TL;DR:

- Effective cash flow management involves forecasting, monitoring, and adjusting inflows and outflows to maintain business stability. Building a 13-week rolling forecast based on real payment behavior and reliable data helps identify early warning signs of financial problems. Proactively securing funding and optimizing operational habits strengthen cash flow resilience and prevent crises.

Step by step cash flow management is the systematic process of forecasting, monitoring, and adjusting cash inflows and outflows so your small business stays financially sound. Cash flow management is an operational discipline distinct from profit. Profit tells you whether your business model works over time. Cash flow tells you whether you can pay your bills next Friday. 61% of small businesses struggle with cash flow, and nearly one in three cannot meet basic financial obligations. The industry gold standard for staying ahead of those pressures is the 13-week rolling cash flow forecast, a tool that gives you 90 days of operational visibility at all times.

What tools and data do you need before you start?

Effective cash flow management starts with accurate data, not perfect data. You need three core inputs before building any forecast: your current bank balance, your accounts receivable aging report, and your accounts payable schedule. These three documents tell you where money is right now, when money is coming in, and when money must go out.

Gathering this data does not require expensive software. Many small business owners start with a well-structured spreadsheet or a cash flow forecast template. Simple cloud-based accounting tools can export the aging reports and payables schedules you need within minutes. The goal at this stage is to get reliable numbers on paper, not to build a perfect system.

One critical distinction separates accurate forecasts from wishful ones. Base your inflow forecasts on actual customer payment behavior, not on the payment terms printed on your invoices. If your net-30 customers routinely pay in 45 days, your forecast must reflect 45 days. Using contractual terms instead of real payment timelines is one of the most common forecasting errors small business owners make.

Your outflow data is typically more predictable. Payroll runs on a fixed schedule. Rent is fixed. Loan payments are fixed. The variable items, like vendor bills and inventory purchases, require you to pull your accounts payable schedule and note due dates. Once you have all three inputs ready, you have everything you need to build a working forecast.

- Current bank balance: Pull this directly from your bank statement, not your accounting software, since timing differences can distort the number.

- Accounts receivable aging report: List every outstanding invoice, the customer name, the invoice date, and the expected payment date based on actual payment history.

- Accounts payable schedule: List every upcoming bill, the vendor, the due date, and the amount.

- Historical payment data: Review the last 90 days of customer payments to identify average days to pay by customer.

- Fixed obligation calendar: Note every recurring payment, including payroll, rent, loan installments, insurance, and subscriptions, with exact due dates.

Pro Tip: An 80% accurate forecast started today is more valuable than waiting for perfect data. Weekly updates will close the accuracy gap quickly. Do not let the pursuit of precision delay your start.

How do you build a 13-week rolling cash flow forecast step by step?

The 13-week rolling cash flow forecast is the industry gold standard because it gives you exactly 90 days of forward visibility. That window is long enough to spot problems early and short enough to keep projections realistic. Here is how to build one from scratch.

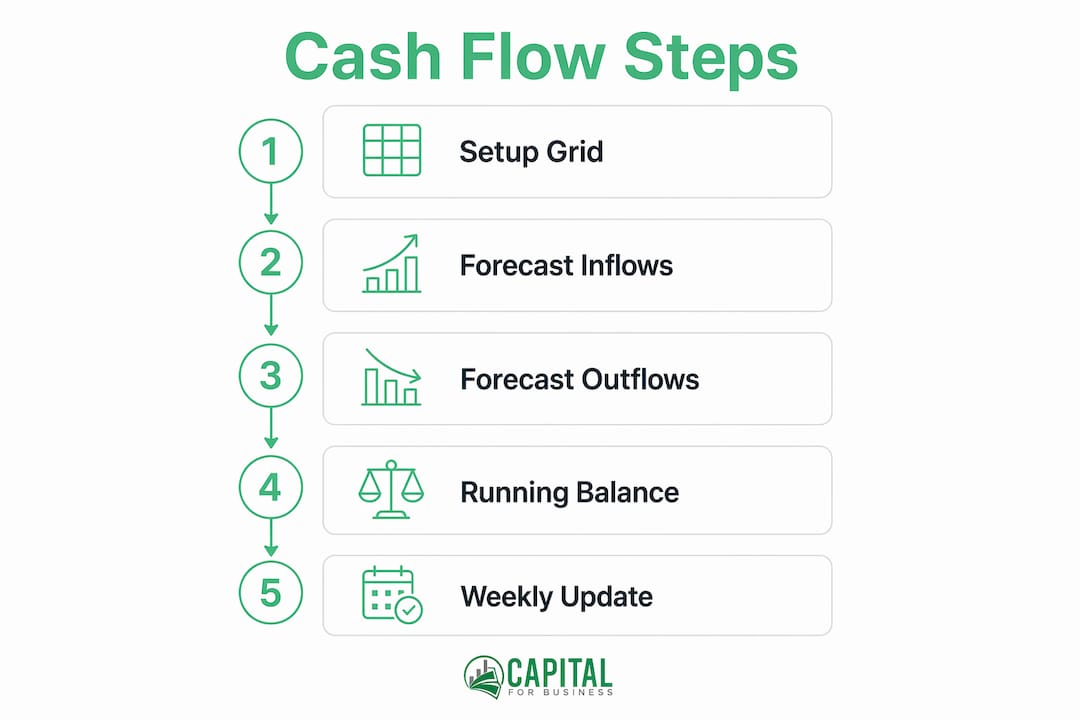

Step 1: Set up the grid

Create a spreadsheet with weeks running across the top (Week 1 through Week 13) and cash categories running down the left side. Divide the rows into three groups: cash inflows, cash outflows, and running balance. Label each outflow row specifically, such as payroll, rent, loan payments, vendor bills, and taxes. Specificity here prevents you from missing obligations later.

Step 2: Forecast cash inflows

Enter expected cash receipts for each week based on your accounts receivable aging report and expected new sales. Use actual customer payment timelines, not invoice terms. If you expect a $10,000 payment from a customer who typically pays in 45 days, place that cash in the correct week. Add expected revenue from new sales conservatively, based on your recent sales history.

Step 3: Forecast cash outflows

Enter every known payment obligation in the week it is due. Payroll, rent, and loan payments go in first because they are fixed and non-negotiable. Then add variable items like vendor bills, estimated tax payments, and inventory purchases. Do not forget annual or quarterly obligations like insurance renewals or estimated tax installments. These are the items that blindside owners who only track monthly expenses.

Step 4: Calculate your running weekly balance

Add a row at the bottom of each week's column that calculates: prior week ending balance plus inflows minus outflows. This running balance is the most important number in your forecast. Any week where the balance drops below your minimum operating threshold is a warning signal that requires action.

Step 5: Update weekly and roll forward

Every week, replace your projections with actual figures for the week that just ended. Then add a new Week 13 to the end of the forecast, extending your visibility window. Weekly updates enable early detection of low-balance weeks while you still have time to act. This rolling update habit is what separates proactive owners from reactive ones.

| Forecast component | What to include | Update frequency |

|---|---|---|

| Cash inflows | Customer payments, new sales, loan proceeds | Weekly |

| Cash outflows | Payroll, rent, taxes, vendor bills, loan payments | Weekly |

| Running balance | Ending balance per week | Weekly |

| Variance tracking | Actual vs. projected for prior week | Weekly |

| Scenario notes | Best case and worst case adjustments | Monthly |

Pro Tip: Build a second scenario tab in your spreadsheet with a worst-case version of the same forecast. Reduce inflows by 20% and keep outflows fixed. If your business can survive that scenario, you have genuine financial resilience.

Traditional budgeting looks backward at monthly or annual totals. The 13-week forecast looks forward at weekly cash positions. That difference in perspective is what makes it an operational tool rather than an accounting exercise.

What are the most effective strategies to improve cash flow?

Improving cash flow comes down to one principle: accelerate cash in, delay cash out, and cut what does not serve the business. Operational inefficiencies alone can cost small businesses 20–30% of top-line revenue annually. That is a significant amount of cash that never makes it to your bank account. Addressing these leaks is often faster than chasing new revenue.

For a deeper look at proven methods, the cash flow improvement strategies outlined by Capitalforbusiness cover a range of practical approaches worth reviewing alongside this guide.

- Invoice immediately after delivery. Failure to send invoices promptly is one of the leading causes of cash flow shortfalls. Every day you delay invoicing is a day you delay getting paid.

- Use automated payment reminders. Set up automated email reminders at 7 days before due, on the due date, and at 7 days past due. This removes the awkwardness of manual follow-up and shortens your average collection cycle.

- Segment your customers by payment behavior. Identify your slow payers and either require deposits from them upfront or tighten their credit terms. Focus your collection energy on accounts with the highest balances and the worst payment history.

- Negotiate extended terms with suppliers. Ask key vendors to extend your payment terms from net-30 to net-45 or net-60. Even a 15-day extension on a $20,000 monthly payables balance meaningfully improves your weekly cash position.

- Review inventory levels monthly. Excess inventory ties up cash without generating returns. Set reorder points based on actual sales velocity, not on gut feel or supplier minimums.

- Audit subscriptions and recurring costs quarterly. Small recurring charges accumulate quickly. A quarterly review of every subscription and service contract often reveals $500 to $2,000 in monthly costs that no longer serve the business.

- Offer early payment discounts selectively. A 1–2% discount for payment within 10 days can accelerate cash from your best customers. Use this tactic for large invoices where the cash timing benefit outweighs the discount cost.

Pro Tip: Securing a business line of credit before you need it is one of the most effective cash flow strategies available. Lenders approve credit when your financials are healthy. Waiting until a cash crisis hits means applying from a position of weakness.

Technology also plays a practical role here. Cloud accounting platforms that connect your bank, invoicing, and payables in one place give you real-time visibility without manual data entry. That visibility is what makes weekly forecast updates fast enough to actually happen.

How do you recognize and prevent cash flow problems before they escalate?

Cash flow problems rarely appear without warning. The warning signs show up in your forecast and your aging reports weeks before they become crises. Recognizing them early is what gives you options.

Warning signs to watch every week:

- Running balance dropping below two weeks of operating expenses

- Accounts receivable aging showing more than 30% of balances past due

- Payables aging showing bills being stretched beyond terms consistently

- Revenue declining for two or more consecutive weeks without a seasonal explanation

- Loan or credit card balances increasing month over month without a corresponding asset purchase

When your forecast shows a shortfall in an upcoming week, you have three levers to pull. The core corrective actions are accelerating cash in, delaying cash out, and adding capital. Accelerating cash in means calling overdue customers directly, offering early payment discounts, or collecting deposits on pending orders. Delaying cash out means negotiating a short extension with a vendor or deferring a discretionary purchase. Adding capital means drawing on a line of credit or arranging short-term financing.

"Waiting for a crisis before seeking financing leads to suboptimal outcomes. Proactive credit readiness is the difference between choosing your financing terms and accepting whatever is available under pressure." — Rohit Arora, Biz2Credit

Maintaining a cash reserve is the most reliable buffer against unexpected shortfalls. A reserve equal to four to six weeks of operating expenses gives you time to respond without panic. Building that reserve takes discipline, but even setting aside a fixed percentage of weekly revenue accelerates the process.

Scenario forecasting is another prevention tool that most small business owners underuse. Running a worst-case scenario alongside your base forecast, where inflows drop and a major expense hits simultaneously, shows you exactly how much runway you have and what actions would be needed. This kind of planning removes the emotional weight from financial decisions because you have already thought through the response.

Review your forecast, your financial practices, and your business strategy together at least once a month. Cash flow is not a set-and-forget system. It reflects every decision you make about pricing, hiring, purchasing, and growth. Keeping those connections visible is what makes cash flow management a genuine operational discipline rather than a monthly accounting task.

Key Takeaways

Consistent step by step cash flow management, built on a 13-week rolling forecast and weekly updates, is the most reliable way for small businesses to maintain financial stability and avoid preventable crises.

| Point | Details |

|---|---|

| Start with accurate data | Gather bank balances, AR aging, and AP schedules before building any forecast. |

| Use the 13-week forecast | Build a rolling 90-day forecast and update it every week with actual figures. |

| Base inflows on real behavior | Use actual customer payment timelines, not invoice terms, for accurate projections. |

| Act on warning signs early | A running balance below two weeks of expenses requires immediate corrective action. |

| Secure financing proactively | Apply for a line of credit while your financials are healthy, not during a cash crisis. |

What working with small businesses has taught me about cash flow

Most owners I work with come to cash flow management after a scare. A slow month, a late customer payment, and suddenly payroll feels uncertain. That experience is common, and it is entirely preventable.

The most persistent misconception I see is treating profit and cash flow as the same thing. A business can show strong profit on paper while running dangerously low on cash. Profit is a long-term signal. Cash flow is a weekly reality. Once owners internalize that distinction, their entire approach to financial management shifts.

The second thing I have observed consistently is that operational improvements unlock more cash than most owners expect. Tightening invoicing, cutting unused subscriptions, and renegotiating one or two vendor contracts can free up meaningful cash without touching revenue at all. These are not dramatic changes. They are disciplined habits applied consistently.

My honest advice is to start simple. A basic spreadsheet with 13 weeks, three rows of inflows, five rows of outflows, and a running balance at the bottom is enough to change how you run your business. Refine it weekly. The accuracy improves fast. The confidence that comes from knowing your cash position three months out is worth every hour you invest.

Proactive financing is part of that confidence. Capitalforbusiness has worked with small business owners since 2009, and the owners who navigate growth most successfully are the ones who arrange working capital access before they need it. That preparation is not a sign of financial weakness. It is a sign of financial maturity.

— Capital

How Capitalforbusiness supports your cash flow strategy

Cash flow planning tells you when gaps will appear. Having the right financing in place means those gaps do not stop your business.

Capitalforbusiness offers small business loan options designed for the realities of running a small business, including working capital loans, merchant cash advances, equipment financing, and business lines of credit. These products exist precisely for the moments your forecast identifies: a slow receivables week, a large equipment purchase, or a seasonal dip in revenue. Capitalforbusiness has served small business owners across hundreds of industries since 2009, providing fast, flexible funding when banks fall short. Explore your funding options and put financing in place before your next cash flow gap arrives.

FAQ

What is step by step cash flow management?

Step by step cash flow management is the structured process of forecasting, tracking, and adjusting weekly cash inflows and outflows to keep a business financially stable. It treats cash flow as an ongoing operational discipline, not a one-time accounting task.

Why is the 13-week rolling forecast the industry standard?

The 13-week rolling forecast provides 90 days of forward visibility, which is long enough to spot problems early and short enough to keep projections accurate. Experts recommend it as the gold standard for operational cash flow management.

How accurate does my cash flow forecast need to be?

An 80% accurate forecast started today is more valuable than waiting for perfect data. Weekly updates using actual figures close the accuracy gap quickly and build a reliable picture of your cash position over time.

What are the first signs of a cash flow problem?

The clearest early warning signs are a running weekly balance dropping below two weeks of operating expenses and more than 30% of accounts receivable balances going past due. Both signals appear in your forecast before they become crises.

When should a small business seek outside financing for cash flow?

The best time to secure a line of credit or working capital loan is when your financials are healthy, not during a cash shortfall. Proactive credit readiness gives you better terms and more options than applying under financial pressure.