TL;DR:

- Manufacturing cash flow depends on managing the cash conversion cycle, forecasting, and working capital discipline. Shortening the cycle and maintaining disciplined receivables, inventory, and payables improve liquidity and reduce financing costs. Effective segmentation and proactive management practices are crucial for sustainable cash flow growth.

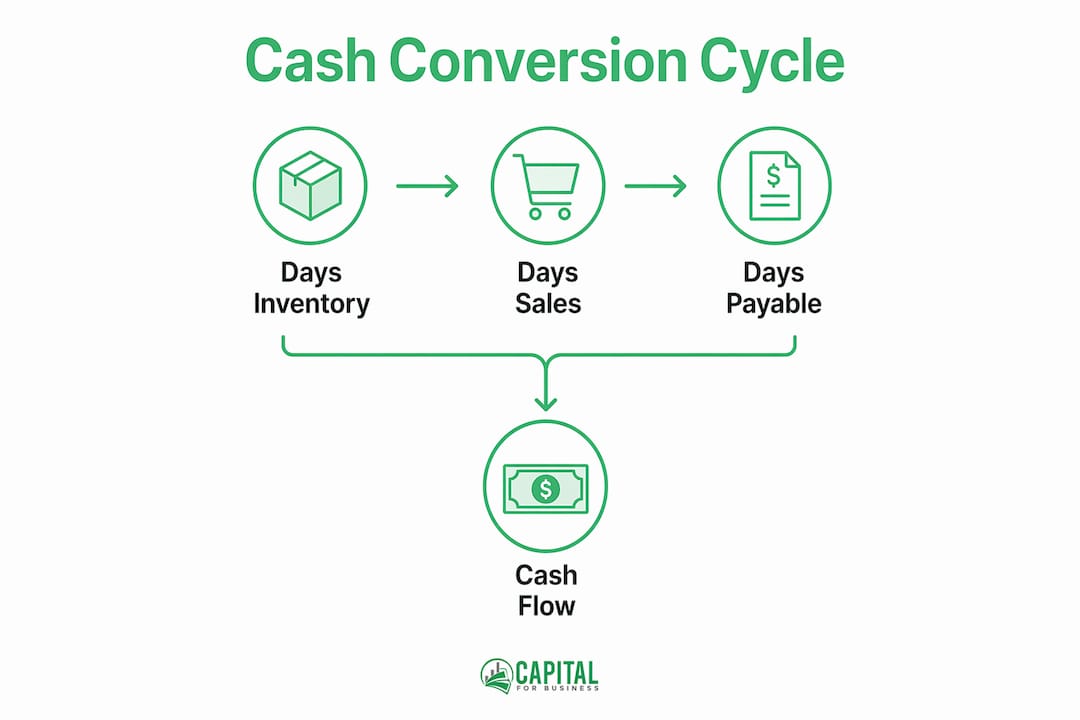

Manufacturing cash flow is defined as the net movement of money into and out of a production business across its operating cycle. Knowing how to improve cash flow manufacturing operations requires targeting three specific levers: the cash conversion cycle (CCC), forecasting accuracy, and working capital discipline. The CCC formula, CCC = Days Inventory Outstanding (DIO) + Days Sales Outstanding (DSO) minus Days Payable Outstanding (DPO), is the single most useful metric for any manufacturing financial manager. Manufacturers who treat working capital as a primary KPI and segment customers and suppliers by strategic importance consistently outperform those who manage cash reactively. This guide delivers the specific techniques that move each lever in the right direction.

How to improve cash flow manufacturing through the cash conversion cycle

The cash conversion cycle measures how long your money is tied up between paying for raw materials and collecting from customers. A shorter CCC means faster liquidity. A longer CCC means you are financing your own operations with cash you do not have yet.

Each component of the CCC responds to different management actions. DIO falls when you reduce inventory levels through lean production and SKU-specific reorder policies. DSO falls when you invoice faster and collect more aggressively. DPO rises when you negotiate longer payment terms with suppliers. The combined effect of improving all three is compounding.

| CCC Component | What It Measures | How to Improve It |

|---|---|---|

| Days Inventory Outstanding (DIO) | Days raw materials and finished goods sit before sale | Lean inventory, just-in-time systems, SKU segmentation |

| Days Sales Outstanding (DSO) | Days between invoicing and cash receipt | Immediate invoicing, early payment incentives, weekly AR review |

| Days Payable Outstanding (DPO) | Days between receiving goods and paying suppliers | Negotiate extended terms, align payables with collections |

Reducing DIO by 10 days while extending DPO by 10 days can free a significant amount of working capital without touching your revenue line. That freed capital reduces your need for short-term borrowing and lowers financing costs directly.

Pro Tip: Apply ABC analysis to your inventory before cutting stock levels. High-velocity "A" items need tight reorder policies. Low-velocity "C" items are where excess capital hides. Cut "C" items first.

The cash conversion cycle is the primary mechanism manufacturers use to improve cash flow, because it directly measures how efficiently the business converts spending into receipts. Every day you shorten the CCC is a day less that your cash is unavailable for operations or growth.

What cash flow forecasting techniques work best for manufacturers?

Accurate forecasting is the difference between arranging financing calmly and scrambling for cash at the worst possible moment. Proactive cash flow forecasting 3–6 months in advance lets you identify shortages and surpluses before they become crises. Manufacturers who forecast reactively always pay more for capital and take worse terms.

The industry standard approach uses two forecast models running simultaneously.

-

Build a 12-month foundational forecast. This model captures your full operating cycle, including seasonal demand swings, scheduled capital expenditures, and annual contract renewals. Update it monthly. Use it for strategic decisions like equipment purchases and credit line sizing.

-

Run a 13-week rolling cash flow forecast. The 13-week rolling forecast is the gold standard for day-to-day liquidity management. Update it every week. It shows you exactly which weeks carry cash risk so you can act before the shortfall arrives.

-

Standardize your data inputs. Forecasts fail when data comes from inconsistent sources. Pull accounts receivable aging, accounts payable schedules, payroll, and production costs from the same systems every week. Inconsistent inputs produce unreliable outputs.

-

Run scenario plans. Build a base case, a downside case (a major customer pays 30 days late), and an upside case (a large order arrives early). Scenario planning reveals which assumptions carry the most risk to your liquidity position.

-

Track variance weekly. Compare your forecast to actual results every week. When actuals deviate from the forecast by more than 5%, investigate the cause immediately. Variance tracking is how you make your forecast more accurate over time.

-

Use accounting or ERP software with cash flow modules. Manufacturing-focused ERP platforms integrate production schedules with financial data, which makes forecasting far more accurate than spreadsheet-based models. Cloud-based tools allow financial managers to update forecasts in real time.

Pro Tip: The 13-week rolling forecast is not a budgeting exercise. It is a liquidity management tool. Keep it simple: cash in, cash out, and ending balance for each week. Complexity kills consistency.

The 13-week rolling forecast bridges daily operations and long-term planning, enabling liquidity issues to be addressed before they become crises. Manufacturers who maintain this discipline consistently secure better financing terms because lenders see organized, forward-looking financial management.

How to manage accounts receivable and inventory to enhance cash flow

Accounts receivable and inventory are the two largest traps for manufacturing cash. Both represent money you have already spent that has not yet returned to your bank account. Managing them well is one of the most direct ways to enhance cash flow without taking on additional debt.

Accounts receivable best practices

Issuing invoices immediately upon shipment is the single fastest way to accelerate cash inflows. Every day between shipment and invoicing is a day added to your DSO for free. Set a rule: invoices go out the same day goods leave your facility.

Weekly accounts receivable aging reviews keep collections from slipping. When you review aging weekly, overdue accounts surface quickly. Follow up on overdue invoices within 24–48 hours of the due date. That response speed alone reduces DSO meaningfully across a full year.

- Invoice on the day of shipment, without exception

- Review AR aging every Monday morning before the week begins

- Follow up on any invoice past due within 24 hours

- Offer early payment discounts only when the math justifies the cost (2% net 10 is often worth it for large accounts)

- Enforce payment terms consistently; inconsistency signals that late payment is acceptable

- Flag accounts with repeated late payments for credit review before the next order ships

Inventory optimization steps

Inventory is trapped capital. Every pallet of slow-moving finished goods or excess raw material sitting in your warehouse represents cash that cannot pay wages, fund growth, or service debt. Lean production principles exist precisely to solve this problem.

Segment your inventory into high-velocity and low-velocity SKUs. Apply tight, data-driven reorder points to high-velocity items and reduce safety stock on low-velocity items. Align purchasing schedules with confirmed production orders rather than forecasted demand wherever possible. That single change reduces raw material holding costs without risking production stoppages.

Conduct a slow-moving stock review every quarter. Any item that has not moved in 90 days is a candidate for liquidation, discounting, or supplier return. Holding slow stock costs you storage, insurance, and opportunity cost simultaneously.

What are best practices for managing accounts payable and capital expenditures?

Accounts payable management is the DPO side of the cash conversion cycle. Extending DPO improves your cash position, but doing it carelessly damages supplier relationships that your production depends on. The goal is to pay as late as your terms allow while maintaining trust with your most critical suppliers.

Consolidating suppliers and negotiating payment terms aligned with your cash flow cycles is the most effective accounts payable strategy for manufacturers. When you concentrate purchasing volume with fewer suppliers, you gain negotiating leverage. Use that leverage to extend standard terms from net 30 to net 45 or net 60 where possible.

| Payment Strategy | Benefit | Risk |

|---|---|---|

| Extend terms to net 60 | Improves DPO, frees working capital | May strain smaller supplier relationships |

| Take early payment discount (2/10 net 30) | Saves money when discount exceeds borrowing cost | Reduces DPO, uses cash earlier |

| Pay on exact due date | Predictable, relationship-neutral | No benefit beyond compliance |

| Consolidate to fewer suppliers | Increases negotiating leverage | Creates single-source supply risk |

Early payment discounts require a specific calculation before you accept them. A 2/10 net 30 discount (2% off if paid within 10 days) translates to an annualized return of roughly 36%. If your short-term borrowing cost is lower than that annualized rate, take the discount. If your borrowing cost is higher, extend the payment and keep the cash.

Pro Tip: Treat your top five suppliers differently from the rest. For strategic suppliers, pay on time every time. For commodity suppliers, negotiate hard on terms. Mixing these two approaches is where manufacturers lose both money and relationships.

Capital expenditure timing also affects cash flow directly. Large equipment purchases create immediate cash outflows that can destabilize liquidity if poorly timed. Financing equipment through loans or leases converts a large one-time outflow into predictable monthly payments. Equipment financing preserves your working capital for operations while still allowing you to acquire the production capacity you need. Schedule capital expenditures during your highest-cash months whenever possible, and avoid stacking multiple large purchases in the same quarter.

Key Takeaways

Manufacturers who shorten their cash conversion cycle, maintain a 13-week rolling forecast, and manage receivables, inventory, and payables with discipline consistently achieve stronger liquidity and lower financing costs than those who do not.

| Point | Details |

|---|---|

| Cash conversion cycle is the core metric | Reduce DIO and DSO while extending DPO to free working capital without new debt. |

| Run two forecasts simultaneously | A 12-month foundational forecast and a 13-week rolling forecast cover both strategy and daily liquidity. |

| Invoice immediately, collect aggressively | Same-day invoicing and 24-hour follow-up on overdue accounts reduce DSO faster than any other single action. |

| Inventory is trapped capital | Segment SKUs by velocity and eliminate slow-moving stock quarterly to release cash tied up in storage. |

| Evaluate early payment discounts mathematically | Only take supplier discounts when the annualized return exceeds your actual short-term borrowing cost. |

What I have learned about cash flow in manufacturing after years of working with producers

Manufacturing cash flow management requires a series of informed tradeoffs, not a single formula. That is the most important thing I have seen working with manufacturers across hundreds of engagements. The businesses that struggle most are not the ones with the worst margins. They are the ones that grow fast without planning for the working capital that growth consumes.

A manufacturer that doubles revenue in 18 months can still run out of cash. More orders mean more raw material purchases, more labor costs, and longer receivables cycles, all before the new revenue arrives. Ignoring growth working capital needs during scaling causes liquidity crises even when the income statement looks healthy. I have seen profitable manufacturers miss payroll because they did not model this dynamic.

The other mistake I see repeatedly is treating all customers and all suppliers the same way. Your largest customer deserves a dedicated collections contact and a clear escalation path when invoices age. Your most critical supplier deserves on-time payment even when cash is tight. Segmenting by strategic importance, not just by dollar volume, changes how you allocate your financial management attention.

Working capital is a KPI, not a byproduct. The manufacturers who report it monthly alongside revenue and gross margin make better decisions faster. They see cash pressure building weeks before it becomes a problem. That visibility is what separates businesses that arrange financing on their own terms from those that accept whatever terms a lender offers under pressure.

— Capital

How Capitalforbusiness supports manufacturing cash flow

Manufacturing businesses face cash flow gaps that banks are slow to address. Capitalforbusiness has worked with production businesses since 2009, providing working capital loans and equipment financing that move at the speed your operations require.

When a seasonal demand spike strains your payables, or a large order requires raw material purchases before the customer pays, a business line of credit gives you the flexibility to cover the gap without disrupting production. Capitalforbusiness offers funding up to $500,000 with a fast application process designed for business owners who cannot wait weeks for a decision. Explore your small business loan options and apply today to keep your cash flow working for your business, not against it.

FAQ

What is the cash conversion cycle in manufacturing?

The cash conversion cycle (CCC) equals Days Inventory Outstanding plus Days Sales Outstanding minus Days Payable Outstanding. It measures how many days pass between spending cash on production inputs and receiving cash from customers.

How does a 13-week rolling forecast help manufacturers?

A 13-week rolling forecast shows your expected cash position for each of the next 13 weeks, updated weekly. It lets you spot liquidity shortfalls in advance and arrange financing before a crisis forces your hand.

What is the fastest way to reduce days sales outstanding?

Issue invoices on the same day goods ship and follow up on any overdue invoice within 24–48 hours. Those two practices alone reduce DSO faster than any payment term renegotiation.

When should a manufacturer take an early payment discount?

Take an early payment discount only when its annualized return exceeds your short-term borrowing cost. A 2/10 net 30 discount yields a high annualized rate, making it worth taking if your credit line costs less than that rate.

How does inventory management affect cash flow?

Excess inventory locks cash inside your warehouse instead of your bank account. Segmenting inventory by velocity and eliminating slow-moving stock quarterly releases that trapped capital back into operations.