TL;DR:

- Fast access to capital is vital for restaurant survival, enabling quick repairs and preventing closures on thin margins. Various quick funding options, like merchant cash advances and equipment financing, provide capital within days, helping operators respond to emergencies and growth opportunities promptly. Proper planning, discipline, and industry knowledge streamline fast borrowing, ensuring it supports long-term health and competitive advantage.

The restaurant industry operates on razor-thin margins where a single bad week can create a cash crisis. Understanding why fast funding is critical for restaurants goes well beyond avoiding worst-case scenarios. It determines whether you can pay your staff on time, replace a broken walk-in freezer before a Friday dinner rush, or lock in a lease expansion before a competitor does. The real reason restaurants close is not bad food or poor service. 44% of small businesses close primarily because they run out of cash, and in restaurants, the speed at which you access capital is often the deciding factor.

Table of Contents

- Key Takeaways

- Why fast funding is critical for restaurants

- Fast funding options for restaurants

- How funding timing affects operations and growth

- Best practices for smart, fast borrowing

- My perspective on funding speed and restaurant resilience

- Get fast, flexible restaurant funding from Capitalforbusiness

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Cash flow drives survival | Running out of cash is a top closure cause, making fast access to capital a daily operational need. |

| Margins leave little buffer | With pre-tax profits averaging 5-10%, one unexpected expense can push a restaurant into the red. |

| Fast funding options exist | Merchant cash advances and equipment financing can deliver capital in as little as 24-48 hours. |

| Timing directly affects revenue | Every day equipment sits broken or a position stays unfilled translates into real, measurable lost income. |

| Smart borrowing protects growth | Matching the right funding product to a specific need prevents over-borrowing and long-term cash strain. |

Why fast funding is critical for restaurants

The financial pressure a restaurant faces is unlike most other businesses. Revenue can swing dramatically from week to week based on weather, local events, or seasonality. Meanwhile, your fixed costs do not flex. Rent is due regardless of how last Tuesday's dinner service went.

Restaurant profit margins average just 5-10% before taxes. That means on $100,000 in monthly revenue, you might keep $5,000 to $10,000. When a commercial dishwasher breaks down, a key supplier raises prices, or a line cook quits during a busy season, that entire buffer disappears fast. The margin for financial error is almost nonexistent.

Here are the most common unexpected expenses that hit restaurants without warning:

- Equipment failures: Commercial refrigerators, ovens, and fryers are expensive to repair or replace, often costing $5,000 to $50,000 or more for full replacements.

- Sudden labor gaps: Hiring and training replacement staff carries real costs, including recruitment, onboarding, and overtime for remaining staff covering shifts.

- Supply cost increases: Food prices are volatile. A sharp rise in protein costs, dairy, or fresh produce can wipe out projected margins in a single month.

- Lease renewals and buildout demands: Landlords sometimes require improvements or deposits on short notice, especially in competitive markets.

- Regulatory compliance expenses: Health inspections, licensing renewals, or ADA updates can generate unplanned costs that demand immediate payment.

Operational cash flow demands stack on top of these unpredictable costs. Payroll typically comes every one or two weeks. Inventory orders go out weekly. Utilities, credit card processing fees, and linen services all draw from the same pool of working capital. Maintaining adequate cash reserves reduces the risk of closure by cushioning against slow months, but many restaurants simply do not carry enough reserve capital to weather multiple disruptions at once.

This is precisely why access to fast capital functions as a form of business insurance. A restaurant owner who can secure funds within 24 to 48 hours is not just solving an immediate problem. They are protecting weeks of future revenue that would otherwise be at risk.

Pro Tip: Keep a running list of your three most likely financial emergencies and get a rough cost estimate for each. When you know what a compressor replacement or a slow week in January actually costs you, you can size a credit line or reserve accordingly before the crisis hits.

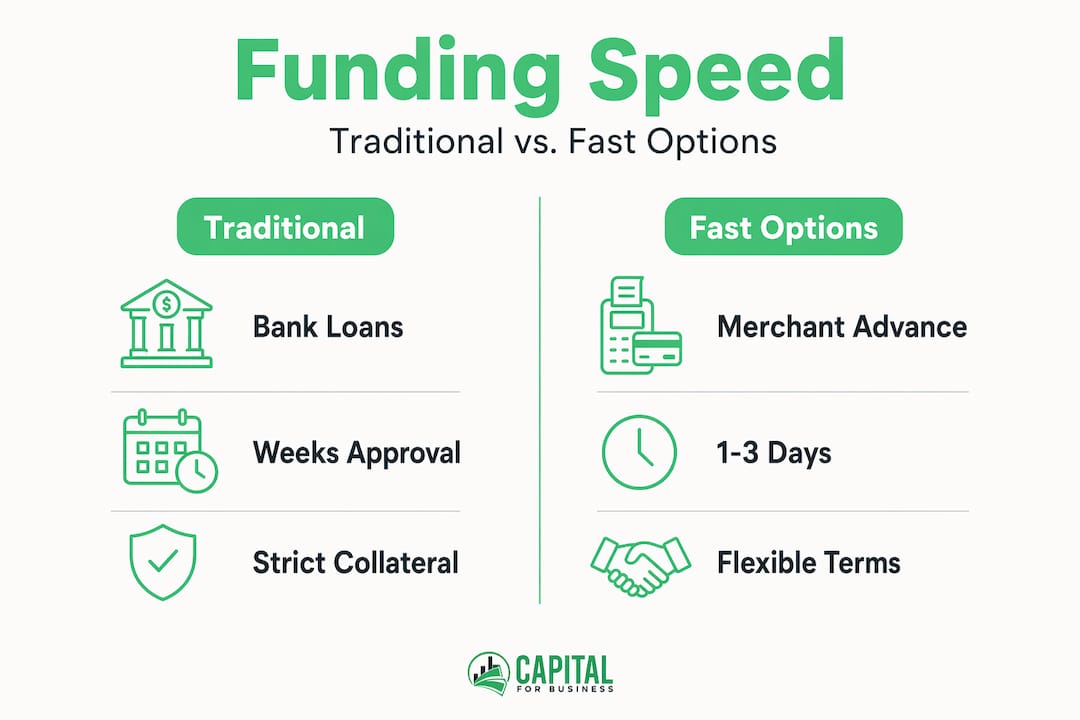

Fast funding options for restaurants

Not all funding products are built for speed. Understanding which options actually deliver capital quickly helps you choose the right tool for the situation instead of defaulting to whatever is most familiar.

Merchant cash advances

A merchant cash advance provides a lump sum of capital upfront in exchange for a percentage of your future daily credit and debit card sales. Merchant cash advances are particularly popular among restaurants because approval requirements are less strict than traditional loans. Your sales history matters more than your credit score, making this a practical option if your credit profile is limited.

Funding through this route often arrives within one to three business days. The repayment adjusts automatically with your sales volume, so slower weeks mean smaller payments, and that flexibility is genuinely useful for businesses with seasonal revenue patterns.

Equipment financing

When your oven fails or your POS system dies, equipment financing targets that specific need directly. Equipment loans can be approved the same day through supplier partners and funded within 24 to 48 hours, compared to traditional bank loans or SBA programs that can take weeks or months. Some alternative lenders have taken speed even further. Fast equipment loan alternatives offer approvals in as little as four hours. The equipment itself often serves as collateral, which removes the need for additional assets and reduces paperwork significantly.

Short-term small business loans

Short-term loans from alternative lenders provide a fixed lump sum with repayment over a defined period, usually three to eighteen months. Approval timelines are much faster than traditional bank loans because alternative lenders focus on recent business performance rather than multi-year tax histories. These loans work well for covering a specific gap, like bridging payroll during a slow month or funding a targeted renovation.

Comparison of common fast funding options

| Funding Type | Typical Approval Speed | Collateral Required | Best Use Case |

|---|---|---|---|

| Merchant cash advance | 1-3 business days | None (sales-based) | Urgent working capital needs |

| Equipment financing | Same day to 48 hours | Equipment itself | Replacing or adding equipment fast |

| Short-term business loan | 24-72 hours | Varies by lender | Bridging cash gaps, targeted projects |

| Business line of credit | 2-5 business days | Often unsecured | Ongoing operational flexibility |

| SBA loan | Weeks to months | Often required | Long-term, lower-cost financing |

Pro Tip: If your restaurant does a high volume of credit and debit transactions, a merchant cash advance will likely offer you a faster approval and fewer documentation requirements than almost any other product. Pull together three to six months of merchant statements before you apply so you can move quickly when you need to.

Alternative lenders have reshaped restaurant financing by prioritizing speed and flexibility over the collateral-heavy requirements that traditionally blocked small operators from getting capital. This shift has genuinely expanded what is available to independent restaurants, food trucks, and smaller chains that would not have qualified under older lending models.

How funding timing affects operations and growth

The consequences of slow funding are not abstract. They play out in lost revenue, damaged customer relationships, and missed opportunities that are often impossible to recover.

Consider the following sequence of events that plays out in restaurants more often than most owners admit:

- Equipment goes down. A commercial refrigerator fails on a Thursday night. The restaurant cannot store perishables safely.

- The decision delay begins. The owner contacts their bank on Friday morning. Loan paperwork is requested. The weekend passes with no resolution.

- Revenue loss accumulates. The restaurant operates at reduced capacity or closes for two days while waiting for funding approval.

- Customer trust erodes. Regulars who came in that weekend and found limited service may not return. Negative reviews appear.

- The repair or replacement finally happens. The loan funds ten days later. But the revenue from that weekend and the lost repeat customers cannot be recovered.

That scenario illustrates exactly why timely funding matters. The cost of waiting is not just the repair bill. It is the compounded loss of revenue, reputation, and customer loyalty.

On the growth side, access to capital enables restaurants to modernize technology, integrate delivery platforms, upgrade kitchen displays, and improve the customer experience in ways that directly affect revenue. A restaurant that can act quickly on a POS system upgrade or a lease expansion opportunity gains a real competitive advantage over one that waits months for traditional financing to process.

"Speed of capital access is often the difference between a restaurant that grows and one that merely survives."

Pro Tip: If you identify a growth opportunity like a neighboring space opening up or a catering contract you want to pursue, contact a lender before you formally commit. Knowing your approval range in advance lets you move with confidence when timing matters.

Urgent funding for restaurants is not only about crisis recovery. It is about staying competitive in a market where conditions shift fast and the operators who can respond quickly are the ones who expand while others stand still.

Best practices for smart, fast borrowing

Getting capital quickly is valuable. Borrowing in a way that supports your long-term financial health is equally important. Speed without discipline can create problems that outlast the original emergency.

Here are the practices that separate restaurant owners who use fast funding effectively from those who end up trapped in a cycle of short-term debt:

- Size your request accurately. Borrow what you actually need, not the maximum you qualify for. Over-borrowing increases your repayment burden during slow periods and reduces your ability to borrow again when you genuinely need it.

- Read the full repayment terms. Factor rates on merchant cash advances and interest rates on short-term loans can vary significantly between lenders. Understand your total repayment amount, not just the monthly payment, before signing.

- Protect your working capital. The right financing structure balances payment size, approval speed, and flexibility with your specific operational goals. A startup restaurant prioritizes liquidity preservation. A multi-location operator may focus on scaling efficiency. Match the product to your stage.

- Build your credit and documentation profile before you need funds. Lenders move faster when your financials are organized. Keep three to six months of bank statements, merchant processing records, and a current profit and loss statement ready to submit at any time.

- Work with lenders who know the restaurant industry. A lender familiar with seasonal revenue cycles, food cost volatility, and the operational reality of running a kitchen will evaluate your application more accurately and offer more appropriate terms than a generalist lender.

- Use a line of credit for recurring needs. If you find yourself needing fast capital repeatedly for the same type of expense, a revolving business line of credit is more cost-effective than taking out individual short-term loans each time.

Restaurant owners can explore small business loan options specifically designed for the speed and flexibility this industry requires. Knowing your options in advance means you never have to make a rushed decision under pressure.

Pro Tip: After you use any fast funding product, review your repayment experience honestly. Did you borrow the right amount? Did the repayment schedule create any strain? Use that information to refine your approach the next time, because in this industry, there will always be a next time.

My perspective on funding speed and restaurant resilience

I have worked with restaurant owners across hundreds of different situations since 2009, from single-location diners in small towns to multi-unit concepts in major metro areas. One pattern shows up repeatedly. The owners who treat fast funding as an operational asset do significantly better than those who treat it as a last resort.

Here is what I have found: most restaurant owners who eventually run into serious financial trouble did not suddenly run out of options. They had options available. What they lacked was a plan to access those options quickly. By the time they started researching lenders and gathering documents, the damage was already accelerating.

The operators who build relationships with lenders before they need them, who know exactly what products they qualify for, and who keep their financial records organized are the ones who can call on Wednesday morning and have capital in their account by Thursday. That difference of a few days versus a few weeks is not a minor convenience. It is the difference between a disruption you absorb and one that derails your business.

I have also seen owners overborrow in a panic and create a repayment burden that made a bad month worse. The discipline to size your request appropriately, even under pressure, is a skill worth developing before you are in crisis mode. Getting fast funding benefits for eateries is not about having a safety net. It is about running your business with the same precision you bring to your menu and your kitchen.

The restaurants that thrive long-term are the ones where the owner thinks about capital access with the same seriousness they give to food cost and labor scheduling.

— Capital

Get fast, flexible restaurant funding from Capitalforbusiness

Capitalforbusiness has served restaurant owners and small business operators since 2009, providing fast access to capital when banks and credit unions are too slow or too restrictive. Whether you need to replace equipment today, cover payroll through a slow stretch, or fund a renovation that will drive more revenue, there is a product designed for exactly that need.

From merchant cash advances that fund based on your sales history to equipment financing up to $250,000 with same-day approval, Capitalforbusiness moves at the speed your restaurant requires. Applications are straightforward, approvals happen fast, and the team understands the financial reality of running a restaurant. You can also explore easy small business loan types to find the product that fits your current situation. If you are ready to stop waiting on slow lenders and start solving the problem, Capitalforbusiness is the place to start.

FAQ

Why does funding speed matter so much for restaurants?

Restaurants operate on thin margins averaging 5-10%, meaning a single disruption like equipment failure or a cash shortfall can create an immediate operational crisis. Fast access to capital prevents short-term problems from becoming permanent closures.

What is the fastest funding option for restaurant owners?

Equipment financing through alternative lenders can be approved in as little as four hours and funded within 24 to 48 hours. Merchant cash advances typically fund within one to three business days and require minimal documentation.

How do merchant cash advances work for restaurants?

A merchant cash advance provides upfront capital in exchange for a percentage of future daily card sales, with repayment drawn automatically until the balance is settled. This makes them practical for restaurants with strong sales volume but limited credit history.

How much should a restaurant borrow in an emergency?

Borrow the amount that covers the specific need, not the maximum you qualify for. Over-borrowing increases repayment pressure during slow periods and limits your ability to access capital again when a future need arises.

Can fast funding support restaurant growth, not just emergencies?

Yes. Access to quick capital allows restaurants to invest in technology upgrades, expand locations, pursue catering contracts, and respond to market opportunities before competitors do. Fast funding supports both crisis recovery and deliberate growth planning.