TL;DR:

- Electricians face cash flow challenges due to delayed customer payments and upfront project costs. Effective working capital management involves precise tracking, structured billing, deposits, and proactive retainage handling to ensure liquidity. When gaps persist, targeted financing options like working capital loans can help bridge short-term timing issues without relying on regular credit.

Running an electrical contracting business means you often spend money long before you collect it. Materials need to be purchased, labor must be paid weekly, and permits cost money upfront. Yet customer payments can lag anywhere from 30 to 120 days after the work is done. This timing gap is exactly what makes the working capital process for electricians so critical. Working capital, formally defined as current assets minus current liabilities, determines whether you can cover payroll next Friday without touching a credit line. This guide breaks down the entire process, from understanding your cash traps to measuring your progress, so you can stop financing your customers' projects with your own money.

Key Takeaways

| Point | Details |

|---|---|

| Working capital is cash, not profit | Available cash excludes AR, retainage, and equipment equity, so plan around actual liquid funds. |

| Deposits reduce self-financing | Collecting 25–50% upfront prevents you from fronting material and labor costs out of pocket. |

| Retainage needs active management | Track release milestones per contract to avoid under-forecasting cash needs on large projects. |

| Billing cadence controls inflow | Monthly progress billing, not end-of-job invoicing, keeps cash arriving throughout the project. |

| Metrics guide improvements | Monitor DSO, DPO, and cash conversion cycle regularly to measure and refine your cash flow process. |

Understanding the working capital process for electricians

Before you can improve anything, you need to understand exactly what working capital means in practical terms for your business. It is not the number your accountant shows on a balance sheet. Available cash excludes AR and equipment equity. Only money sitting in your bank account that is not already committed to a payable counts as true working capital.

For electricians, current assets typically include cash on hand, accounts receivable (AR), material inventory, and deposits paid to suppliers. Current liabilities include accounts payable, payroll obligations, short-term loan payments, and any subcontractor balances owed. The gap between those two numbers tells you how much breathing room you actually have.

The challenge is that several categories eat into that breathing room faster than most electricians expect. Here are the most common working capital traps and their typical financial impact:

| Working Capital Trap | How It Drains Cash | Estimated Impact |

|---|---|---|

| Cash conversion gap | Paying costs 30–120 days before collecting payment | Ties up thousands per active job |

| Fronting materials | Purchasing wire, panels, and fixtures before deposit is collected | $5K–$15K or more per job |

| Retainage holdbacks | 5–10% withheld until project completion | $500K–$1M on a $10M project |

| Slow AR collections | Delayed invoicing or no follow-up process | Extends DSO by 15–30 additional days |

| Material prepayments | Paying suppliers upfront without matching customer deposit | Creates immediate cash shortfall |

Retainage alone deserves special attention. A retainage holdback of 5 to 10 percent might sound small on paper, but on a six-month commercial project, that money is locked away for the entire duration and often longer. Many electricians mentally count it as income when it is actually unavailable cash sitting in someone else's account.

The cash conversion gap compounds these issues. You might be profitable on every job you run, yet still find yourself short on payroll because your receivables have not converted to actual dollars yet. Understanding this distinction is the first step toward fixing it.

Setting up the foundation for better cash flow

Fixing your working capital does not start with financing. It starts with putting the right systems in place so you know where every dollar is at any given moment. Here is what needs to be in place before you can optimize anything.

Accurate job costing. Every job should have its own cost bucket that tracks labor hours, material costs, subcontractor fees, and overhead. Overhead should be allocated at roughly 10 to 15 percent of revenue per job, depending on your business size. Without this, you cannot tell whether a job is draining cash or generating it until the final invoice is paid.

Billing structures built into contracts. Before a job starts, your contract should specify deposit requirements, progress billing milestones, and net payment terms. Structured billing with deposits of 25 to 50 percent significantly improves your ability to predict cash inflows. Do not treat billing as an afterthought. Build it into the agreement before you pick up a single tool.

Retainage tracking by contract. Do not manage retainage from memory. Create a simple spreadsheet or use your project management software to log the retainage amount, release conditions, and expected release date for every active contract. This is the only way to accurately forecast when that cash will actually arrive.

Accounting or project management software. Tools like QuickBooks, Buildertrend, or similar platforms let you monitor job-level cash flow in real time. They also make it easier to see your aggregate AR balance and flag overdue invoices before they become a serious problem.

A cash reserve buffer. This is the most frequently skipped step and the one that causes the most pain.

Pro Tip: Maintain a cash reserve equal to two to three months of operating expenses. This is not idle money. It is your protection against a slow-paying general contractor or an unexpected delay in retainage release, without having to reach for expensive short-term credit.

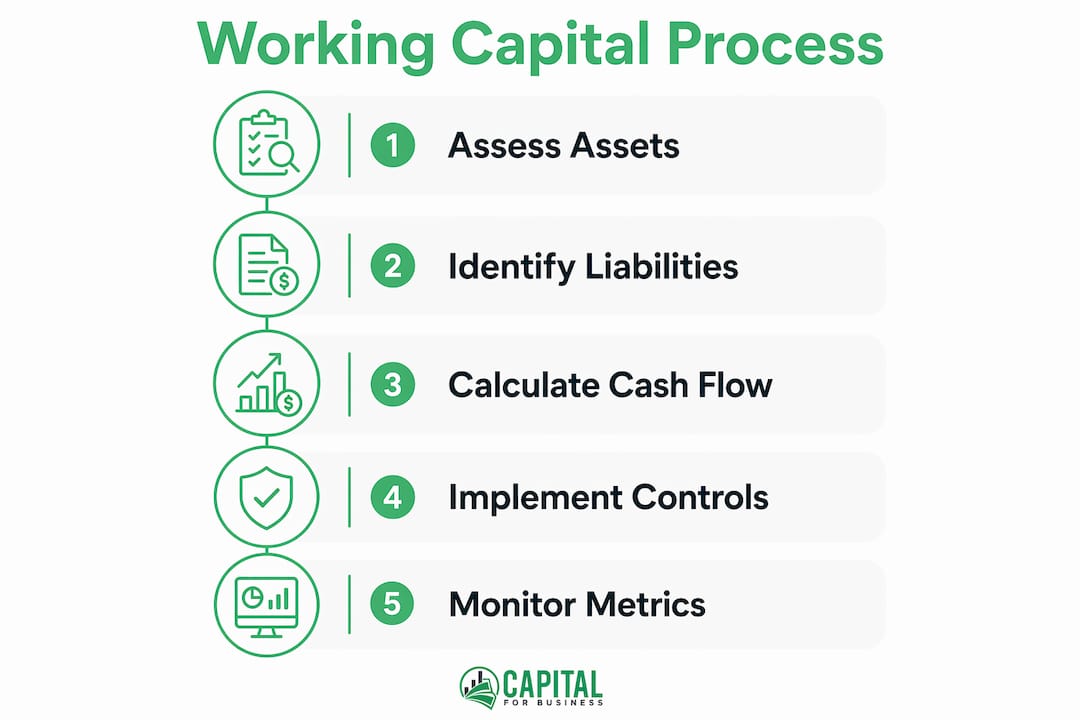

Step-by-step process to manage cash flow on every project

This is where the planning becomes practice. The following steps represent a working sequence you can apply to every new electrical project, from small residential service calls to large commercial installations.

-

Collect a deposit before work begins. Request 25 to 50 percent of the total contract value upfront. This deposit should at minimum cover your initial material purchase and the first week of labor. When you treat deposits as working capital tools, you stop self-financing from day one. Residential customers generally accept this as standard practice. Commercial GCs may push back, but a smaller mobilization fee is often negotiable.

-

Switch to progress billing on projects longer than two weeks. Instead of billing at job completion, send invoices at defined milestones. Typical milestones for electrical contractors include rough-in completion, panel installation, trim-out, and final inspection. Monthly progress billing keeps cash arriving throughout the job rather than in one lump sum at the end.

-

Negotiate supplier payment terms before you order. Talk to your material suppliers about extending payment terms to 45 or 60 days. Many will accommodate contractors with a history of reliable payments. You want to create a situation where your customer pays you before your supplier bill comes due. Aligning payables with collections can even create a negative cash conversion cycle, meaning you collect before you pay out.

-

Invoice immediately after hitting each milestone. Prompt invoicing is one of the simplest cash flow improvements available and one of the most commonly ignored. Every day you wait to send an invoice is a day added to your collection timeline. Set a rule: milestone completed, invoice sent same day.

-

Follow up on unpaid invoices within 48 hours of the due date. Many contractors wait weeks before chasing payment. A short email or phone call within two days of a missed due date signals professionalism and urgency. Automate this reminder if your software allows it.

-

Manage retainage as a separate cash flow category. Log every retainage balance and its release trigger. When a project nears completion, begin the closeout documentation process early so you can request retainage release without delay. On larger commercial jobs, negotiate reduced retainage percentages or phased releases tied to milestone completions rather than full project close.

Pro Tip: For large commercial contracts, ask early whether the GC accepts substitute security, such as a retainage bond, in place of cash holdback. Not every GC will agree, but those who do free up significant working capital throughout the project.

Common mistakes that hurt working capital management

Even electricians with solid systems in place make predictable errors that quietly drain their cash. Recognizing these mistakes is the fastest way to plug the leaks.

-

Treating AR as spendable cash. Your accounts receivable balance is not money in the bank. Until the check clears, it is a promise. Planning expenses around uncollected AR leads directly to payroll shortfalls and overdrafts. Forecasting requires separating liquid cash from AR balances, especially when some of those receivables are in dispute or sitting in long-hold retainage.

-

Underestimating overhead in job costing. Many electricians price jobs based on labor and materials but forget to allocate overhead consistently. When overhead is ignored or guessed, profitable-looking jobs quietly drain cash because the true cost of running the business is not being recovered.

-

Ignoring retainage holdbacks in cash planning. If you have three commercial jobs running simultaneously with 10 percent retainage on each, you could have $50,000 or more locked away for months. Not accounting for that in your cash flow forecast means you will be surprised when the bills arrive.

-

Delaying invoices or skipping deposits. Both behaviors extend the time between spending money and collecting it. Every week of delay on an invoice is typically one additional week before you get paid. Skipping deposits, especially on larger jobs, means you front the entire mobilization cost yourself.

-

Over-relying on short-term financing. Lines of credit and merchant cash advances have their place, but using them repeatedly to cover gaps caused by poor billing practices is expensive. You end up paying interest on problems that better contract terms and billing discipline would have eliminated. Explore options for electrical businesses first, then treat financing as a supplement, not a substitute for process.

-

Failing to use automation for billing and follow-up. Manual invoicing processes introduce delays and human error. A billing workflow that is automated reduces the time between milestone completion and invoice delivery, and helps you track which clients are chronically slow payers.

Measuring whether your cash flow improvements are working

Fixing your process is step one. Knowing whether it is actually working requires regular measurement. These are the metrics that matter most for electricians tracking their financial health.

Days Sales Outstanding (DSO) measures how long it takes to collect payment after invoicing. A lower number is better. For electrical contractors, a DSO under 45 days is a reasonable target. If yours is above 60, your collection process needs attention.

Days Payable Outstanding (DPO) measures how long you take to pay your suppliers. A higher number generally means better cash flow, as long as you are not damaging supplier relationships. A DPO of 30 to 45 days is typical for trades.

Cash Conversion Cycle (CCC) combines both: it equals DSO minus DPO. A lower or negative CCC means you collect faster than you pay, which is the goal. Closing the DSO versus DPO gap directly improves working capital without touching your profit margins.

Here is how typical metrics compare before and after implementing a structured working capital process:

| Metric | Before Process Improvements | After Process Improvements |

|---|---|---|

| Days Sales Outstanding (DSO) | 65–90 days | 30–45 days |

| Days Payable Outstanding (DPO) | 15–20 days | 35–50 days |

| Cash Conversion Cycle (CCC) | 50–70 days | Negative to 10 days |

| Deposit Collection Rate | Under 30% of jobs | 80–100% of jobs |

| Retainage Tracked Per Contract | Rarely | Every active contract |

Beyond these headline numbers, conduct weekly job margin reviews for every active project. A job that looked profitable at the bid stage can quietly erode if labor hours run over or material prices spike. Catching this early, during the job rather than after it closes, gives you time to adjust before the damage compounds.

Set a monthly rhythm as well. Review your job-type margin reports to see which categories of work, residential service, commercial new construction, or industrial maintenance, actually generate the best cash-adjusted returns. Some job types look profitable on paper but carry retainage or slow-pay risk that others do not.

My perspective on working capital in electrical contracting

I have worked with electricians and trade contractors long enough to notice a consistent pattern. The ones who struggle most are not the ones doing bad work or running unprofitable jobs. They are the ones who focus on gross revenue and profit margins while treating cash flow as something that will sort itself out.

It will not sort itself out. Cash flow requires the same discipline as your installation work. You would not rough in a panel without planning the circuit layout first. The same logic applies here.

What I have found is that the biggest single shift electricians can make is separating reported profit from available cash. You can be showing a $200,000 profit on your books at the end of the year and still have $15,000 in your checking account because half your profit is sitting in outstanding AR and retainage. That is not a failure of skill. It is a failure of financial management for electricians, and it is fixable.

Retainage is the part most contractors simply accept as a given. In my experience, that passive approach is costly. Retainage should be negotiated, tracked, and scheduled for release just like any other billing milestone. The contractors who treat retainage as a passive outcome tend to under-forecast their cash needs repeatedly, then turn to credit lines to fill gaps they created themselves.

Weekly margin reviews feel tedious until the first time they catch a job spiraling before it is too late. That early warning is worth more than any financing product on the market. Start there. Build the discipline first, then use external capital to accelerate growth, not to survive.

— Capital

How Capitalforbusiness supports your working capital needs

Even with a disciplined process, timing gaps happen. A general contractor delays a progress payment. A retainage release takes longer than expected. Material prices spike mid-project. When your process is solid but a gap still appears, having access to the right financing makes the difference between absorbing the disruption and losing the job.

Capitalforbusiness has worked with electrical contractors and trade businesses since 2009, providing funding solutions designed for the realities of project-based businesses. From working capital loans up to $500,000 to SBA-backed products through the SBA 7(a) program, the options are built to move quickly when you need them. The SBA Working Capital Pilot Program alone has delivered over $150 million in lending, offering 100 percent financing of direct project costs for qualifying businesses.

If you are an electrician looking to bridge a payment gap, cover a large material purchase ahead of a deposit, or simply build a cash reserve buffer, explore small business loan options tailored to your needs. Capitalforbusiness approves applications faster than traditional banks and works with businesses that banks often turn away.

FAQ

What is working capital for electricians?

Working capital for electricians is the liquid cash available to cover daily operating expenses after accounting for current liabilities. It excludes accounts receivable, retainage, and equipment value since those cannot be spent until converted to cash.

How much deposit should electricians collect upfront?

Electricians should collect a deposit of 25 to 50 percent of the contract value before work begins. This deposit covers initial material purchases and early labor costs, reducing the amount you finance out of pocket.

What is retainage and how does it affect cash flow?

Retainage is a percentage, typically 5 to 10 percent, that a client or general contractor withholds until the project is complete. On large jobs, this can lock up hundreds of thousands of dollars in cash for months, making proactive tracking and negotiation essential.

How do electricians measure cash flow improvement?

Track Days Sales Outstanding, Days Payable Outstanding, and your Cash Conversion Cycle monthly. A decreasing DSO and an increasing DPO together signal that your billing and collection process is improving.

When should electricians consider a working capital loan?

A working capital loan makes sense when a verified timing gap, such as a delayed progress payment or a large material order ahead of a deposit, creates a short-term cash shortfall in an otherwise profitable business. It should supplement a solid billing process, not replace one.