TL;DR:

- Merchant financing provides small businesses with fast, flexible funding based on sales volume rather than credit. Repayments adjust automatically with daily sales through a holdback, offering a cash flow-friendly alternative to traditional loans. However, it often comes at higher effective costs, making thorough comparison essential before acceptance.

Merchant financing is a form of business funding where a lender provides an upfront lump sum repaid through a percentage of future card sales rather than fixed monthly payments. This structure separates it from every traditional loan product a bank offers. The two most common forms are merchant cash advances (MCAs) and payment processor financing, offered by companies like Stripe, Square, and PayPal. For small business owners who need fast capital without the rigid repayment schedule of a conventional loan, merchant financing explained in plain terms comes down to one idea: your repayment moves with your revenue, not against it.

What is merchant financing and how does it work?

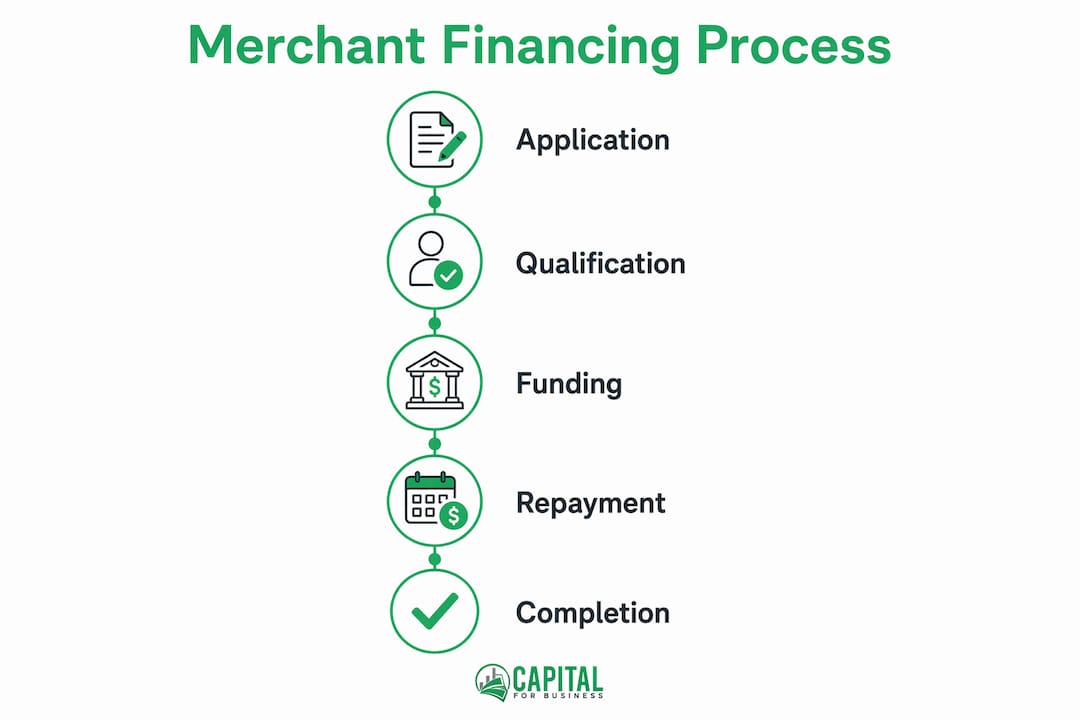

Merchant financing works through a straightforward three-stage process: application, funding, and automatic repayment. Understanding each stage helps you decide whether this product fits your business before you sign anything.

1. Application and qualification

Unlike a bank loan, underwriting focuses on sales volume rather than your credit score or collateral. Lenders typically review three to six months of credit and debit card processing statements to assess your average monthly revenue. This means a business with a thin credit file but consistent card sales can still qualify. Most providers ask for basic business documentation, a few months of bank statements, and proof of card processing activity.

2. Funding

Once approved, funding arrives fast. Stripe, for example, deposits funds within 24 to 48 hours of approval. Many independent MCA providers match that pace. This speed makes merchant financing one of the few options that can cover a payroll gap or an urgent inventory purchase without a week-long wait.

3. Repayment via holdback

Repayment happens automatically through a mechanism called a holdback. Each day your card processor settles transactions, a fixed percentage of that day's sales goes directly to the lender. That percentage, typically between 10% and 20%, is agreed upon upfront and does not change. What changes is the dollar amount you pay each day, because it depends entirely on how much you sold.

Here is why that matters in practice. On a strong Saturday in December, a retail store might process $8,000 in card sales and send $1,200 to the lender. On a slow Tuesday in January, the same store processes $1,500 and sends only $225. A fixed monthly loan payment would demand the same amount regardless of which day it is. Merchant financing adjusts automatically, which is the core flexibility benefit that draws small business owners to this product.

Pro Tip: Before accepting any merchant financing offer, calculate the total repayment amount, not just the holdback percentage. Divide the total payback amount by the advance amount to find the factor rate, then compare that cost against a traditional loan's APR to make an informed decision.

What are the benefits and drawbacks of merchant financing?

Merchant financing offers genuine advantages for the right business, but it also carries real costs that deserve honest attention. Comparing it directly to traditional small business loans reveals where it wins and where it falls short.

Benefits worth considering

- Fast qualification. Approval decisions often come within hours because lenders prioritize recent sales data over credit history. Businesses that banks routinely decline can access capital through this channel.

- No fixed payment pressure. Because repayment is tied to sales volume, slow months do not trigger missed payments or penalties. The repayment simply takes longer.

- No collateral required. Most merchant financing products are unsecured. You do not pledge equipment, real estate, or inventory to access the funds.

- Speed of funding. Capital can arrive in one to two business days, making it one of the fastest funding options available to small businesses.

Drawbacks that require honest evaluation

- High effective cost. Merchant cash advances often carry effective rates exceeding 300% APR. That figure reflects how expensive short-term, high-frequency repayment structures become when expressed as an annualized rate. A business borrowing $50,000 with a factor rate of 1.35 repays $67,500 total, regardless of how quickly it happens.

- Cash flow strain during slow periods. While repayments slow down when sales drop, they do not stop. A business already operating on thin margins may find even a reduced holdback difficult to absorb.

- Limited regulatory protection. Traditional loans carry clear consumer protections. Merchant financing has historically operated in a grayer area, though that is changing.

Pro Tip: If your business has seasonal revenue swings, merchant financing can actually outperform a fixed-rate loan during your slow season. Model both scenarios using your actual monthly sales data before deciding.

Merchant financing vs. traditional small business loans

| Feature | Merchant financing | Traditional bank loan |

|---|---|---|

| Qualification basis | Recent card sales volume | Credit score, collateral, financials |

| Funding speed | 1 to 2 business days | 1 to 4 weeks |

| Repayment structure | Percentage of daily card sales | Fixed monthly payment |

| Collateral required | No | Often yes |

| Effective cost | Higher (factor rates, not APR) | Lower (regulated APR) |

| Credit impact | Minimal reporting | Reported to credit bureaus |

| Best for | Short-term cash flow gaps | Long-term capital investment |

The table above makes the tradeoff clear. Merchant financing wins on speed and accessibility. Traditional loans win on cost and long-term affordability. The right choice depends on how urgently you need capital and how much that urgency is worth to your business.

What merchant financing options are available for small businesses?

The merchant financing market has expanded well beyond the original MCA model. Small business owners today have three distinct categories to evaluate.

Merchant cash advances from independent providers

An MCA is technically not a loan. The provider purchases a portion of your future receivables at a discount, giving you cash today in exchange for a larger amount collected over time through the holdback. Independent MCA companies operate outside the traditional banking system, which is why they can fund businesses that banks reject. Capitalforbusiness offers merchant cash advances up to $500,000, with funding structured around your actual card processing volume. Deal sizes typically range from $5,000 to $500,000, and factor rates vary based on industry, sales consistency, and time in business.

Payment processor financing

Square, PayPal, and Stripe each offer their own financing products built directly into their processing platforms. The key advantage here is integration. Repayment is deducted automatically from transactions processed through the same platform, eliminating any manual payment step. Stripe Capital, for instance, offers pre-approved offers to eligible merchants based on their existing processing history, with no separate application required. The tradeoff is that you must already process payments through that provider, and funding limits are often lower than what independent MCA companies offer.

Revenue-linked and Pay-As-You-Sell advances

An emerging model takes the MCA concept further by linking repayments to real-time sales data rather than a fixed holdback percentage. JaiDee and Seedflex launched Thailand's first Pay-As-You-Sell advance specifically to address SME credit gaps in digital commerce. This model adjusts repayment amounts dynamically based on actual daily revenue, not a predetermined percentage. While still rare in the U.S. market, this structure represents the direction merchant financing is heading as more businesses operate through digital sales channels.

Here is a quick comparison of the three main options:

| Option | Best for | Typical funding speed | Repayment method |

|---|---|---|---|

| Independent MCA | Businesses needing large advances | 1 to 2 business days | Daily holdback from card sales |

| Processor financing | Existing platform users | 24 to 48 hours | Auto-deducted from transactions |

| Pay-As-You-Sell | Digital commerce businesses | Varies by provider | Dynamic, real-time revenue-linked |

Understanding how merchant cash advances work for your specific business type is the starting point for choosing between these options.

What regulatory and legal nuances affect merchant financing in 2026?

Merchant financing has operated with less regulatory oversight than traditional lending for most of its history. That is changing, and small business owners need to understand what protections now exist and where gaps remain.

California's DFPI disclosure rules

California's Department of Financial Protection and Innovation (DFPI) implemented rules effective October 1, 2023, that require MCA providers to disclose terms clearly and prohibit unfair practices. Providers must now present the total repayment amount, the holdback percentage, and an estimated repayment timeline in plain language before a business signs. California also established a complaint channel for businesses that believe they were misled. This is a meaningful shift. Before these rules, some providers buried critical cost information in dense contract language, making it difficult for business owners to compare offers accurately.

The CFPB's uncertain position on MCAs

At the federal level, the Consumer Financial Protection Bureau (CFPB) created significant compliance ambiguity in 2025 when it retracted its 2023 position treating MCAs as credit under the Equal Credit Opportunity Act (ECOA). The CFPB had previously required MCA providers to report data under Section 1071 of the Dodd-Frank Act, which would have brought MCAs under the same reporting and anti-discrimination framework as traditional loans. By retracting that position, the CFPB left the credit classification of MCAs open, meaning the question of whether federal lending protections apply to MCAs remains unresolved.

"The CFPB leaves future credit classification open, creating ongoing compliance ambiguity for both providers and borrowers in the merchant cash advance market." — JD Supra analysis of CFPB's retracted position

What this means for you as a business owner is practical. In California, you now have clear disclosure rights. In most other states, you are still largely relying on contract terms and your own due diligence. Reading the full agreement before signing, asking for a plain-language summary of total repayment costs, and comparing at least two or three offers are not optional steps. They are necessary ones given the current regulatory environment.

The trajectory is toward more regulation, not less. Several other states are considering disclosure requirements similar to California's. Businesses that understand these rules today are better positioned to recognize fair terms and flag problematic ones.

Key takeaways

Merchant financing suits businesses with consistent card sales that need fast, flexible capital without the rigid structure of a traditional bank loan.

| Point | Details |

|---|---|

| Definition and repayment | Merchant financing delivers upfront cash repaid through a daily percentage of card sales, not fixed monthly payments. |

| Qualification advantage | Lenders assess recent sales volume rather than credit score, making approval accessible for businesses banks often decline. |

| Cost tradeoff | Effective costs are higher than traditional loans, sometimes exceeding 300% APR, so total repayment must be calculated before signing. |

| Options available | Independent MCAs, processor financing from Square or Stripe, and emerging Pay-As-You-Sell models each serve different business profiles. |

| Regulatory awareness | California requires clear disclosures from MCA providers; federal protections remain uncertain, making personal due diligence critical. |

My honest assessment of merchant financing for small businesses

Working with small business owners across hundreds of industries since 2009, I have seen merchant financing used brilliantly and used poorly. The difference almost always comes down to one thing: whether the business owner understood the total cost before signing.

Merchant financing is genuinely well-suited to businesses with fluctuating revenue. A restaurant that does 60% of its monthly sales on weekends, a retail shop with a strong holiday season, or a contractor who invoices in cycles rather than steady monthly increments can all benefit from a repayment structure that moves with their cash flow. The flexibility tied to sales receipts reduces the risk of a missed payment during a slow stretch, which is a real operational advantage.

Where I see businesses get into trouble is when they use merchant financing to cover ongoing operating losses rather than a temporary cash flow gap. An MCA is not a substitute for profitability. If your business is consistently spending more than it earns, a high-cost advance accelerates the problem rather than solving it. The total cost and repayment terms must be weighed carefully against what the capital will actually produce.

My recommendation is to treat merchant financing as one tool in a broader funding strategy. Use it for specific, short-term needs where the speed and flexibility justify the cost. For longer-term capital needs, explore business funding solutions that carry lower effective rates. And always compare at least two offers before committing. The terms across providers vary more than most business owners realize, and a few hours of comparison can save thousands of dollars in total repayment costs.

— Capital

How Capitalforbusiness supports your merchant financing needs

Capitalforbusiness has been helping small businesses access capital since 2009, and merchant financing is one of our most requested products.

Whether you need a merchant cash advance up to $500,000 or want to explore the full range of easy small business loan options available to you, Capitalforbusiness makes the process fast and straightforward. We work with businesses in hundreds of industries nationwide and in Canada, and we specialize in meeting needs that banks and credit unions cannot. Applications take minutes, funding can arrive within one to two business days, and our team walks you through every term before you sign. If you are ready to explore what merchant financing can do for your business, start your application today.

FAQ

What is a merchant cash advance?

A merchant cash advance is a type of merchant financing where a provider purchases a portion of your future card sales at a discount, giving you upfront cash repaid through a daily holdback from transactions. It is technically a purchase of receivables, not a loan, which is why it operates under different regulations than traditional bank products.

How fast can I get merchant financing?

Most merchant financing providers fund approved businesses within one to two business days, with processor-based options like Stripe Capital sometimes funding within 24 hours. Speed depends on how quickly you submit documentation and how fast the provider processes your sales history.

Is merchant financing right for me?

Merchant financing works best for businesses with consistent credit and debit card sales that need fast capital without fixed monthly payment obligations. If your revenue fluctuates seasonally or week to week, the flexible repayment structure offers a real advantage over traditional loans.

What are the requirements for merchant financing?

Most providers require three to six months of card processing statements, a minimum monthly revenue threshold (often $5,000 to $10,000), and at least six months to one year in business. Credit score requirements are minimal compared to bank loans, making this accessible to a wider range of businesses.

How does merchant financing differ from a traditional business loan?

Traditional loans carry fixed monthly payments, require collateral and strong credit, and take weeks to fund. Merchant financing requires no collateral, qualifies based on sales volume, funds in days, and collects repayment as a percentage of daily card transactions rather than a fixed amount each month.