TL;DR:

- Securing HVAC funding requires matching the right financing product to your cash flow needs and applying during peak season for better approval chances. Proper preparation, including gathering financial documents and understanding your business cycle, increases approval likelihood and favorable terms. Different options like SBA loans, equipment financing, lines of credit, and C-PACE serve specific purposes, so choosing the correct one and planning disbursements help manage cash flow effectively.

Securing HVAC funding means matching your business's cash flow needs with the right financing product and applying at the right time to maximize approval odds. Small business owners and contractors have access to several strong options: SBA 7(a) and 504 loans, equipment financing, business lines of credit, and C-PACE financing for energy-efficiency upgrades. The challenge is not finding a product. The challenge is knowing which one fits your situation and how to present your business to a lender convincingly. This guide covers exactly that, from preparation through application to troubleshooting.

What do you need before applying for HVAC funding?

Preparation separates approved applications from rejected ones. Lenders evaluate your business on financial health, credit history, and the clarity of your funding purpose. Walking into an application without these elements in order is the fastest way to get declined or receive unfavorable terms.

The documents you need to gather before applying include:

- Recent bank statements (typically the last 3–6 months) showing consistent revenue and cash flow patterns

- Business and personal tax returns from the last 2 years to confirm income and profitability

- A current credit report for both your business and personal credit, since many lenders review both

- Profit and loss statements and a balance sheet dated within the last 90 days

- A clear funding purpose statement explaining what the HVAC equipment or upgrade will cost and how it will benefit the business

Your credit score directly affects the loan products available to you and the interest rates attached to them. A business credit score above 680 opens the door to SBA loans and traditional equipment financing. Scores below that range push you toward alternative lenders, which typically carry higher rates. Reviewing your credit management practices before applying gives you time to correct errors or pay down balances.

Seasonal cash flow is a factor that many HVAC contractors overlook during preparation. HVAC financing is unique because lenders favor applicants who document seasonal demand patterns clearly. If your revenue spikes in summer and winter and drops in spring and fall, show that pattern with labeled bank statements and a brief explanation. Lenders who understand HVAC business cycles will reward that transparency.

Pro Tip: Pull your business credit report from Dun & Bradstreet or Experian Business at least 60 days before applying. Dispute any errors early. A single incorrect delinquency can cost you a full loan tier.

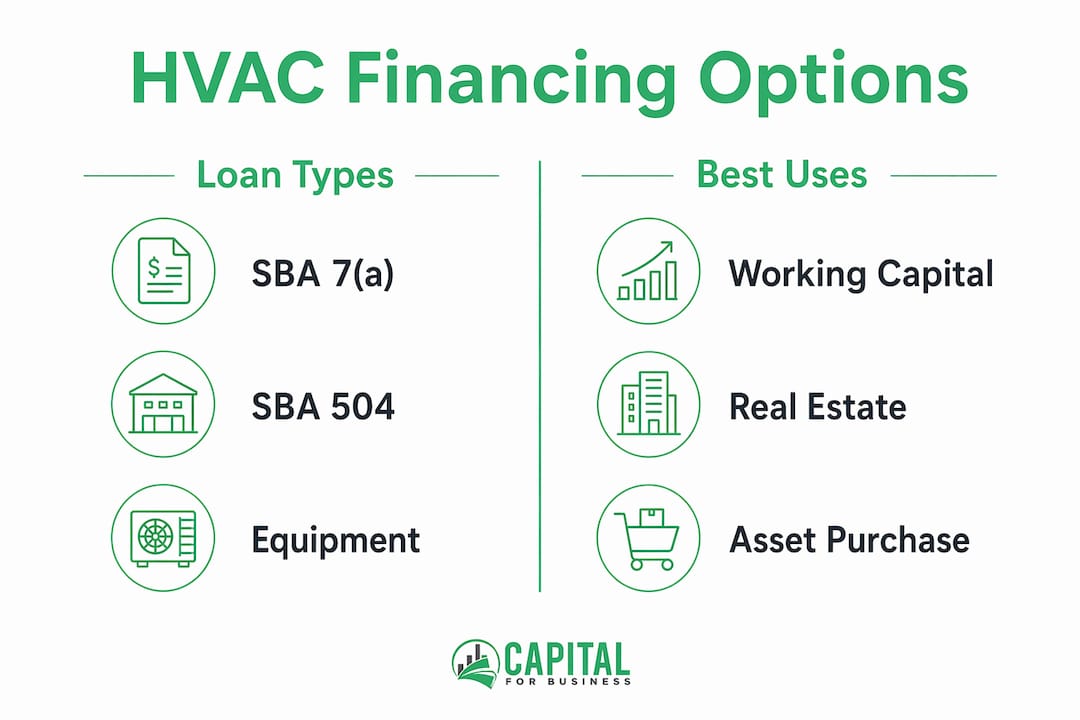

What are the HVAC financing options and their best uses?

The right financing product depends on what you are funding and when you need the money. Using a working capital loan to buy a $40,000 commercial HVAC unit is a mismatch. Using a long-term equipment loan to cover a two-month payroll gap is equally wrong. Each product has a purpose.

SBA 7(a) vs. SBA 504 loans

SBA 7(a) loans cover working capital and equipment, making them flexible for most HVAC business needs. SBA 504 loans target major fixed assets like real estate and long-term HVAC equipment installations. The 504 program typically offers lower fixed rates and longer terms, but it requires a Certified Development Company as a partner lender. If you are financing a large commercial HVAC system tied to a property you own, the 504 is worth the extra paperwork. For general working capital or smaller equipment purchases, the 7(a) is faster and more flexible. You can read more about how these programs apply to HVAC businesses in this SBA loan comparison.

Equipment financing

Equipment financing uses the purchased asset as collateral. That structure benefits you in two ways. First, approval is often easier because the lender's risk is secured by the equipment itself. Second, equipment loans keep your credit lines open for operating expenses during shoulder-season slowdowns. If you need a new commercial rooftop unit, a fleet vehicle, or diagnostic tools, equipment financing is the most direct path. Terms typically range from 24 to 84 months, and same-day funding is available through some lenders, including equipment financing options up to $250,000.

Business lines of credit

A business line of credit works like a revolving account. You draw what you need, repay it, and draw again. This product is built for seasonal cash flow gaps, not large capital purchases. If you need to cover payroll, parts, or subcontractor costs during a slow spring, a line of credit is the right tool. Capitalforbusiness offers business lines of credit up to $250,000, which fits most small HVAC contractor needs. Lines of credit also help you avoid taking on a full term loan for a short-term gap.

C-PACE financing

C-PACE (Commercial Property Assessed Clean Energy) is a specialized option for energy-efficiency HVAC upgrades on commercial properties. C-PACE ties repayment to property tax assessments rather than to the borrower's personal credit. That structure reduces the lender's credit risk and allows longer repayment terms, sometimes up to 25 years. If you own the commercial property where the HVAC upgrade will occur, C-PACE is worth serious consideration. It does not require a traditional loan application and does not affect your business credit utilization.

| Financing Type | Best Use | Repayment Structure | Credit Requirement |

|---|---|---|---|

| SBA 7(a) | Working capital, equipment | Monthly, fixed or variable | 650+ credit score |

| SBA 504 | Major fixed assets, real estate | Monthly, fixed rate | 680+ credit score |

| Equipment Financing | HVAC units, vehicles, tools | Monthly, asset-secured | 600+ credit score |

| Business Line of Credit | Seasonal cash flow gaps | Revolving, draw as needed | 620+ credit score |

| C-PACE | Energy-efficiency upgrades | Property tax assessment | Property-based, not credit-based |

Pro Tip: Never use a line of credit to fund a capital purchase. Use it for short-term gaps only. Mixing these purposes drains your available credit exactly when you need it most.

How to apply for HVAC funding step by step

A structured application process improves your approval odds and speeds up funding. Rushing the process or submitting incomplete documents is the most common reason contractors get delayed or denied.

-

Apply during the shoulder period. Applying in july or august gives lenders access to your strongest recent financials from peak season. Lenders reviewing strong summer revenue are more likely to approve and offer better terms. Applying in january after a slow fall puts your weakest statements front and center.

-

Gather all documentation before starting the application. Incomplete applications stall in underwriting. Have your tax returns, bank statements, P&L, balance sheet, and business license ready before you submit a single form.

-

Write a clear funding purpose statement. Explain what you are buying, what it costs, and how it will generate or protect revenue. A lender who understands your plan is a lender who approves your loan.

-

Submit to lenders who know HVAC business cycles. General business lenders may not understand why your revenue drops in april. Lenders familiar with contractor businesses read seasonal patterns correctly and underwrite accordingly.

-

Understand the underwriting criteria. Lenders typically evaluate time in business, annual revenue, credit score, debt service coverage ratio, and the purpose of the loan. Know your numbers before the lender asks.

-

Plan for milestone-based disbursements. HVAC contractor funding often pays out in stages. If your loan disburses in three payments tied to project milestones, you need a reserve account to cover costs between disbursements. Failing to plan for this gap is a common cash flow mistake.

Common application mistakes to avoid:

- Applying for more than you need, which raises lender concern about repayment capacity

- Mixing personal and business finances, which makes your financials harder to read

- Ignoring your personal credit score when applying for a business loan, since most lenders check both

- Submitting outdated financial documents, which signals poor record-keeping

- Applying to multiple lenders simultaneously without a strategy, which can trigger multiple hard credit pulls

Pro Tip: Open a separate reserve account before your loan funds. Deposit a fixed percentage of each payment into it. This account covers loan repayments during slow months without touching your operating funds.

How to troubleshoot HVAC funding challenges

Not every application goes smoothly. Credit issues, thin financial history, or poor timing can all create obstacles. The good news is that each problem has a practical workaround.

Credit score issues are the most common barrier. If your score is below 620, traditional SBA loans and equipment financing become harder to access. The fastest fixes are paying down revolving balances and disputing errors on your credit report. If you need funding now and cannot wait for your score to improve, bad credit business loans are a real option. They carry higher rates, but they keep your business moving while you rebuild credit.

Merchant cash advances provide fast capital based on your daily card sales rather than your credit score. Online lenders and MCAs offer near-immediate decisions, which suits short-term needs like buying parts for a large job before the customer pays. The tradeoff is cost. Factor rates on MCAs are significantly higher than traditional loan interest rates. Use them for short gaps, not long-term financing. The MCA workflow for HVAC companies explains how to use this product without overextending.

Invoice factoring is an underused option for contractors with strong commercial clients. Factoring advances a portion of your outstanding receivables based on your customers' credit, not yours. If you completed a $50,000 commercial HVAC installation and the client has 60-day payment terms, a factoring company can advance you 70–90% of that invoice immediately. You get cash now. The factoring company collects from your client later.

Cash flow planning prevents most funding emergencies. Contractors who track their monthly cash position 90 days out rarely need emergency funding. Use your working capital management practices to identify gaps before they become crises. A gap you see coming is a gap you can fund cheaply. A gap that surprises you forces expensive, fast solutions.

Pro Tip: If you use invoice factoring, only factor invoices from clients with strong payment histories. Factoring companies check your clients' credit, not yours. A client with a poor payment record can get your factoring application declined.

Key takeaways

Securing HVAC funding requires matching the right financing product to your specific cash flow need and applying during peak season when your financials are strongest.

| Point | Details |

|---|---|

| Timing your application | Apply in july or august to show lenders your strongest peak-season financials. |

| Matching product to purpose | Use equipment financing for assets, lines of credit for seasonal gaps, and C-PACE for energy upgrades. |

| Documentation readiness | Prepare tax returns, bank statements, and a funding purpose statement before starting any application. |

| Alternative options exist | Invoice factoring and merchant cash advances fill gaps when traditional loans are not accessible. |

| Reserve accounts protect you | Set aside funds before your loan disburses to cover costs between milestone-based payments. |

What I've learned from working with HVAC contractors on funding

The contractors who get funded quickly share one trait: they treat their financial records like a sales tool. They know their numbers, they can explain their seasonal patterns in plain language, and they apply before they need the money. The ones who struggle tend to apply in january after a slow fall, with outdated documents and no clear plan for how the funds will be used.

The best funding choice matches your cash flow gap rather than forcing every need into a single loan. I have seen contractors take a 10-year SBA loan to cover a 3-month payroll gap. That is an expensive mistake. A line of credit would have cost a fraction of the interest and kept the SBA loan capacity available for real capital needs.

C-PACE is the most underused option in this space. Contractors who own commercial property and want to upgrade to high-efficiency HVAC systems often do not realize that the repayment ties to the property, not their personal credit. That distinction changes the math entirely for property owners with average credit scores.

My practical advice: build a relationship with a lender who understands contractor business cycles before you need a loan. Apply for a small line of credit when your financials are strong. Use it once, repay it, and keep it open. When a real need arrives, you already have credit in place and a lender who knows your business.

— Capital

Capitalforbusiness HVAC funding solutions

Capitalforbusiness has worked with HVAC contractors and small business owners since 2009, providing fast access to the financing products that fit contractor cash flow realities.

Whether you need working capital loans up to $500,000, equipment financing with same-day decisions, or a revolving line of credit to cover seasonal gaps, Capitalforbusiness matches you with the right product quickly. The application process is straightforward, and decisions come fast. Explore the full range of small business loan options available to HVAC businesses and find the product that fits your next project.

FAQ

What is the best loan for HVAC equipment purchases?

Equipment financing is the best loan for HVAC equipment purchases because the asset itself serves as collateral, making approval easier and keeping your credit lines free for operating costs.

When should I apply for HVAC business funding?

Apply during the shoulder period, typically july or august, when your peak-season financials are fresh and show lenders your strongest revenue performance.

Can I get HVAC funding with bad credit?

Yes. Options like merchant cash advances, invoice factoring, and bad credit business loans are available to contractors with lower credit scores, though they carry higher rates than traditional loans.

What is C-PACE financing for HVAC upgrades?

C-PACE financing funds commercial HVAC energy-efficiency upgrades with repayment tied to property tax assessments rather than personal credit, making it accessible to property owners who may not qualify for traditional loans.

How do I apply for HVAC grants?

Federal and state energy-efficiency grant programs exist for commercial HVAC upgrades, but eligibility requirements vary by location and project type. Check the U.S. Department of Energy and your state energy office for current programs before applying.