TL;DR:

- Gap financing is a short-term loan that covers the difference between primary funding and total project costs. It is a second-position loan focused on specific, time-sensitive funding needs for small businesses.

Gap financing is defined as a short-term loan that covers the difference between your primary funding and the total capital required to complete a business project or operation. Think of it as the financial layer that sits between what your main lender approves and what you actually need to move forward. Small business owners use gap loans to cover down payments, unexpected costs, and cash flow shortfalls that would otherwise stall a project. Lenders like Capitalforbusiness have offered these solutions since 2009, helping entrepreneurs across hundreds of industries keep their operations moving when traditional banks fall short.

What is gap financing and how does it work?

Gap financing is a subordinate, or second-position, loan placed behind your primary financing. That means if you default, the primary lender gets paid first and the gap lender absorbs the remaining risk. This elevated risk is exactly why gap loans carry higher interest rates and stricter repayment expectations than conventional loans.

The mechanics are straightforward. You secure a primary loan that covers most of your project cost. A funding gap remains. A gap lender steps in to cover that shortfall. Gap loans typically carry terms of 6–12 months, with repayment expected after a sale, refinance, or project completion. That short window keeps the cost of borrowing contained, but it also means you need a clear plan for repayment before you sign.

Lenders who provide gap financing focus heavily on your exit strategy and project viability rather than your credit score alone. Gap financing approval centers on exit strategy and the overall profitability of the deal. A lender wants to know how and when you will repay, not just whether you have good credit. This is a meaningful shift from traditional underwriting and one that opens the door for business owners who have strong projects but imperfect credit histories.

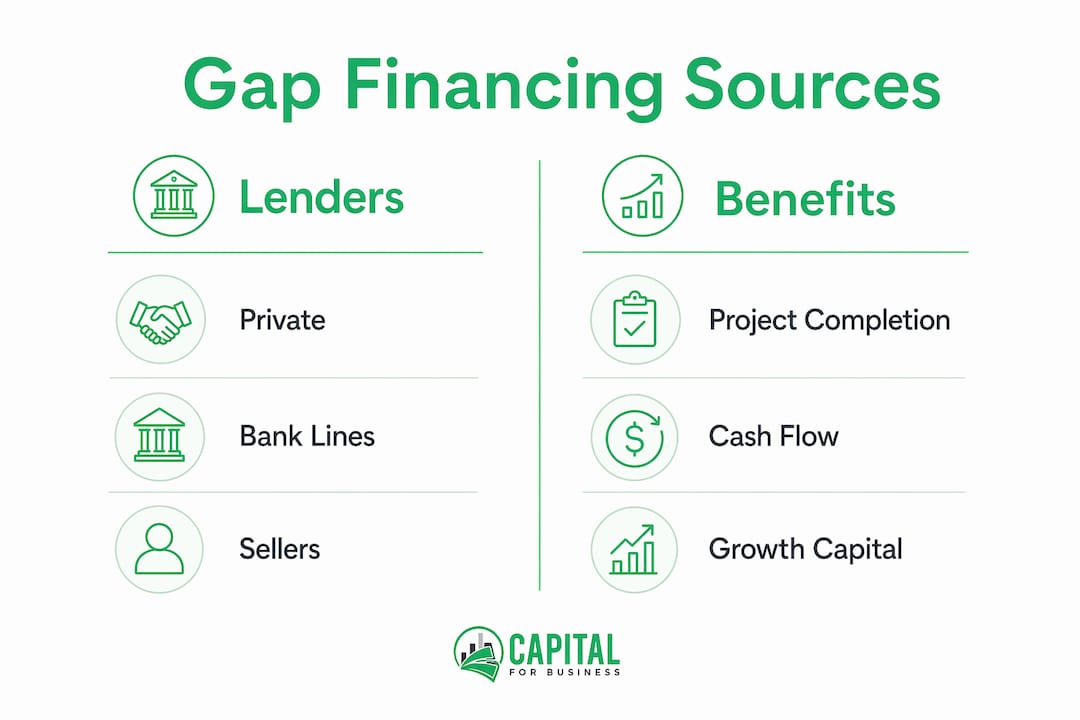

Common providers of gap financing include:

- Private money lenders: Fast approval, flexible terms, higher rates

- Community banks and credit unions: Lower rates, slower process, stricter criteria

- Seller financing: The seller carries part of the purchase price, reducing the gap size

- Business lines of credit: Revolving access to capital that can fill smaller, recurring gaps

Gap financing sources include private lenders, lines of credit, and seller financing, depending on your business profile and deal specifics. Each source carries different costs and timelines, so matching the right provider to your situation matters.

Pro Tip: Before approaching a gap lender, confirm your primary lender allows subordinate financing. Many loan agreements prohibit secondary liens without written consent, and violating that clause can trigger a default.

What are the uses and benefits of gap financing for small businesses?

Gap financing covers the funding shortfalls that would otherwise stop a project cold. Gap financing enables businesses to bridge shortfalls for critical costs, allowing projects and operations to proceed without delay and freeing up capital for other growth efforts. That ability to keep moving is the core value of a gap loan.

Common uses for gap loans

Business owners use gap financing in several practical scenarios:

- Down payment coverage: Your primary lender requires 20% down, but you only have 10% liquid. A gap loan covers the rest.

- Closing costs and fees: Transaction costs on commercial deals can run into the tens of thousands. Gap financing absorbs those without draining your operating reserves.

- Renovation overruns: Construction projects routinely exceed budget. A gap loan covers the difference between the original estimate and the final bill.

- Operational cash flow gaps: Seasonal businesses or those waiting on large receivables use gap loans to cover payroll, inventory, or rent during slow periods.

- Simultaneous deal funding: Gap financing allows entrepreneurs to run multiple deals at once by providing short-term capital without tying up personal reserves.

Key benefits of using gap loans

The advantages of gap financing go beyond simply filling a dollar shortfall:

- Speed: Gap loans can close within 7–14 days, making them one of the fastest capital solutions available for time-sensitive deals.

- Flexibility: Gap lenders evaluate deals individually, which means terms can be negotiated around your specific project timeline.

- No equity dilution: You borrow money and repay it. You do not give up ownership stake in your business or project.

- Capital efficiency: By using a gap loan instead of personal savings, you keep your own capital available for other opportunities.

- Project continuity: Delays cost money. A gap loan keeps contractors, suppliers, and timelines on track.

For small business owners who want to grow faster than their personal capital allows, gap financing is a practical tool. It lets you take on projects that would otherwise be out of reach while preserving your liquidity for day-to-day operations.

What are the costs, risks, and strategic considerations?

Gap financing is not cheap. Interest rates on gap loans range from 8% to 18%, with origination fees of 1–2% on top. That cost reflects the lender's elevated risk from sitting in a second-lien position. You need to account for every dollar of that cost before committing to a gap loan.

Understanding the cost structure

| Cost Component | Typical Range | What It Means for You |

|---|---|---|

| Interest rate | 8%–18% annually | Higher than primary loans; factor into total project cost |

| Origination fee | 1%–2% of loan amount | Paid upfront at closing; reduces net proceeds |

| Loan term | 6–12 months | Short window; repayment plan must be solid |

| Closing timeline | 7–14 days | Fast access, but fees still apply from day one |

Gap loans carry 12%–18% interest rates and upfront points, making high debt service a real risk if your project runs long or margins are thin. That rate range is not a minor line item. On a $100,000 gap loan at 15% for 12 months, you are paying $15,000 in interest alone before fees.

Risks every borrower must understand

- Profit margin erosion: In tight-margin projects, the cost of gap financing can consume the entire net profit. Run detailed cash flow projections before closing.

- Default risk from primary lender restrictions: Most primary lenders prohibit secondary liens without approval. Securing a gap loan without that consent can trigger a default clause on your primary loan.

- Repayment pressure: A 6–12 month term is short. If your project is delayed or your exit strategy falls through, you face refinancing under pressure.

- Compounding debt service: Carrying both a primary loan and a gap loan simultaneously increases your monthly obligations. Cash flow must support both.

Pro Tip: Run a full interest-accrual projection before signing. Calculate the total cost of the gap loan against your projected profit. If the numbers are close, the deal may not be viable with gap financing layered on top.

Experienced lenders also emphasize managing overall loan-to-value and loan-to-cost ratios to keep projects financially sound despite the added cost of secondary debt. Keeping your combined borrowing well below the project's total value gives you a buffer if costs rise or timelines shift.

How does gap financing compare to other short-term options?

Gap financing is one of several short-term tools available to small business owners. Understanding where it fits relative to other options helps you choose the right solution for your situation.

Bridge loans are senior, short-term loans used primarily for acquisition or refinancing. They sit in first-lien position, carry lower rates than gap loans, and are typically larger. A bridge loan replaces or precedes permanent financing rather than supplementing it. If you need a bridge loan, you can read more about short-term property financing to understand how it differs from a gap loan.

A business line of credit offers flexible, revolving access to capital at lower rates than gap loans, but it requires qualifying revenue and an established credit profile. It works well for recurring cash flow gaps but is not always available to newer businesses or those with limited credit history.

Seller financing reduces the size of the gap by having the seller carry part of the purchase price. It is often the lowest-cost option but depends entirely on the seller's willingness to participate.

| Feature | Gap Loan | Bridge Loan | Business Line of Credit | Seller Financing |

|---|---|---|---|---|

| Lien position | Second | First | Unsecured | Subordinate |

| Interest rate | 8%–18% | 6%–12% | 7%–15% | Negotiated |

| Speed to fund | 7–14 days | 2–4 weeks | 1–2 weeks | Varies |

| Best use case | Funding shortfalls | Acquisition or refi | Recurring cash gaps | Purchase price gaps |

| Credit requirement | Flexible | Moderate | Strict | None |

Gap financing is the right choice when you need capital fast, your primary lender cannot cover the full amount, and your project margins can absorb the extra cost. When your credit is strong and you need flexible ongoing access to funds, a business line of credit is often a better fit.

Practical steps to obtain and use gap financing effectively

Getting a gap loan right requires preparation. Rushing into one without a clear plan is how business owners end up with eroded margins and repayment problems.

- Quantify the gap precisely. Calculate your total project cost, subtract your primary loan amount and available equity, and identify the exact shortfall. Borrowing more than you need increases your interest burden.

- Review your primary loan agreement. Check for any clauses that restrict secondary liens. Get written consent from your primary lender before approaching a gap lender.

- Shop multiple gap lenders. Rates and terms vary significantly between private lenders, community banks, and specialty finance companies. Compare at least three offers before committing.

- Negotiate fees and terms. Origination fees and interest rates on gap loans are often negotiable, especially if your project is strong and your exit strategy is clear.

- Prepare a solid business plan and exit strategy. Gap lenders want to see how and when you will repay. A written plan with projected timelines and revenue figures strengthens your application.

- Model your cash flow under multiple scenarios. Project repayment under your expected timeline, a 3-month delay, and a 6-month delay. If the numbers break under a delay scenario, reconsider the deal structure.

- Monitor repayment timing actively. Do not wait until the loan matures to arrange repayment. If you are selling an asset or refinancing, start that process well before the gap loan term ends.

For additional context on short-term financing goals, reviewing how other business owners structure their borrowing can help you avoid common mistakes.

Pro Tip: Time your gap loan draw to match when you actually need the funds. Interest accrues from the day you draw, not the day you close the deal. Drawing early costs you money for no reason.

Key Takeaways

Gap financing is a second-position, short-term loan that fills the funding shortfall between your primary loan and your total project cost, with interest rates of 8%–18% and terms of 6–12 months.

| Point | Details |

|---|---|

| Gap financing definition | A subordinate loan covering the difference between primary funding and total project cost. |

| Typical cost range | Interest rates run 8%–18% with 1%–2% origination fees; model these costs before committing. |

| Lender approval focus | Gap lenders prioritize your exit strategy and project viability over credit score alone. |

| Primary lender consent | Always get written approval from your primary lender before securing a gap loan to avoid default. |

| Best use scenario | Gap financing works best when margins are strong, timing is critical, and repayment is clearly planned. |

Gap financing as a tactical tool, not a default strategy

At Capitalforbusiness, we have worked with small business owners since 2009, and the pattern we see most often is this: gap financing works brilliantly when it is used with precision and fails painfully when it is used out of desperation.

The business owners who use gap loans well treat them as a timing solution. They have a deal that pencils out, a primary loan in place, and a repayment event on the calendar. The gap loan fills a specific, quantified shortfall for a defined period. That is the right use of this tool.

The business owners who struggle with gap financing are the ones who use it to paper over a deal that does not quite work. If your margins are already thin and you layer on 15% interest for 12 months, you have not solved a problem. You have delayed it and made it more expensive.

My honest advice: run the numbers twice. Calculate your total debt service, including both your primary loan and the gap loan, against your projected revenue or sale price. If the gap loan cost pushes your break-even point past what the market will support, walk away from the deal or restructure it. No project is worth a default.

Gap financing can absolutely unlock growth. We have seen it help entrepreneurs take on projects that doubled their revenue in a single year. But that outcome requires discipline, a clear exit plan, and margins that can genuinely absorb the cost. If those three conditions are in place, a gap loan is one of the most effective short-term capital tools available to a small business owner.

— Capital

Capitalforbusiness funding solutions for small businesses

Small business owners who need to fill a funding gap have more options than they often realize. Capitalforbusiness has provided small business loans up to $500,000 to entrepreneurs across hundreds of industries since 2009, with fast approvals and terms designed for real business needs.

Whether you need working capital to cover a cash flow gap, a short-term loan to complete a project, or a line of credit for ongoing needs, Capitalforbusiness offers a range of small business loan options built for owners who cannot wait weeks for a bank decision. The application process is fast, the requirements are practical, and the team understands what small business owners actually face.

FAQ

What is gap financing in simple terms?

Gap financing is a short-term loan that covers the difference between your primary loan and the total amount you need to complete a project or business operation. It sits in second-lien position behind your main lender.

What are typical gap loan interest rates?

Gap loan interest rates typically range from 8% to 18% annually, with origination fees of 1%–2%. The exact rate depends on your lender, project risk, and exit strategy.

How long are gap loan terms?

Most gap loans carry terms of 6–12 months, with repayment expected after a sale, refinance, or project completion. This short duration keeps the loan focused on a specific funding need.

Can a gap loan trigger a default on my primary loan?

Yes. Most primary lenders prohibit secondary liens without written consent. Securing a gap loan without that approval can activate default clauses in your primary loan agreement.

When does gap financing make sense for a small business?

Gap financing makes sense when your project margins can absorb the extra cost, you have a clear repayment event on the horizon, and the funding gap is too large to cover with personal capital or a line of credit alone.