TL;DR:

- Most restaurant owners view loans as a last resort, but strategic borrowing supports sustainable growth during scale-up. Lenders seek financial discipline and clear plans, emphasizing metrics like EBITDA to assess repayment capacity. Using appropriate financing early enables operational improvements, safeguards existing value, and signals professionalism to stakeholders.

Most restaurant owners think of loans as a last resort, something you seek when cash runs out or sales drop. That assumption can cost you dearly. Loans can be particularly important for funding changes that protect or restore your ability to generate revenue during scale-up, not just for patching holes in a budget. Strategic borrowing, planned well before strain appears, gives you the capital to invest in systems, people, and infrastructure that support stable, lasting growth rather than scrambled, reactive expansion.

Table of Contents

- Why loans are essential for sustainable restaurant growth

- Types of loans and alternative financing for restaurants

- Costs, risks, and repayment: Comparing loans vs. cash advance solutions

- Best practices for funding a growth-ready restaurant

- What many restaurant owners get wrong about loans

- Explore fast, flexible funding for your restaurant's growth

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Loans fund sustainable growth | Smart borrowing enables upgrades, staffing, and expansion while protecting revenue during business transitions. |

| Alternatives have trade-offs | Merchant cash advances and other fast funding can cost far more than traditional loans, especially in long-term cash flow impact. |

| Preparation secures approval | Strong financials, realistic projections, and operational discipline increase your chances for favorable loan terms. |

| Timing is strategic | Seeking loans before growth strain—during proactive planning—offers the best foundation for stable scaling. |

Why loans are essential for sustainable restaurant growth

Now that we've set the strategic context, let's break down exactly why loans matter so much when scaling up.

A common misconception is that profitable restaurants don't need outside funding. The reality is more nuanced. Even a high-revenue location can find itself short on working capital when it is simultaneously managing a renovation, onboarding new staff, and absorbing higher food costs. Loans don't signal weakness. They signal that you are serious about growing on a structured, financially sound foundation. Understanding how a small business loan can support growth reveals just how many operational scenarios benefit from outside capital.

"Loans help bridge the gap for inventory, build-out costs, and operational system investments needed for scale-up." — MarginEdge Hospitality CFO Podcast

Here are the most common and impactful ways restaurant operators use loan capital during periods of growth:

- New location build-outs: Securing a lease is just the beginning. Construction costs, permitting, equipment installation, and initial payroll add up quickly before the first customer walks through the door.

- Equipment upgrades: Commercial kitchen equipment is expensive. A single high-capacity oven or refrigeration system can run tens of thousands of dollars, and outdated equipment slows service, increases energy costs, and raises the risk of mid-service breakdowns.

- Inventory expansion: Scaling up volume means stocking more ingredients. That ties up cash before sales have a chance to replenish it.

- Operational system improvements: Point-of-sale systems, scheduling software, and inventory management platforms all require upfront investment but pay back consistently over time.

- Renovations and rebrands: Refreshing a dining room or updating your brand identity takes capital, and delaying this work can mean losing customers to competitors who invest in their spaces.

Lenders who specialize in restaurant financing don't just want to hear a compelling story about growth potential. They want to see financial discipline. Revenue history, expense ratios, and profitability metrics all factor into underwriting decisions. Exploring your restaurant business loan options early, before you urgently need capital, gives you time to prepare the financial documentation that makes approval more straightforward.

Pro Tip: Track your EBITDA (earnings before interest, taxes, depreciation, and amortization) consistently across all locations. This is one of the primary figures lenders examine to determine how much debt your business can realistically service. A strong EBITDA figure gives lenders confidence that you can repay without jeopardizing day-to-day operations.

Types of loans and alternative financing for restaurants

Having established loans' importance, it's key to understand which type suits which stage and goal in your growth journey.

Not all financing products are built the same, and choosing the wrong one can create cash-flow pressure at exactly the wrong moment. Restaurant operators have access to a broad range of products, from government-backed loans to flexible alternative financing. The right choice depends on your timeline, credit profile, growth stage, and risk tolerance.

Conventional loan types

- SBA loans: The Small Business Administration offers several loan programs, with the SBA 7(a) being the most commonly used for restaurant growth. These loans can fund up to $5 million and carry competitive interest rates, but they require detailed documentation and can take several weeks to close. Complex SBA deals rely on owner experience, defensible projections, and careful risk management. They reward operators who have kept clean books and can demonstrate a clear plan for the funds.

- Term loans: A lump sum repaid over a fixed period with a set interest rate. Predictable and straightforward, these work well for specific, well-defined projects like buying equipment or funding a build-out.

- Lines of credit: A revolving credit facility that you draw from as needed and repay on a rolling basis. This is particularly useful for managing seasonal revenue swings or covering short-term inventory gaps.

Alternative financing products

- Merchant cash advances (MCAs): A lump sum provided in exchange for a percentage of future sales. Fast to access and requires less documentation, but carries higher effective costs.

- Equipment financing: Loans or leases specifically tied to equipment purchases, where the equipment itself serves as collateral. This reduces lender risk and often results in more favorable terms.

- Revenue-based loans: Repaid as a fixed percentage of monthly revenue, which gives operators some flexibility when sales fluctuate.

For a thorough breakdown of which product fits which scenario, this restaurant loan guide walks through current options in detail. If your customers would benefit from financing at the point of sale, understanding available consumer financing options can also open new revenue opportunities.

| Financing type | Approval speed | Requirements | Cost level | Flexibility |

|---|---|---|---|---|

| SBA loan | Slow (weeks to months) | High | Low to moderate | Low |

| Term loan | Moderate | Moderate | Moderate | Low |

| Line of credit | Moderate | Moderate | Moderate | High |

| Equipment financing | Moderate | Low to moderate | Low to moderate | Low |

| Merchant cash advance | Fast (days) | Low | High | High |

| Revenue-based loan | Fast to moderate | Low to moderate | Moderate to high | High |

Pro Tip: Merchant cash advances offer speed, but that speed comes at a cost. The factor rates used to calculate repayment can translate to effective annual percentage rates well above 40%, and sometimes much higher. Use MCAs strategically for short, high-return opportunities rather than as a default funding source.

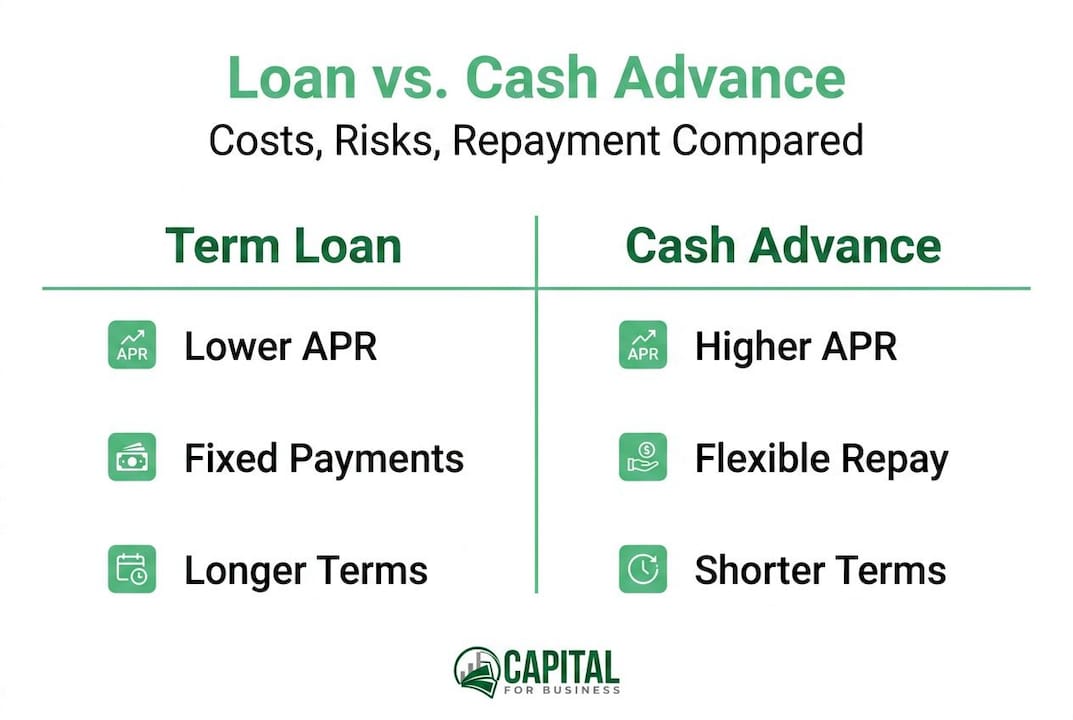

Costs, risks, and repayment: Comparing loans vs. cash advance solutions

Next, it's vital to examine the stakes: how does the cost and risk of different financial products impact your bottom line?

Approval speed is easy to get excited about. But speed is only one variable in a much larger equation. The true cost of capital, how repayment structures interact with your cash flow, and the risk that comes with daily deductions from your revenue all deserve careful analysis before you sign.

Merchant cash advances are often marketed for speed but can be substantially more expensive and repaid via sales holdbacks. That means a percentage of every card transaction is routed to the lender before it ever reaches your account. On a busy weekend this might feel manageable, but during a slow month it can squeeze your operating budget in ways that are hard to plan around.

"The total repayment amount on a merchant cash advance can be 20% to 50% higher than the original advance, depending on the factor rate and repayment term."

Here is a side-by-side look at how conventional loans and MCAs compare across the factors that matter most:

| Factor | Conventional term loan | Merchant cash advance |

|---|---|---|

| Typical APR | 6% to 25% | 40% to 150%+ |

| Repayment structure | Fixed monthly payments | Daily or weekly sales holdback |

| Collateral required | Often yes | No |

| Credit score impact | Yes | Minimal |

| Approval timeline | Days to weeks | 24 to 72 hours |

| Total repayment cost | Predictable | Can vary significantly |

| Cash-flow predictability | High | Lower (tied to sales volume) |

Understanding these differences is not just an academic exercise. It directly affects how much money you actually keep and reinvest in your business. For a full breakdown, this guide on restaurant financing options explained provides detailed comparisons across multiple product types.

Here are the key risks to evaluate before choosing any financing product:

- Daily repayment pressure: When your cash advance is repaid as a daily holdback, your net deposit every day is smaller than your gross sales. During slow periods, this can make it feel like you are running just to stay in place.

- Stacking advances: Some operators take a second or third MCA before paying off the first. This can create a cycle of escalating costs that is genuinely difficult to exit.

- Hidden fees: Origination fees, prepayment penalties, and administrative charges can add meaningfully to the total cost of any loan product. Always request a full fee schedule before accepting an offer.

- Build-out risk: If you are using a loan to open a new location, delays in construction or permitting can push back your revenue start date while your loan repayment clock is already running.

For a detailed look at how the MCA process actually works for restaurant operators, reviewing the restaurant MCA process guide can help clarify what to expect. If you are new to MCAs entirely, starting with understanding merchant cash advances for small businesses gives a solid foundation before you compare offers.

Pro Tip: Always calculate the true APR of any financing product, not just the stated rate or factor rate. Ask the lender to provide the total repayment amount and the repayment timeline, then divide accordingly. This one step alone can prevent costly financing mistakes.

Best practices for funding a growth-ready restaurant

To maximize financing, let's move from options and risks to practical steps for making the right loan work for your restaurant.

Being ready to grow is not just about finding a location or hiring staff. It's about demonstrating to a lender, and to yourself, that your financial foundation can support expansion without cracking under pressure. Lenders underwrite on financial readiness and risk, not just on growth narratives. Financial discipline, metrics, and defensible plans are what move applications forward.

Preparing a strong loan application: A step-by-step checklist

- Gather at least two years of financial statements. This includes profit and loss statements, balance sheets, and cash flow statements for all active locations. Lenders want to see consistency and trend lines, not just a single strong year.

- Calculate and document your EBITDA. Know this number cold. It tells lenders how much operating income your business generates before debt and non-cash charges, and it directly influences how much you can borrow.

- Build a detailed use-of-funds plan. A vague plan like "expand the restaurant" is not enough. Break it down by line item: $80,000 for equipment, $150,000 for build-out, $40,000 for initial inventory, and so on. Specificity signals seriousness.

- Prepare a 12 to 24-month cash flow projection. Show how the loan will be repaid, and demonstrate that you have accounted for a conservative revenue scenario, not just your best-case numbers.

- Check and improve your personal and business credit. Both often factor into underwriting. Resolve any open collections, reduce credit utilization, and ensure your business credit file is accurate before applying.

- Organize legal and operational documents. Business licenses, lease agreements, franchise agreements (if applicable), and tax returns are commonly requested. Having these ready speeds up the process significantly.

Once you secure financing, how you deploy the capital is just as important as how you obtained it. Here are best practices for putting loan funds to work effectively:

- Prioritize revenue-generating investments first. Equipment that increases output, systems that reduce labor costs, and renovations that improve customer experience all generate measurable returns. These should come before cosmetic upgrades.

- Build a cash reserve from loan proceeds. Allocating 10% to 15% of a loan toward an operational buffer protects you if revenue ramps more slowly than projected.

- Track spending against your use-of-funds plan. Deviating significantly from your stated plan can complicate future borrowing and create internal accountability gaps.

- Monitor cash flow weekly during the growth phase. Growth periods are inherently unpredictable. Weekly reviews catch problems before they become crises.

- Communicate proactively with your lender. If something unexpected happens during repayment, reaching out early gives you far more options than waiting until you miss a payment.

Reviewing top small business loans for restaurants gives you a practical reference point for current products that match these best practices, with options suited to different growth stages and credit profiles.

What many restaurant owners get wrong about loans

Stepping back, here's a candid look at why the best operators think differently about restaurant lending.

There is a persistent belief in the restaurant industry that borrowing is reactive, something you do after things go wrong or after a growth opportunity has already materialized and demands immediate funding. We've seen this pattern play out repeatedly since 2009, working with operators across hundreds of industries. The owners who struggle most with financing are almost never the ones who borrowed too early. They are the ones who waited too long.

The savviest restaurant operators treat loans as infrastructure, not rescue operations. They secure a line of credit before they need it, because they know that applying from a position of strength, when cash flow is healthy and metrics are strong, produces far better terms than applying under pressure. They use loan capital to upgrade inventory management systems before a second location opens, not after the chaos of an unprepared launch reveals the gaps. They fund staff training programs and technology integrations during a stable period, so that growth doesn't expose structural weaknesses.

There's also a misconception about what loans actually protect. Many operators think in terms of location count: loans help you open more restaurants. That's true, but it's an incomplete picture. A well-timed loan protects your existing business value just as much as it creates new value. If a key piece of kitchen equipment fails and you have no reserves, you lose revenue every day it's down. If your point-of-sale system is outdated and can't integrate with delivery platforms, you leave revenue on the table. These aren't dramatic emergencies. They're slow drains that loans can prevent.

The operators who get the most from financing are those who think about readiness first and expansion second. They ask, "Is our current operation strong enough to withstand the pressure of growth?" before they ask, "How do we fund the next location?" Understanding the full range of restaurant financing options and when to use each one is what separates operators who scale successfully from those who scale and then scramble.

Loans aren't just financial tools. They're a signal. A restaurant owner who approaches a lender with clean books, a clear plan, and documented metrics is signaling to the market, to partners, to suppliers, and to future employees, that this is a professionally managed operation. That reputation compounds over time.

Explore fast, flexible funding for your restaurant's growth

If you're ready to transform insight into action, here's how to take the first step toward growth-focused funding.

Capital for Business has worked with restaurant owners and operators across North America since 2009, providing financing solutions that fit real growth timelines, not just ideal ones. Whether you need a conventional loan for a planned expansion or faster alternative financing to capitalize on an immediate opportunity, we offer products built around your business needs.

From exploring easy business loan types to understanding how the MCA funding process works for restaurant operators, we give you the information and access you need to make confident decisions. Our team moves quickly, works transparently, and focuses on finding terms that support your cash flow rather than strain it. When you're ready to move forward, Capital for Business is ready to help you take the next step with financing that matches where your restaurant is going.

Frequently asked questions

How do I know which loan is right for my restaurant?

Assess your growth goals, timeline, and cash flow before comparing conventional loans, SBA options, or alternatives like merchant cash advances. Selecting financing based on readiness, risk, and operational need leads to better long-term outcomes than choosing based on speed alone.

What metrics do lenders look for on a restaurant loan application?

Lenders focus on EBITDA, revenue history, and a clear plan for how funds will be used. Strong metrics and defensible projections signal financial readiness and significantly improve your odds of approval at favorable terms.

Are merchant cash advances a smart choice for quick capital?

MCAs can provide fast funding, but they are often much more expensive than traditional loans over the repayment period and are repaid through frequent sales holdbacks. Always compare total costs, not just approval speed, before committing.

When is the best time to apply for a restaurant growth loan?

Apply before financial strain appears, ideally when you are actively planning major upgrades or expansion and your metrics show solid performance. Securing loans when planning, rather than at a moment of crisis, gives you access to better terms and a stronger negotiating position.