TL;DR:

- Lending provides essential capital for restaurant startups to cover buildout, equipment, and operating expenses before revenue stabilizes.

- A well-structured funding stack, including SBA loans and vendor credit, reduces risks and supports long-term growth.

Lending is the primary financial mechanism that gives restaurant startups access to the capital required for equipment, leasehold improvements, inventory, marketing, and working capital before a single customer walks through the door. The role of lending in restaurant startups goes far beyond simply covering opening costs. It determines whether you have enough runway to survive the slow months, absorb unexpected expenses, and grow with intention. Key loan products used in this space include SBA 7(a) loans, equipment financing, and business lines of credit. Your creditworthiness, business plan quality, and available collateral will shape which of these tools you can actually access.

What types of loans are available for restaurant startups?

Restaurant startup financing, the industry term for the full range of capital solutions used to launch a food service business, covers several distinct loan products. Each one serves a different purpose and carries different qualification requirements. Knowing the difference before you apply saves time and protects your credit.

SBA 7(a) loans

SBA 7(a) loans are the most common and cost-effective source of restaurant startup capital. They provide up to $5 million with terms up to 25 years and require 10–30% owner equity. Lenders prefer a credit score of 680 or above, and approval typically takes 60–90 days. That timeline is slow, but the long repayment terms keep monthly payments manageable during the critical early period.

Conventional bank loans

Conventional bank loans carry stricter requirements than SBA products. Banks typically require a 25–30% down payment, a credit score above 720, significant collateral, and 3–5 years of restaurant experience. Restaurants are classified as high-risk borrowers by most traditional lenders. That classification means fewer approvals and higher collateral demands for first-time operators.

Equipment financing

Equipment financing covers the physical assets your kitchen cannot operate without: commercial ovens, refrigeration units, dishwashers, and point-of-sale systems. The equipment itself serves as collateral, which makes approval easier than unsecured loans. This product is well suited for operators who want to preserve SBA loan funds for buildout and working capital rather than spending them on depreciating assets.

Merchant cash advances and revenue-based financing

Merchant cash advances and revenue-based financing require existing revenue to qualify. MCA effective APRs often exceed 25% and can exceed 100%. That cost structure makes them entirely unsuitable as startup capital. They are short-term tools for established businesses managing cash flow gaps, not for operators who have not yet opened their doors.

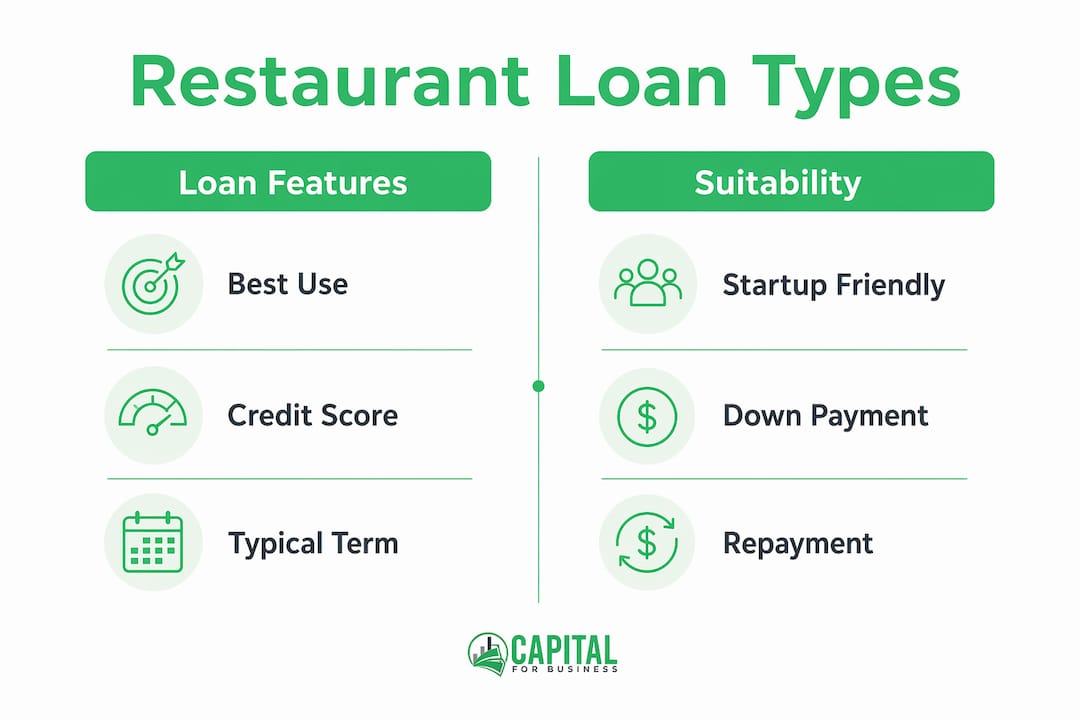

Comparison of common restaurant loan types

| Loan type | Best use | Credit score needed | Typical term | Startup-friendly? |

|---|---|---|---|---|

| SBA 7(a) loan | Buildout, equipment, working capital | 680+ | 10–25 years | Yes |

| Conventional bank loan | Large capital needs with strong credit | 720+ | 5–10 years | Limited |

| Equipment financing | Commercial kitchen assets | 620+ | 2–7 years | Yes |

| Business line of credit | Post-opening cash flow gaps | 650+ | Revolving | Post-opening |

| Merchant cash advance | Short-term revenue gaps | Revenue-based | 3–18 months | No |

Pro Tip: Apply for your SBA loan at least 90 days before your target opening date. The approval process is slow, and delays can push back your lease start date and increase pre-opening costs.

How does lending impact the success of a restaurant startup?

Adequate funding is the single most direct predictor of whether a restaurant survives its first year. A typical restaurant startup requires $175,000 to $500,000 in capital, with a median budget around $375,500. That figure covers buildout, equipment, inventory, and the working capital needed to sustain operations until the business reaches break-even. Running out of cash is the top reason restaurants fail in their early months.

The importance of cash runway

Cash runway refers to how many months you can cover operating expenses without relying on revenue. Industry guidance recommends maintaining 3–6 months of operating capital at opening. Restaurants rarely hit consistent revenue in the first 60 days. Staff training, menu adjustments, and marketing all consume cash before the customer base stabilizes.

Lending directly funds that runway. Without it, a slow week in month two can become a crisis. With it, you have the time to adjust your operations, refine your menu pricing, and build repeat business without the pressure of an empty bank account.

Managing cash flow fluctuations

Seasonal slowdowns, unexpected equipment repairs, and supplier price increases all create cash flow gaps that even well-run restaurants face. Lending gives you a buffer. A business line of credit, for example, lets you draw funds when you need them and repay when revenue recovers. That flexibility is not available to operators who launched undercapitalized and spent every dollar on opening day.

Lending as a growth tool

Lending also enables strategic growth after the initial launch. Operators who build a strong repayment history on their startup loan create the credit profile needed to access renovation financing, additional location funding, or equipment upgrades later. The first loan is not just a survival tool. It is the foundation of your long-term borrowing relationship with lenders.

Pro Tip: Track your debt service coverage ratio (DSCR) from day one. Lenders want to see a DSCR of at least 1.25x, meaning your monthly revenue covers loan payments with 25% to spare. Knowing your number early helps you plan repayment before it becomes a problem.

What are the key challenges when seeking loans for restaurant startups?

The restaurant industry carries one of the highest failure rates of any sector, and lenders know it. That perception creates real friction for first-time operators seeking capital. Understanding the specific hurdles before you apply puts you in a stronger position to address them.

-

High-risk classification. Banks view restaurants as high-risk because of thin margins, high labor costs, and volatile consumer demand. This classification results in stricter credit score requirements, higher collateral demands, and lower loan-to-value ratios compared to other industries.

-

Limited operator experience. Lenders assess operators, not just business plans. First-time restaurateurs without documented industry experience face significant difficulty securing traditional loans. Successful applicants often bring on partners with established track records or use real estate equity to offset the experience gap.

-

Inadequate business plans. A business plan without detailed financial projections, a realistic break-even analysis, and a clear market positioning statement will not satisfy a commercial lender. Generic templates do not work. Your plan needs location-specific revenue assumptions and a cost structure that reflects actual vendor quotes.

-

Misuse of high-cost capital. Some first-time operators turn to merchant cash advances when traditional lenders decline their applications. This is a costly mistake. Using a product with an effective APR that can exceed 100% to fund a buildout creates a debt burden that most new restaurants cannot service. The MCA process guide at Capitalforbusiness explains when these products are and are not appropriate.

-

Investor agreement gaps. Equity investors may take 10–49% ownership in exchange for capital. Without a professionally drafted operating agreement that defines governance, profit-sharing, and exit terms, founder-investor disputes become common and expensive. Verbal agreements do not hold up when a restaurant starts generating real money.

-

Collateral shortfalls. Many first-time operators do not own real estate or other significant assets. Without collateral, lenders either decline the application or require a personal guarantee. Knowing your collateral position before applying helps you target the right lender and loan product.

Pro Tip: If you lack restaurant experience, consider partnering with a seasoned operator as a co-applicant or advisor. Their track record can satisfy lender requirements that your personal history cannot meet alone.

How to structure a practical funding strategy for your restaurant

A well-structured funding plan combines multiple capital sources to cover different cost categories without over-relying on any single product. This approach, often called a funding stack, reduces risk and keeps your debt service manageable from day one.

A practical example from the SBA loan funding model looks like this: a $300,000 SBA loan covers the buildout and major equipment, $56,000 in owner equity covers soft costs and deposits, and $19,500 in vendor credit terms covers initial inventory. At a projected $48,000 in monthly revenue, this structure produces a DSCR of 1.25x, which satisfies most lender requirements.

Key elements of a strong funding stack

- Owner equity (10–30% of total costs). Lenders require skin in the game. Personal savings, retirement account rollovers, or proceeds from a property sale all qualify. The more equity you contribute, the better your loan terms.

- SBA or bank loan for major costs. Use long-term debt for buildout, leasehold improvements, and large equipment purchases. These are assets that generate revenue over years, so matching them to long-term debt makes financial sense.

- Equipment financing for kitchen assets. Separate your commercial kitchen equipment from your SBA loan. Equipment financing uses the asset as collateral and often closes faster than SBA products.

- Vendor credit terms for inventory. Many food and beverage distributors offer net-30 or net-60 payment terms to new accounts. This is free short-term capital that reduces your cash need at opening.

- Business line of credit post-opening. Lines of credit offer flexible capital at lower rates than merchant cash advances. Apply for one after you have three to six months of operating history to show a lender.

Loan application preparation checklist

Before you submit any application, confirm you have the following ready:

- Personal credit report reviewed and errors corrected

- Two years of personal tax returns

- Detailed business plan with financial projections for 24 months

- Signed lease or letter of intent for your location

- Contractor bids for buildout work

- Equipment quotes from vendors

- Personal financial statement showing assets and liabilities

- Resume or biography documenting your restaurant or business experience

Preparation at this level separates applicants who get funded from those who get declined. Lenders make faster decisions when the documentation package is complete on the first submission. You can also explore restaurant financing options at Capitalforbusiness to compare products before you apply.

Key takeaways

Lending is the structural foundation of restaurant startup success, and the right combination of loan products determines whether you open strong or run out of cash before you find your footing.

| Point | Details |

|---|---|

| SBA loans are the best starting point | They offer the lowest cost and longest terms for restaurant startup capital. |

| Cash runway is non-negotiable | Secure 3–6 months of operating capital before opening to survive slow early months. |

| MCAs are not startup tools | Effective APRs above 100% make merchant cash advances unsuitable for launch funding. |

| Lenders evaluate you, not just your plan | Industry experience and collateral matter as much as your business concept. |

| A funding stack reduces risk | Combining SBA loans, equipment financing, and vendor terms spreads debt across cost categories. |

What I have learned about restaurant lending after years in the field

Working with restaurant owners since 2009 at Capitalforbusiness has shown me one consistent pattern: the operators who struggle most are not the ones with the weakest concepts. They are the ones who underestimated how much capital they actually needed and overestimated how quickly revenue would stabilize.

The conventional advice says to get a loan and open your doors. What that advice misses is the gap between opening day and the point where your restaurant actually runs at a profitable pace. That gap is where most first-time operators get into trouble. They borrow enough to open, but not enough to survive the learning curve.

My honest view is that the importance of credit for restaurants goes beyond the initial application. Your credit profile is a long-term asset. Every on-time payment builds the borrowing capacity you will need when you want to add a second location, renovate your dining room, or upgrade your kitchen. Operators who treat their first loan as a one-time transaction miss the compounding benefit of building a strong lender relationship.

I also think too many first-time restaurateurs avoid equity investors out of fear of losing control, then turn to high-cost debt products instead. A well-structured equity deal with a clear operating agreement is often cheaper in the long run than a merchant cash advance at 80% APR. The key word is "well-structured." Get a lawyer involved before you accept a single dollar from an outside investor.

The capital requirements for eateries are real and significant. Treat your funding strategy with the same seriousness you give your menu development and location selection. Those decisions are visible to customers. Your capital structure is invisible to them, but it determines whether they ever get to walk through your door.

— Capital

How Capitalforbusiness supports restaurant startup funding

Capitalforbusiness has worked with food service businesses across the country since 2009, providing small business loans tailored to the real capital requirements of restaurant startups. Whether you need equipment financing to outfit your kitchen, working capital to cover your first few months of operations, or a business line of credit to manage cash flow after opening, Capitalforbusiness offers funding solutions designed for operators at every stage.

When banks decline your application or move too slowly, Capitalforbusiness steps in with fast, affordable funding up to $500,000. Explore your restaurant loan options today and get the capital your concept deserves.

FAQ

What is the role of lending in restaurant startups?

Lending provides the capital restaurant startups need to cover buildout, equipment, inventory, marketing, and working capital before revenue is stable. Without adequate financing, most restaurants cannot sustain operations long enough to reach profitability.

How much capital does a restaurant startup typically need?

A typical restaurant startup requires $175,000 to $500,000, with a median budget around $375,500 covering all pre-opening and early operating costs. The exact amount depends on location, concept type, and lease terms.

What credit score do I need for a restaurant startup loan?

SBA 7(a) loans prefer a credit score of 680 or above, while conventional bank loans typically require 720 or higher. Equipment financing is available to operators with scores as low as 620 in many cases.

Are merchant cash advances a good option for financing restaurant startups?

No. Merchant cash advances require existing revenue to qualify and carry effective APRs that can exceed 100%, making them unsuitable for startup capital. They are better suited for established restaurants managing short-term cash flow gaps.

How can a first-time operator improve their chances of loan approval?

First-time operators should document any relevant experience, contribute 10–30% owner equity, prepare a detailed business plan with realistic financial projections, and consider partnering with a co-applicant who has an established industry track record.