TL;DR:

- A funding cycle is a structured process from application to compliance reporting that directly impacts small business cash flow. Managing timing gaps and preparing for each phase, especially during delays, helps businesses avoid cash crises and maintain operations. Understanding differences across funding types enables better planning, reserve sizing, and strategic financing decisions.

A funding cycle is the complete sequence of steps from initial application through final compliance reporting, and every phase directly affects your business cash flow and planning capacity. Most small business owners treat funding as a single event. In practice, understanding funding cycles means recognizing a structured process that can span 3–12 months or longer, covering application preparation, award notification, active disbursement, and post-award obligations. Federal programs like NIH and USDA grants, as well as construction loan draw schedules, each follow distinct timelines that shape when cash actually arrives in your account. Getting ahead of that timeline is the difference between smooth operations and a cash crisis.

What are the typical phases of funding cycles?

The funding lifecycle stages follow a predictable sequence across most grant and loan programs. Knowing each phase helps you plan around timing gaps rather than react to them.

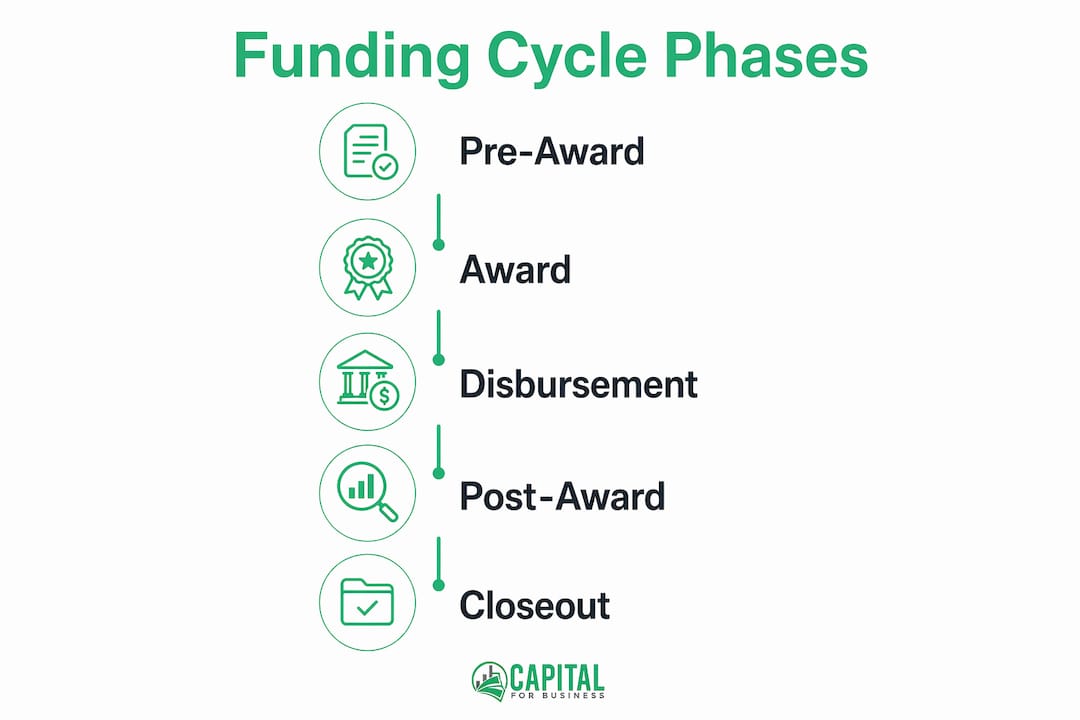

The four core phases are:

- Pre-award: Application preparation, eligibility review, and submission. This phase demands the most documentation and sets the timeline for everything that follows.

- Award notification and acceptance: The funder reviews your application, issues a decision, and you formally accept terms. For federal grants, this alone can take months.

- Active disbursement: Funds are released, either as a lump sum or in scheduled draws tied to milestones or reimbursement requests.

- Post-award management: Reporting, audits, and closeout activities that legally extend the cycle well beyond the final payment.

The USDA NIFA Capacity Grants lifecycle formally defines these phases as pre-award, award notification, program operation, and post-award closeout and reporting. That structure applies broadly across federal programs, not just agriculture grants.

Timelines vary significantly by program type:

- NIH R01 grants: Typically 9–12 months from submission to award decision

- USDA competitive grants: Often 6–9 months from application close to award

- Construction loan draws: Each individual draw takes 9–13 business days end-to-end, with commercial projects running 12–24 total draws

Federal grants also carry compliance obligations that extend the cycle past cash receipt. Under 2 CFR 200.344 and 2 CFR 200.334, recipients must complete closeout activities within 120 days of the performance period end and retain records for three years. The funding cycle does not end when the money arrives. It ends when the paperwork is complete and the records are filed.

How do funding cycles create cash flow challenges?

Timing gaps are the core problem in funding cycle management. The period between when you incur costs and when funds actually arrive is where most small businesses run into trouble.

For federal grants, GrantMetric's 2026 timeline guide recommends budgeting at least six months between application submission and funding receipt. NIH R01 applicants should plan for 9–12 months. That is a long time to carry operational costs without a corresponding cash inflow.

Construction businesses face a different but equally demanding version of this problem. Projects typically require 6–8 weeks of working capital outflow before progress billing generates any cash inflows. On a $550,000 project, that means $110,000–$165,000 of working capital tied up before the first draw payment arrives. Draw packages and inspection timing add further risk. Missing or incomplete documents regularly delay funding by one to two weeks per draw, compounding the cash gap.

The cash conversion cycle, or CCC, is a useful framework for quantifying this pressure. The CCC is calculated as inventory days plus receivable days minus payable days. A CCC of 75 days means you must fund 75 days of operating expenses through cash reserves or external financing before collections catch up. For businesses waiting on grant reimbursements or construction draws, the effective CCC can stretch well beyond that.

Common cash flow pressure points during funding cycles include:

- Payroll and overhead: Fixed costs continue regardless of where you are in the funding timeline

- Material purchases: Construction and manufacturing businesses must buy supplies before billing

- Seasonal expense spikes: Inventory buildup, staffing increases, or equipment rentals tied to seasonal demand often hit before funding arrives

- Reimbursement-based grants: For grants paid by reimbursement, costs must be incurred and documented before any funds are released, requiring meticulous cost-tracking workflows

Pro Tip: Track your cash flow disruption factors monthly, not just quarterly. Funding delays compound quickly when you are not watching the gap between outflows and expected inflows.

How can small businesses plan for funding cycle timing?

Proactive planning is the most reliable way to avoid a cash crisis caused by funding delays. The goal is to anticipate gaps weeks before they become problems, not scramble to fill them after the fact.

A 13-week rolling cash forecast updated weekly is the most practical tool for this. It tracks weekly inflows and outflows with enough precision to spot funding gaps 60–90 days ahead. Annual budgets are too broad to catch the timing mismatches that funding cycles create. A rolling forecast gives you the visibility to act early.

Practical planning steps for managing funding cycle timing:

- Align with funder fiscal calendars: Institutional funding timing often clusters around fiscal year cycles, with slowdowns near year-end and accelerations after. Submitting applications at the right point in a funder's calendar improves both timing and approval odds.

- Maintain a working capital reserve: Keep at least 60–90 days of operating expenses in liquid reserves to cover the gap between application and first disbursement.

- Prepare documentation in advance: Draw package completeness is the critical path in construction funding cycles. Missing documents delay funding by one to two weeks per draw. Build a documentation checklist before the project starts.

- Use bridge financing strategically: A business line of credit or short-term loan can cover the gap between cost incurrence and fund receipt without disrupting operations.

- Shorten your cash conversion cycle: Reducing receivable days and managing payables effectively improves funding readiness by decreasing the amount of external financing you need to bridge gaps.

Pro Tip: If you rely on seasonal business funding, map your funding cycle phases against your peak expense months at the start of each year. Knowing that a grant award will arrive in month seven tells you exactly how many months of bridge financing you need.

Businesses that treat funding cycle management as an ongoing process rather than a one-time task consistently handle delays better. The planning infrastructure you build for one cycle pays dividends across every subsequent one.

How do funding cycles differ across fund types?

Not all funding cycles work the same way. The structure of disbursement, the documentation requirements, and the timing of cash receipt vary significantly depending on the funding type. Understanding those differences helps you size your reserves correctly and choose the right financing tools.

| Funding Type | Disbursement Method | Typical Timeline | Key Cash Flow Risk |

|---|---|---|---|

| Federal grants (NIH, USDA) | Lump sum or reimbursement | 6–12 months to award | Long pre-award gap; post-award compliance costs |

| Construction loans | Draw-based (5–24 draws) | 9–13 business days per draw | Documentation delays add weeks per draw |

| SBA loans | Lump sum at closing | 30–90 days to fund | Underwriting delays; prepayment of costs |

| Business lines of credit | Revolving draws on demand | 1–5 business days | Requires active management; interest on drawn balance |

| Merchant cash advances | Lump sum upfront | 24–72 hours | Daily repayment reduces cash flow flexibility |

The most significant structural difference is between lump sum and draw-based disbursements. Lump sum funding arrives once and gives you full control of timing. Draw-based funding, like construction loans, ties cash release to milestone completion and documentation approval. Construction loan balances often follow an S-curve pattern rather than a straight line, meaning draws accelerate in the middle of a project and slow at the start and end. Relying on average draw assumptions can underestimate the interest reserve and working capital you need during peak draw periods.

Federal grants add a compliance layer that other funding types do not. The post-award phase requires reporting, audits, and record retention that extend the cycle legally and administratively. A business that closes out a grant poorly risks repayment demands or disqualification from future awards.

For small businesses comparing options, the right funding type depends on how quickly you need cash, how predictable your milestones are, and how much administrative capacity you have to manage documentation and reporting. A business line of credit works well for bridging predictable gaps. A merchant cash advance suits businesses with strong daily revenue but limited documentation history.

Key takeaways

Effective funding cycle management requires treating every phase, from application to closeout, as part of a single continuous process that demands proactive cash flow planning.

| Point | Details |

|---|---|

| Funding cycles span four phases | Pre-award, award, disbursement, and post-award compliance each carry distinct timing and cash flow implications. |

| Federal grants take 6–12 months | Budget for at least six months between application submission and first cash receipt to avoid operational gaps. |

| Construction draws carry documentation risk | Missing draw package documents delay funding by one to two weeks per draw, compounding cash shortfalls. |

| Rolling forecasts catch gaps early | A 13-week cash forecast updated weekly spots funding timing gaps 60–90 days before they become crises. |

| Disbursement structure shapes reserve needs | Lump sum funding and draw-based funding require different reserve sizing and bridge financing strategies. |

What i've learned after working with hundreds of small business owners

Most small business owners I work with at Capitalforbusiness make the same mistake: they think the funding cycle ends when the money hits their account. It does not. The post-award phase, with its reporting deadlines, audit requirements, and record retention rules, is where compliance stress builds and where underprepared businesses get into trouble.

The second misconception is equally costly. Many owners assume that applying for a grant or loan is the hard part. In reality, the hardest part is managing the 6–12 months between application and first disbursement without disrupting operations. That gap is where cash reserves get depleted, payroll gets tight, and growth plans stall.

What actually works is treating funding as a lifecycle with defined phases, not a single transaction. Businesses that build documentation systems before they need them, maintain rolling cash forecasts, and keep a line of credit available for bridge financing consistently outperform those that plan reactively. The businesses that struggle are the ones that apply for funding, assume it will arrive on schedule, and make spending commitments based on that assumption.

One more thing worth saying directly: the structure of your funding type matters as much as the amount. A $200,000 construction loan paid in 18 draws over 14 months creates very different cash flow demands than a $200,000 SBA loan paid as a lump sum at closing. Knowing that difference before you sign changes how you plan, what reserves you hold, and what bridge financing you arrange.

— Capital

Funding solutions that work around your funding cycle

Managing the timing gaps in a funding cycle is a real operational challenge, and Capitalforbusiness has helped small business owners navigate it since 2009.

Whether you need working capital to cover costs before a grant disbursement, bridge financing between construction draws, or a flexible credit line to handle seasonal expense spikes, Capitalforbusiness offers small business loan options built for exactly these situations. For businesses with strong daily revenue, a merchant cash advance can put capital in your account within 24–72 hours, well ahead of any grant or draw timeline. Explore your options and apply directly at Capitalforbusiness to keep your operations running while your funding cycle catches up.

FAQ

What is a funding cycle in simple terms?

A funding cycle is the full sequence of steps from applying for funds to completing post-award reporting. It includes application, award, disbursement, and compliance closeout.

How long does a typical federal grant funding cycle take?

Most federal grants take 6–12 months from application to first disbursement. NIH R01 grants specifically average 9–12 months, making advance cash flow planning critical.

Why do construction loan draws take so long?

Each construction loan draw requires documentation review and inspection, a process that takes 9–13 business days end-to-end. Incomplete draw packages add one to two weeks per draw.

What is the best tool for managing funding cycle cash flow gaps?

A 13-week rolling cash forecast updated weekly is the most effective tool. It identifies funding gaps 60–90 days ahead, giving you time to arrange bridge financing before a shortfall hits.

How does a business line of credit help with funding cycles?

A business line of credit provides on-demand access to capital that covers operating costs during the gap between funding phases. You draw only what you need and repay as disbursements arrive, keeping interest costs low.