TL;DR:

- Plumbing business credit ratings are separate from personal scores, tracked by different bureaus, and influence financing and vendor terms. Building strong credit requires forming reporting vendor relationships, timely payments, and regular monitoring over several months. Improving your business credit enhances access to better loan rates, supplier terms, and growth opportunities.

Most plumbing business owners think their personal credit score speaks for their entire operation. It does not. Plumbing business credit ratings are a separate system, scored differently, tracked by different agencies, and used by lenders and vendors to make decisions you may not even realize are happening. If you have been applying for financing or negotiating supplier terms without understanding your business credit profile, you may be leaving money on the table or getting turned down for reasons you can fix. This guide breaks down exactly how these ratings work, what affects them, and what you can do right now to build a stronger financial position.

Table of Contents

- Key takeaways

- Plumbing business credit ratings explained

- How to build strong credit for your plumbing company

- Factors that affect your score and myths to avoid

- How credit ratings affect financing and loan approvals

- Steps to monitor and improve your credit ratings now

- My perspective on managing business credit as a plumber

- Financing options built for plumbing businesses

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Business credit is separate | Your plumbing company needs its own credit profile, distinct from your personal score. |

| Vendors must report payments | Without vendors who report to credit bureaus, your business has no score regardless of payment behavior. |

| Payment timing drives scores | Consistent on-time payments are the single most influential factor in all major business credit models. |

| Strong scores improve loan terms | A PAYDEX score of 80 or higher signals payment reliability and helps you secure better financing rates. |

| Monitoring prevents surprises | Business credit reports are public, meaning lenders and vendors can check them without notifying you. |

Plumbing business credit ratings explained

When someone refers to a business credit rating, they are talking about a number produced by one of several credit bureaus that measures how reliably your business pays its debts. This is not the same as your personal FICO score, and it does not follow the same scale or methodology.

There are four major scoring models you will encounter as a plumbing business owner.

- PAYDEX (Dun & Bradstreet): Scored on a 1 to 100 scale. A score of 80 means you pay on time. Above 80 means you pay early. Below 50 signals serious risk to lenders and vendors.

- Experian Intelliscore Plus: Also scored 1 to 100, where 76 to 100 signals low risk to creditors. This model factors in credit utilization and public records alongside payment history.

- Equifax Business Credit Risk Score: Ranges from 101 to 992, focusing heavily on delinquency risk and overall financial behavior.

- FICO Small Business Scoring Service (SBSS): Scored 0 to 300 and is frequently used by the SBA and many traditional lenders when reviewing loan applications.

Here is a direct comparison of how these scores differ from personal credit scores:

| Feature | Personal Credit Score | Business Credit Score |

|---|---|---|

| Scale | 300 to 850 | Varies by model (1 to 100, 101 to 992, 0 to 300) |

| Primary bureau | Experian, Equifax, TransUnion | D&B, Experian Business, Equifax Business |

| Who reports data | Banks, credit card issuers | Vendors, suppliers, lenders |

| Publicly accessible | No | Yes |

| Tied to an individual | Yes (SSN) | Yes (EIN and business identity) |

The practical takeaway here is that your business credit rating reflects how your plumbing company behaves as a borrower and buyer. It is independent of your personal financial habits. Building it requires deliberate action, because it will not generate on its own.

Understanding why plumbing businesses need credit scores separate from personal ones comes down to liability and growth. When your business has its own strong credit profile, lenders and vendors assess your company on its own merits. That reduces your personal exposure and opens doors that personal credit alone cannot.

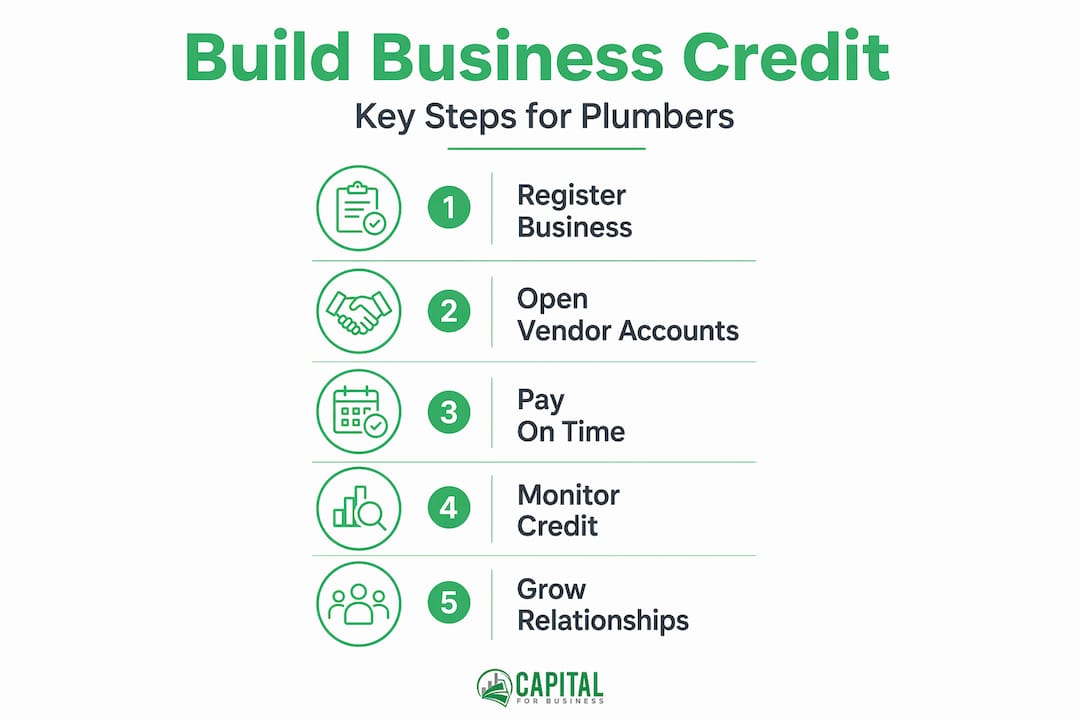

How to build strong credit for your plumbing company

Setting up and building business credit for your plumbing company requires a specific sequence of steps. Skipping steps early on means delays later, so follow this process methodically.

-

Incorporate your business or form an LLC. Sole proprietorships do not have legal separation from their owners. You need a formal business entity with its own Employer Identification Number (EIN) to establish a separate credit profile.

-

Register for a D-U-N-S number. Dun & Bradstreet assigns this nine-digit identifier to your business, and it is required before any PAYDEX score can be generated. Registration is free through D&B's website.

-

Open a dedicated business bank account and business phone line. These are basic credibility signals that bureaus and lenders use to verify your business is real and operating independently.

-

Establish vendor trade credit with suppliers who report to credit bureaus. This step is where many plumbing business owners stall. PAYDEX requires at least three payment experiences from at least two different vendors before a score can even be generated. Paying your materials supplier on time means nothing to D&B if that supplier does not report to them.

-

Apply for a business credit card. Business credit cards with low utilization rates contribute to credit mix and give you another reporting tradeline to build with.

-

Pursue equipment financing or a small business term loan. Diversifying your tradelines through credit cards, trade credit, term loans, and equipment leases signals to bureaus that your business manages multiple credit types responsibly.

-

Pay everything early or on time, every time. PAYDEX actually rewards early payment. Paying invoices before the due date can push your score above 80, which is the threshold that reduces financing costs.

Pro Tip: When you start opening vendor accounts, ask each supplier directly whether they report payment data to D&B, Experian Business, or Equifax Business. If they do not report, those payments will not help your score. Seek out vendors who do report, or consider working with credit-reporting trade credit programs specifically designed to build business credit histories.

The common challenge plumbing businesses face at this stage is impatience. Building a credit profile takes months, not weeks. Without reporting vendors, your business simply has no score regardless of how consistently you pay. Patience combined with a deliberate vendor strategy is the only path forward.

Factors that affect your score and myths to avoid

Understanding what actually moves your plumbing business credit ratings up or down saves you from wasting effort on strategies that do not work.

What genuinely impacts your score:

- Payment history. Payment history is the most influential factor across all major business credit scoring models. One late payment with limited vendors reporting can cause a disproportionate drop.

- Credit utilization. Keeping balances well below your credit limits on business credit cards and lines of credit signals responsible financial management.

- Public records. Tax liens, judgments, and bankruptcies weigh heavily on business credit scores. A single tax lien can make an otherwise healthy profile look risky to any lender.

- Account mix. Having a mix of trade credit, revolving credit, and installment loans gives bureaus more data to assess your reliability.

- Credit inquiries. Too many hard inquiries in a short window can suggest financial stress. Space out your credit applications when possible.

Myths that waste your time and money:

"Paying off all my debt will fix my score immediately." Paying off debt improves your financial position, but credit scores take time to reflect changes. Bureaus only update when vendors report, and reporting schedules vary. Do not expect instant results.

"If I pay on time personally, my business credit will be fine." Personal payment discipline has zero direct impact on your business credit profile. The two systems do not share data.

"My business already has a credit score." Different business credit scores can diverge significantly, and many businesses have a PAYDEX but no Intelliscore Plus, or vice versa. Check all three major bureaus separately.

The insight most plumbers miss is this: improving payment timeliness helps your PAYDEX score quickly, but other scores like Intelliscore Plus may lag because they also factor in utilization rates and public records that take longer to resolve. Treating all business credit scores as one unified number is a mistake that leads to confusion when your Experian score looks different from your D&B score.

How credit ratings affect financing and loan approvals

Your plumbing business credit ratings do not just affect whether you get approved for a loan. They affect how much you can borrow, at what interest rate, and whether you need to put up a personal guarantee.

Here is a realistic picture of how scores translate to financing outcomes:

| Credit Profile | Typical Outcome |

|---|---|

| PAYDEX 80 or above | Access to better rates, higher loan amounts, and favorable vendor terms |

| PAYDEX 50 to 79 | May qualify but with higher rates or lower approved amounts |

| PAYDEX below 50 | Likely declined by traditional lenders; alternative financing needed |

| No business credit score | Lenders fall back on personal credit score and may require a guarantee |

A PAYDEX score of 80 indicates strong payment reliability and directly reduces financing costs for plumbing companies. It is a practical benchmark to target before approaching traditional lenders.

Beyond approval odds, strong business credit for plumbing operations gives you negotiating power with suppliers. Net-30 or net-60 payment terms with materials suppliers can dramatically improve your cash flow on large jobs, but vendors extend those terms based on your credit profile, not just your word.

Many lenders also require a minimum of six months in business and monthly revenues of at least $10,000 alongside credit score minimums. Credit score alone does not guarantee approval. Time in business and revenue history work together with your credit rating.

If your score is currently low, you are not without options. Many lenders increasingly consider business credit scores instead of leaning solely on personal credit, which means building your business profile now pays off even if you need financing in the near term. Plumbing businesses with weaker credit can still qualify for alternative financing while working to improve their ratings over time.

Pro Tip: Before applying for any financing, check your business credit reports across all three bureaus. Lenders will see what is there, and you should too. Identifying and disputing errors before you apply can prevent unnecessary declines.

Steps to monitor and improve your credit ratings now

Taking control of your plumbing business credit ratings is less complicated than most business owners expect. The steps below can be started immediately, and each one compounds on the last over time.

-

Pull your business credit reports from all three bureaus. D&B, Experian Business, and Equifax Business all maintain separate files. Each charges a fee for full reports, but the investment is worth it. You need to know your baseline before you can improve it.

-

Review each report for errors. Incorrect payment records, outdated information, or accounts that do not belong to your business can drag scores down. Business credit reports are public, meaning errors are visible to every lender and vendor who checks. Dispute inaccuracies directly with the bureau.

-

Audit your vendor relationships. Make a list of all suppliers you pay regularly. Confirm which ones report to credit bureaus. For those that do not, evaluate whether switching to a reporting vendor makes sense for your business.

-

Set up payment reminders or autopay for all trade accounts. Even small late payments with limited vendors reporting can hurt scores significantly. Automating payments removes human error from the equation.

-

Add at least one new reporting tradeline per quarter. Gradual, steady growth in the number of vendors reporting positive payment data is more sustainable than trying to open many accounts at once.

-

Set a recurring calendar reminder to review reports quarterly. Scores change as vendors report. Regular monitoring lets you catch problems early and track your progress against realistic benchmarks.

Building credit is a slow process, but plumbing business owners who treat it like any other operational priority see measurable results within six to twelve months. Contractors who manage cash flow strategically alongside credit building tend to make faster progress because they are not scrambling for last-minute financing that could hurt their profile.

My perspective on managing business credit as a plumber

I have worked with plumbing business owners across the country for years, and the pattern is consistent. Most of them think about their business credit rating once, right before they apply for a loan. That is exactly the wrong time to start paying attention.

What I have seen actually move the needle is treating business credit as an ongoing operational task, not a one-time fix. The plumbers who build strong profiles early spend less time worrying about financing later. They get better vendor terms, access more capital, and grow without the constant scramble that comes from credit invisibility.

The hardest thing to communicate is that the score you build today determines the options you have twelve months from now. A plumbing company that spends six months adding reporting vendors, paying early, and keeping utilization low will have choices that a company ignoring credit simply will not have.

My honest advice: stop waiting until you need money to care about your credit. Start now. Pull your reports, find the gaps, and close them one tradeline at a time. The business credit system rewards patience and discipline, and those are two things most experienced plumbers already have in abundance.

— Capital

Financing options built for plumbing businesses

Understanding your plumbing business credit ratings is only the first step. Putting that knowledge to work means finding financing that fits where your business is right now and where you want it to go. Whether you have a strong credit profile and want to expand your fleet, or you are still building your score and need working capital to manage a busy season, there are loan options for plumbers designed for exactly those situations. Capitalforbusiness has worked with plumbing companies across the country since 2009, offering small business loans, equipment financing, and lines of credit. Explore the types of small business loans available to find the right fit for your goals and current credit profile.

FAQ

What are plumbing business credit ratings?

Plumbing business credit ratings are scores assigned by bureaus like D&B, Experian Business, and Equifax Business to measure how reliably your plumbing company pays its debts. They are separate from personal credit scores and use different scales and data sources.

How long does it take to build a business credit score?

Building a basic business credit score typically takes three to six months, provided you have the right vendor relationships reporting payment data. A strong, established profile with multiple tradelines can take one to two years to develop.

What is a good PAYDEX score for a plumbing business?

A PAYDEX score of 80 indicates consistent on-time payment and is a practical target for plumbing businesses. Scores above 80 reflect early payment habits and typically unlock better loan terms and vendor agreements.

Can I get a plumbing business loan with bad credit?

Yes. While strong business credit improves your loan options and terms, alternative lenders consider factors like monthly revenue and time in business alongside credit scores. Plumbing companies with weaker credit can often qualify for merchant cash advances or alternative term loans while building their ratings.

Why do vendors need to report payments for my score to count?

Business credit bureaus only record payment data that vendors and suppliers submit directly. If a vendor does not report to D&B, Experian, or Equifax Business, those payments are invisible to the credit system and do not contribute to your score regardless of how consistently you pay.