TL;DR:

- Managing business credit utilization below 30% by timing payments before statement closes and increasing credit limits improves credit scores and financing options. Tracking creditor reporting schedules and distributing balances across accounts help maintain a consistently low utilization ratio. Regular monitoring and strategic management of credit limits and payment timing are essential for optimal credit health.

Business credit utilization is defined as the percentage of your available revolving credit that your business currently carries as a balance, and it directly shapes your credit scores and your ability to secure financing. Lenders use this ratio, formally called the credit utilization ratio, to assess how much financial risk your business carries at any given moment. Credit experts at Experian and the SBA consistently flag it as one of the most controllable factors in your credit profile. This business credit utilization guide covers how to calculate your ratio, what targets to aim for, how payment timing affects what bureaus actually see, and which credit utilization strategies move the needle fastest for small business owners.

How to calculate your business credit utilization ratio

Business credit utilization is calculated as revolving balance divided by revolving credit limit multiplied by 100. That formula gives you a percentage that tells lenders how much of your available credit you are actively using.

The math is straightforward. If your business carries a $10,000 balance across a $50,000 total credit limit, your utilization ratio is 20%. That single number appears on your credit report and influences every lending decision you face.

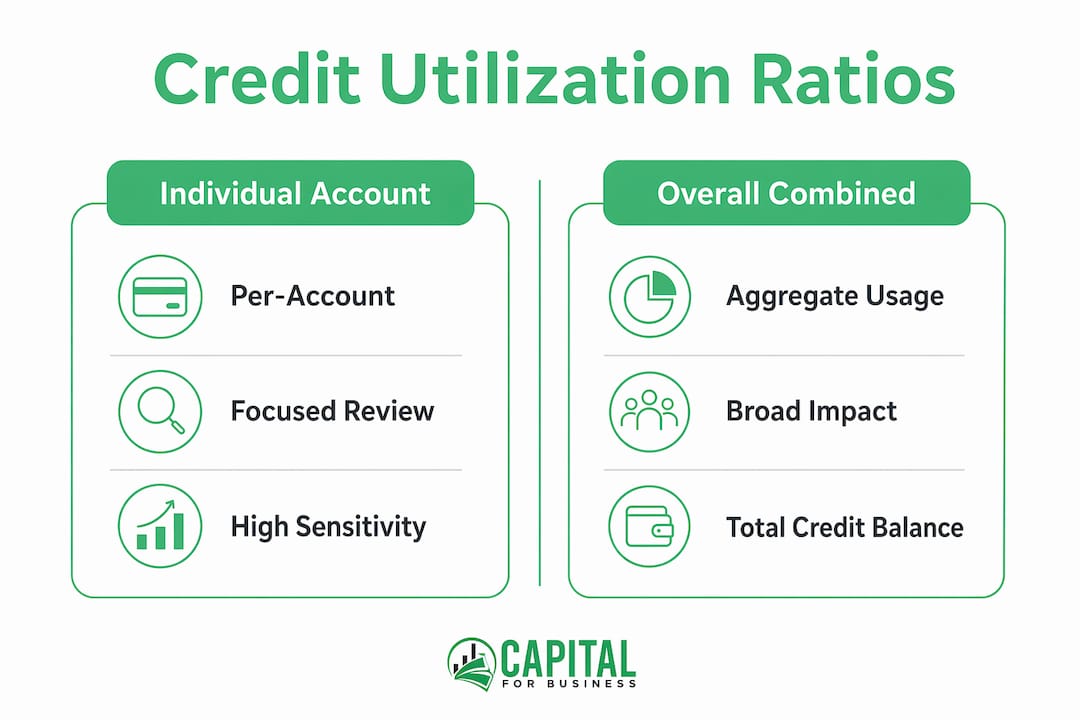

Individual account ratio vs. overall combined ratio

Most credit scoring models look at two levels simultaneously. The first is your per-account ratio, which measures utilization on each individual card or line of credit. The second is your overall combined ratio, which aggregates all balances against all limits.

Both numbers matter. A business with three credit cards, each at 25% utilization, will typically score better than a business with one card maxed at 75% and two cards at zero, even if the total debt is identical. Credit models reward balance distribution, not just total debt levels.

Here is how to run the calculation across multiple accounts:

- List every revolving account: Include all business credit cards and business lines of credit.

- Record the current balance on each account: Use the most recent statement balance, not the real-time balance.

- Record the credit limit on each account: Use the approved limit, not any temporary adjustments.

- Add all balances together: This is your total revolving balance.

- Add all credit limits together: This is your total revolving credit limit.

- Divide total balances by total limits, then multiply by 100: The result is your overall utilization percentage.

Pro Tip: Run this calculation monthly, not just when you apply for financing. Lenders pull your credit at any time, and a single high-utilization month can cost you favorable terms.

Statement closing date balances are the figures that actually land on your credit report. Your real-time balance on a Tuesday afternoon is irrelevant to bureaus. What matters is the balance recorded when your statement closes. This distinction becomes critical when you start timing payments strategically.

What is a good business credit utilization ratio?

Credit experts recommend keeping utilization below 30%, with the optimal target sitting between 10% and 20% for the strongest credit scores. Staying under 30% is the floor, not the goal.

That 10%–20% range is where lenders see a business as financially disciplined. It signals that you use credit as a tool, not as a lifeline. Businesses that consistently operate in this range tend to receive better interest rates, higher credit limits, and faster loan approvals.

How high utilization hurts your business

High utilization sends a clear signal to lenders: this business is stretched. A ratio above 50% on any single account raises red flags during underwriting, even if your payment history is spotless. Lenders interpret high utilization as a sign of cash flow pressure, which increases their perceived risk.

The table below shows how different utilization ranges are generally interpreted by lenders and credit scoring models:

| Utilization Range | Credit Score Impact | Lender Perception |

|---|---|---|

| 0%–10% | Excellent | Highly favorable |

| 11%–20% | Very good | Strong and disciplined |

| 21%–30% | Good | Acceptable, minor concern |

| 31%–50% | Fair | Moderate risk flag |

| 51%–75% | Poor | High risk, may affect approval |

| 76%–100% | Very poor | Serious risk, likely denial |

Some credit profiles can absorb higher utilization without severe score damage if payment history is long and strong. A business with five years of on-time payments and a single month of 45% utilization will not collapse its score. However, sustained high utilization over multiple reporting cycles compounds the damage significantly.

Strong credit management also improves your negotiating position with suppliers and vendors, not just lenders. Businesses with clean credit profiles regularly secure better payment terms, which reduces the need to carry revolving balances in the first place.

Pro Tip: Do not aim for 0% utilization. Lenders want to see that you use credit responsibly. A ratio between 5% and 15% demonstrates active, controlled credit use and typically produces the best scoring outcomes.

How do statement closing dates affect reported utilization?

Creditors report balances at statement closing dates, not at payment due dates. This is the single most misunderstood aspect of credit utilization management for small business owners.

Here is the practical difference. Your statement closes on the 15th of the month. Your payment is due on the 10th of the following month. If you carry a $20,000 balance on the 15th, that $20,000 is what gets reported to the credit bureaus, regardless of whether you pay it in full by the 10th. Paying on time is excellent for your payment history, but it does not reduce the utilization figure that bureaus record.

Why payment timing changes everything

The strategy is to pay down balances before the statement closing date, not just before the due date. This requires knowing your closing date for each account, which you can find on any statement or by calling your issuer directly.

Key steps to manage your reported utilization through timing:

- Identify the statement closing date for every revolving account: This date is fixed each month and determines what balance gets reported.

- Make a mid-cycle payment before the closing date: Reduce your balance to your target utilization level before that date arrives.

- Confirm the payment posts before the closing date: Processing times vary, so submit payments two to three business days early.

- Track which bureau each creditor reports to: Experian, Equifax, and Dun & Bradstreet each receive data on different schedules.

Creditor reporting schedules vary, and different bureaus update at different intervals. This means your utilization ratio can look different depending on which bureau a lender pulls. Tracking multiple reporting cycles reveals each creditor's pattern and helps you avoid misreading a score change as new spending activity.

Pro Tip: Set a calendar reminder three to five days before each account's statement closing date. Use that reminder to check your balance and make a payment if your utilization is above your target.

Effective utilization management consistently hinges on timing payments around the statement close date rather than the payment due date. Most small business owners focus entirely on the due date and never realize their reported utilization is far higher than their actual financial position suggests.

What are the best strategies to optimize business credit utilization?

Optimizing business credit utilization requires more than paying bills on time. The most effective approach combines limit management, balance distribution, payment frequency, and account structure. Here are the proven methods, ranked by impact:

-

Request credit limit increases on existing accounts. Increasing available credit limits reduces your utilization percentage immediately if your balances stay the same. A $15,000 balance on a $30,000 limit is 50% utilization. That same balance on a $60,000 limit drops to 25%. Call your issuer, demonstrate consistent on-time payments, and ask for a limit review.

-

Open additional revolving accounts strategically. Adding a new business credit card or a business line of credit increases your total available credit. This lowers your overall utilization ratio even before you pay down a single dollar of existing debt. Space out new account applications to minimize the impact of hard inquiries on your score.

-

Make multiple payments per month. Paying before your statement closes affects what balance gets reported to bureaus. Making a payment mid-cycle, before the closing date, and another after the due date keeps your reported balance lower throughout the month. This is one of the fastest ways to reduce reported utilization without changing your actual spending.

-

Distribute balances across multiple accounts. Balancing debt across multiple accounts improves scores in models that evaluate both per-account and overall utilization. If you carry $9,000 in revolving debt, spreading it across three cards at $3,000 each scores better than concentrating it on one card. This requires discipline but produces measurable results.

-

Keep your oldest accounts open. Closing an old credit card removes its limit from your total available credit, which instantly raises your overall utilization ratio. Even if you rarely use an older account, keeping it open preserves the credit limit and supports a lower ratio.

-

Convert revolving debt to installment debt. Installment loans, such as a term loan or equipment financing, are not included in your revolving utilization calculation. Moving a large revolving balance to an installment product reduces your reported utilization immediately. This is particularly useful when you carry a persistent balance on a business line of credit.

-

Monitor both personal and business credit reports consistently. Regular credit monitoring prevents surprises during loan applications and helps you catch reporting errors before they damage your score. The SBA recommends this as a core practice for any business planning to apply for financing.

Understanding how these strategies interact with your specific credit profile is part of how to manage business credit over the long term. No single tactic works in isolation. The businesses that maintain the strongest credit profiles combine limit management, timing discipline, and consistent monitoring into a regular financial practice.

Pro Tip: Before applying for any new financing, run a full utilization audit across all revolving accounts. Lenders look at your credit profile at the moment of application. A two-week effort to reduce reported balances can meaningfully improve the terms you receive.

Utilization is considered the easiest credit factor to optimize because it responds quickly to direct action. Unlike payment history, which takes years to build, utilization can shift within a single billing cycle. That speed makes it the highest-leverage lever available to small business owners managing their credit profiles.

Understanding the 5 Cs of credit before applying for financing helps you see exactly where utilization fits within the broader picture lenders evaluate. Capacity, capital, conditions, character, and collateral all interact with your utilization ratio during underwriting.

Key takeaways

Keeping business credit utilization below 30%, with an optimal target of 10%–20%, is the single most controllable action small business owners can take to protect their credit scores and improve financing eligibility.

| Point | Details |

|---|---|

| Calculate across all accounts | Add all revolving balances and divide by total credit limits to get your true overall ratio. |

| Target 10%–20% utilization | Staying in this range signals financial discipline and produces the strongest credit scores. |

| Pay before statement closing | Bureaus record statement-close balances, so paying down debt before that date lowers reported utilization. |

| Increase limits and distribute balances | Requesting higher limits and spreading debt across accounts reduces both per-account and overall ratios. |

| Monitor credit reports regularly | Consistent monitoring catches errors and keeps you prepared for loan applications at any time. |

What most business owners get wrong about credit utilization

After working with small business owners across hundreds of industries since 2009, Capitalforbusiness has seen the same pattern repeat itself. Owners focus entirely on whether they paid on time and completely ignore the balance that was reported on the statement closing date. They pay their bill in full every month and assume their utilization is zero. In reality, their reported utilization may be 60% or higher because they carried a large balance through the statement close.

The second mistake is treating utilization as a one-time fix rather than an ongoing practice. A business owner will reduce their balances before a loan application, get approved, and then let utilization creep back up over the following months. That cycle creates a credit profile that looks good only in snapshots and weak the rest of the time.

The tactic most owners overlook is tracking each creditor's specific reporting schedule. Different lenders report to different bureaus on different days. Once you map those schedules, you can time payments with precision and maintain a consistently low reported ratio without dramatically changing your spending habits. This level of tracking takes about 30 minutes to set up and pays off every single month.

The businesses Capitalforbusiness sees qualify for the best loan terms are not necessarily the ones with the lowest debt. They are the ones who understand how their credit profile looks to a lender at any given moment and manage it accordingly. That awareness, combined with the timing and distribution strategies covered in this article, is what separates businesses that get approved on favorable terms from those that get declined or pay higher rates.

If you want to avoid common debt pitfalls that quietly damage your credit profile, start with your statement closing dates. That single change produces faster results than almost any other credit management action.

— Capital

Ready to put your credit profile to work?

Managing your credit utilization ratio is one part of building a strong financial foundation. The other part is knowing when and how to access capital that supports your growth without straining your revolving credit.

Capitalforbusiness has helped small business owners nationwide access funding since 2009, including small business loans, working capital, and equipment financing. Whether you are looking to consolidate revolving debt, fund a growth opportunity, or simply improve your cash flow position, the right financing product can work alongside your credit management strategy. Explore fast business funding up to $500k and see which options fit your current credit profile and financial goals.

FAQ

What is business credit utilization?

Business credit utilization is the percentage of your total revolving credit limit that your business currently carries as a balance. It is calculated by dividing total revolving balances by total revolving credit limits and multiplying by 100.

What is the ideal credit utilization ratio for a business?

Credit experts at Experian recommend keeping utilization below 30%, with the optimal range being 10%–20% for the best credit scores. Staying consistently within this range signals financial discipline to lenders.

Does paying my bill in full each month eliminate my utilization?

Not necessarily. Creditors typically report your balance at the statement closing date, not the payment due date. If you carry a high balance through the statement close, that figure is what bureaus record, even if you pay it in full afterward.

How can i quickly lower my reported business credit utilization?

The fastest methods are making a payment before your statement closing date, requesting a credit limit increase, and distributing balances across multiple accounts. Utilization responds to direct action within a single billing cycle.

Does opening a new business credit card help my utilization ratio?

Opening a new account increases your total available credit, which lowers your overall utilization ratio if your balances stay the same. Space out new applications to limit the impact of hard inquiries on your credit score.