TL;DR:

- Most founders assume venture capital is the only way to fund startups, which often leads to unnecessary dilution. Alternative tools like grants, venture debt, and revenue-based financing offer flexible, non-dilutive options aligned with different growth stages. Building a diversified capital stack allows startups to maintain control, extend runway, and increase resilience against market fluctuations.

Most founders assume that building a successful startup means pitching venture capitalists and handing over a significant slice of ownership. That belief is understandable, but it leaves real money on the table. Startups today have access to a broader range of funding tools than ever before, including venture debt, revenue-based financing, and non-dilutive grants that require no equity at all. This guide breaks down each option with real numbers, practical examples, and a clear framework so you can make smarter capital decisions at every stage of your company's growth.

Table of Contents

- Understanding the startup funding landscape

- Venture debt: How to use debt without giving up control

- Revenue-based financing: Grow without ownership dilution

- Non-dilutive funding: Grants and ecosystem support

- How to choose and layer your funding sources

- Our perspective: Most founders over-focus on VC and miss smarter capital plays

- Ready to fund your startup? Explore tailored solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Diversify funding strategy | Smart founders combine equity, debt, and non-dilutive options for best results. |

| Understand dilution | Equity rounds often dilute ownership 10–25%, while alternatives can preserve control. |

| Target right fit | Pre-revenue startups should favor grants and angels, not debt or RBF. |

| Leverage non-dilutive capital | Grants and RBF support growth without sacrificing ownership or cash flow flexibility. |

Understanding the startup funding landscape

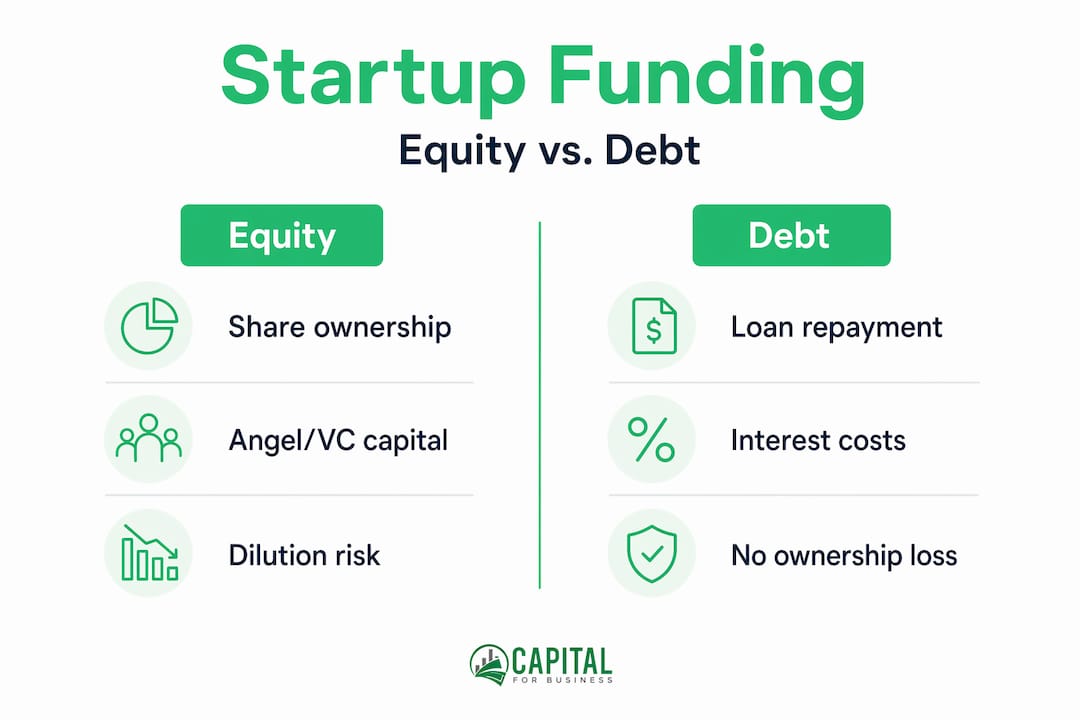

Before you can choose the right funding path, you need to understand what the options actually are. Startup funding generally falls into four categories: equity-based, debt-based, non-dilutive, and hybrid. Each carries different implications for ownership, repayment, and the stage of business they suit best.

Equity-based funding means exchanging ownership shares for capital. This includes angel investors, venture capital (VC) firms, and crowdfunding platforms. Seed equity rounds target 10–25% dilution with typical raises of $1 to $5 million post-YC, often structured as SAFEs (Simple Agreements for Future Equity) or convertible notes. Friends and family deals tend to run 5–20% equity.

Debt-based funding includes venture debt, traditional small business loans, and lines of credit. You borrow capital and repay it with interest, keeping your ownership intact.

Non-dilutive funding covers grants, government programs, and competitions. No repayment, no equity given up.

Hybrid options like revenue-based financing (RBF) sit between debt and equity. You repay from future revenue at a fixed multiple, with no ownership change.

Here is a quick breakdown of the major funding sources and what they typically require:

- Angel investors: Early-stage equity, $25K to $500K, in exchange for 5–20% ownership

- Venture capital: Growth-stage equity, $1M to $50M+, typically 15–30% ownership per round

- Venture debt: Post-equity debt, 20–50% of last round size, low warrant dilution

- Revenue-based financing: $10K to $10M, repaid as a percentage of monthly revenue

- SBIR/STTR grants: Up to $275K (Phase I) or $1.83M (Phase II), zero repayment or dilution

- Accelerator programs: Structured mentorship plus capital (e.g., $500K for 7% equity at YC)

Understanding short term financing goals early helps you match the right tool to the right moment. Many founders also benefit from supporting working capital through non-equity instruments while equity rounds are in progress. And if you want to go deeper on the non-traditional side, alternative financing strategies are worth exploring before you commit to any single path.

Venture debt: How to use debt without giving up control

Venture debt is one of the most underused tools in a startup's capital toolkit. It lets you borrow capital without issuing new shares, which means your ownership percentage stays intact. But it is not for everyone, and the terms matter enormously.

Who qualifies? Venture debt is primarily available to VC-backed startups, usually post-Series A, with a credible investor base and some level of annual recurring revenue (ARR). Lenders underwrite the loan based on investor quality and growth trajectory, not just cash flow. Pre-revenue startups almost never qualify.

What do the numbers look like? Venture debt typically provides 20–50% of the last equity round size, with all-in interest rates of 8–17% (SOFR/Prime plus 3–10%), repayment terms of 36–48 months, and warrants for 0.3–2% equity. Here is a sample breakdown:

| Term | Typical range |

|---|---|

| Loan amount | 20–50% of last equity round |

| Interest rate | 8–17% all-in (SOFR/Prime + 3–10%) |

| Repayment period | 36–48 months |

| Warrant coverage | 0.3–2% equity |

| Best fit | Post-Series A, VC-backed, $1M+ ARR |

The primary appeal is runway extension. If you raised a $5M Series A, you might access $1.5M to $2.5M in venture debt, buying 6–12 additional months without diluting your cap table. That extra time can be the difference between hitting a key milestone and having to raise at a lower valuation.

"Venture debt for startups typically provides 20–50% of the last equity round size, with interest rates of SOFR/Prime + 3–10% (all-in 8–17%), 36–48 month terms, and warrants for 0.3–2% equity." This structure makes it one of the most capital-efficient tools available to post-equity startups.

Pro Tip: When negotiating venture debt, push for warrant coverage at the lower end of the range (0.3–0.5%) and insist on minimal financial covenants. Avoid prepayment penalties so you can retire the debt early if a new equity round closes faster than expected.

The risks are real. Debt adds a fixed repayment obligation to your cash flow, which becomes a serious problem if revenue slows. Startups that take on venture debt without a clear repayment plan often find themselves in a cash crunch at exactly the wrong moment. Understanding technology in small business lending can help you evaluate lenders more effectively. If you are trying to bridge the finance gap between rounds, venture debt is worth a serious look, but only with a realistic cash flow model in hand.

Revenue-based financing: Grow without ownership dilution

Revenue-based financing (RBF) is exactly what it sounds like. A lender advances you capital upfront, and you repay it as a fixed percentage of your monthly revenue until you hit a predetermined repayment cap, called the repayment multiple.

How the math works: If you receive $100,000 at a 1.5x repayment multiple, you owe $150,000 total. Each month, 5–10% of your revenue goes toward repayment. A strong revenue month means you pay back more. A slow month means you pay less. No fixed monthly payment, no equity given up.

RBF advances $10K to $10M at a 1.3–2.0x repayment multiple, repaid as 2–20% of monthly revenue. It is ideal for SaaS and ecommerce companies with $10,000 or more in monthly recurring revenue (MRR), with effective interest equivalents of 15–25% for early-stage companies.

Who benefits most from RBF?

- SaaS companies with predictable subscription revenue

- Ecommerce brands with consistent monthly sales

- Startups with $10K+ MRR but not yet ready for a Series A

- Founders who want to avoid dilution between equity rounds

How the qualification process works:

- Connect your revenue data (Stripe, Shopify, QuickBooks) to the RBF platform

- The provider analyzes 3–12 months of revenue history

- An offer is generated based on your MRR and growth rate

- You review the repayment multiple and percentage

- Funds arrive, often within 48–72 hours of approval

Here is how RBF compares to equity and venture debt:

| Factor | Equity | Venture debt | Revenue-based financing |

|---|---|---|---|

| Dilution | 10–30% per round | 0.3–2% (warrants) | None |

| Repayment | None (until exit) | Fixed monthly | % of monthly revenue |

| Qualification | Pitch, traction, team | VC backing, ARR | Revenue history, MRR |

| Speed to funding | 3–6 months | 4–8 weeks | 48–72 hours |

| Best stage | Seed to growth | Post-Series A | Revenue-generating |

| Effective cost | High (ownership) | 8–17% interest | 15–25% effective rate |

Pro Tip: Use RBF to bridge between equity rounds rather than taking a down round or diluting early investors. If you need $200K to hit a revenue milestone that justifies a higher Series A valuation, RBF can fund that gap without touching your cap table.

You can learn more about how this works in practice on our revenue-based financing overview page.

Non-dilutive funding: Grants and ecosystem support

Grants are the cleanest form of startup capital. No repayment. No equity. No warrants. The catch is that they are competitive, often slow to arrive, and usually tied to specific use cases like R&D or underrepresented founder support.

The major sources worth knowing:

The federal government's SBIR/STTR program provides non-dilutive R&D funding in two phases: Phase I awards up to $275,000 over 6–12 months, and Phase II awards up to $1.83 million over 24 months. These are specifically designed for tech startups working with research institutions. No repayment required.

The Kauffman Foundation offers project grants of $250,000 or more per year on a multi-year basis, focused on entrepreneurship ecosystem building. They prioritize underrepresented founders and organizations working to improve capital access.

| Grant source | Max amount | Timeline | Best fit |

|---|---|---|---|

| SBIR Phase I | $275,000 | 6–12 months | Tech/R&D startups |

| SBIR Phase II | $1.83 million | 24 months | Established R&D programs |

| Kauffman Foundation | $250,000+/year | Multi-year | Ecosystem builders, underrepresented founders |

| Startup accelerators (e.g., YC) | $500,000 | 3 months | Early-stage, high-growth |

| State/local economic grants | Varies | 3–12 months | Location-specific industries |

Advantages of non-dilutive funding:

- No ownership given up, ever

- No interest payments or repayment obligations

- Often comes with ecosystem support, mentorship, and credibility

- Particularly valuable for pre-revenue or R&D-intensive startups

- Many programs specifically support women, minorities, and veterans

Disadvantages to consider:

- Application processes are time-consuming and competitive

- Funds often arrive slowly (months after approval)

- Restricted to specific uses (R&D, community development, etc.)

- Not suitable for general operating expenses or rapid scaling

Grants are not a replacement for growth capital, but they are an excellent foundation. A $275,000 SBIR grant can fund a year of product development without touching your equity. That is a significant advantage when you eventually go to raise a seed round.

How to choose and layer your funding sources

The smartest founders do not pick one funding source and stick with it. They build a capital stack, layering different instruments at different stages to minimize dilution, manage cash flow, and extend runway.

Here is a practical framework for thinking through your options:

- Start with grants and angels. If you are pre-revenue or early-stage, focus on SBIR grants, angel investors, and accelerator programs. These sources do not require the revenue history that lenders and RBF providers demand.

- Add equity when you have traction. Once you have product-market fit and measurable growth, a seed or Series A round gives you the capital to scale. Expect 10–25% dilution per round.

- Layer in debt after your equity round. Post-Series A, venture debt can extend your runway by 6–12 months at a fraction of the dilution cost. Use it to hit milestones before your next raise.

- Use RBF for working capital between rounds. If you have recurring revenue and need operational capital without dilution, RBF fills that gap efficiently.

- Revisit grants throughout your lifecycle. SBIR Phase II and foundation grants remain available to growing companies. Do not assume grants are only for startups in their first year.

Pre-revenue startups rarely qualify for debt or RBF and should focus on grants like SBIR or accelerators like YC, which offer $500,000 for 7% equity. Venture debt requires strong VC backing since lenders underwrite on investor quality rather than cash flow alone.

When you do access venture debt, negotiate for lower warrants in the 1–2% range, minimal covenants, and no prepayment penalties. Layering RBF with venture debt is possible but requires careful attention to total leverage. Equity is cheaper long-term for companies targeting 10x or greater exits, while debt preserves ownership but adds cash flow obligations.

Pro Tip: Before signing any debt or RBF agreement, model out three scenarios: your current growth rate, a 30% revenue slowdown, and a 50% slowdown. If your repayment obligations become unmanageable in the slowdown scenarios, the leverage is too high.

Common mistakes founders make include chasing capital from sources they do not qualify for, ignoring covenant terms until they become a problem, and underestimating the long-term cost of high-multiple RBF deals. Knowing how your business can borrow for operating expenses responsibly is just as important as knowing how to raise equity.

Our perspective: Most founders over-focus on VC and miss smarter capital plays

The startup media ecosystem has a VC problem. Every major publication celebrates the headline raise, the nine-figure valuation, the founder who landed a term sheet from a top-tier firm. What rarely gets covered is the founder who built a $10 million revenue business by combining a $275,000 SBIR grant, a $500,000 angel round, and two rounds of RBF without ever giving up more than 15% of their company.

That founder often has more control, more options, and more resilience than the one who raised $20 million and handed over 40% of their business in the process.

The VC model works extremely well for a specific type of company: one targeting a massive market, built for rapid scale, and willing to accept the pressure that comes with institutional investors who need a 10x return. For every other type of startup, including profitable service businesses, niche SaaS products, and mission-driven companies, the VC path can actually be counterproductive.

What we see consistently is that founders who diversify their capital sources build more durable companies. They are not dependent on a single investor relationship. They are not forced into premature scaling because a board demands it. They have the flexibility to weather a slow quarter without triggering a down round.

The alternative financing strategies available today give founders real options. The problem is that most founders do not learn about them until they have already committed to the VC path. That is a timing problem, and it is fixable.

Our honest take: spend as much time understanding your non-dilutive and debt options as you spend preparing your pitch deck. The founder who walks into a VC meeting having already secured a $275,000 SBIR grant and $200,000 in RBF has more leverage, a stronger signal of execution, and less pressure to accept unfavorable terms. That is not a small advantage.

Ready to fund your startup? Explore tailored solutions

You now have a clear picture of the funding tools available, from equity and venture debt to RBF and non-dilutive grants. The next step is finding the right fit for where your business is today.

At Capital for Business, we work with startups and growing businesses across North America to provide practical funding solutions that banks often cannot. Whether you need easy small business loans to cover early operational costs, working capital loans to bridge a revenue gap, or a flexible business line of credit that grows with your needs, we have options designed for real business situations. We move quickly, work across industries, and focus on finding solutions that fit your stage and your goals. Explore what is available for your startup today.

Frequently asked questions

What funding options are best for pre-revenue startups?

Grants, angel investors, and accelerator programs are usually the best choices for pre-revenue startups since lenders and RBF providers require proof of revenue. Pre-revenue startups should focus on SBIR grants or accelerators like YC rather than debt or RBF.

How much equity should I expect to give up in a seed round?

Typical seed equity rounds see 10–25% ownership dilution, with friends and family deals usually ranging from 5–20%. Seed rounds target 10–25% dilution and are commonly structured as SAFEs or convertible notes.

Do I need recurring revenue to qualify for revenue-based financing?

Yes, most providers require at least $10,000 per month in recurring revenue and a track record in SaaS or ecommerce. RBF advances $10K to $10M repaid as 2–20% of monthly revenue, making it ideal for companies with established MRR.

What are the main advantages of grants like SBIR or Kauffman Foundation funding?

These grants are non-dilutive, do not require repayment, and often support ecosystem building and underrepresented founders. SBIR/STTR grants provide non-dilutive R&D funding with no repayment obligation at any stage.

When does debt make sense for a startup?

Debt works best for revenue-generating startups with VC backing, solid growth, and a need to extend runway without further dilution. Venture debt provides 20–50% of the last equity round size and is best suited to post-Series A companies with strong investor backing.