Securing rapid small business funding without excessive paperwork or rigid repayment terms remains difficult when time is limited. Many traditional lenders demand lengthy approval times, collateral, or restrictive repayment schedules that exclude businesses with imperfect credit or seasonal cash flow. This comparison lays out four alternatives so owners can select a loan provider that matches their timing, credit profile, and repayment needs.

Table of Contents

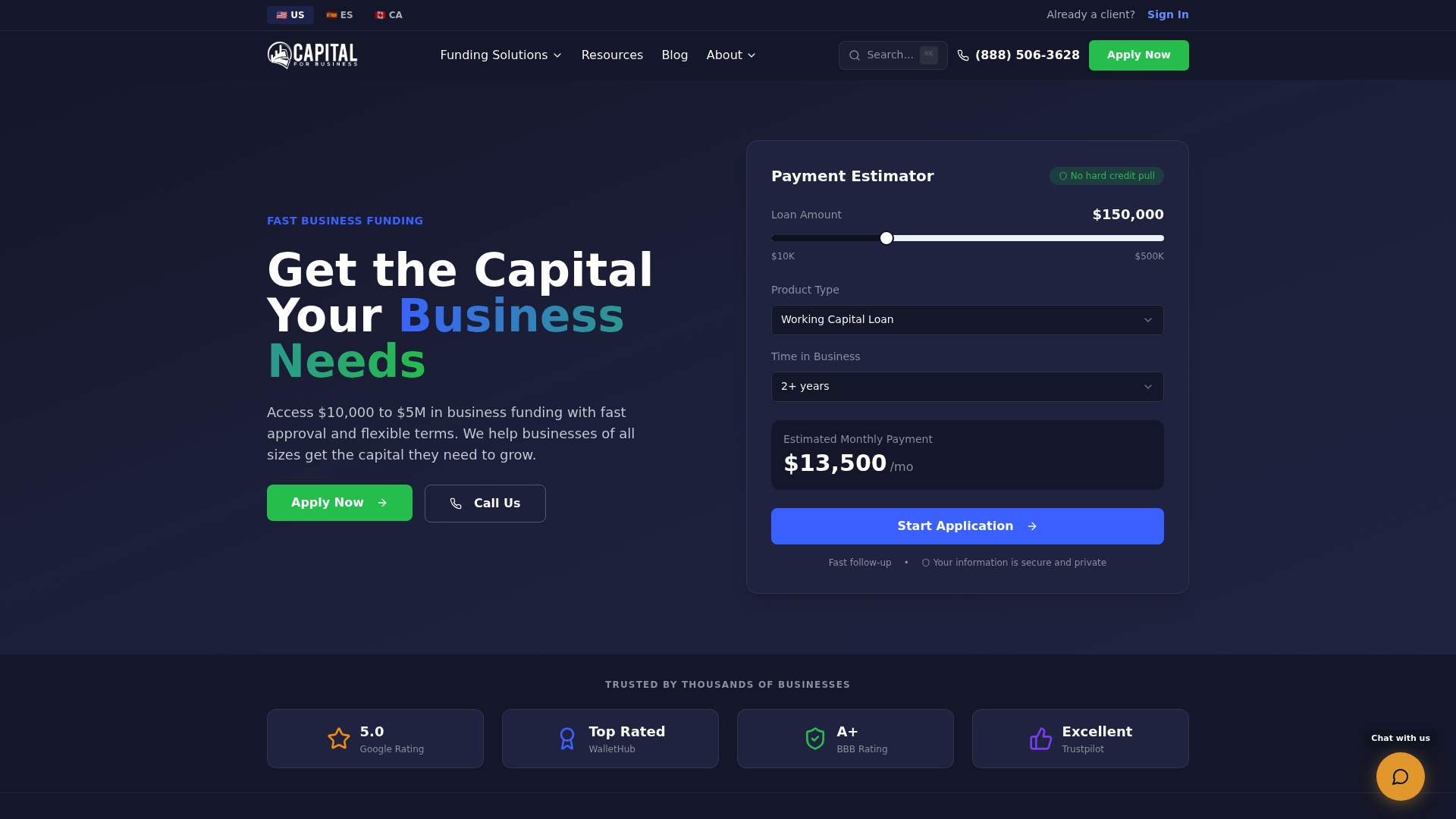

Capital for Business

At a Glance

Capital for Business reports it has funded $2 billion to 50,000 businesses since 2016. The company serves small business owners across retail, healthcare, construction, and hospitality. It pairs a broad product mix with a claim of fast approvals to meet short term cash needs.

Core Features

- Loans, lines of credit: Term loans and revolving capital for short and medium term needs.

- Equipment financing and SBA loans: Options to purchase or lease machinery and pursue government backed loans.

- Nationwide coverage: Serves businesses in all 50 US states and positions itself to serve clients in Canada as well.

- Customized industry offers and dedicated funding specialists provide one on one guidance through the application and closing process.

Key Differentiator

According to the company, approvals and funding can occur in as little as 24 hours. That speed pairs with a broad menu of industry specific products so owners can choose the funding type that matches their cash flow. The platform emphasizes tailored terms and an assigned specialist to reduce back and forth during underwriting.

Pros

-

Fast access to cash. The platform advertises quick decisions and aims to cut the time between application and funding for urgent needs.

-

Wide product mix. You can compare term loans, working capital, equipment financing, and alternative products without visiting multiple lenders.

-

Nationwide reach and local support. Coverage across all US states means owners in rural or underserved markets can apply. Dedicated specialists help translate business details into lender terms.

-

Approvals for imperfect credit profiles. The company reports it approves businesses that traditional banks often decline, which helps owners with short credit histories.

-

Transparent pricing. The service highlights clear fee disclosures rather than buried costs during closing.

Cons

- Primarily serves US based businesses, so international expansion or non US entities will find limited options.

Who It's For

Small and medium sized business owners who need quick funding and cannot wait on a bank timeline. Owners in retail, construction, healthcare, and hospitality will find relevant product options and a specialist to discuss terms. Owners who value speed over the lowest possible bank rate will get the most practical fit.

Unique Value Proposition

Dedicated funding specialists shape offers and manage the approval flow for industry specific requests. That hands on support reduces paperwork friction and helps translate seasonal revenue or contract backlog into lender friendly terms. The result is a funding path that fits short windows for inventory or project starts rather than a one size fits all quote.

Real World Use Case

A Texas retail store needed $50,000 before a holiday buying period. According to the company, the owner applied and closed on a loan within the 24 hour claim, allowing inventory purchase on time. The specialist adjusted repayment cadence to match the store s sales rhythm.

Pricing

The site does not publish a standard pricing table. Quotes are customized to the borrower s profile, product choice, and term. Interested owners must apply to receive a specific rate and fee schedule rather than a single posted starting price.

Website: https://capitalforbusiness.net

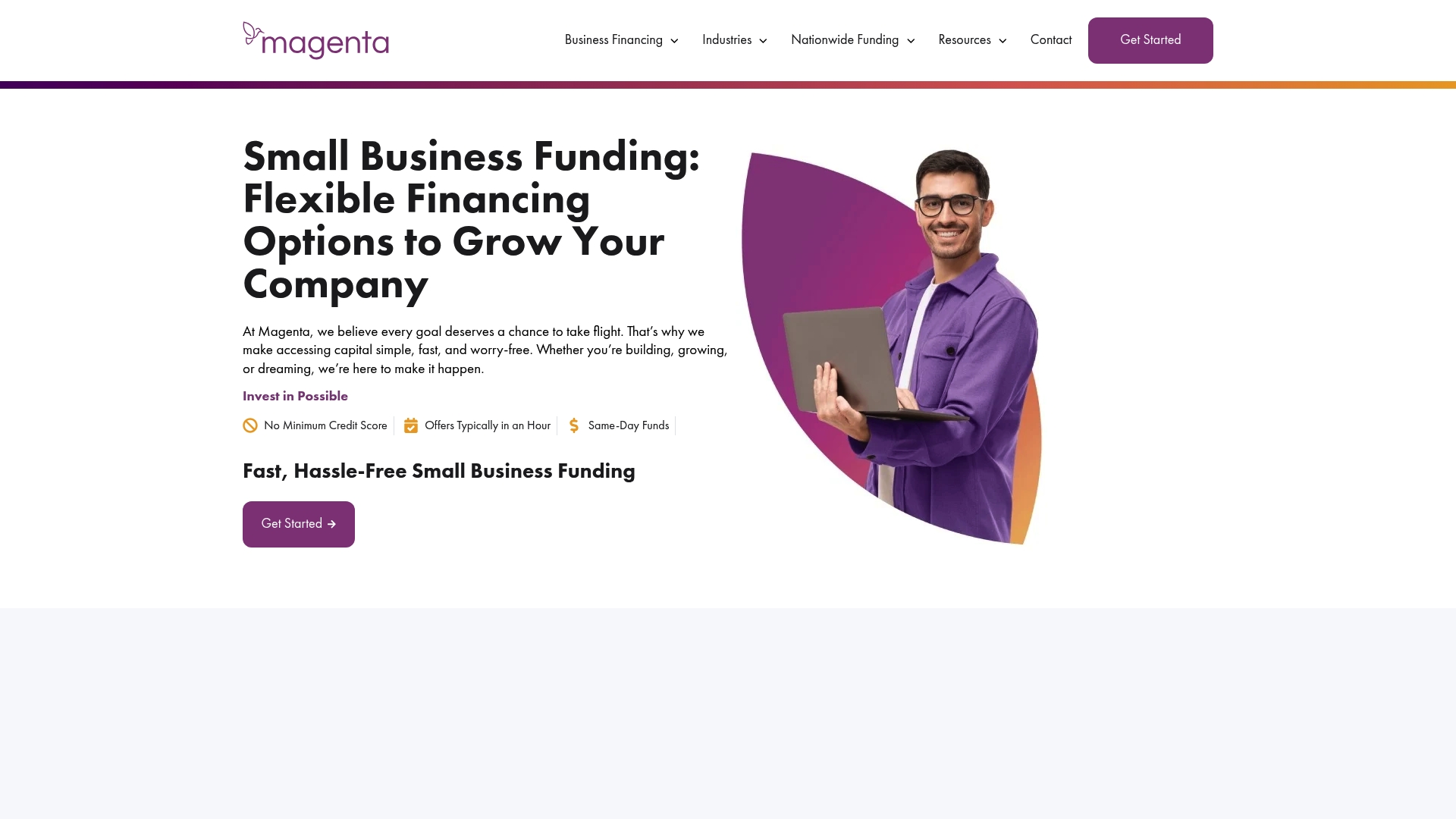

Magenta Funding

At a Glance

According to the company, Magenta typically approves applications within an hour and disburses funds the same day. The product ties financing directly to business revenue instead of fixed monthly payments. It requires at least 1 year in operation and about $15,000 in monthly revenue. That model aims to reduce pressure during slow sales months while keeping repayment proportional to income.

Core Features

Magenta focuses on a small set of finance features built around revenue performance.

- Revenue based financing that links payments to your actual sales, not a fixed amortization schedule.

- Fast approval process that the vendor reports often completes within an hour for eligible applicants.

- Same day fund disbursement when approvals clear, according to the vendor's materials.

- No minimum credit score and no collateral required for qualifying businesses.

- Flexible repayment options with discounts available for early payoff.

Key Differentiator

Magenta’s standout claim is that funding scales with your top line, so repayments rise and fall with sales. That design removes fixed loan payments and avoids selling equity. The product also advertises acceptance without a minimum credit score, which changes the pool of businesses that can apply. For owners who prefer payments tied to cash flow, that revenue linked structure is the defining difference.

Pros

-

Accessible qualification. No minimum credit score and no collateral requirement open the product to owners with thin credit histories.

-

Less strain in slow months. Because payments adjust with revenue, you pay less when sales drop and more when sales improve.

-

Speed of execution. The vendor reports approvals and funding can happen very quickly, which helps with time sensitive needs.

-

Clear use cases. The model suits inventory buys, equipment upgrades, payroll coverage, and seasonal spikes where timing matters.

-

No credit impact from applying. The company states applications do not affect your credit score.

Cons

-

Cost can exceed traditional loans. Third party reviewer signals suggest it may be pricier than bank financing for some businesses.

-

Payment unpredictability. Revenue linked repayments can swing quarter to quarter, complicating long term cash flow planning.

-

Eligibility floor. You must have at least 1 year in operation and about $15,000 in monthly revenue to apply.

When It May Not Fit

Magenta is not a good match for startups under one year of operation or businesses with monthly revenue below $15,000. Owners who need a fixed amortization schedule or lower, predictable interest cost should look to term loans or lines of credit instead. Firms that prefer collateralized borrowing will also find this product mismatched to their needs.

Who It's For

Established small and medium sized businesses that reliably clear roughly $15,000 or more per month will find Magenta relevant. Owners with credit challenges who still generate steady revenue can use this option. It also fits businesses that must act fast on seasonal or inventory opportunities and prefer repayments tied to cash flow.

Real World Use Case

A retail shop needs inventory for the holiday season. They submit an application and, according to the company, receive approval within an hour and access funds the same day. The retailer repays with a share of daily sales during the season, which lowers strain compared with a fixed loan payment.

Pricing

Pricing is not explicitly disclosed and varies by business profile and revenue. The vendor advertises that it provides transparent total repayment estimates upfront so you see the expected cost before accepting funds. Exact rates and payback amounts depend on your revenue and business profile.

Website: https://magentafunding.com

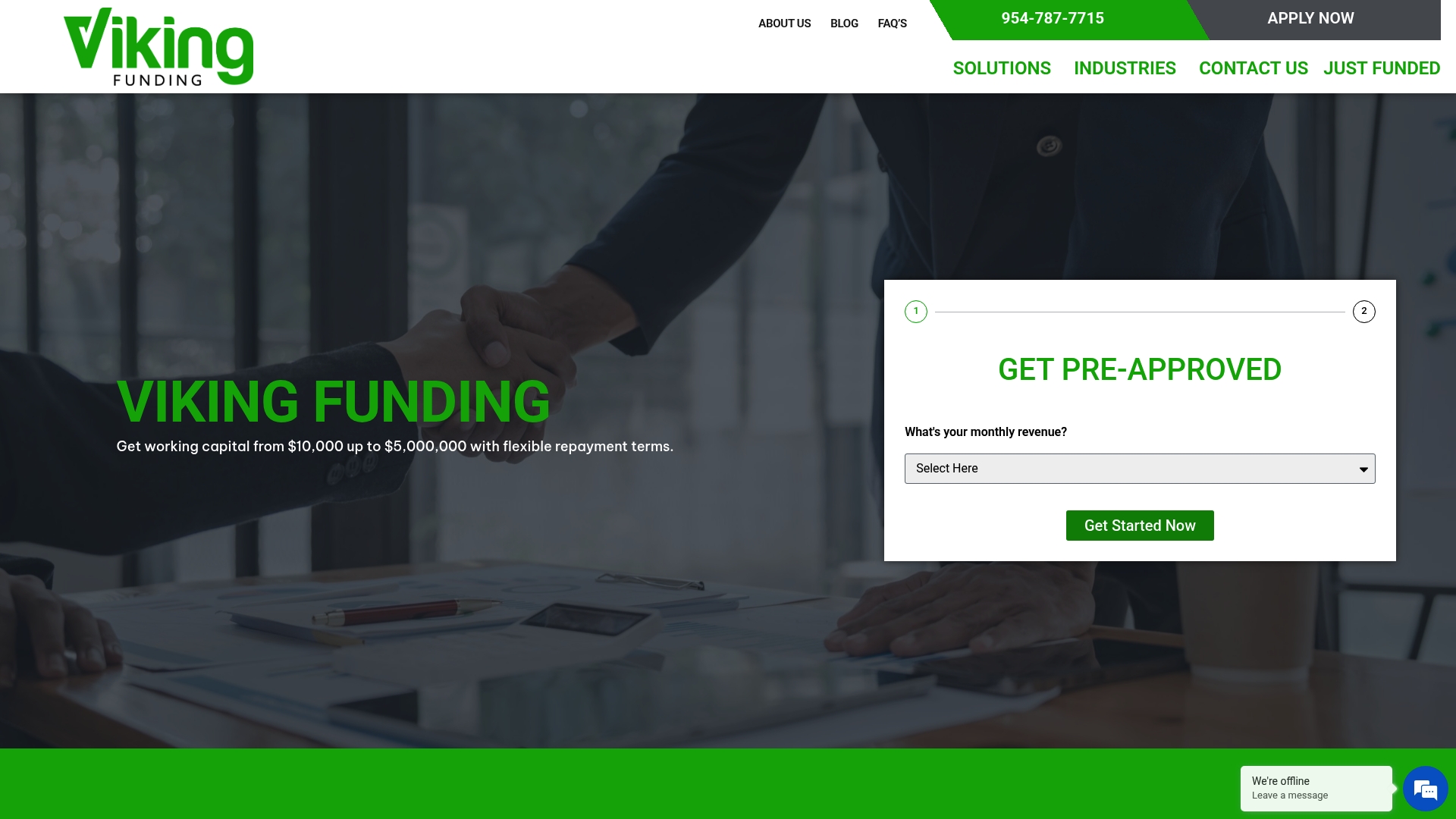

Viking Funding

At a Glance

Viking Funding's marketing materials state it can fund qualified businesses within 24 hours without credit checks or collateral. That claim targets companies with urgent cash needs, such as payroll or inventory purchases. The public messaging highlights a mix of revenue based financing, lines of credit, term loans, and SBA loan assistance.

Core Features

-

Fast approval and funding within 24 hours for eligible applicants, according to vendor materials. This shortens wait times compared with traditional bank timelines.

-

No credit checks or collateral for certain products, which lowers upfront barriers for businesses with thin credit histories.

-

A range of financing types: revenue based financing, lines of credit, term loans, and SBA loans to match different capital needs.

-

Tailored solutions and dedicated support from experienced staff to guide paperwork and repayment planning.

Key Differentiator

The product's main angle is speed and simplified underwriting. Viking Funding emphasizes rapid disbursement with limited documentation. That funding claim suits businesses that must act before a seasonal peak or to cover an unexpected shortfall. The model favors fast access over published rate transparency in public materials.

Pros

-

Speedy funding turnaround supports urgent business needs. Quick access helps cover payroll, rush inventory, or time sensitive vendor invoices.

-

Variety of financing products tailored to different situations, from short term cash needs to longer term SBA options. That variety helps match product to the use case.

-

The vendor advertises high approval rates compared with traditional lenders. Higher approvals can benefit applicants who face bank refusals.

-

No collateral or credit checks for certain financing types, which reduces entry barriers for newer businesses with limited credit history.

-

Personalized assistance from staff helps manage documents and repayment expectations. This support matters for owners who prefer hands on guidance.

Cons

-

Eligibility often requires specific revenue and time in business criteria, which can exclude startups under six months.

-

Public information offers limited clarity on pricing and total fees. That makes cost comparison difficult for rate conscious owners.

-

Alternative financing options can carry potentially high costs, especially compared with conventional bank loans.

-

May not serve every industry equally; some verticals face stricter approval conditions.

When It May Not Fit

Businesses with under six months in operation or revenues below the vendor thresholds likely will not qualify. Owners who need clear, comparable pricing may find public disclosures insufficient for apples to apples comparisons. Companies that can wait for bank terms or prefer fully transparent rate schedules should look elsewhere.

Who It's For

Small and medium sized business owners who need fast, flexible financing and who prioritize speed over detailed rate transparency. This includes retailers, restaurants, and seasonal wholesalers who need cash quickly to meet inventory or payroll demands. Owners comfortable with alternative financing should consider the trade off between speed and cost.

Real World Use Case

A retail store faces an unexpected supplier opportunity before a high season. The owner applies and, per the vendor claim, receives rapid approval and funds to purchase inventory. The quick capital lets the store meet demand that a slower bank process would have missed.

Website: https://vikingfunding.com

Fundbox

At a Glance

According to the company, $6 billion in capital has been unlocked and 500,000+ businesses have connected to Fundbox. That scale underpins its focus on embedded financing and platform partnerships. The product emphasizes rapid approvals through machine learning and aims to reduce paperwork for small business owners.

Core Features

-

Embedded capital solutions that platforms can surface directly inside their workflows. These let partners offer credit without building underwriting from scratch.

-

Fast approval process using machine learning. Fundbox uses automated underwriting to speed decisions and reduce manual review.

-

Transparent pricing and flexible repayment terms. Public content highlights no early repayment fees and an intent to show costs during application.

-

Platform integrations. Native connections to accounting and payments tools help pull transaction and invoicing data for underwriting.

Key Differentiator

Fundbox centers on fast, data driven underwriting tied to platform integrations. The platform combines transaction and accounting signals with machine learning to produce quick credit decisions. That mix makes Fundbox a natural fit for marketplaces and software vendors that want embedded financing for SMB customers. Fundbox aims to keep the application lightweight for business owners.

Pros

-

The vendor advertises quick funding decisions. That speed helps businesses cover short term cash needs without lengthy paperwork.

-

The vendor advertises a 4.8 Trustpilot score. High review counts in public listings suggest strong customer satisfaction, according to the company.

-

Deep integrations with accountants, payments, and bookkeeping platforms reduce manual data entry and speed underwriting for connected customers.

-

Reporting to business credit bureaus helps businesses build credit when they borrow and repay on a line of credit.

-

Flexible repayment terms and no early repayment fees give owners room to pay off obligations when revenue allows.

Cons

-

Public-facing documentation does not list specific interest rates or fee tables. Final pricing is disclosed during application based on underwriting.

-

Eligibility has concrete minimums. The platform typically requires at least $30,000 in annual revenue, 3 or more months in business, and a business checking account with transaction history.

-

Availability varies by state or region because of regulatory limits. Some products may be restricted depending on location.

-

Many positive claims rest on vendor marketing and review aggregators rather than independent auditing of underwriting outcomes.

When It May Not Fit

Fundbox may not suit startups with under $30,000 in annual revenue or those less than 3 months old. Businesses without a business checking account or without transaction history will struggle to qualify. Companies that need fully transparent, published rates before applying will find the model frustrating. Firms operating where regulatory restrictions apply should check local availability.

Notable Integrations

Fundbox lists native integrations with Stripe, Joist, FreshBooks, Autobooks, Synchrony, Intuit, Nav, and Zoho. These connections feed accounting and payments data into underwriting and can speed approval for connected accounts.

Who It's For

Small business owners who need working capital quickly and who already use mainstream accounting or payments software will benefit most. Platform providers or marketplaces that want embedded financing for SMB customers will find Fundbox useful for white label or integrated credit offerings.

Real World Use Case

An e commerce retailer links their bookkeeping and payments account to Fundbox. They draw a line of credit to buy inventory ahead of seasonal demand. Funds arrive faster than bank loans, and repayment aligns with sales cycles because the line can be drawn and repaid as cash flow allows.

Pricing

Public materials do not publish rates. Fundbox states pricing and fees are disclosed during the application and vary by underwriting. Borrowers receive a personalized offer that lists interest and any fees before accepting.

Website: https://fundbox.com

Comparison of alternatives

Choosing the right financing partner is critical for small business owners seeking support tailored to their unique operational challenges and goals. Below, we analyze alternatives to mulliganfunding.com focusing on how they serve small and medium-sized businesses needing fast and reliable financial solutions.

Speed of capital access

All reviewed options emphasize quick fund disbursement as a core feature, addressing pressing financial requirements:

- Capital for Business and Viking Funding both provide approvals and funding within 24 hours for qualified applicants, with Viking excelling in eliminating credit score checks and collateral requirements for some options.

- Magenta Funding leads the pack with a process designed to approve applications within one hour, offering same-day funding when eligibility criteria are met—a superior choice for businesses requiring swift resolutions to critical cash flow challenges.

Repayment structures

Flexibility in repayment terms is a vital consideration for seasonal or variable-income businesses:

- Magenta Funding prominently features revenue-linked repayment plans that adjust with sales performance, a unique and advantageous aspect for mitigating financial strain during slower operation periods.

- Fundbox, while not offering adaptive repayments, includes favorable terms with no penalties for early repayments, enabling businesses to manage debt efficiently according to earning capacity.

Best fit

- For businesses prioritizing fast funding turnaround with nationwide accessibility, Capital for Business offers dedicated specialists for personalized term adjustments and approvals within 24 hours.

- Companies with seasonal revenue patterns or the need for adaptive repayment will benefit from Magenta Funding’s revenue-based loan plans coupled with expedited approval timelines.

- Technology-forward businesses that utilize integrated solutions in their operations might find Fundbox’s platform partnerships streamline financial workflows effectively.

Our pick

Capital for Business stands out for its blend of fast approvals, widespread accessibility across the US, and personalized funding support for diverse industries. However, businesses focusing on revenue-adaptive repayment options should consider Magenta Funding as a suitable alternative.

When comparing business financing solutions, it's essential to evaluate each option on factors such as approval speed, financing types offered, and qualification requirements.

Comparison of Small Business Lending Platforms

| Product | Key Financing Types | Approval Speed | Unique Feature | Notable Limitation |

|---|---|---|---|---|

| Capitalforbusiness | Term loans, lines of credit, equipment financing | As fast as 24 hours | Nationwide coverage with dedicated specialists | Primarily serves US-based businesses |

| Magenta Funding | Revenue-based financing | Within an hour, same-day funds | Payments tied to daily income | Minimum $15,000 monthly revenue required |

| Viking Funding | Revenue-based, SBA, term loans | As fast as 24 hours | No collateral for some loans | Limited pricing transparency |

| Fundbox | Lines of credit | Automated, very fast | Integrated with accounting tools | Requires $30,000 annual revenue minimum |

Explore Reliable Mulliganfunding.com Alternatives with Capitalforbusiness

Finding fast and dependable funding is a key challenge outlined in the article comparing Mulliganfunding.com alternatives. Many small business owners struggle with slow approvals, unclear pricing, and limited product choices when seeking working capital. Capitalforbusiness directly addresses these pain points by offering quick funding decisions within 24 hours, transparent fee structures, and a broad range of loan products tailored to retail, healthcare, construction, and hospitality sectors.

If you need flexible funding that fits your unique business cycle and industry, visit Capitalforbusiness today. Start by exploring loan options designed to meet urgent inventory, payroll, or equipment investment needs without the guesswork. Get dedicated support from funding specialists who help translate your business requirements into personalized financing. Apply now to receive a custom offer and access capital that empowers your growth with confidence.

FAQ

What features make Capitalforbusiness suitable for urgent funding needs?

Capitalforbusiness provides fast access to cash, with approvals and funding occurring in as little as 24 hours. This rapid turnaround is designed specifically to address urgent cash needs such as payroll or inventory purchases, making it a practical option for business owners needing immediate funds.

How does Capitalforbusiness compare to Magenta Funding for established businesses?

Magenta Funding typically approves applications within an hour and disburses funds the same day, making it a strong choice for businesses requiring quick access to capital. However, Capitalforbusiness is particularly tailored for businesses in industries like construction and retail, providing customized offers and dedicated specialists for application assistance, which may better suit those who prefer personalized guidance.

What unique support does Capitalforbusiness offer during the financing process?

Capitalforbusiness assigns dedicated funding specialists to guide applicants through the funding process, which reduces paperwork friction and facilitates clearer communication of terms. This personalized support is particularly beneficial for businesses managing complex or industry-specific financing needs.

What are the eligibility requirements for loans from Capitalforbusiness?

Capitalforbusiness offers loans that are accessible to businesses with imperfect credit profiles, which means it can approve businesses that traditional banks often decline. This makes it a viable option for startups or entrepreneurs with limited credit history seeking immediate funding solutions.

What types of financing options does Capitalforbusiness provide?

Capitalforbusiness offers a variety of financing options, including term loans, lines of credit, and equipment financing, allowing small business owners to select the type of loan that best suits their cash flow needs and project requirements. This flexibility enables businesses to address both short and medium-term financial challenges effectively.