and stable.

The tech startup with a split approach. A software development firm needed both servers for infrastructure and laptops for its growing team. They financed the server infrastructure on a five-year loan and leased the laptops on a two-year cycle. This approach meant the core infrastructure would be owned outright and depreciated over time, while the team always had current devices without paying to own hardware that becomes outdated quickly.

Business owners in these scenarios share a common insight:

"The right structure let us grow faster and control costs. Financing gave us options we didn't have before."

This mirrors what the data shows: combining leasing and financing based on asset type and cash flow needs produces better outcomes than a one-size-fits-all approach. Reviewing additional equipment financing examples from businesses in your industry can help you spot patterns that apply to your own situation.

Our take: What most small business owners miss about equipment financing

Taking these stories into account, here is our candid perspective after working with hundreds of small businesses across North America since 2009.

The most common mistake we see is fixating on the monthly payment. A lower monthly payment feels like a win, but it often means a longer term, more total interest, and a worse overall deal. The businesses that use financing most effectively are the ones asking a different question: what is the total cost of this asset over its full useful life, and which structure minimizes that cost while maximizing tax advantage?

Another gap we see constantly is treating equipment financing as a one-time transaction rather than an ongoing strategy. The businesses that grow fastest treat their financing portfolio the same way they treat their product line or their team: as something that needs regular attention, adjustment, and optimization.

The hybrid approach is where the real advantage lives. Most small businesses have a mix of fast-changing and slow-changing assets. Applying the same financing structure to all of them is a missed opportunity. Leasing your tech and financing your heavy equipment is not complicated. It just requires a little planning.

Pro Tip: Schedule your annual equipment finance review for Q4 each year. That timing aligns with tax planning season and gives you time to act before year-end deadlines.

For context on why this matters financially, read more on optimizing capital with financing and what it actually looks like to manage a financing portfolio strategically rather than reactively.

Explore your equipment financing options for 2026

Ready to take the next step? Here is how you can act on these insights.

Capital for Business has worked with small business owners across hundreds of industries since 2009, helping them access fast, affordable financing when traditional banks fall short. Whether you are exploring equipment loans, leasing structures, or a hybrid strategy, we have the experience and the product range to match your needs.

Start with the beginner's guide to equipment financing if you want a clear overview before making any decisions. When you are ready to move forward, you can apply for equipment funding directly through our platform. Approvals are fast, funding can happen the same day, and our team supports both single-product and hybrid strategies. If you want to see how equipment financing fits within your broader borrowing options, the overview of types of business loans gives you the full picture.

Frequently asked questions

What kinds of equipment can be financed in 2026?

Most equipment essential to business operations qualifies, including vehicles, restaurant ovens, manufacturing machines, medical devices, and technology hardware. The range of eligible assets covers nearly every industry from food service to construction.

Will new 2026 tax rules make equipment financing more advantageous?

Yes. Accelerated depreciation rules and expanded Section 179 limits mean that financing equipment in 2026 can deliver larger first-year tax deductions than in prior years, making it financially smarter than a straight cash purchase in many cases.

How do I choose between leasing and financing equipment?

Lease equipment that changes quickly, like computers and software tools, and finance equipment with a long useful life, like heavy machinery. A hybrid approach combining both often produces the best tax and cash flow outcome.

Does equipment financing improve cash flow?

Yes. Instead of a large upfront payment that strains your reserves, financing spreads the cost over a defined term, freeing up cash for payroll, inventory, marketing, and other day-to-day business needs.