TL;DR:

- A merchant cash advance is an upfront payment for HVAC businesses, repaid through a percentage of future card sales. It is best used for short-term needs because of high costs and seasonal repayment risks. Alternative financing options often offer lower costs for equipment purchases and ongoing working capital.

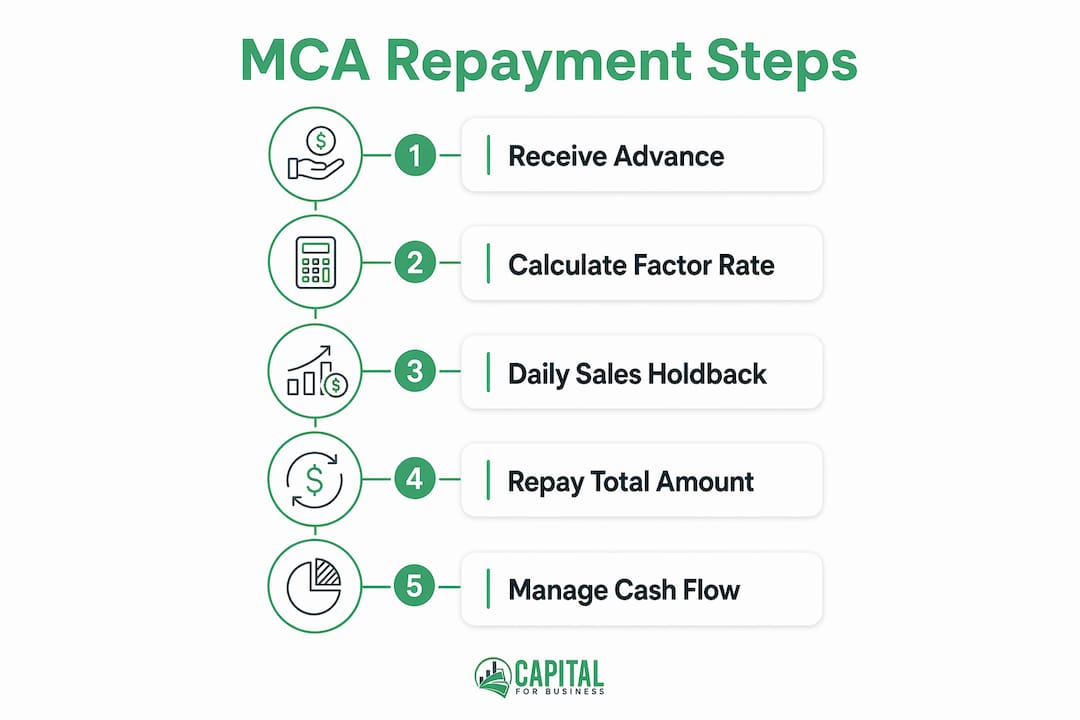

A merchant cash advance (MCA) is a financing arrangement where an HVAC business receives an upfront lump sum repaid through a percentage of future credit and debit card sales, with no traditional loan interest. Explaining merchant cash advances for HVAC owners matters because the repayment structure, cost calculation, and seasonal cash flow risks are fundamentally different from bank loans. The key concepts to understand are the holdback rate, the factor rate, and how repayment speed varies with sales volume. Capitalforbusiness has worked with HVAC contractors since 2009 and has seen firsthand how MCAs can help or hurt depending on how they are used.

How repayment and costs work in merchant cash advances for HVAC companies

The holdback rate is the percentage of your daily or weekly card sales that goes toward repaying the advance. Holdback rates generally range from 5% to 20% of daily or weekly credit and debit card sales, and some 2026 providers now offer monthly reconciliation for seasonal businesses like HVAC. Monthly reconciliation is a meaningful development. It means your repayment amount adjusts to your actual monthly revenue rather than pulling a fixed daily amount regardless of how slow business is.

The factor rate determines your total repayment cost. Factor rates typically range from 1.1 to 1.5, meaning you repay $1.10 to $1.50 for every $1.00 you borrow. Effective APRs on MCAs can vary between 40% and 350%, which makes them significantly more expensive than most traditional financing products. That range is wide because repayment speed directly affects the annualized cost.

Here is a straightforward example of how the math works:

- Advance amount: You receive $50,000 to cover payroll and parts during a busy summer season.

- Factor rate applied: At a factor rate of 1.3, your total repayment obligation is $65,000.

- Holdback rate set: Your provider sets a 10% holdback on daily card sales.

- Daily repayment: On a day with $3,000 in card sales, $300 goes to the MCA provider automatically.

- Repayment timeline: If your daily card sales average $2,500, you repay the full $65,000 in roughly 26 months at that pace.

The fixed total repayment is the critical detail. Unlike a traditional loan where paying early saves you interest, early repayment does not reduce the total MCA cost. You owe the full factor rate amount regardless of how quickly you pay it off. That structure rewards slow repayment and penalizes fast repayment, which is the opposite of how most HVAC owners think about debt.

Pro Tip: Before signing any MCA agreement, calculate the total repayment amount by multiplying the advance by the factor rate. Then divide that total by your average monthly card sales to estimate how long repayment will take. That number tells you the real cost.

What are the seasonal risks of MCAs for HVAC businesses?

HVAC businesses face a cash flow pattern that makes MCAs genuinely risky during shoulder seasons. Revenue spikes in summer and winter, then drops sharply in spring and fall. An MCA provider pulling 10%–15% of daily card sales during a slow october or april can drain your operating account faster than you expect.

The core problem is repayment rigidity. Some MCA providers pull fixed ACH debits that ignore seasonal sales variations entirely. That means your repayment amount stays the same whether you ran $5,000 in card sales last week or $500. Fixed ACH pulls during a slow season can create a cash flow crunch that forces you to take another advance just to cover operating costs.

Key risks HVAC owners face with MCAs during seasonal downturns:

- Stacking advances: Taking a second MCA to cover repayments on the first one. This compounds costs rapidly and is one of the most common mistakes Capitalforbusiness sees among HVAC contractors.

- Payroll shortfalls: Daily holdback pulls reduce the cash available for technician wages during slow months.

- Inventory gaps: Reduced operating cash limits your ability to pre-purchase refrigerant or parts before peak season.

- Credit damage: Defaulting on an MCA can trigger legal action and damage your ability to qualify for better financing later.

"MCAs are best used as emergency cash flow solutions, not long-term strategies, for immediate needs like technician payroll or emergency repairs." — HVAC financing analysis, Relay

Pro Tip: If your HVAC business has a predictable slow season, time any MCA draw to coincide with the start of your peak season. That way, high card sales volume accelerates repayment before the slow months arrive.

What financing alternatives should HVAC owners consider first?

HVAC owners should evaluate lower-cost financing options before committing to an MCA. The cost difference between an MCA and alternatives like equipment financing or supplier credit is substantial enough to affect your annual profit margin.

Equipment financing typically offers 8%–15% APR and is collateralized by the asset being purchased. That makes it far cheaper than an MCA for buying service trucks, diagnostic tools, or HVAC units. The HVAC equipment financing process is more involved than an MCA application, but the cost savings justify the extra steps for capital purchases above $10,000.

Supplier credit with net 30–60 day terms is common among HVAC distributors and is often the cheapest way to manage material purchases. If your distributor offers net 30 terms and you collect payment from customers within 14 days, you effectively finance your materials at zero cost. Most HVAC owners underuse this option.

Invoice factoring suits commercial HVAC contractors with steady B2B invoices and slow-paying clients. It is less useful for residential HVAC businesses where revenue comes from individual service calls paid at completion. If your revenue mix is primarily residential, invoice factoring will not solve your cash flow problem.

| Financing option | Typical cost | Best use case | HVAC suitability |

|---|---|---|---|

| Merchant cash advance | Factor rate 1.1–1.5 (40%–350% APR) | Emergency cash, immediate payroll | Short-term only |

| Equipment financing | 8%–15% APR | Trucks, tools, HVAC units | Strong for capital purchases |

| Supplier credit | 0% if paid on time | Parts and materials | Strong for material costs |

| Invoice factoring | 1%–5% per invoice | Commercial B2B slow payers | Limited for residential HVAC |

| Business line of credit | Varies by lender | Ongoing working capital | Strong for seasonal gaps |

Key questions to ask before choosing a financing product:

- Does the purchase involve a physical asset that can serve as collateral?

- Is the cash need tied to a specific invoice or client payment delay?

- Is the need truly an emergency, or can it wait 2–3 weeks for a lower-cost option?

- Does your business have consistent card sales volume to support MCA repayment?

Pro Tip: A business line of credit gives you access to funds without committing to a lump sum repayment. For seasonal HVAC businesses, a line of credit often costs less than an MCA and gives you more control over when and how much you draw.

How do you know if an MCA fits your HVAC business right now?

An MCA fits your HVAC business when you have a specific, short-term cash need and consistent card sales volume to support repayment. MCA providers focus heavily on daily credit and debit card sales volume for both approval and repayment predictability. If most of your customers pay by card and your monthly card volume is steady, you are a stronger MCA candidate than a business with irregular or cash-heavy revenue.

Ideal use cases for an MCA in an HVAC business:

- Emergency vehicle repair: A service truck breaks down in peak season and you need it back on the road within 48 hours. An MCA can fund the repair faster than any bank loan.

- Urgent payroll coverage: A large commercial job delayed payment and you need to cover technician wages this week. An MCA bridges that gap without missing payroll.

- Short-term inventory purchase: A supplier is offering a bulk discount on refrigerant that expires in five days. An MCA lets you act on that opportunity immediately.

- Equipment deposit: A new HVAC unit requires a deposit before installation, but the customer pays on completion. An MCA covers the deposit while you wait for the final payment.

Situations where an MCA is the wrong choice:

- Slow season borrowing: Taking an MCA in october or november when card sales are low means repayment will drag into your next slow period.

- Long-term capital needs: Financing a fleet of trucks or a major equipment upgrade with an MCA will cost two to three times more than equipment financing over the same period.

- Stacking on existing advances: Adding a second MCA while repaying the first multiplies your daily holdback burden and can destabilize your cash flow entirely.

- Covering recurring operating costs: Using an MCA to pay rent or utilities month after month signals a structural cash flow problem that an MCA will worsen, not solve.

Before applying, calculate your total repayment obligation and divide it by your average monthly card sales. That calculation gives you a realistic repayment timeline. Then check whether your card sales volume holds up during the months that timeline covers. If it dips significantly, the MCA will cost more than your factor rate implies. Consulting a financing specialist at Capitalforbusiness before signing can save you from a repayment structure that does not fit your revenue pattern. The MCA workflow for HVAC companies is straightforward once you understand the numbers.

Pro Tip: Ask your MCA provider directly whether repayments are percentage-based or fixed ACH debits. Percentage-based repayment adjusts with your sales volume. Fixed ACH does not. That single question can determine whether the product works for your seasonal business.

Key Takeaways

A merchant cash advance gives HVAC businesses fast capital but carries high costs and repayment risks that make it suitable only as a short-term, emergency financing tool.

| Point | Details |

|---|---|

| Factor rate defines total cost | Multiply your advance by the factor rate (1.1–1.5) to know exactly what you will repay before signing. |

| Holdback rate affects daily cash flow | A 5%–20% daily holdback reduces your operating cash every day until the advance is fully repaid. |

| Seasonal timing is critical | Drawing an MCA at the start of peak season reduces repayment risk during slow months. |

| Alternatives cost less for capital purchases | Equipment financing at 8%–15% APR is far cheaper than an MCA for trucks, tools, or major equipment. |

| MCAs are emergency tools only | Use MCAs for payroll gaps, urgent repairs, or short-term inventory needs, not ongoing operating costs. |

What I have learned about MCAs after years of working with HVAC contractors

HVAC owners who get into trouble with MCAs almost always share one trait: they treated the advance as a solution to a recurring problem rather than a bridge for a specific, time-limited need. I have seen contractors take their third or fourth MCA in 18 months, each one larger than the last, each one carrying a higher factor rate. By the time they reach Capitalforbusiness, their daily holdback is consuming 25%–30% of card sales and they have almost no operating cash left.

The mistake is not taking the MCA. The mistake is not having an exit plan before taking it. Every MCA should come with a clear answer to one question: what specific event will generate the cash to repay this advance? If the answer is "next season's revenue" or "business will pick up," that is not a plan. That is a hope.

The HVAC contractors who use MCAs well treat them like a tool, not a lifeline. They draw a specific amount for a specific purpose, confirm their peak-season card volume can absorb the holdback, and pay it off before the slow season starts. They also explore HVAC financing options before defaulting to an MCA, because equipment financing or a line of credit often solves the same problem at a fraction of the cost.

My honest advice: calculate the total repayment cost on paper before you sign anything. Then ask yourself whether a lower-cost product could solve the same problem with a two-week delay. If the answer is yes, take the two weeks. If the answer is no, an MCA may be exactly the right tool. The difference between a good MCA decision and a bad one is almost always that calculation.

— Capital

HVAC financing solutions from Capitalforbusiness

Capitalforbusiness has offered merchant cash advances up to $500,000 to small businesses nationwide since 2009, including HVAC contractors who need fast capital without the paperwork burden of a bank loan.

HVAC owners can access multiple financing products through Capitalforbusiness, including working capital loans, equipment financing, and business lines of credit. Each product is matched to your specific cash flow situation, not a one-size-fits-all template. If you are comparing options or need help calculating the real cost of an MCA versus alternatives, Capitalforbusiness makes it straightforward. Explore small business funding options or apply directly to find out what your HVAC business qualifies for today.

FAQ

What is a merchant cash advance for an HVAC business?

A merchant cash advance is an upfront lump sum given to an HVAC business, repaid through a fixed percentage of daily or weekly credit and debit card sales. It is not a loan and carries no traditional interest rate; instead, a factor rate determines the total repayment amount.

How does the holdback rate affect HVAC cash flow?

The holdback rate, typically 5%–20% of daily card sales, is automatically deducted from your card revenue each day. During slow seasons, this daily pull can reduce your operating cash significantly if your card sales volume drops.

Are MCAs more expensive than equipment financing for HVAC?

Yes. Equipment financing typically carries an APR of 8%–15%, while MCA effective APRs can range from 40% to 350% depending on the factor rate and repayment speed. For capital purchases like trucks or tools, equipment financing is the lower-cost choice.

Can an HVAC business with bad credit qualify for an MCA?

MCA providers focus primarily on card sales volume rather than credit scores, making MCAs more accessible than bank loans for HVAC owners with imperfect credit. Consistent daily card transactions are the primary qualification factor.

When should an HVAC business avoid taking an MCA?

An HVAC business should avoid an MCA during slow seasons, when stacking on an existing advance, or when the cash need is for recurring operating costs rather than a specific short-term gap. In those situations, a business line of credit or equipment financing is a more sustainable choice.