TL;DR:

- Commercial credit enables businesses to access goods, services, or capital now and repay later, independent of personal credit. Building a strong commercial credit profile requires deliberate actions like opening vendor accounts that report to bureaus and monitoring reports regularly. Most entrepreneurs mistakenly assume profit alone establishes solid credit, but proactive management is essential to secure favorable financing terms.

Commercial credit is a pre-approved financial arrangement that allows a business to obtain goods, services, or capital now and repay the amount at a later date. The industry also refers to this as business credit, though the term "commercial credit" is standard in lending and vendor contexts. For small business owners, this arrangement covers everything from a supplier's Net 30 payment terms to a bank-issued line of credit. Bureaus like Dun & Bradstreet and Experian Business track your company's payment behavior and assign scores that directly affect your loan rates, vendor terms, and deposit requirements. Understanding how commercial credit works is one of the most practical steps you can take to expand your financing options.

What is commercial credit and how does it work?

Commercial credit allows businesses to access goods, services, or capital immediately and pay later. This covers two broad categories: trade credit from vendors and lender credit from financial institutions. Trade credit is the arrangement where a supplier ships your inventory today and gives you 30, 60, or 90 days to pay. Lender credit includes formal products like term loans, business lines of credit, and equipment financing.

The mechanics are straightforward. A vendor or lender evaluates your business's creditworthiness, sets a credit limit, and extends terms. You use the credit, make payments on schedule, and your payment behavior gets reported to commercial credit bureaus. Those bureaus compile your history into a report that future lenders and vendors use to decide whether to extend credit and on what terms.

Business credit is tied to your EIN, not your Social Security number. That separation is the foundation of a healthy commercial credit profile. It means your business can build its own financial reputation, independent of your personal finances.

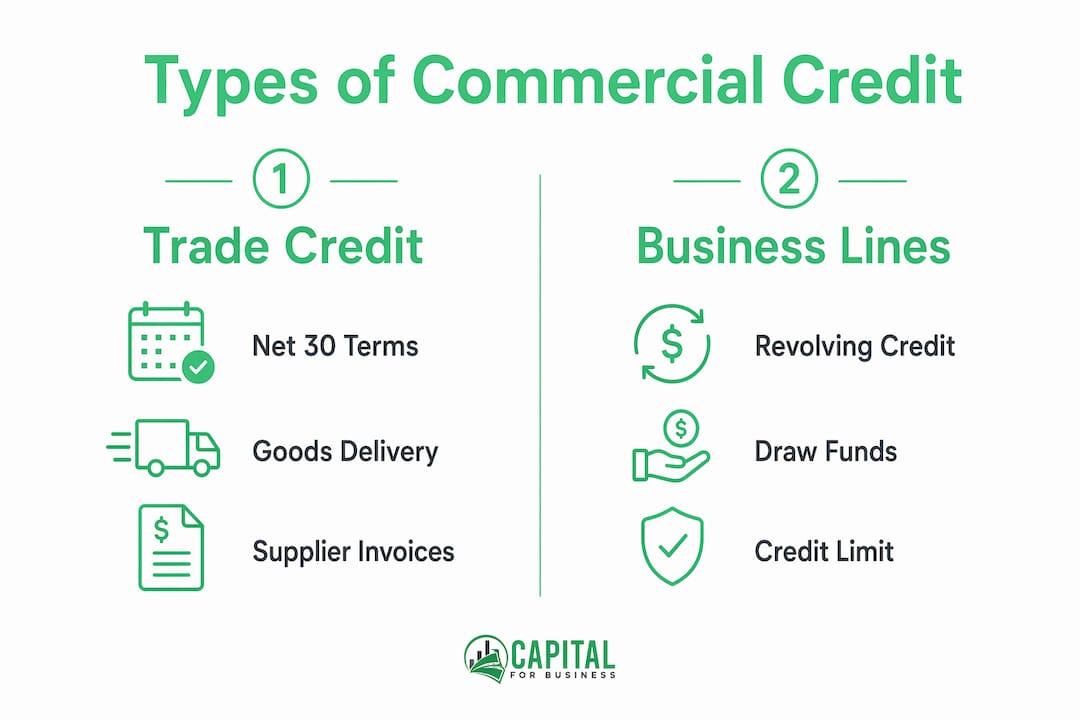

What types of commercial credit exist?

Three primary types of commercial credit serve different operational needs. Each carries distinct terms, risk profiles, and use cases.

Trade Credit is the most common form. A supplier delivers goods and invoices you with Net 30 or Net 60 terms. You have that window to pay without interest. This type of credit directly supports inventory purchasing and day-to-day supply chain management. A retail shop ordering merchandise from a wholesale distributor on Net 30 terms is using trade credit.

Business Lines of Credit function as revolving credit. A lender approves a maximum limit, and you draw funds as needed, repay, and draw again. This structure suits businesses with variable cash flow, like a landscaping company that needs to cover payroll during slow winter months and repays when spring contracts come in.

Commercial Term Loans deliver a fixed lump sum repaid over a set schedule, typically with a fixed or variable interest rate. These work best for defined investments: buying equipment, funding a renovation, or acquiring another business.

| Credit Type | Typical Terms | Best Use | Risk Profile |

|---|---|---|---|

| Trade Credit | Net 30, Net 60, Net 90 | Inventory, supplies | Low to moderate |

| Business Line of Credit | Revolving, 12–36 months | Working capital, cash flow gaps | Moderate |

| Commercial Term Loan | 1–10 years, fixed schedule | Equipment, expansion | Moderate to high |

| Equipment Financing | 2–7 years, asset-backed | Machinery, vehicles | Moderate |

- Trade credit requires no formal application in many cases, but late payments still damage your credit profile.

- Lines of credit charge interest only on the amount drawn, not the full limit.

- Term loans carry the most structured repayment obligations and typically require stronger credit profiles.

- Equipment financing uses the purchased asset as collateral, which can make approval easier for newer businesses.

Pro Tip: Open at least three vendor accounts with suppliers who report to Dun & Bradstreet or Experian Business. Three active trade lines are the minimum threshold most lenders look for when reviewing a commercial credit profile.

How does commercial credit differ from personal credit?

Commercial credit and personal credit operate under fundamentally different rules. Unlike standardized FICO scoring for personal credit, commercial credit agencies like Dun & Bradstreet and Experian use separate scoring methods with no universal standard. That means a score from one bureau may not translate directly to another.

The structural differences go deeper than scoring models. Personal credit is linked to your Social Security number and regulated by the Fair Credit Reporting Act, which gives you rights like free annual reports and dispute protections. Commercial credit is linked to your EIN and operates in a largely market-driven environment with far fewer legal protections. You can read more about how these profiles diverge in the context of business vs. personal loans.

Payment tracking also works differently. Personal credit uses delinquency buckets: 30 days late, 60 days late, 90 days late. Commercial credit measures payment behavior in "days beyond terms." If your invoice is Net 30 and you pay on day 45, your report records 15 days beyond terms. Even a small, consistent delay compounds into a pattern that harms your score.

The practical consequences of weak commercial credit are significant:

- Lenders may require personal guarantees or additional collateral.

- Vendors may demand cash on delivery instead of extending payment terms.

- Insurance carriers may charge higher premiums based on your business credit profile.

- Contract opportunities with larger companies may require a minimum credit score.

Pro Tip: Never assume your personal credit score substitutes for a commercial credit profile. Lenders and vendors check both, and a strong personal score does not offset a thin or absent business credit file.

How do commercial credit reports and scores affect your business?

Commercial credit reports are the primary tool lenders, vendors, and insurers use to assess your business's financial reliability. Lenders and vendors use these reports to determine lending amounts, interest rates, collateral requirements, and vendor terms. A strong report leads to better rates and lower personal guarantee requirements. A weak report can result in denial or unfavorable conditions.

The data inside a commercial credit report goes beyond payment history. Reports typically include:

| Data Point | What It Signals |

|---|---|

| Trade line payment history | Consistency and reliability of payments |

| UCC filings | Assets pledged as collateral to lenders |

| Public records (liens, judgments) | Legal and financial disputes |

| Business background (age, size, industry) | Stability and risk context |

| Credit utilization | How much available credit is in use |

Commercial credit reports often include UCC filings, which signal pledged assets and directly affect how lenders calculate available collateral. A business with multiple UCC filings may appear over-leveraged even if its payment history is clean.

Commercial credit reports lack the federal protections that consumer credit reports carry. Third parties can purchase your business credit report without your knowledge or consent. You have no legal right to a free annual report. This makes proactive monitoring a necessity, not an option.

The commercial credit environment is highly volatile because few businesses remain unchanged after five years. Lenders and suppliers rely on current reports to manage risk. A report that was strong two years ago may not reflect your current financial position accurately. Checking your Dun & Bradstreet PAYDEX score and Experian Business Intelliscore regularly gives you the clearest picture of how the market sees your business.

How can small business owners build strong commercial credit?

Building business credit requires intentional action through vendor relationships that report payment data to bureaus. Everyday operations alone do not build a credit profile. A profitable business that pays all its bills in cash has no commercial credit history. That absence is a liability when you need financing.

Follow these steps to build a credit profile that opens doors:

-

Register your business as a legal entity. Form an LLC or corporation and obtain an EIN from the IRS. This separates your business identity from your personal finances and is the prerequisite for all commercial credit activity.

-

Open a dedicated business bank account. Lenders verify that your business operates independently. A business checking account in your company's name establishes that separation clearly.

-

Apply for a DUNS number from Dun & Bradstreet. This free identifier is required by many lenders and federal contractors. Without it, your business may not appear in commercial credit databases at all.

-

Open trade accounts with vendors who report to credit bureaus. Net 30 accounts with suppliers that report to Dun & Bradstreet or Experian Business are the fastest way to generate positive trade lines. Office supply companies, wholesale distributors, and business fuel card providers often offer these accounts.

-

Pay early whenever possible. Paying on day 25 of a Net 30 term records a positive payment pattern. Paying on day 31 records one day beyond terms. The difference in your score over 12 months is significant.

-

Monitor your reports and dispute errors. Pull your reports from Dun & Bradstreet, Experian Business, and Equifax Business Credit at least twice per year. Errors in commercial reports are not uncommon, and the lack of regulatory protection means you must catch and correct them yourself.

-

Avoid maxing out credit lines. High utilization signals financial stress to lenders. Keep usage below 30% of your available credit limit on revolving accounts.

Profitability alone does not build creditworthiness. Lenders require documented, reported payment histories. You can review additional strategies in this business credit basics guide and find specific score improvement tactics at Capitalforbusiness's credit score tips.

Key takeaways

Commercial credit is the financial foundation that determines what financing terms, vendor relationships, and growth opportunities your business can access.

| Point | Details |

|---|---|

| Commercial credit definition | Businesses access goods, capital, or services now and repay later through trade or lender credit. |

| Separate from personal credit | Commercial credit ties to your EIN and uses different scoring models than personal FICO scores. |

| Reports drive financing terms | Lenders and vendors use commercial credit reports to set rates, limits, and collateral requirements. |

| Active building is required | Opening vendor accounts that report to bureaus is the only way to establish a business credit profile. |

| Proactive monitoring matters | No federal protections apply to commercial reports, so regular review and error disputes are your responsibility. |

What most business owners get wrong about commercial credit

After working with small business owners across hundreds of industries since 2009, one pattern stands out clearly. Most entrepreneurs treat commercial credit as something that builds itself. They assume that running a profitable business, paying suppliers, and staying current on expenses automatically creates a strong credit profile. It does not.

Many entrepreneurs confuse commercial credit with personal credit, not recognizing the unique demands and scoring models involved. The business owner who has a 780 personal credit score but no formal trade lines or EIN-linked accounts has essentially no commercial credit profile. When they apply for a $200,000 business loan, lenders see a blank file. That blank file is treated as risk, not neutrality.

The second mistake is waiting too long to start. Building business credit early is critical because the commercial credit environment has far less regulatory oversight than consumer credit. You cannot rely on legal protections to correct problems after the fact. The businesses that access the best financing terms are the ones that started building their profiles years before they needed a large loan.

My honest recommendation: treat your commercial credit profile as a business asset you manage deliberately, the same way you manage cash flow or inventory. Open the right vendor accounts, pay early, monitor your reports, and review your profile before you need financing, not during the application process.

— Capital

Ready to put your commercial credit to work?

Understanding commercial credit is the first step. The next step is connecting that knowledge to real financing options that fit your business.

Capitalforbusiness has worked with small business owners nationwide since 2009, providing fast access to working capital, equipment financing, business lines of credit, and more. Whether your credit profile is established or still developing, Capitalforbusiness offers small business loan options designed to meet you where you are. When banks say no, Capitalforbusiness delivers funding quickly and at a price that fits your budget. Explore business funding up to $500k and find the solution that matches your growth goals today.

FAQ

What is the definition of commercial credit?

Commercial credit is a financial arrangement that allows a business to receive goods, services, or funds immediately and defer payment to a later date. It covers both trade credit from vendors and formal lending products like lines of credit and term loans.

How is commercial credit different from personal credit?

Commercial credit is tied to a business EIN and tracked by bureaus like Dun & Bradstreet and Experian Business, while personal credit is tied to a Social Security number and governed by the Fair Credit Reporting Act. Commercial credit uses different scoring models and carries no federal consumer protections.

What is a PAYDEX score and why does it matter?

The PAYDEX score is Dun & Bradstreet's commercial payment index, ranging from 1 to 100, measuring how promptly a business pays its bills relative to agreed terms. A score of 80 or above indicates on-time payment and signals low risk to lenders and vendors.

How long does it take to build commercial credit?

Most businesses can establish a basic commercial credit profile within 3–6 months by opening three or more vendor trade accounts that report to commercial bureaus and paying consistently on time. A strong, well-documented profile typically takes 12–24 months to develop.

Can a business get commercial credit with no credit history?

Yes. Starting with vendor trade accounts, a business fuel card, or a secured business credit card allows a company to generate its first reported payment history. These entry-level accounts report to commercial bureaus and form the foundation of a credit profile even when no prior history exists.