Finding a small business loan with fast approval and flexible requirements can be a challenge when cash flow is tight. Many providers offer rigid credit checks, geographic limits, or high upfront costs that disqualify applicants before exploring terms. This comparison highlights product features, approval timelines, and eligibility details so you can pick a lender that fits your funding window and business profile.

Table of Contents

- Capital for Business

- OnDeck

- Credibly

- SMB Funding

- Bluevine Business Checking and Lending Platform

- Fundbox

- Comparison of alternatives

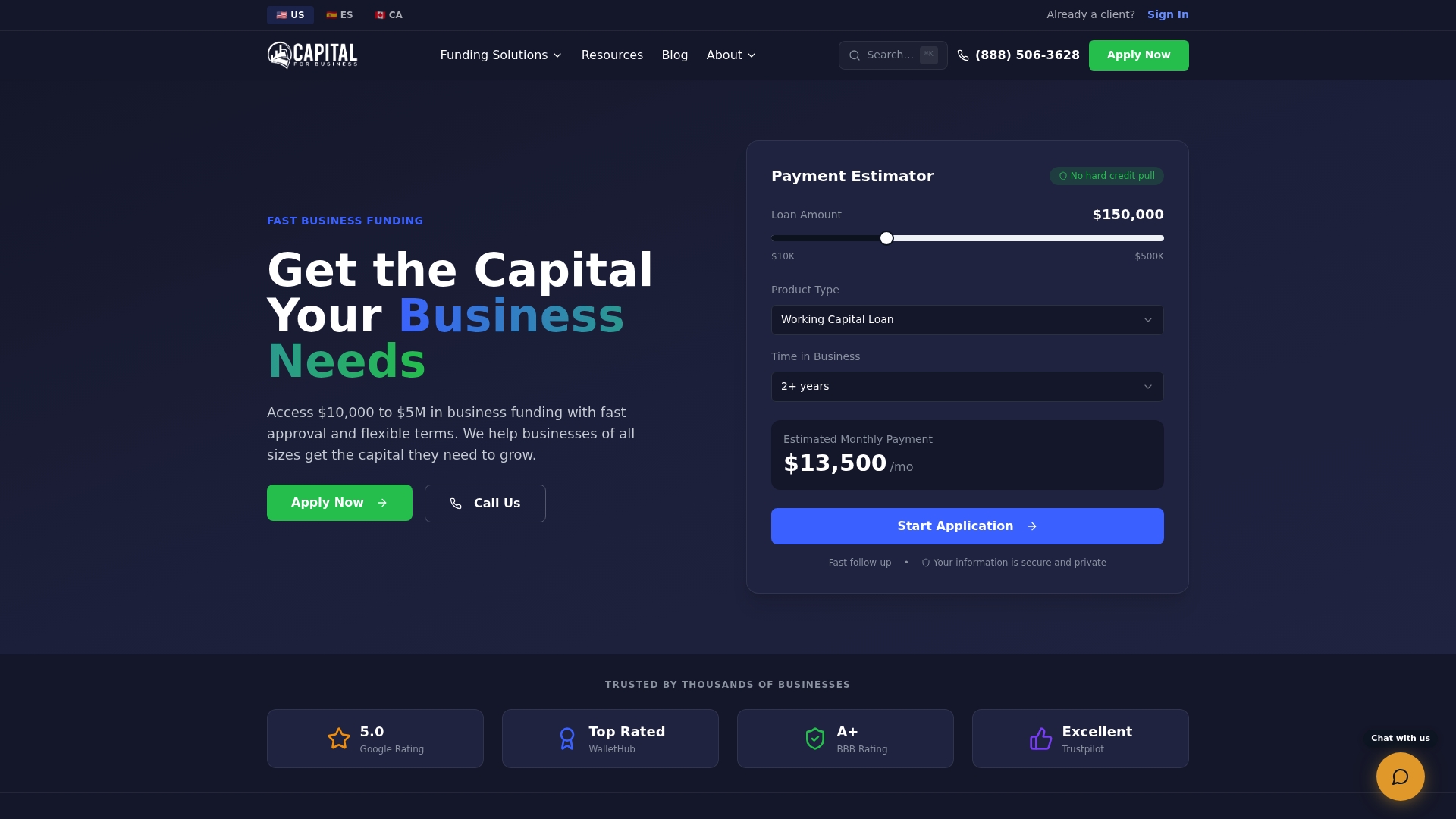

Capital for Business

At a Glance

According to the company, funding can be available in as little as 24 hours for qualifying applicants. The platform combines AI-driven application assistance with human funding specialists to speed approvals. Capital for Business focuses on fast working capital and equipment financing for small businesses across the United States.

Core Features

-

Offers a breadth of financing options including working capital loans, business lines of credit, equipment financing, term loans, SBA loans, and revenue-based financing. Each product maps to common operational needs like payroll, inventory, or capex.

-

The vendor reports serving over 50,000 clients since 2016 and states it is certified to operate in all 50 US states. That client figure and nationwide coverage show the company aims for broad availability.

-

AI-assisted applications reduce manual paperwork and route requests to dedicated funding specialists who customize repayment schedules to match seasonal cash flow.

-

Flexible repayment terms and options for collateral or personal guarantees when required by risk profiles.

Key Differentiator

What separates Capital for Business from many bank options is the combination of AI-assisted intake and a fast operational pipeline that the company says can deliver funding within a single business day. That pairing targets owners who need capital quickly rather than waiting weeks for traditional lenders.

Pros

-

Fast approval and funding. The platform emphasizes a quick approval process and the possibility of same day funding for eligible borrowers.

-

Accepts applicants with imperfect credit. The underwriting approach includes alternative credit signals, which expands access beyond strict bank criteria.

-

Wide product mix. You can pick from working capital, equipment financing, SBA-style options, or revenue-based plans to match the use case.

-

Nationwide service with local expertise. The company states it operates across all 50 US states, which helps businesses in different regulatory environments.

-

Transparent pricing and visible customer reviews. The company highlights public ratings and review sites, which helps you check real customer experiences.

Cons

- Specific eligibility rules for each loan product may exclude applicants with extremely low credit or irregular revenue profiles.

Who It's For

Capitalforbusiness and Capital for Business target small to medium-sized businesses in the United States and Canada that need quick access to working capital or funding for equipment. This platform fits owners who prefer faster decisions and are willing to accept alternative underwriting or pledge collateral when required.

Unique Value Proposition

AI-powered application assistance paired with a live funding specialist accelerates the approval path and reduces time spent on forms. That combination shortens the administrative burden for you and often moves approvals out of a queue and into an active underwriting conversation. For seasonal retailers or contractors with tight cash windows, this lowers the friction between applying and receiving funds.

Real World Use Case

A retail store in Chicago used a working capital loan to restock ahead of a busy season without draining reserves. The store completed an AI-guided application, spoke with a funding specialist, and received funds fast enough to buy inventory and meet demand.

Pricing

Pricing varies by loan product, term length, credit profile, and collateral requirements. Rates and fees depend on the product you choose. Contact a funding specialist for a personalized quote and a breakdown of repayment terms.

Website: https://capitalforbusiness.net

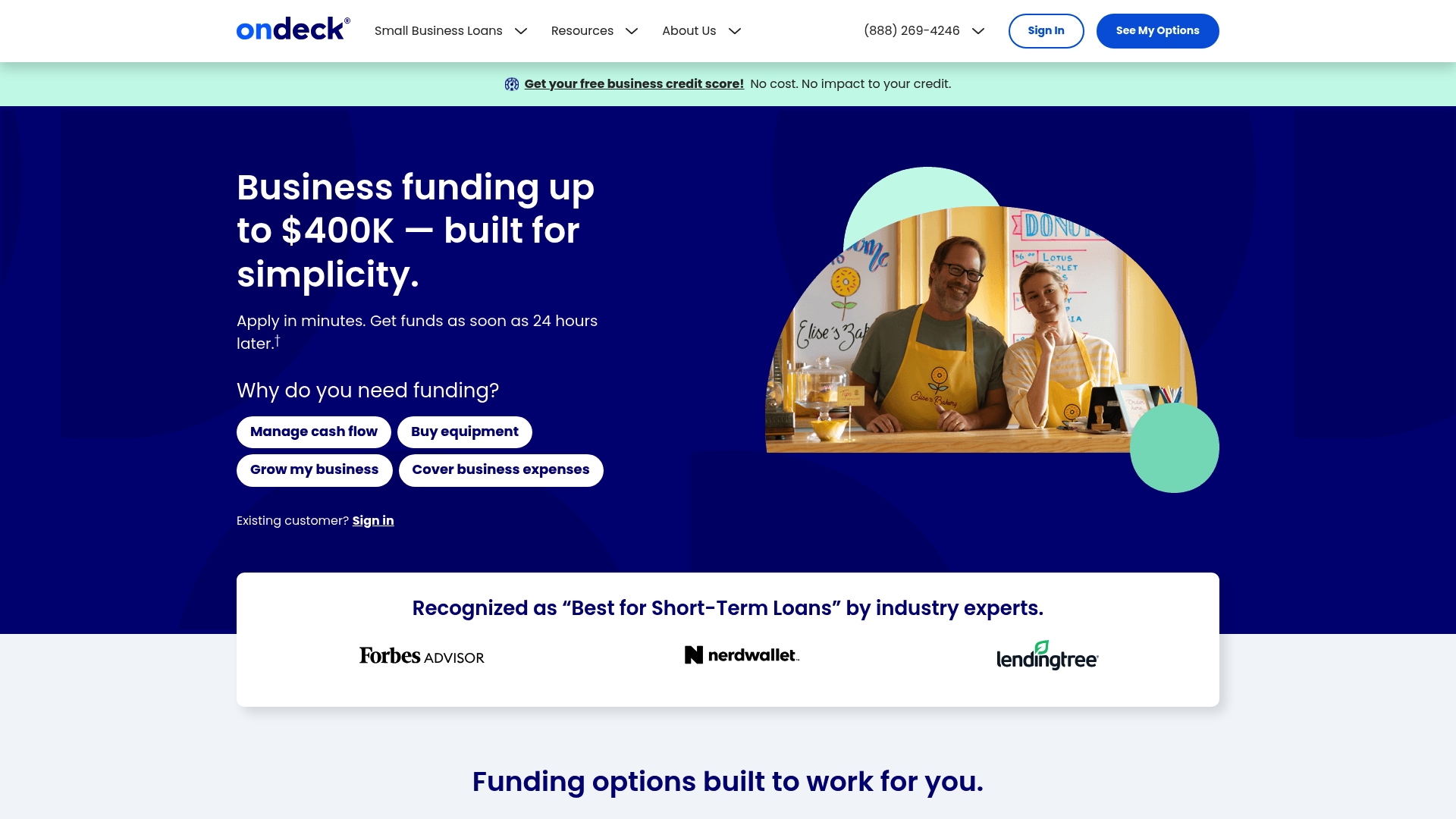

OnDeck

At a Glance

OnDeck reports it has funded over 185,000 businesses and says it delivered more than $25 billion since 2006. The vendor advertises funding in as little as 24 hours in some cases. That scale and speed aim to serve owners who need fast working capital rather than long term, low cost loans.

Core Features

OnDeck offers a quick application that takes minutes to complete and eligibility checks that do not use a hard credit pull. The platform supports revolving lines of credit and lump sum term loans with flexible repayment choices. Approved borrowers can access funding the same day after approval when submitted Monday through Friday before 10:30 a.m. ET. Repayment terms include 12, 18, or 24 months for lines of credit and up to 24 months for term loans.

Key Differentiator

The product's standout feature is its speed and prequalification approach. OnDeck runs eligibility checks without a hard inquiry, which lets prospective borrowers check options without affecting their credit. That design targets businesses that prioritize quick access to capital and simple application flows.

Pros

- Fast application and funding process. The form takes minutes and approval can lead to same day funding under the stated cutoff.

- No impact on a credit score when checking preliminary eligibility. This reduces risk for applicants shopping rates.

- High funding limits up to $400K. That capacity helps small firms pursue larger equipment or expansion moves.

- Recognized firm with an A+ BBB rating and dedicated in house loan advisors for personalized help. Advisors guide documentation and repayment setup.

Cons

- The vendor reports average APRs over 56%. That figure makes these loans costly for long term borrowing.

- Eligibility requires specific creditworthiness and revenue thresholds. Businesses below those thresholds will not qualify.

- Some industries and geographic areas are excluded, and North Dakota is explicitly ineligible according to the data. This limits availability for certain owners.

- Requires a minimum credit score and revenue. Applicants with thin or new business histories may struggle to meet those rules.

When It May Not Fit

Owners seeking low cost, long term financing should look elsewhere because the rates are high by the vendor's report. Businesses with marginal credit or low revenue will likely fail initial eligibility checks. Firms in restricted industries or in North Dakota cannot use this option. For companies needing multi year amortization at low interest, this product is a poor match.

Who It's For

Small business owners who need rapid working capital and can meet credit and revenue minimums will find this useful. It fits firms that value quick funding for payroll, inventory, or short term equipment needs. Owners who prioritize low rates over speed should consider alternatives.

Real World Use Case

A retailer facing a seasonal inventory spike applies for a line of credit and receives funds the same day. That turnaround reflects the funding timeline the vendor advertises and lets the owner buy stock before peak sales. The in house advisors help set draw schedules and repayment expectations.

Pricing

OnDeck does not publish a single pricing table for all applicants. Loan pricing is quoted per application and depends on business credit and revenue. Refer back to the APR figure above for a sense of likely cost when comparing offers.

Website: https://ondeck.com

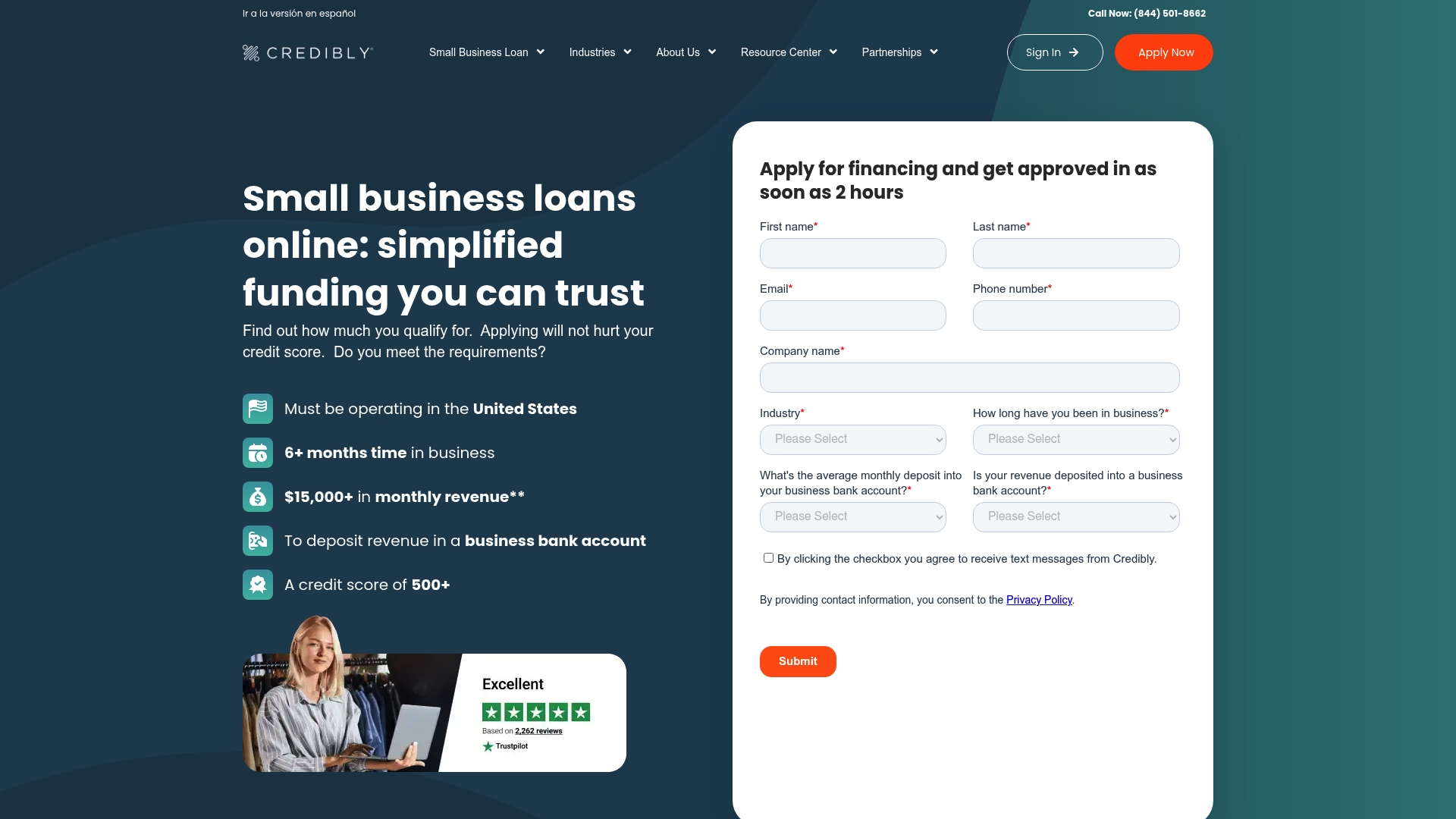

Credibly

At a Glance

Credibly's marketing materials state applications can be approved in as little as 2 hours, with funds available in roughly 4 hours. The platform targets small and medium sized businesses with a mix of working capital, lines of credit, equipment loans, and merchant cash advances. Customer reviews emphasize a straightforward online application and responsive loan officers.

Core Features

Credibly supports a broad set of loan programs including working capital, merchant cash advances, lines of credit, equipment loans, long term loans, and SBA loan assistance. The online application offers quick pre qualification and dedicated loan officer support. The company uses data science to evaluate business health beyond credit scores, which helps match applicants to appropriate products. Products also include options for seasonal revenue and imperfect credit.

Key Differentiator

The platform stands out for its emphasis on data science during underwriting. That approach factors in cash flow and other operational signals rather than relying solely on credit scores. For owners with uneven revenue or a shorter credit history, that wider view can speed approval and improve access to funding compared with lenders that use strict credit cutoffs.

Pros

-

Fast approvals and funding. The vendor claims approvals in hours and same day funding in some cases, which helps when cash flow gaps are urgent.

-

Multiple product types for different needs. You can pursue short term working capital, longer term loans, or equipment financing from the same application.

-

Flexible for lower credit profiles. The underwriting model considers business metrics beyond credit, making some borrowers eligible who would fail strict credit checks.

-

Online application with loan officer support. The platform lets you pre qualify quickly then work with a person to finalize terms.

-

Positive customer feedback on transparency and responsiveness. Reviews frequently mention clear communications during the process.

Cons

-

Startup eligibility limits. The company generally requires six months in operation and a minimum revenue level, which excludes many brand new businesses.

-

Some products use external funding partners. That arrangement can mean different terms or less direct control over certain loans.

-

Variable costs by profile. Interest and factor rates vary with creditworthiness, so pricing can be higher for riskier applicants.

-

Multiple product rules increase complexity. New users may find the range of loan types and criteria confusing without guidance.

When It May Not Fit

If your business is under six months old or does not deposit revenue into a business bank account, Credibly is likely not a fit. If you need the absolute lowest market rate, large banks or SBA programs might offer better pricing for well established companies. Also expect some loan types to depend on partner availability in your state.

Who It's For

Small and medium sized business owners in the United States who need quick access to capital and who may have imperfect credit. It suits retail, restaurant, and service operators with seasonal revenue who want an online application plus human support.

Real World Use Case

A small retail store facing an inventory shortage can apply online, qualify using sales and deposit history, and work with a loan officer to secure a working capital advance. According to the vendor, approval and funding can happen in hours, letting the owner buy inventory before peak season.

Pricing

Pricing varies by loan type and borrower profile. The company cites factor rates as low as 1.11, but specific rates and fees are disclosed during individual consultations and depend on your credit and revenue picture.

Website: https://credibly.com

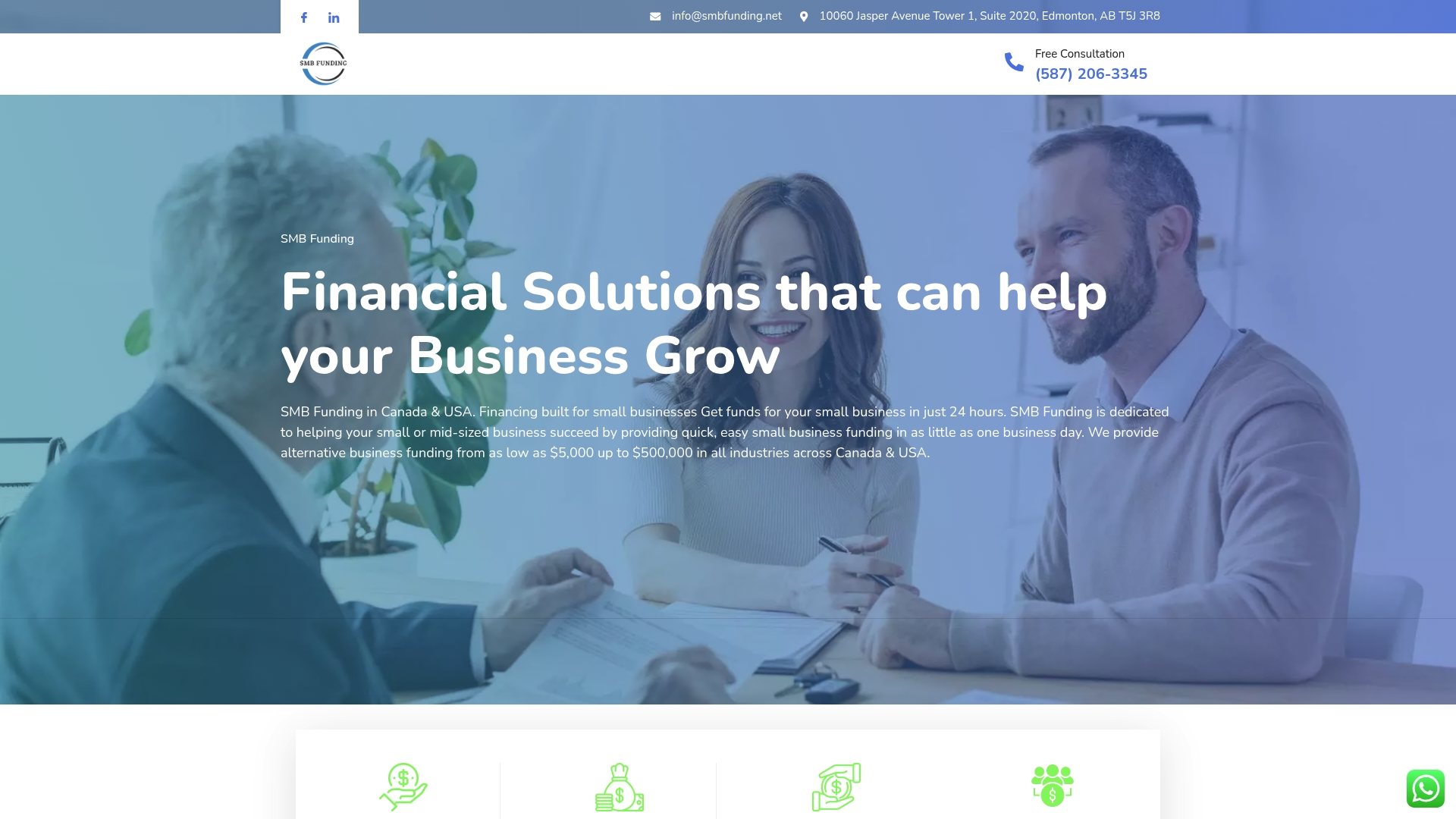

SMB Funding

At a Glance

SMB Funding reports it can provide funds within 24 hours for approved applications. The vendor pairs an online application with a proprietary risk evaluation system that looks at business potential over credit scores. Funding ranges from $5,000 to $500,000, and eligibility requires roughly six months in business and modest monthly revenue.

Core Features

The product centers on fast access to working capital through several funding types and a simplified online workflow. The application process is primarily web based and aims to cut paperwork for owners who need cash quickly. The underwriting uses nontraditional signals to evaluate higher risk businesses.

- Online streamlined application process that reduces form overload and speeds decisions.

- Merchant cash advances and small business loans for short term needs.

- Lines of credit for rolling working capital and repeat use.

- Funding tiers from $5,000 to $500,000, with minimal collateral requirements.

Key Differentiator

SMB Funding emphasizes rapid approvals by prioritizing business cash flow and sales potential. That underwriting approach differs from lenders that rely mainly on credit scores. The vendor positions its proprietary risk evaluation system to approve more applicants in high risk sectors.

Pros

-

Quick approvals. The application and funding flow aims to move capital into accounts fast for time sensitive needs.

-

Flexible product mix. Owners can choose merchant cash advances, loans, or lines of credit based on short term needs.

-

No collateral required for most products. This lowers the barrier for owners with few assets.

-

Focus on business potential. That underwriting method helps applicants with lower credit scores or seasonal sales patterns.

-

Broad industry support. The service accepts high risk sectors that many traditional lenders decline.

Cons

-

High cost for some options. Merchant cash advances use factor rates that can be expensive compared with term loans.

-

Frequent repayment schedules. Daily or weekly deductions from sales can strain tight cash flow.

-

Not designed for long term capital projects. The product mix favors short term working capital over major investments.

-

Minimum eligibility rules. Businesses need roughly six months of operation and modest monthly revenue to qualify.

When It May Not Fit

This solution is not a good match for owners seeking low cost, long term financing for major equipment or real estate. Businesses that cannot tolerate daily or weekly repayments should avoid merchant cash advances. Firms that have strong credit and access to bank financing will likely find cheaper options elsewhere.

Who It's For

Small and mid sized business owners in Canada and the USA who need quick working capital will find this useful. It suits owners with limited collateral or lower credit scores and businesses in higher risk categories. Use it when short term cash flow or an immediate inventory purchase is the priority.

Real World Use Case

A retail shop needs rapid capital to restock before peak season. SMB Funding provides approval based on projected sales and deposits funds within a day for qualified applicants. Repayment ties to daily card sales, which matches the store's revenue pattern.

Pricing

Pricing is not published on the site and varies by product type and risk profile. Merchant cash advances generally carry higher effective costs than term loans. Interested owners should request a quote to compare factor rates, repayment frequency, and any origination fees.

Website: https://smbfunding.net

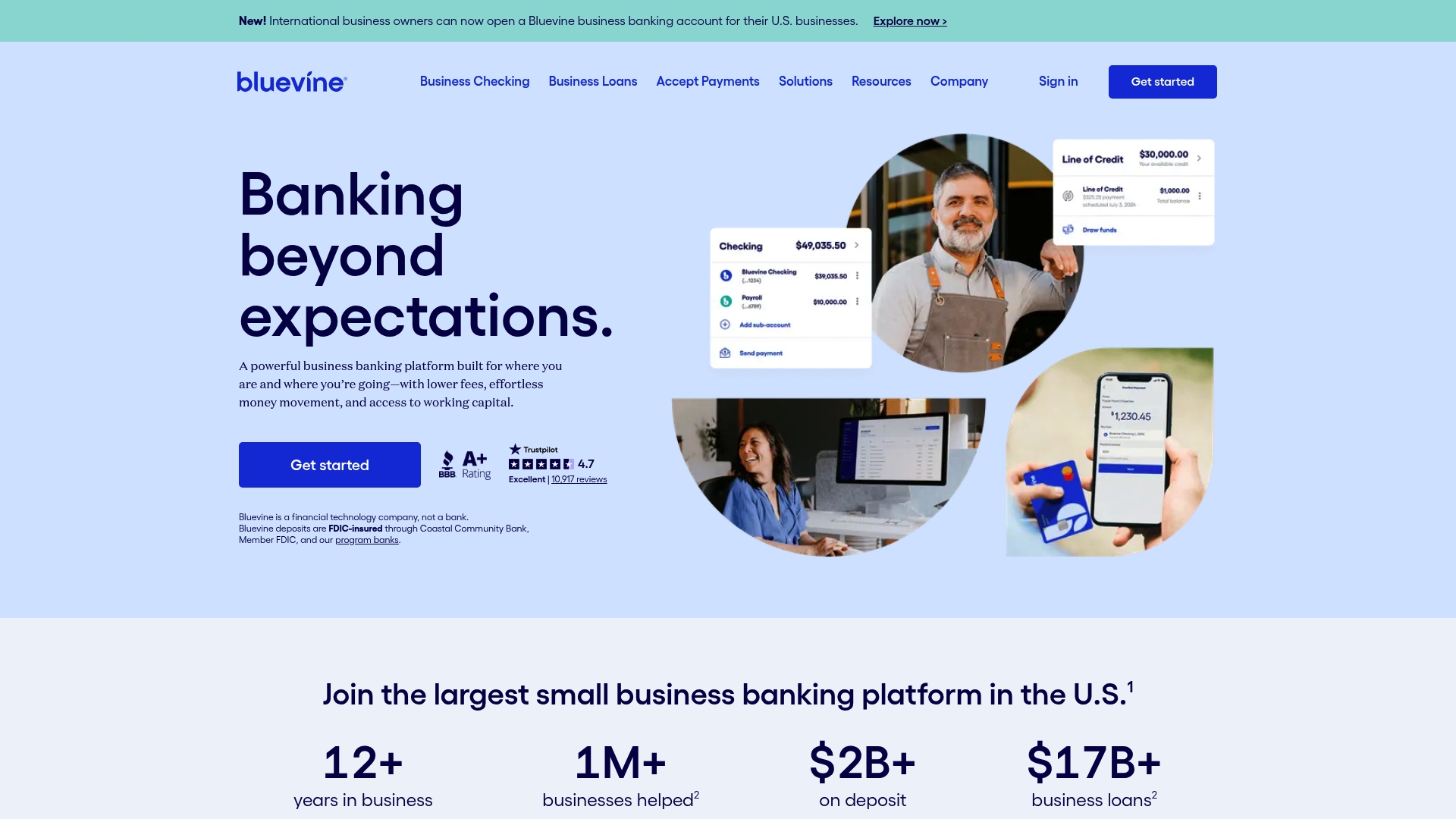

Bluevine Business Checking and Lending Platform

At a Glance

Bluevine offers FDIC insurance up to $3 million by sweeping deposits across multiple partner banks. The sweep model spreads funds into several insured banks for larger coverage than the usual $250,000 limit. It also bundles checking, lending, and payment tools so you can manage core cash flows from one dashboard.

Core Features

-

No monthly or overdraft fees. Standard accounts avoid monthly maintenance charges and typical overdraft penalties.

-

High APY on checking accounts. Upgraded plans deliver higher interest on balances compared with many small business accounts.

-

Accounts payable automation and support for multiple subaccounts to separate budgets and projects.

-

International payments with transfers that can arrive as fast as 24 hours and features for non U.S. residents with some restrictions.

-

Multiple payment acceptance methods including invoicing, payment links, Tap to Pay, ACH, wires, checks, and card processing via Stripe.

-

Security measures such as two factor authentication, data encryption, and real time alerts.

Key Differentiator

The standout feature is the sweep network that provides FDIC coverage up to $3 million. That structure targets business owners who hold larger cash balances and want bank level deposit protection without managing multiple bank relationships. This focus narrows Bluevine toward businesses that prioritize deposit insurance while still wanting loans and payments in a single platform.

Pros

-

Offers broad deposit protection through the sweep network. That appeals to businesses with sizable operating cash.

-

No monthly or overdraft fees lowers ongoing account cost for small firms and freelancers.

-

Combines checking, credit products, and payments so you can handle invoicing and funding decisions without separate vendors.

-

Strong security stack with two factor authentication and data encryption gives practical protection for online banking.

-

Industry recognition and positive customer feedback position the product as a credible fintech choice for small business banking.

Cons

-

Banking services come from partner banks rather than Bluevine acting as a traditional bank. Some customers prefer a direct bank charter.

-

Limited physical branch presence since the offering is primarily digital.

-

International features vary by country and may include higher fees for certain transfers.

-

Application approval depends on creditworthiness which can limit access to lending for some businesses.

When It May Not Fit

If your operation needs in person branch services then this digital first model will feel limiting. Businesses that require full international banking capabilities in specific countries may encounter restrictions or higher fees. Firms that prefer a single bank relationship rather than a sweep network should look elsewhere.

Who It's For

Small and medium sized business owners, startups, and accountants who need a combined checking and lending platform with enhanced deposit protection. It fits companies that hold larger cash balances and want to reduce account complexity while keeping payment acceptance and credit options close at hand.

Real World Use Case

A retail owner automates invoicing, keeps separate subaccounts for inventory and payroll, and pulls a line of credit when stock spikes. The owner moves customer receipts into higher yielding checking and keeps large cash protected by the sweep network. Payments arrive quickly and card processing works through the same account.

Website: https://bluevine.com

Fundbox

At a Glance

Fundbox reports it has helped over 500,000 businesses unlock more than $6 billion in capital. That figure signals a platform focused on frequent, smaller lending events for small businesses and merchants. The offering centers on embedded credit and fast approval flows inside accounting and commerce tools.

Core Features

-

Fast application process that the vendor advertises as taking under 3 minutes. This reduces paperwork and gets decisions into a busy owner’s workflow.

-

Quick access to funds that the vendor advertises as often arriving within 2 business days. That timing suits short cash flow gaps and inventory purchases.

-

Flexible repayment terms with no early repayment fees. Borrowers can repay early without facing prepayment penalties.

-

Embedded integrations with platforms like Stripe, FreshBooks, Zoho, and Intuit. These connections let you request credit inside systems you already use.

-

Reporting to business credit bureaus such as Experian, Dun & Bradstreet, and Equifax to help build business credit profiles.

Key Differentiator

Fundbox’s primary angle is its embedded model that places credit inside familiar business tools. The vendor pairs that placement with machine learning driven underwriting to speed decisions. That combination reduces context switching and fits platform partners that want built in funding rather than a separate lender relationship.

Pros

-

Ease of use and automation praised by customers. The application and funding flow minimize administrative time for owners.

-

High trust signals on public review sites, with strong user ratings reported by the vendor. That reflects consistent customer satisfaction in many cases.

-

Flexible repayment options and no early repayment fees. This helps owners who can repay quickly without penalty.

-

Integration with widely used business tools supports workflows. Connecting to accounting and payments systems cuts manual steps.

-

The vendor reports over $6 billion in capital unlocked, which indicates a high level of transaction experience. That scale suggests repeatable operations for small credit events.

Cons

-

Limited eligibility requires at least 3 months of bank transactions, a business checking account, and minimum revenue and age thresholds. New or very small businesses may not qualify.

-

Availability varies by state and industry. The product is not offered in all jurisdictions and excludes prohibited business types.

-

Some users find costs comparable to other nonbank options. Fees are transparent, but they can still be meaningful for tight margins.

When It May Not Fit

Fundbox is a poor fit if you need credit amounts above the platform cap of $250,000. It also does not serve prohibited business categories or certain states where legal restrictions apply. Finally, startups with under three months of transaction history will likely fail the eligibility checks.

Notable Integrations

- Stripe

- Joist

- FreshBooks

- Autobooks

- Synchrony

- Intuit

- Nav

- Zoho

Who It's For

Small business owners and platform partners that want quick, embedded access to working capital inside accounting, invoicing, or payments software. It fits merchants who can document banking history and who prefer requesting credit inside familiar tools rather than handling a separate loan application.

Real World Use Case

A small retailer requests credit inside their accounting platform to buy inventory before a busy season. Funds arrive fast enough to close supplier orders, and sales during the season provide repayments over flexible terms. The integration keeps the funding step inside the retailer’s normal workflow.

Pricing

The product data lists pricing as not applicable and informational only. Fundbox presents fees and repayment options at application rather than publishing a single public rate. Prospective borrowers must view terms during the application to see their exact cost.

Website: https://fundbox.com

Comparison of alternatives

When businesses need to secure financing, selecting the right platform depends on matching their specific needs with the available services. While some prioritize rapid funding, others look for specialized features like embedded tools or low-cost options. Here we compare notable alternatives including Capital for Business, OnDeck, Credibly, SMB Funding, Bluevine, and Fundbox, focusing on how each provider addresses distinct needs.

Speed and accessibility of funding

Capital for Business and OnDeck both excel in quick funding access, often providing funds within one business day of approval. However, while Capital for Business ensures coverage across all 50 U.S. states, OnDeck's services are not available in certain regions, limiting its accessibility for some users.

Customization and range of financial products

Credibly and SMB Funding offer diverse product ranges catering to various business needs, such as seasonal financing options and underwriting focusing on business potential. Contrastingly, Bluevine provides integrated financial services, blending lending with business checking accounts, making it a versatile platform for combined banking and financing needs.

Best fit

- Capital for Business: Businesses seeking rapid funding with local expertise across all U.S. territories.

- OnDeck: Businesses prioritizing flexible term lending with minimal impact on credit during eligibility checks.

- Credibly: Small enterprises requiring personalized repayment structures based on nontraditional underwriting criteria.

- Fundbox: Businesses that benefit from embedded credit services within their operational tools.

Our pick

Capital for Business is an choice for establishments needing fast, nationwide funding with an emphasis on tailored financing solutions. While other platforms shine in unique areas, Capital for Business's streamlined AI-supported application process and the involvement of dedicated funding specialists ensure dependable and efficient services. For small businesses with unique or specific funding needs outside these scenarios, alternatives like Bluevine and Credibly may offer better synergies.

When evaluating options for quick small business funding, the following comparison highlights key aspects to consider:

| Provider | Key Differentiator | Best For | Pricing | Limitation |

|---|---|---|---|---|

| Capitalforbusiness | AI-assisted application and 24-hour funding | Small to medium-sized businesses | Not disclosed | Specific eligibility criteria for certain products |

| OnDeck | Prequalification without credit inquiry; funding up to $400K | Owners prioritizing speed and guidance | Average APR ~56% | Geographical and credit restrictions apply |

| Credibly | Data science underwriting; same-day funding | Businesses with uneven revenue streams | Factor rates 1.11 | Limited if under six months of operation |

| SMB Funding | Proprietary cash flow evaluation; quick approvals | Lower-credit business owners | Not disclosed | High costs for merchant cash advances |

| Bluevine Business Checking and Lending Platform | High FDIC insurance with fully digital management | Firms managing larger cash balances | Not disclosed | Does not serve all geographies |

| Fundbox | Embedded credit in accounting tools; flexible repayment terms | Merchants using integrated tools | Transparent fees | Limited to businesses over 3 months old |

Find Reliable Alternatives with Capitalforbusiness for Your Small Business Financing Needs

Choosing the right lender can feel challenging, especially when fast access to working capital or equipment financing is a priority. This article highlights the search for headwaycapital.com alternatives, focusing on lenders that offer quick approvals, flexible terms, and support for businesses with varied credit profiles. Capitalforbusiness meets these needs by serving small businesses and startups across the United States and Canada, offering tailored loans, merchant cash advances, and business lines of credit when traditional banks fall short.

Explore how Capitalforbusiness can deliver fast, affordable funding with personalized service and a broad product range. Visit Capitalforbusiness to get a customized quote and speak with a funding specialist who understands your seasonal cash flow and project requirements. Act now to secure the capital you need to keep your business growing smoothly.

FAQ

What types of business loans does Capitalforbusiness offer?

Capitalforbusiness offers a variety of financing options, including working capital loans, business lines of credit, equipment financing, term loans, and SBA loans. These products are tailored to meet common operational needs like payroll, inventory, or capital expenditures.

How does OnDeck compare with Capitalforbusiness for fast funding?

OnDeck is known for its rapid application process and the possibility of same-day funding, which makes it an appealing choice for urgent cash needs. However, Capitalforbusiness distinguishes itself by combining AI-assisted applications with dedicated funding specialists, which can lead to approvals in as little as 24 hours, catering to those who prefer personalized service alongside speed.

Can applicants with low credit scores find options with Capitalforbusiness?

Yes, Capitalforbusiness accepts applicants with imperfect credit due to its approach of considering alternative credit signals beyond traditional metrics. This makes it a viable option for small business owners who might be turned away by stricter criteria from other lenders.

What is the typical funding timeline with Capitalforbusiness?

Capitalforbusiness claims that funding can be available in as little as 24 hours for qualifying applicants. This quick turnaround can be especially beneficial for seasonal retailers or contractors with tight cash windows needing immediate access to funds.

What should business owners expect regarding pricing from Capitalforbusiness?

Pricing with Capitalforbusiness varies by loan product, term length, and credit profile, meaning each quote will be tailored to the applicant's specific situation and needs. Potential borrowers should reach out to a funding specialist for a personalized quote and repayment terms.