When your business needs flexibility and quick access to funds, finding the right financial solution can make all the difference. Companies often look for options that offer convenience and speed without the stress of traditional loans. Some lines of credit provide a safety net for unexpected expenses or growth opportunities. Others cater to specific industries or offer unique features that stand out from the crowd. With so many options out there, the search for a reliable and adaptable way to manage cash flow becomes both exciting and challenging. Which choices truly live up to the promise of helping your business move forward

Table of Contents

capitalforbusiness.net

At a Glance

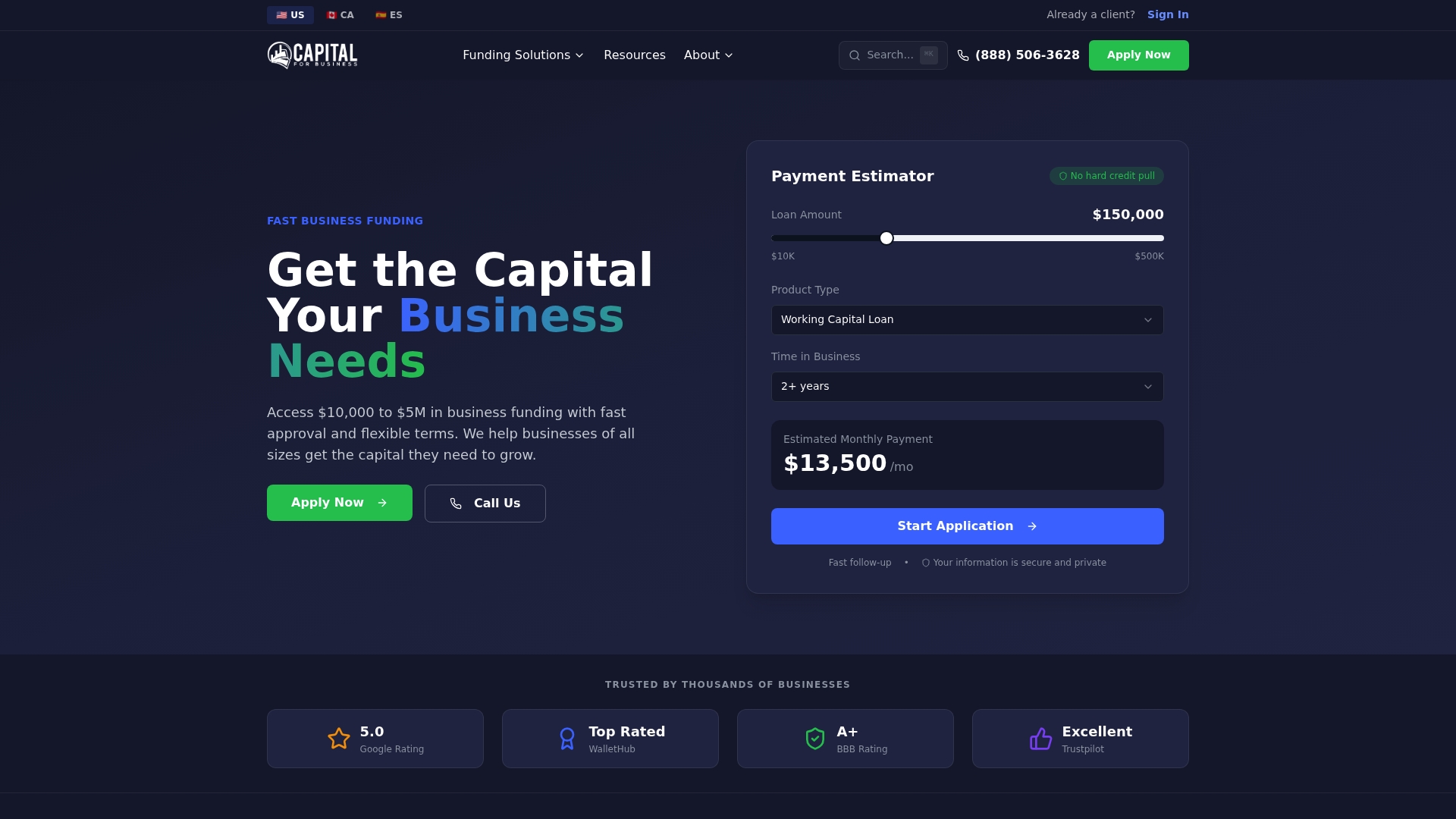

Capital for Business is the leading choice for manufacturers seeking flexible working capital and equipment financing. With national and Canadian reach and a decade plus of experience, this provider positions itself as the reliable alternative when banks and credit unions fall short.

Core Features

Capital for Business serves the small business community nationwide and in Canada by offering a large range of financial services to customers. Since 2009, the company has worked with business owners in hundreds of industries to help them expand, upgrade, and grow. As the product line expanded, Capital for Business became the most reliable lender of small business loans.

Pros

-

Broad product mix gives manufacturers access to working capital, equipment financing, merchant cash advances, credit card processing, and business lines of credit, all from one partner.

-

Proven track record since 2009 shows sustained experience underwriting commercial lenders across multiple economic cycles, which reduces execution risk for borrowers.

-

Nationwide plus Canadian reach allows multi-state and cross border operations to consolidate financing relationships with a single lender.

-

Speed and responsiveness are priorities so you secure funds quickly when bank approvals stall and production schedules depend on timely capital.

-

Competitive pricing focus means the company aims to deliver affordable options compared with alternative short term financing sources.

Who It's For

Manufacturers with recurring cash flow needs and recurring supplier payments will benefit most. Capital intensive small manufacturers that need equipment upgrades or short term working capital to bridge receivables find the product set particularly relevant. Multi location shops and firms selling to large retailers gain value from predictable financing.

Unique Value Proposition

Capital for Business combines specialized products for manufacturers with a lender mentality built around speed and accessibility. The firm meets borrowers where banks stop, offering tailored equipment loans and revolving credit that align with production cycles and vendor terms. Sophisticated buyers choose this option for the single lender model that reduces administrative overhead, the ability to layer financing types to match asset lives, and the lender experience that understands manufacturing cash flow patterns.

Real World Use Case

A mid sized sheet metal shop needs $150,000 to replace a punch press and to cover seasonal payroll while a large order ships. Capital for Business provides equipment financing for the press and a short term line to bridge payroll until receivables clear. The facility keeps production on schedule and avoids strained supplier relations.

Pricing

Specific pricing and rate schedules are not available in the current content. Capital for Business emphasizes affordable terms and quick execution, and final pricing is determined by credit profile, collateral, and loan structure.

Website: https://capitalforbusiness.net

OnDeck

At a Glance

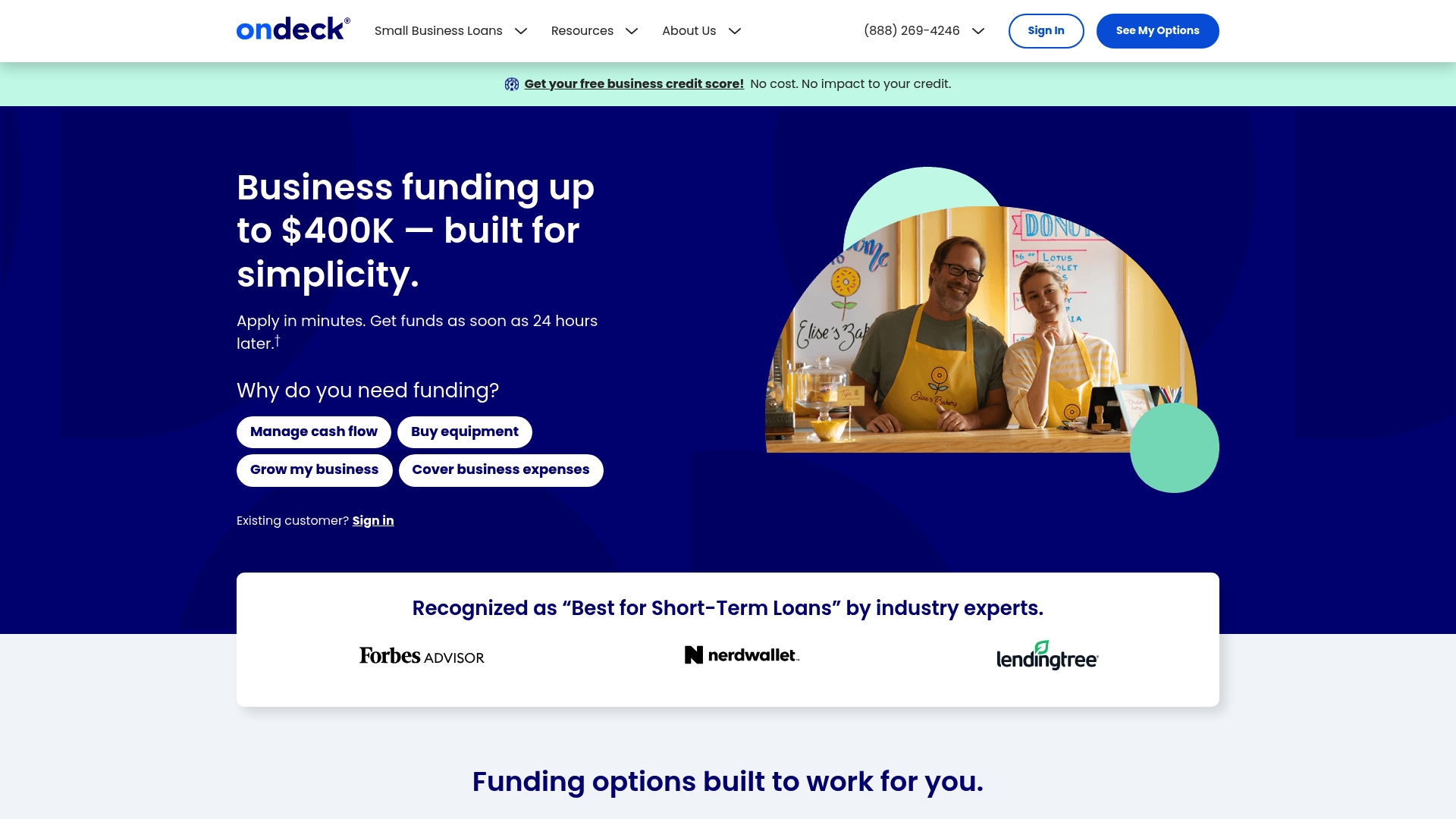

OnDeck offers fast, flexible financing aimed at small businesses that need quick access to working capital and equipment funds. Its no hard credit pulls policy and same day funding after approval make it attractive when cash needs are urgent.

Core Features

OnDeck provides a business line of credit with revolving funds, flexible repayment terms, and instant access alongside term loans with lump sum disbursement and repayment terms up to 24 months. The application is simplified for quick decisions and funding, and eligibility checks do not impact credit.

Pros

-

Fast funding: OnDeck can fund approved applicants as soon as 24 hours, which helps bridge short term cash gaps for payroll or materials.

-

No impact on credit score: Checking eligibility uses a soft inquiry so your personal FICO remains unchanged during the prequalification step.

-

High borrowing limits: OnDeck offers loans and lines up to $400K, providing meaningful capital for equipment purchases or production expansion.

-

Streamlined application: The simplified application and quick decision process reduce administrative time and speed access to capital.

-

Strong market reputation: Industry recognition and positive reviews give added confidence when comparing alternative lenders.

Cons

-

Interest rates and APRs can be very high, with averages above 56 percent which increases total borrowing cost for longer term needs.

-

Eligibility requires at least one year in business, minimum revenue thresholds, and a personal FICO score around 625 which can exclude newer or lower revenue manufacturers.

-

OnDeck restricts lending in certain regions and industries and specifically does not lend in North Dakota which limits availability for some businesses.

Who It's For

OnDeck fits small businesses that meet basic eligibility including one year of operation and roughly $100K or more in annual revenue and a personal FICO near 625. Manufacturing owners with recurring purchase orders and seasonal cash flow swings will find the revolving credit useful for smoothing operations.

Unique Value Proposition

OnDeck delivers speed and accessibility as its core advantage by combining a fast application, soft credit checks, and quick funding, with borrowing options that scale up to $400K. That combination appeals when time to cash matters more than minimizing interest expense.

Real World Use Case

A small retail business used an OnDeck line of credit to buy inventory and cover personnel costs during a seasonal expansion. Manufacturers can apply the same approach to buy raw materials, upgrade a machine, or cover payroll while awaiting large customer payments.

Pricing

Pricing is variable and depends on business creditworthiness, with average APRs around 56.4% for loans and 56.6 percent for lines of credit, which makes short term use most suitable and long term financing costly.

Website: https://ondeck.com

National Funding

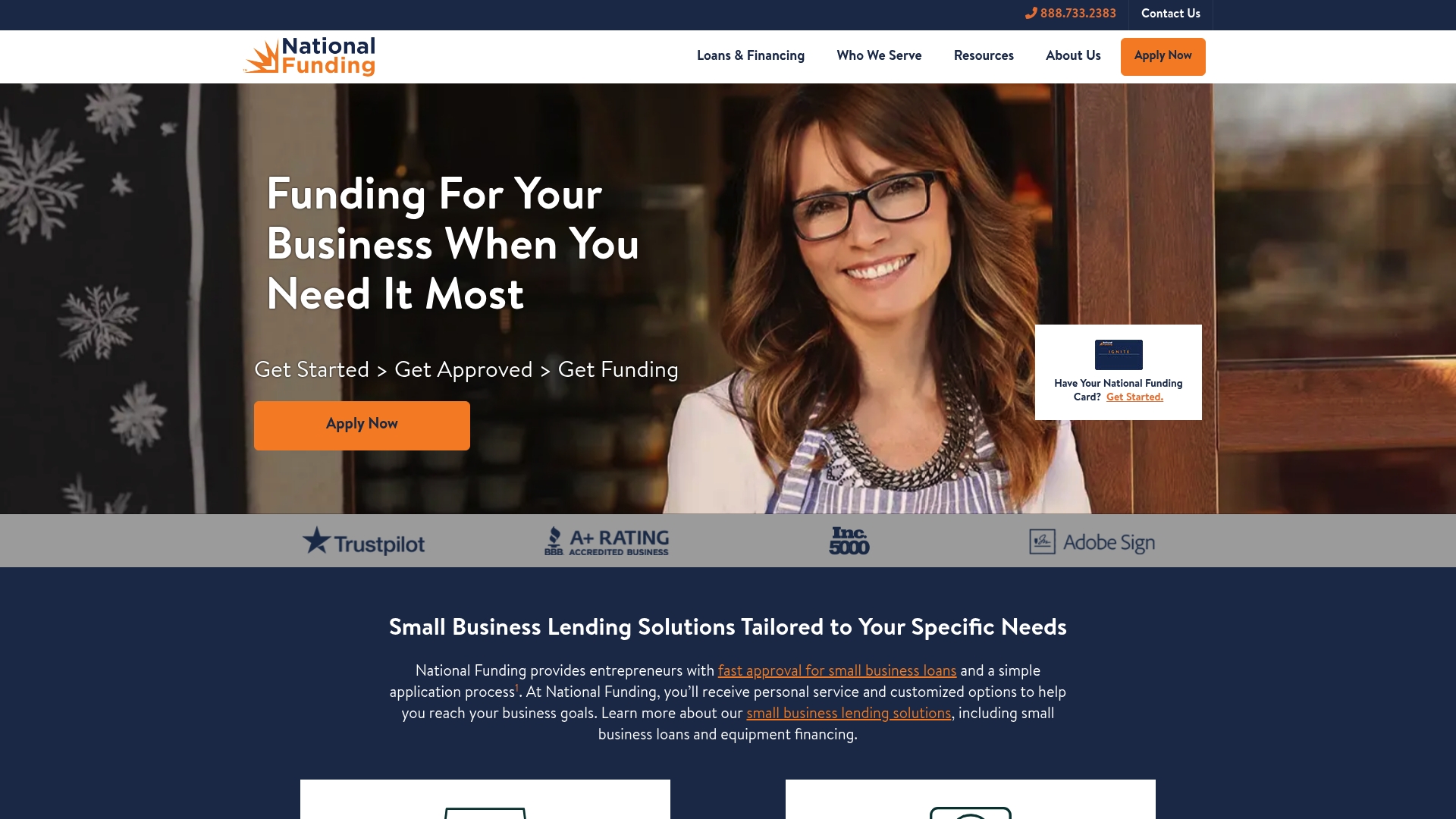

At a Glance

National Funding offers manufacturers rapid access to capital with a focus on personalized service and flexible options. Its strength is speed paired with tailored solutions for working capital and equipment financing that fit seasonal and scale up needs.

Core Features

National Funding provides a fast approval process with decision and funding in as little as 24 hours for qualified applicants. The company delivers customized lending solutions across small business loans and equipment financing with an online application and minimal paperwork.

Pros

-

Quick funding turnaround: Manufacturers facing payroll gaps or late supplier invoices can get funds in as little as 24 hours when approved, reducing production interruptions.

-

Tailored financing options: National Funding adapts loan structures to cover inventory, payroll, marketing, taxes, and equipment purchases or leases so financing matches operational needs.

-

Personal service model: Dedicated Funding Specialists guide borrowers through application and repayment, which helps manufacturers unfamiliar with finance options make informed choices.

-

Proven track record: The firm reports over $4.5 billion funded and thousands of clients, indicating experience across a wide array of industries and business cycles.

-

Accessible online process: The online application reduces paperwork and speeds decision making for busy owners who need capital without lengthy bank back and forth.

Cons

-

Eligibility thresholds limit access: The minimum requirements such as at least 6 months in business and $250,000 or more in annual sales exclude newer or very small manufacturers.

-

U.S. only service area: Businesses outside the U.S. cannot apply which matters for manufacturers operating cross border or with facilities in Canada.

-

Third party relationships for products: Some offerings involve third party lenders which can add complexity to terms and underwriting compared with direct single lender products.

Who It's For

This option suits U.S. Small to medium sized manufacturers that have been operating at least six months and report roughly $250,000 or more in annual sales. It works best for owners who need fast working capital or equipment funding before a busy season.

Unique Value Proposition

National Funding combines speed and hands on support so manufacturers can convert orders into cash flow quickly. The ability to structure loans for equipment purchase or lease alongside working capital makes it a practical one stop option when timing matters.

Real World Use Case

A small manufacturing shop secured a $50,000 working capital loan to cover payroll and buy extra inventory ahead of a seasonal spike. Funds arrived in time to meet orders, avoid overtime bottlenecks, and retain two skilled machinists through the season.

Pricing

Pricing details are not listed publicly. Applicants receive customized quotes after application and underwriting which reflect loan type, term, and risk profile.

Website: https://nationalfunding.com

National Business Capital

At a Glance

National Business Capital moves quickly to provide working capital and tailored financing for manufacturers. Their strength lies in fast approvals and a focus on cash flow based underwriting rather than heavy collateral requirements. The trade off is limited public pricing detail.

Core Features

The company offers term loans, lines of credit, equipment financing, subordinated debt, and cash flow financing with an emphasis on fast funding sometimes within 24 hours. Advisors provide industry expertise and ongoing funding strategy support aimed at operational continuity and growth.

Pros

- Fast funding turnaround: They regularly secure funds in days and advertise approvals sometimes within 24 hours, which helps you cover payroll and urgent supplier invoices.

- Cash flow focused underwriting: Approval decisions lean on revenue and potential rather than fixed assets, which benefits manufacturers with strong orders but limited collateral.

- High approval rates: Entrepreneurial underwriting increases the chance small and medium manufacturers get access when traditional lenders decline.

- Industry advisory support: Advisors who understand manufacturing operations help shape funding strategies and timing for purchases or seasonal demand.

- Relationship based approach: Ongoing support positions the lender as a partner for repeat financing needs and strategic growth planning.

Cons

- Details on actual interest rates and fee structures are not provided publicly in the extracted data, leaving cost comparisons incomplete for manufacturers shopping for credit.

- Eligibility criteria and application specifics are not detailed, which makes it hard to estimate approval likelihood for specialized manufacturers or high risk sectors.

- Limited disclosure about product restrictions or prepayment terms reduces visibility into potential downsides when planning long term capital budgets.

Who It'S For

National Business Capital fits small to medium sized manufacturers that need quick access to working capital and prefer underwriting that values cash flow over collateral. Use this when an urgent order, payroll shortfall, or equipment need cannot wait for a bank timeline.

Unique Value Proposition

The firm pairs rapid funding capability with manufacturing-aware advisors to convert near term sales and purchase orders into usable capital. That mix helps businesses bridge gaps and scale production without tying up assets as primary collateral.

Real World Use Case

A fragrance manufacturer obtained $15 million in subordinated debt after a senior lender declined funding. That capital allowed them to accelerate production, fulfill major retailer orders, and preserve operations during a critical growth window.

Pricing

Pricing details are not explicitly provided in the extracted content. Manufacturers should contact National Business Capital directly to obtain specific rates, fees, and term options for their situation.

Website: https://nationalbusinesscapital.com

Business Financing Options Comparison

This table compares various providers offering business financing services, highlighting their features, special benefits, target users, and pricing structures to assist small business owners in making informed decisions.

| Provider | Features | Advantages | Target Audience | Pricing |

|---|---|---|---|---|

| Capital for Business | Working capital, equipment financing, lines of credit, merchant cash advances | Established since 2009, nationwide and Canadian services, competitive rates, responsive and quick approval | Manufacturers requiring recurring cash flow and equipment upgrades | Determined case-by-case; emphasizes affordability |

| OnDeck | Business lines of credit, term loans, streamlined application process | Fast funding within 24 hours, up to $400K limit, no hard credit pull, simplified process | Small businesses with stable revenue over $100K/year needing fast cashflow solutions | High APRs averaging 56.4%-56.6% |

| National Funding | Small business loans, equipment financing, tailored solutions | Approval and funding within 24 hours, personalized assistance, proven track record of over $4.5 billion funded | U.S.-based manufacturers with $250K+ annual sales needing immediate working capital | Custom quoted based on case |

| National Business Capital | Term loans, cash flow financing, subordinated debt, advisors for funding strategies | Rapid funding within days, cash-flow-based underwriting, high approval rate, strategy support from manufacturing-aware advisors | Manufacturers leveraging existing revenue streams for growth without heavy collateral | Specific rates not disclosed; contact directly |

Unlock Flexible Business Lines of Credit to Fuel Your Growth

Struggling to maintain smooth cash flow or needing quick access to working capital are common challenges highlighted in the "Top 4 Business Lines of Credit 2026" article. If you face hurdles like bridging seasonal payroll gaps or upgrading equipment without long bank delays, Capital for Business offers tailored solutions designed for manufacturers and small businesses across the United States and Canada. Our streamlined approval process and flexible financing options help you stay on schedule and avoid costly production interruptions.

Key benefits include

- Fast funding when banks fall short

- Industry-aware financing that matches your cash flow cycles

- Competitive pricing focused on affordability

Explore how Capital for Business can support your working capital needs today and take control of your cash flow with confidence.

Capital for Business makes it simple to secure equipment financing, merchant cash advances, and business lines of credit tailored specifically for small manufacturers. Act now to keep your operations moving without costly delays.

Frequently Asked Questions

What is a business line of credit and how does it work?

A business line of credit is a flexible loan option that provides access to funds up to a certain limit. You can withdraw money as needed and only pay interest on the amount borrowed. To establish one, approach a lender, apply, and upon approval, you can begin using the funds as required.

What are the typical eligibility requirements for a business line of credit?

Most lenders require at least one year in business, a minimum annual revenue, and a decent credit score. Prepare your financial statements and current business documents to apply successfully, which can improve your chances of approval.

How quickly can I access funds from a business line of credit?

Depending on the lender, funds can be available as soon as 24 hours after approval. To expedite the process, ensure your application is complete and accurate, which can help you receive funds faster than traditional loans.

What can I use a business line of credit for?

You can use a business line of credit for various purposes, including managing cash flow, purchasing inventory, or covering unexpected expenses. Determine your specific financial needs and draw from the line accordingly to improve operational efficiency.

Are there any fees associated with a business line of credit?

Yes, fees can vary but often include an annual fee, maintenance fees, and interest charges on the amounts used. Review the terms and conditions carefully before applying to understand all potential costs involved in using the credit.

Can I improve my chances of approval for a business line of credit?

Yes, you can enhance your approval chances by maintaining a strong credit score, having solid business financials, and demonstrating a consistent cash flow. Consider creating a detailed business plan to present to potential lenders, which can significantly strengthen your application.