TL;DR:

- Non-bank lending provides faster, more flexible business financing outside traditional banks, with higher rates and fewer regulations. Small business owners can access various loan types from private credit funds, online platforms, and specialty lenders, often for urgent or higher-risk needs. Careful planning and fee comparison are essential to maximize benefits and minimize risks when choosing non-bank funding options.

Non-bank lending is defined as business financing provided by lenders who operate entirely outside the traditional regulated banking system. These lenders, formally called non-bank financial institutions (NBFIs), include private credit funds, specialty finance companies, online platforms, and peer-to-peer lenders. The private credit market now manages approximately $1.78 trillion in assets globally. That scale signals one clear fact: non-bank financing is no longer a fringe option. For small business owners who need capital quickly or who don't qualify for a conventional bank loan, explaining non-bank lending is the first step toward finding the right funding path.

What is non-bank lending and how does it work?

Non-bank lending covers every form of business financing that does not originate from a federally chartered bank or credit union. The industry term for these providers is non-bank financial institutions, or NBFIs. You will also hear the term "alternative lenders," which is the more common phrase in small business circles. Both terms describe the same category of lender.

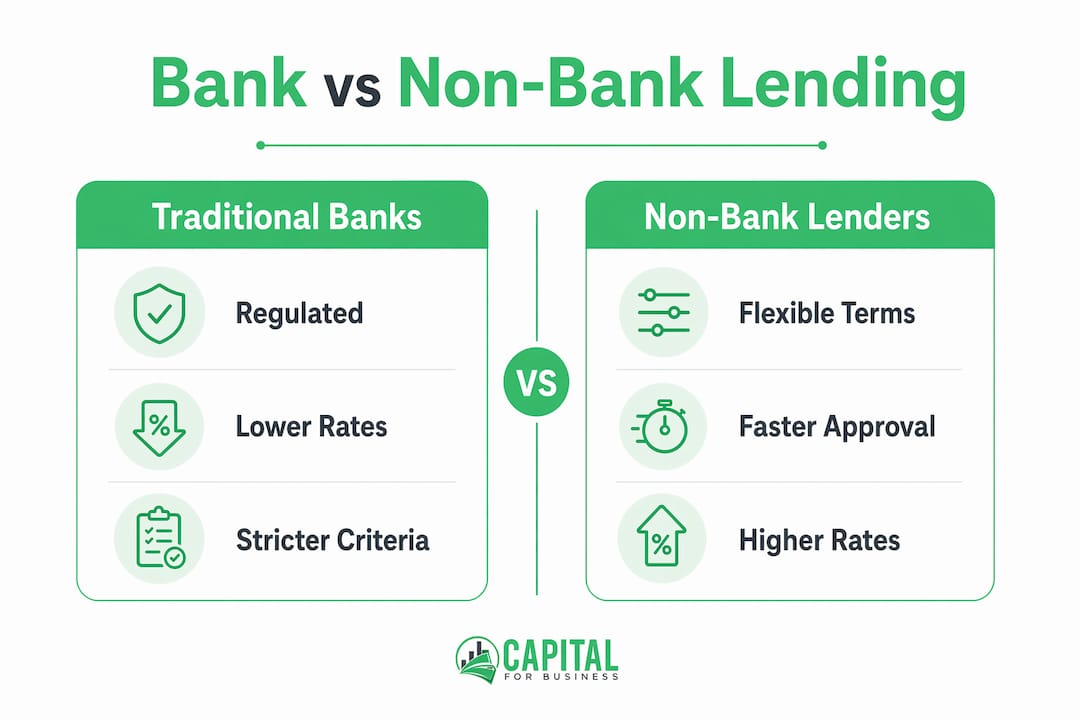

The core difference between a bank and a non-bank lender is the funding source. Traditional banks collect deposits from customers and lend those deposits out. Non-bank lenders fund their loans through wholesale debt markets, institutional investors, and private capital. This distinction matters because it frees non-bank lenders from many of the capital reserve and liquidity rules that govern banks. The result is a lender that can move faster and structure deals differently.

Private credit is now about 10% of total U.S. corporate borrowing. That figure shows how quickly this market has grown from a niche category into a mainstream financing channel. Small business owners are a significant part of that growth, particularly those who need funding that banks routinely decline.

Non-bank lenders must comply with consumer protection and financial conduct laws, but they do not hold full banking licenses. They cannot offer deposit accounts or checking services. Think of them as focused funding partners rather than full-service financial institutions.

What types of non-bank lenders and loan products are available?

The non-bank lending category includes a wide range of lender types, each with a specific focus and funding structure.

Common types of non-bank lenders:

- Private credit funds: Institutional pools of capital that lend directly to businesses, often at larger loan sizes and longer terms.

- Business development companies (BDCs): Publicly registered investment firms that lend to small and mid-sized businesses, often at competitive rates.

- Specialty finance companies: Lenders focused on specific asset classes such as equipment, invoices, or real estate.

- Online lending platforms: Technology-driven lenders that use automated underwriting to approve loans quickly, often within 24–48 hours.

- Peer-to-peer lenders: Platforms that connect individual investors directly with business borrowers, cutting out institutional intermediaries.

Each category operates under a different regulatory regime and serves a different borrower profile. A BDC may work best for an established business seeking a term loan. An online platform may suit a newer business that needs fast working capital.

Common loan products from non-bank lenders include:

- Term loans (fixed repayment schedules over a set period)

- Business lines of credit (revolving access to funds up to a set limit)

- Merchant cash advances (lump-sum funding repaid through a percentage of daily sales)

- Equipment financing (loans or leases tied to specific business equipment)

- Invoice financing (advances against outstanding receivables)

Pro Tip: Before applying, confirm which regulatory body oversees your lender. Legitimate non-bank lenders are registered under financial conduct or consumer protection laws, even if they lack a full banking license.

You can also review alternative lending options to see how these products compare across different lender types.

How does non-bank lending compare to traditional bank lending?

The differences between bank and non-bank lending affect your cost, your approval odds, and how fast you get funded. Understanding these differences helps you choose the right source for your situation.

| Factor | Traditional banks | Non-bank lenders |

|---|---|---|

| Regulatory framework | Basel III capital rules, deposit insurance, full banking license | Financial conduct laws, consumer protection rules, no deposit license |

| Approval speed | Days to weeks | Same day to a few days |

| Credit flexibility | Strict credit score and history requirements | More flexible underwriting, serves higher-risk borrowers |

| Loan-to-value ratios | Conservative, regulated limits | More flexible, deal-by-deal basis |

| Interest rates | Generally lower | Generally higher, reflecting speed and risk |

| Services offered | Full banking relationship (deposits, payments, loans) | Lending only, no deposit or transaction accounts |

Non-bank lenders offer more flexible loan-to-value ratios and underwriting criteria because they are not restricted by the strict capital and liquidity requirements that traditional banks face. That flexibility is the primary reason small business owners turn to them after a bank decline.

The cost difference is real. Non-bank lending rates are typically higher than bank rates, and short-term or bridge loans can carry even steeper pricing. That premium reflects the lender's higher risk exposure and the cost of faster processing.

Non-bank lenders do not provide deposit accounts or full banking services. This means you will still need a traditional bank for your day-to-day business banking. Non-bank lenders are funding partners, not replacements for your primary banking relationship.

Pro Tip: Use a non-bank lender to solve a specific, time-sensitive funding need. Keep your primary banking relationship with a traditional bank for deposits, payments, and long-term credit building.

The migration of corporate lending toward non-bank channels reflects regulatory effects as much as borrower preference. As bank capital requirements tighten under frameworks like Basel III, non-bank lenders fill the gap by taking on deals that banks must decline. You can read more about small business lending trends shaping this shift in 2026.

What are the benefits and risks of non-bank lending?

Non-bank financing options offer genuine advantages for small business owners, but they also carry risks that deserve honest attention before you sign anything.

Benefits of using non-bank lenders

- Faster access to capital. Approvals can happen the same day or within a few business days. For a business facing a time-sensitive opportunity or a cash flow gap, that speed is the deciding factor.

- Flexible underwriting. Non-bank lenders evaluate deals based on cash flow, collateral, and business performance rather than relying solely on credit scores. This opens doors for newer businesses or owners with imperfect credit histories.

- Customized loan structures. Non-bank lenders can tailor repayment schedules, collateral arrangements, and loan terms to fit your specific situation. Banks rarely offer this level of deal customization.

- Access for underserved borrowers. Non-bank lenders serve firms that are unrated or highly leveraged, acting as necessary alternatives rather than replacements for traditional banks.

- Variety of products. From merchant cash advances to equipment financing, non-bank lenders offer products that match specific business needs rather than a one-size-fits-all loan.

Risks to evaluate carefully

- Higher interest rates. The speed and flexibility of non-bank lending comes at a price. Expect to pay an interest premium compared to bank rates. Short-term loans can carry significantly higher costs.

- Opaque fee structures. Some non-bank lenders charge origination fees, prepayment penalties, or administrative costs that are not immediately obvious. Always request a full fee disclosure before signing.

- No deposit protection. Because non-bank lenders are not deposit-taking institutions, your funds are not protected by federal deposit insurance programs.

- Indirect bank exposure. A portion of non-bank lending is indirectly funded by banks, which means liquidity stress in the banking system can affect non-bank lenders too. This is a systemic risk most borrowers overlook.

- Regulatory variation. Non-bank lenders operate under different rules depending on their license type and state. Protections available to bank borrowers may not apply.

Understanding the risks of personal and business loans in the non-bank space helps you ask better questions before committing to any agreement.

How can small business owners choose the right non-bank financing option?

Choosing the right non-bank lender requires more than comparing interest rates. A structured evaluation process protects you from costly mistakes.

-

Define your funding purpose clearly. Know exactly what you need the money for and how long you need it. Equipment purchases suit term loans or equipment financing. Short-term cash flow gaps suit lines of credit or merchant cash advances. Matching the product to the purpose reduces cost and risk.

-

Compare total cost, not just interest rate. Calculate the annual percentage rate (APR) across all fees, not just the stated interest rate. A loan with a lower rate but high origination fees may cost more than one with a slightly higher rate and no fees.

-

Verify lender credentials. Confirm that the lender is registered with the appropriate state or federal financial regulatory body. Legitimate non-bank lenders comply with financial conduct and consumer protection laws, even without a full banking license.

-

Assess collateral requirements. Some non-bank lenders require personal guarantees or specific business assets as collateral. Understand exactly what you are pledging before you sign.

-

Build an exit plan before you borrow. Experts advise mapping a clear exit strategy from non-bank loans before signing. This typically means planning to refinance into a lower-cost bank loan once your business credit profile improves. Paying a premium now is acceptable if you have a defined path to cheaper capital later.

-

Work with a loan specialist or financial advisor. A qualified advisor can compare offers across multiple lenders and identify fee structures that are not obvious in the loan documents. This step is especially valuable for first-time borrowers.

Pro Tip: Review the key considerations before signing any loan agreement. A five-minute checklist can prevent months of financial strain.

Non-bank lending works best as a targeted tool. Use it to solve a specific problem, then refinance or pay it off as soon as your cash flow allows. Treating a short-term non-bank loan as a long-term financing solution is the most common and costly mistake small business owners make.

Key Takeaways

Non-bank lending gives small business owners faster, more flexible access to capital than traditional banks, but the speed and flexibility always come at a higher cost that requires a clear repayment plan.

| Point | Details |

|---|---|

| Non-bank lending defined | Financing from NBFIs outside the traditional banking system, funded by wholesale capital and institutional investors. |

| Faster approvals, higher cost | Non-bank lenders approve loans in days but charge higher rates; always calculate the full APR before committing. |

| Flexible underwriting | Non-bank lenders evaluate cash flow and collateral, making them accessible to businesses banks routinely decline. |

| Exit plan is non-negotiable | Plan to refinance into lower-cost bank financing once your credit profile improves to reduce long-term borrowing costs. |

| Verify credentials and fees | Confirm regulatory registration and request full fee disclosure before signing any non-bank loan agreement. |

What I've learned from watching small businesses use non-bank lenders

The most common mistake I see is treating a non-bank loan like a long-term solution. Business owners take a merchant cash advance or a short-term bridge loan to solve an immediate problem, then roll it over repeatedly because they never built the exit plan. Each rollover adds cost. Within a year, what started as a manageable funding decision becomes a serious drag on cash flow.

The businesses that use non-bank lending well treat it as a bridge, not a destination. They borrow specifically, repay quickly, and use the experience to build a track record that qualifies them for better terms later. That discipline separates the owners who grow from the ones who get stuck.

The other pattern worth noting is documentation. Non-bank lenders move fast, but their underwriting still requires solid financials. Business owners who show up with clean profit and loss statements, current bank statements, and a clear explanation of how the loan will be repaid get better terms and faster decisions. Preparation is not just for bank loans.

The private credit market managing $1.78 trillion globally is a signal that non-bank lending has real institutional backing. That backing also means the market is maturing, with more lenders, more products, and more competition on pricing. Small business owners who understand how to evaluate these options are in a stronger position than ever to find capital that fits their actual needs.

— Capital

Capitalforbusiness: funding solutions built for small business owners

Small business owners across the country face the same challenge: banks say no, but the business still needs capital to grow.

Capitalforbusiness has worked with business owners in hundreds of industries since 2009, providing small business loans, working capital, merchant cash advances, equipment financing, and business lines of credit. The application process is straightforward, funding is fast, and the team works with businesses that traditional banks turn away. If you are ready to explore your options, fast business funding up to $500,000 is available now. Contact Capitalforbusiness to get a personalized funding recommendation for your business.

FAQ

What is non-bank lending in simple terms?

Non-bank lending is business financing provided by lenders who are not traditional banks or credit unions. These lenders use private capital and wholesale funding instead of customer deposits to make loans.

Are non-bank lenders safe to use?

Legitimate non-bank lenders comply with consumer protection and financial conduct laws, though they do not hold full banking licenses. Always verify a lender's regulatory registration before signing any agreement.

Why do non-bank lenders charge higher interest rates?

Non-bank lenders charge an interest premium because they take on higher-risk borrowers and provide faster approvals than banks. The premium compensates for the additional risk and the cost of faster processing.

What types of loans do non-bank lenders offer?

Non-bank lenders offer term loans, business lines of credit, merchant cash advances, equipment financing, and invoice financing. The right product depends on your specific funding need and repayment timeline.

How do I know if a non-bank loan is right for my business?

A non-bank loan is a strong fit when you need fast capital, have been declined by a bank, or need a loan structure that a bank cannot provide. Build a clear repayment or refinance plan before borrowing to manage the higher cost effectively.