TL;DR:

- Diversifying funding sources reduces reliance on a single revenue stream, increasing a small business's resilience against economic disruptions. It offers operational stability, planning certainty, and strategic flexibility, but also introduces management complexity and compliance challenges. Effective diversification involves gradual addition of complementary sources, regular review, and leveraging technology for streamlined management.

Funding source diversification is defined as the practice of intentionally spreading a business's financial support across multiple, distinct revenue channels to reduce dependency on any single source. For small business owners, this practice is the difference between a business that survives economic disruption and one that collapses when a single lender tightens terms or a key contract disappears. The importance of diverse funding becomes clear fast: organizations that rely on more than 70% of their income from one source face existential concentration risk that can paralyze operations overnight. This guide covers the core benefits, real challenges, and practical steps to build a funding mix that supports sustainable growth.

Why diversify funding sources: the core case for small businesses

The primary reason to diversify funding sources is risk reduction. When one funding channel fails, whether that is a bank loan being denied, an investor pulling back, or a grant program ending, a business with multiple sources continues operating. A business with only one source stops.

The industry term for this practice is revenue portfolio management, and it applies directly to how small businesses structure their capital. The concept borrows from investment theory: a portfolio of revenue streams with low or negative correlation smooths earnings and reduces overall risk exposure. That means when one funding source contracts during an economic downturn, another may hold steady or even grow, providing a natural buffer.

The benefits of funding diversification extend beyond simple risk protection:

- Operational continuity: Having 3 to 5 well-aligned revenue sources protects against budget failure when any single source falters. This is not a theoretical benefit. It is the operational floor that keeps staff paid and suppliers satisfied.

- Planning stability: Diversified companies have more reliable planning horizons and a stable base for long-term investment. When revenue is predictable, you can commit to hiring, equipment, and expansion with confidence.

- Decision-making flexibility: When no single funder controls more than 30 to 40% of your income, you retain the authority to make strategic decisions without external pressure. This autonomy is one of the most undervalued benefits of funding diversification.

- Growth enablement: New funding relationships open doors to new markets, networks, and partnerships. An equipment financing arrangement, for example, often connects small businesses to supplier networks they could not access through a standard bank loan.

- Competitive resilience: Businesses with diversified funding can absorb sector shocks that force competitors to cut operations or exit the market entirely.

Recurring revenue deserves special attention here. Monthly recurring income provides budgeting stability and increases the lifetime value of each funding relationship. For small businesses, this translates directly to subscription models, retainer contracts, and revolving credit lines that deliver predictable cash flow month over month.

What risks and challenges come with funding diversification?

Diversification is not a free lunch. The reasons for funding variety are compelling, but the operational complexity that comes with managing multiple sources is real and must be planned for.

The most common challenge is management overhead. Each funding source carries its own reporting requirements, compliance obligations, and relationship management demands. A business drawing from a bank loan, an SBA program, an equipment financing arrangement, and a merchant cash advance simultaneously must track four separate repayment schedules, four sets of covenants, and four lender relationships. Hybrid revenue models improve resilience and autonomy but require rigorous management and traceability tools to function without error.

Small businesses with lean teams face a specific risk: spreading staff too thin across funding management tasks pulls attention away from core operations. The finance function at a 10-person company is often one person wearing multiple hats. Adding three new funding sources without adding capacity creates a compliance and reporting burden that can cause missed deadlines, damaged lender relationships, and avoidable penalties.

Other challenges to anticipate include:

- Diminishing returns: Adding too many new funding streams indiscriminately spreads teams too thin. The goal is a sustainable mix, not the maximum number of sources.

- Cash flow timing mismatches: Different funding sources convert to usable cash at different speeds. A grant may take 90 days to arrive. A merchant cash advance funds in 24 hours. Matching source timing to operational needs is a critical skill.

- Mission drift: Accepting funding that comes with conditions or restrictions can pull a business away from its core strategy. Disciplined governance is required to maintain coherence when funding sources multiply.

- Increased compliance costs: Each funding relationship may require audited financials, insurance certificates, or specific reporting formats, all of which cost time and money to produce.

Pro Tip: Use accounting software like QuickBooks or FreshBooks to create separate tracking categories for each funding source from day one. Retrofitting your books after the fact costs far more time than setting up the structure correctly at the start.

Technology is the practical answer to most of these challenges. Financial management platforms, cash flow forecasting tools, and document management systems reduce the manual burden of running multiple funding relationships. The upfront investment in the right tools pays back quickly when you avoid a missed covenant or a delayed draw.

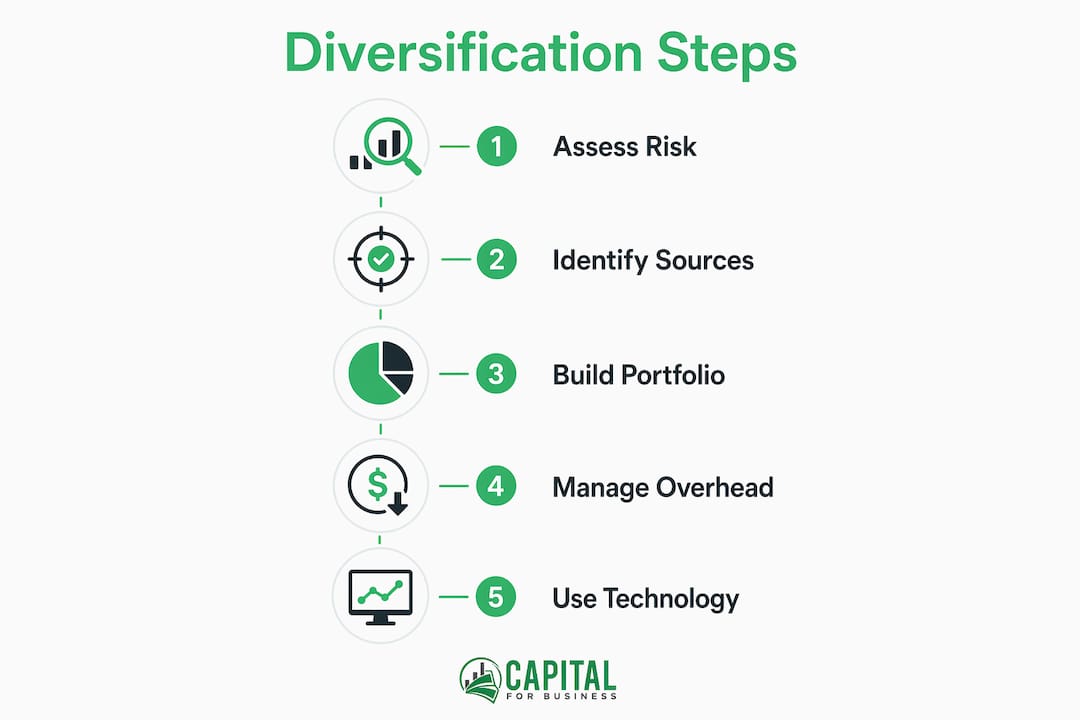

How can small businesses effectively diversify their funding sources?

Effective diversification follows a structured process, not a random accumulation of funding options. Here is a practical sequence for small business owners to follow:

-

Audit your current funding concentration. Calculate what percentage of your total capital comes from each source. If any single source exceeds 40%, you have a concentration risk that needs addressing. The operational rule is clear: over 70% from one source triggers active diversification efforts immediately.

-

Identify complementary funding types. Look for sources that behave differently under economic stress. A bank term loan and a business line of credit are both debt instruments, but they serve different purposes and carry different risk profiles. Adding equity investment or earned revenue from a new product line creates genuine diversification.

-

Set quantifiable targets. A practical diversification goal is no more than 30 to 40% dependence on any single source, with 3 to 4 significant funding channels active at any time. Write these targets into your annual financial plan so they are tracked, not just aspirational.

-

Add sources gradually. Attempting to onboard four new funding relationships in a single quarter overwhelms your team and increases the risk of errors. Add one new source per quarter, stabilize the management process, then add the next.

-

Align funding with strategy. Every funding source you accept should support your core business direction. Strategic focus on compatible funding streams avoids mission drift and keeps operational complexity manageable. If a grant or investor requires you to pivot your product line, the cost may outweigh the capital.

-

Track and review regularly. Review your funding mix quarterly. Markets change, lender appetites shift, and your own business needs evolve. A funding portfolio that was well-balanced 18 months ago may have drifted back toward concentration without active monitoring.

For small businesses exploring startup funding options across equity, debt, and alternative channels, the key is building a mix where no single source controls your operational fate.

| Funding source | Best use case | Cash timing | Control impact |

|---|---|---|---|

| Bank term loan | Capital expenditures, equipment | 2 to 4 weeks | Low, fixed covenants |

| Business line of credit | Working capital, short-term gaps | 1 to 3 days | Low, flexible draws |

| Equity investment | Rapid scaling, product development | Varies | High, ownership dilution |

| Merchant cash advance | Immediate cash needs, seasonal gaps | 24 to 48 hours | None, revenue-based repayment |

| Grants and government programs | Specific projects, R&D, hiring | 30 to 90 days | Moderate, restricted use |

Comparing funding types: which sources work best together?

Choosing the right combination of funding sources is as important as diversifying in the first place. Not all sources complement each other, and some combinations create cash flow problems rather than solving them.

Bank loans vs. equity investment represent the two ends of the control spectrum. Bank loans preserve full ownership but require regular repayment regardless of revenue performance. Equity investment provides capital without fixed repayment obligations but transfers partial ownership and decision-making authority. For most small businesses, a combination of debt financing for operational needs and selective equity for growth initiatives creates a practical balance.

Crowdfunding platforms like Kickstarter and Indiegogo serve a specific purpose: they validate market demand while raising capital simultaneously. The tradeoff is public commitment to delivery timelines and the reputational risk of a failed campaign. Crowdfunding works best as a supplementary source, not a primary one.

Government grants and SBA programs offer non-dilutive capital, meaning you do not give up ownership or pay interest. The cost is time. Applications are detailed, approval cycles are long, and funds often carry use restrictions. Businesses that build grant applications into their annual planning calendar capture this capital without disrupting operations.

Earned revenue models are the most underutilized diversification tool for small businesses. Adding a service tier, a licensing arrangement, or a subscription product to an existing business creates a revenue stream that is entirely within your control and carries no lender relationship to manage. The impact of funding sources on cash flow timing is a critical variable here: earned revenue arrives on your schedule, while debt and grant funding arrives on someone else's.

Key considerations when selecting your funding mix:

- Match the repayment timeline of debt instruments to the revenue cycle of the projects they fund.

- Prioritize sources with different economic sensitivities so they do not all contract simultaneously.

- Keep at least one revolving or flexible source, such as a business line of credit, active at all times for unexpected needs.

- Review the total cost of capital across all sources annually, not just the interest rate on individual instruments.

The most resilient small businesses treat their funding portfolio the same way a CFO at a large company treats the balance sheet: with regular review, deliberate rebalancing, and clear criteria for adding or removing sources.

Key takeaways

Diversifying funding sources is the single most effective way for small businesses to reduce financial risk while creating the stability needed for sustainable growth.

| Point | Details |

|---|---|

| Concentration risk is the core threat | Any single source exceeding 40% of total funding creates dangerous dependency that can halt operations. |

| Target 3 to 4 active sources | A practical diversification goal limits any single source to 30 to 40% of total capital for planning stability. |

| Add sources gradually | Onboarding one new funding channel per quarter prevents management overload and compliance errors. |

| Match source timing to cash needs | Different funding types convert to cash at different speeds; align each source to the operational need it serves. |

| Technology reduces complexity | Accounting and cash flow tools like QuickBooks make managing multiple funding relationships practical for lean teams. |

What I've learned about funding diversification from working with small businesses

At Capitalforbusiness, we have worked with small business owners across hundreds of industries since 2009. The pattern we see most often is not a lack of awareness about diversification. Most owners know they should not rely on a single lender or a single revenue stream. The problem is timing. Businesses typically start diversifying after a crisis forces the issue, not before one arrives.

The owners who build the most resilient operations start the diversification process early, when they have the time and leverage to be selective. A business with strong cash flow and a clean credit profile can negotiate better terms across multiple funding sources. A business scrambling after a primary lender exits has almost no negotiating power and often accepts unfavorable terms just to keep the lights on.

The second pattern we see is over-diversification without strategy. Some owners, once they understand the concept, pursue every available funding option simultaneously. The result is a management burden that consumes more resources than the additional capital justifies. The goal is a focused portfolio of 3 to 5 sources that complement each other, not a catalog of every product on the market.

One insight that rarely appears in standard financial advice: the relationship value of a diversified funding portfolio often exceeds the capital value. When you maintain active relationships with multiple lenders and investors, you have a network that can respond quickly when an unexpected opportunity or crisis arrives. A single lender relationship, no matter how strong, cannot provide that speed or flexibility.

My honest recommendation is to treat funding diversification as an ongoing operational discipline, not a one-time project. Review your funding mix every quarter. Set concentration thresholds and enforce them. Add new sources before you need them. The businesses that do this consistently are the ones that grow through downturns while their competitors contract.

— Capital

How Capitalforbusiness supports your funding diversification

Capitalforbusiness has helped small business owners build stronger, more resilient funding structures since 2009. Whether you need a term loan to anchor your funding base, a merchant cash advance to cover a short-term gap, or equipment financing to support a growth project, the right combination of products makes diversification practical rather than theoretical.

Explore the full range of small business loan types available through Capitalforbusiness to identify which options fit your current funding mix. If concentration risk is already a concern, funding solutions up to $500k are available to help you add a complementary source quickly. Capitalforbusiness works with businesses across all credit profiles, including those that banks have turned away, so your options are broader than you may expect.

FAQ

Why is it risky to rely on a single funding source?

Businesses that draw more than 70% of their capital from one source face the risk of complete operational disruption if that source withdraws or changes terms. Spreading funding across 3 to 5 sources eliminates this single point of failure.

What is a realistic diversification target for a small business?

A practical target is no more than 30 to 40% dependence on any single funding source, with at least 3 to 4 active channels. This threshold provides planning stability without creating unmanageable complexity.

How do I start diversifying if I currently have only one funding source?

Begin by auditing your current concentration, then identify one complementary funding type that serves a different operational need. Add it, stabilize the management process, and then add a second source the following quarter.

What is the biggest mistake small businesses make when diversifying funding?

The most common mistake is adding too many sources too quickly without the management infrastructure to support them. Diversification requires tracking tools, clear reporting processes, and dedicated oversight to deliver its benefits without creating new operational risks.

Do different funding sources affect cash flow differently?

Yes. Bank loans and grants typically take weeks to months to fund, while merchant cash advances and lines of credit can deliver capital within 24 to 72 hours. Matching the timing of each source to the specific cash need it serves is a critical part of effective portfolio management.