TL;DR:

- Construction cash flow is often misaligned with standard financial ratios, requiring project-level cash tracking.

- Managing retainage actively and negotiating early releases can significantly improve working capital.

- Building reserves and securing flexible funding options are essential for contractors to sustain growth and handle cash gaps.

Cash flow gaps are one of the most persistent threats to a contractor's ability to grow. You may win a great project, complete quality work, and still find yourself short on funds to start the next job. According to construction payment statistics, 90% of construction leaders have passed on profitable work because of cash timing issues, and 56% turned down projects outright. Working capital is not just a financial ratio buried in a spreadsheet. It is the operational fuel that keeps your crew on the job, your suppliers paid on time, and your business positioned to say yes when the right opportunity arrives. This guide walks you through the practical steps to understand, measure, and improve working capital so your construction business can grow with confidence.

Table of Contents

- Understanding working capital in construction

- Empirical benchmarks and industry standards

- Managing retainage and cash traps

- Tactics to optimize cash flow and unlock capital

- Why conventional working capital advice falls short for contractors

- Connect with funding solutions: Maximize your working capital

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Cash flow drives success | Contractors must prioritize available cash—not just ratios—to unlock project growth. |

| Retainage impacts capital | Aggressive management of retainage can free up 5–10% of revenue and reduce financing costs. |

| Benchmarks guide decisions | Measuring working capital using industry ratios and revenue percentages helps spot risks early. |

| Optimize daily processes | Practical tactics and technology streamline cash flow, reduce delays, and enable expansion. |

| Funding solutions available | Tailored loans and funding strategies support sustained contractor growth and stability. |

Understanding working capital in construction

Working capital sounds straightforward in finance textbooks. The standard formula is simple: subtract your current liabilities from your current assets, and what remains is your working capital. A positive number means you have more short-term resources than short-term obligations. A negative number signals trouble.

For contractors, though, this formula tells only part of the story. According to a construction working capital guide, working capital is calculated as current assets minus current liabilities, but contractors should focus on available cash rather than textbook ratios due to timing mismatches in construction cash flows. That distinction matters enormously in practice.

Why the standard definition falls short

In most industries, a business collects revenue shortly after delivering a product or service. Construction does not work that way. Payment cycles in construction are notoriously long and irregular. You pay subcontractors and suppliers often before you receive payment from the general contractor or project owner. Retainage withholds a portion of every invoice, sometimes for months or years. Lien waivers, draw schedules, and change order disputes can all delay cash coming in while your cash going out remains constant.

This means your balance sheet might show a technically healthy working capital ratio at the end of the quarter while your bank account tells a very different story on any given Tuesday in the middle of a project. The ratio reflects what you own versus what you owe at one moment in time. It does not reflect when cash actually moves.

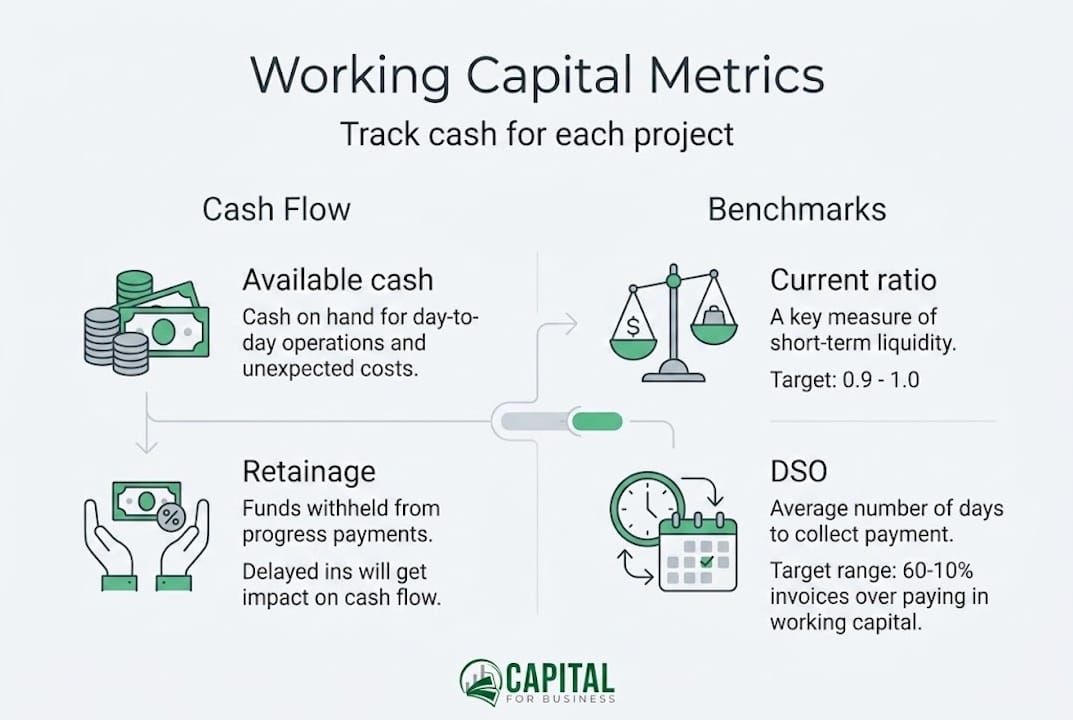

The more useful measure for day-to-day decisions is available cash by project. You need to know, at any point, how much real cash you can deploy without putting another project at risk. That requires project-level visibility, not just company-wide totals.

Key components of construction working capital

Understanding what goes into your working capital helps you manage it more precisely. Here is a breakdown of the most relevant items for contractors:

Current assets that count toward working capital:

- Cash and bank balances

- Accounts receivable (amounts billed but not yet collected)

- Costs in excess of billings (work completed but not yet invoiced)

- Prepaid expenses and deposits

Current liabilities that reduce working capital:

- Accounts payable (amounts owed to subcontractors and suppliers)

- Billings in excess of costs (amounts collected but not yet earned)

- Short-term loan payments

- Accrued wages and payroll taxes

The table below illustrates how two contractors with the same working capital ratio can have very different cash positions:

| Metric | Contractor A | Contractor B |

|---|---|---|

| Current assets | $800,000 | $800,000 |

| Current liabilities | $600,000 | $600,000 |

| Working capital | $200,000 | $200,000 |

| Cash on hand | $180,000 | $30,000 |

| Receivables (aged 90+ days) | $20,000 | $170,000 |

Both companies have the same working capital on paper. Contractor A has $180,000 in usable cash. Contractor B has $30,000. The ratio hides the risk entirely.

Pro Tip: Track available cash separately for each active project. Use a simple spreadsheet or construction management software to record projected inflows and outflows by job. This gives you a real picture of where your money is and when you will need more.

Many contractors find that exploring funding solutions for construction early, before a cash crunch develops, is far more effective than scrambling for capital mid-project. Understanding how business loans for cash flow work can also help you build a safety net before you need it. Using cash basis accounting methods alongside accrual reporting can also sharpen your real-time view of available cash.

Empirical benchmarks and industry standards

Once you understand how working capital operates in construction, the next step is gauging your financial health using benchmarks. Knowing what healthy looks like in your industry helps you set realistic targets and spot warning signs before they become real problems.

Current ratio standards

The current ratio divides your current assets by your current liabilities. According to rising working capital data from the National Association of Surety Bond Producers, empirical benchmarks for contractors include a current ratio of 1.25 to 1.5 considered solid, while 1.5 to 2.0 is considered healthy. Days Sales Outstanding typically falls between 45 and 75 days, with industry averages ranging from 56 to 83 days. Working capital as a percentage of annual revenue generally sits between 15% and 25% for well-capitalized contractors, and the data shows a rising trend in working capital levels among small and mid-size general contractors.

These benchmarks matter for more than internal planning. Surety companies, banks, and bonding agents use them to evaluate your financial strength before approving bonds or lines of credit. If your numbers fall below these thresholds, you may face higher premiums, reduced bonding capacity, or outright denial of financing.

DSO: Days Sales Outstanding

DSO measures how many days on average it takes you to collect payment after invoicing. A lower DSO means faster collections and better cash flow. A higher DSO means more cash is tied up waiting on clients or general contractors to pay.

Here is how DSO ranges stack up in practical terms:

| DSO Range | Cash Flow Condition | Typical Impact |

|---|---|---|

| Under 45 days | Strong | Low borrowing need, high flexibility |

| 45 to 60 days | Adequate | Manageable with discipline |

| 60 to 75 days | Tight | May need short-term funding solutions |

| Over 75 days | Stressed | Significant risk of cash gaps |

If your DSO is consistently above 75 days, you are likely turning down work or delaying vendor payments as a direct result. Improving collections by even 10 to 15 days can free up tens of thousands of dollars depending on your revenue volume.

Working capital as a percentage of revenue

Another useful benchmark is working capital as a percentage of annual revenue. Smaller contractors, those generating under $5 million per year, may need working capital at the higher end of the 15% to 25% range because they have less ability to absorb project delays. Larger contractors with diversified project portfolios may operate closer to the lower end.

Key takeaways for benchmarking your position:

- A current ratio below 1.25 is a warning signal that deserves immediate attention

- DSO trending upward over consecutive quarters indicates a collection problem

- Working capital below 15% of revenue limits your ability to take on new projects safely

- Surety companies typically require working capital evidence as part of bond applications

Working capital loans can help bridge gaps when your benchmarks reveal a shortfall. For contractors preparing to scale, reviewing your construction business loan options is a practical starting point. You can also use project growth loans to build reserves before taking on larger contracts.

Managing retainage and cash traps

Having benchmarked your working capital, shift focus to one of the biggest cash traps: retainage and how to overcome it.

![]()

Retainage is the practice of withholding a percentage of your contract value, typically 5% to 10%, until the project reaches substantial completion or a defined milestone. On a $5 million project, that means $250,000 to $500,000 of earned revenue is sitting in someone else's account while you are paying your crew and suppliers every week.

According to construction payment statistics, retainage ties up 5% to 10% of revenue on any given project. If you finance that shortfall through a line of credit or loan, the carrying cost can reach 6% to 9% annually. On a $500,000 retainage balance held for 12 months, that financing cost alone could reach $45,000.

"Retainage is often accepted as a standard cost of doing business, but few contractors calculate what it actually costs them to carry it. On a $5 million project, 10% retainage means $500,000 tied up. At a 9% carrying cost, that is $45,000 per year effectively paid for the privilege of completing the work."

How to track and negotiate retainage effectively

Managing retainage requires both discipline and strategy. The following steps give contractors a practical framework:

-

Build a retainage schedule at contract signing. Before any work begins, document the exact retainage percentage, release conditions, and expected release dates. Add this to your project financial tracker.

-

Track retainage by project, not just in aggregate. Knowing total retainage owed across all projects is useful, but knowing which projects are closest to release and which have disputes helps you prioritize collection efforts.

-

Request retainage reduction at the 50% completion milestone. Many contracts allow the owner to reduce retainage from 10% to 5% when the project is half done. Request this proactively. Not every owner will agree, but many will, especially if your work quality has been strong.

-

Explore retainage bonds as an alternative. A retainage bond allows the owner to release the retainage funds while still having a bond in place to protect against incomplete work. The bond typically costs 1% to 3% of the retainage amount, according to construction retainage management resources. Compared to a 6% to 9% carrying cost, this is often a clear financial win.

-

Forecast release dates conservatively. When modeling your cash flow, assume retainage will arrive 30 to 60 days later than contractually required. Projects run long, punch lists stretch out, and owners often delay. Planning for this prevents surprise shortfalls.

-

Include retainage reduction clauses in your standard contract templates. If you are a general contractor or project manager, make automatic retainage reduction a default clause in contracts you draft. This shifts the baseline negotiation in your favor.

Pro Tip: Create a simple retainage tracker with five columns: project name, retainage amount, expected release date, conservative release date, and financing cost per month. Update it weekly. Seeing the financing cost accumulate in real time creates urgency to resolve delays faster.

Learning to manage retainage more aggressively is one of the fastest ways to improve your working capital without taking on more debt. Coupling this with sound cash flow forecasting practices helps you plan around release dates accurately. If you need bridge capital while retainage is outstanding, reviewing business loans for contractors and funding tips for growth can point you toward the right options.

Tactics to optimize cash flow and unlock capital

After tackling retainage, let's focus on everyday cash flow tactics that make a tangible difference.

The core challenge most contractors face is a timing mismatch. Revenue comes in irregularly while expenses go out on a fixed schedule. Payroll does not wait for the general contractor to process your draw request. Material vendors expect payment within 30 days regardless of when your client pays you. Closing that gap requires proactive systems, not reactive scrambling.

Consider that construction payment statistics show 90% of industry leaders have passed on profitable work due to cash timing issues, and 56% turned down projects entirely. These are not struggling businesses making bad decisions. These are experienced contractors who ran out of financial runway because cash flow was not actively managed.

Practical steps to improve cash flow daily

-

Invoice immediately upon milestone completion. Every day you delay sending an invoice is a day added to your DSO. Build invoicing into your project schedule as a non-negotiable task.

-

Offer early payment incentives where possible. A 1% to 2% discount for payment within 10 days can be cheaper than carrying a line of credit for 30 to 60 days.

-

Negotiate front-loaded draw schedules. When drafting contracts, push for larger initial payments and smaller back-end payments. More money early means more available cash throughout the project.

-

Sequence vendor payments strategically. Prioritize suppliers and subcontractors who hold lien rights and whose work is on the critical path. Delaying a non-critical subcontractor by 10 days is far less risky than delaying a concrete supplier.

-

Establish a cash reserve fund equal to one month of fixed overhead. Even $20,000 to $50,000 set aside specifically for operational continuity can prevent the need to pass on a project or take on expensive emergency financing.

-

Use project-level cash flow forecasts updated weekly. Look 60 to 90 days ahead on each active project. Identify where gaps will occur before they arrive.

Ways to reduce DSO and avoid funding gaps

- Send invoices with clearly stated payment terms and due dates

- Follow up on unpaid invoices at 15, 30, and 45 days without waiting for 60 or 90

- Use digital payment platforms to reduce check clearing delays

- Include lien notice requirements in your payment workflow as a leverage tool

- Separate billing and project management roles so invoicing does not get deprioritized

Pro Tip: Use accounting software or a business cash flow management system that connects your receivables and payables in real time. Seeing outstanding invoices and upcoming obligations on a single dashboard eliminates the guesswork that leads to missed payments and cash surprises.

When gaps do appear despite your best efforts, having a funding plan in place matters. Explore small business loans for working capital to understand what options exist before you need them. Understanding how loans work for contractors helps you choose the right product at the right time without overpaying for capital you could have structured better with more lead time.

Why conventional working capital advice falls short for contractors

Most financial advice on working capital focuses on ratios: maintain a current ratio above 1.5, keep DSO below 60 days, hold 15% of revenue in liquid reserves. That advice is not wrong. It is just incomplete for contractors.

Here is the uncomfortable truth. A contractor can hit every benchmark on paper and still miss payroll. The textbook ratios measure position, not flow. They tell you where you stand today, not what happens when a $200,000 draw gets delayed by 45 days because the project owner is waiting on their own financing to clear. That kind of delay does not show up on your balance sheet until it is already a problem.

As noted in the construction working capital guide, contractors must focus on available cash rather than textbook ratios because of the timing mismatches inherent in construction cash flows. That is not a nuance. It is the central insight that separates contractors who scale successfully from those who stall despite winning good work.

The practical lesson is this: build your cash management system around project-level cash flow projections, not quarterly ratio reviews. Update your forecasts weekly. Model conservative scenarios where payments arrive 30 days late and retainage stretches two months beyond contract terms. If your business survives those scenarios on paper, you have real financial resilience. If it does not, you know exactly where to focus.

Generic financial advice also tends to overlook the risk adaptation required in construction. Seasonal slowdowns, weather delays, labor shortages, and supply chain issues can all compress your cash position with little warning. Contractors who build working capital reserves specifically as a buffer against those variables, not just to meet surety benchmarks, are the ones who can actually absorb disruption and keep growing. Exploring practical funding solutions is part of that preparation, not a fallback when things go wrong.

Connect with funding solutions: Maximize your working capital

Managing working capital effectively requires the right strategies and, sometimes, the right financial partner. At Capital for Business, we have spent over 15 years working with contractors and construction business owners who face the exact challenges covered in this guide: slow pay cycles, retainage lockup, and the pressure to fund new projects before old ones settle.

We offer flexible working capital loans designed specifically for businesses that need fast access to funds without the delays of traditional bank lending. Our team understands construction timelines and cash flow patterns. Whether you need to bridge a retainage gap, cover payroll during a slow draw cycle, or build reserves before taking on a larger contract, our business funding solutions can be structured to fit your situation. Learn more about supporting working capital through our small business loan programs and take the next step toward financial stability and growth.

Frequently asked questions

How is working capital calculated for contractors?

Working capital is current assets minus current liabilities, but contractors should prioritize tracking available cash by project because construction's irregular payment cycles make standard ratios misleading in day-to-day operations.

What retainage strategies can boost cash flow for contractors?

Track retainage by project with scheduled release dates, request reductions at 50% project completion, consider retainage bonds to release cash at a lower cost, and always forecast release dates conservatively to avoid surprise shortfalls.

What are healthy working capital benchmarks for contractors?

A current ratio between 1.25 and 2.0 is considered healthy, and working capital should represent 15% to 25% of annual revenue to support project activity and bonding capacity.

How does poor working capital management affect contractors?

Contractors with weak working capital frequently turn down profitable projects because cash timing does not align with project start requirements, limiting growth despite strong demand for their services.

What role can business loans play in working capital optimization?

Business loans provide flexible, fast funding to bridge cash flow gaps between project draws, retainage releases, and payroll cycles, allowing contractors to maintain operations and accept new work without interruption.