TL;DR:

- Small businesses often have longer cash conversion cycles than large firms, affecting cash flow.

- Managing working capital strategically involves understanding its components, cycles, and industry benchmarks.

- Active strategies like faster invoicing and negotiating better payment terms can optimize cash flow and support growth.

Managing cash flow is one of the most pressing challenges small business owners face, yet many focus on bank balances rather than the real driver of financial health: working capital. You might have strong sales and still struggle to pay suppliers, cover payroll, or seize a growth opportunity. That disconnect is more common than you think. In fact, small US companies with revenues under $300 million carried a median Cash Conversion Cycle of 120 days in 2024, nearly double that of large firms at 65 days. That gap means small businesses wait far longer to turn their operations into usable cash, creating hidden pressure that no bank balance alone can reveal. This guide breaks down what working capital is, why it matters, and how you can use it to make smarter decisions every day.

Table of Contents

- What is working capital? Key terms every business owner needs to know

- How working capital impacts cash flow and business operations

- Positive vs. negative working capital: What it really means for small business survival

- Optimizing working capital for growth: Tools, tips, and real-world strategies

- The surprising truth about working capital most business guides miss

- Get the support your small business needs to master working capital

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Working capital basics | Working capital means the difference between what your business owns and owes right now. |

| Cash flow impact | A long cash conversion cycle can strain your business and limit growth. |

| Positive vs. negative | Both positive and negative working capital can be good or bad depending on your industry and cash flow model. |

| Actionable improvement | Regularly monitor, assess, and optimize your working capital to support strong, steady growth. |

What is working capital? Key terms every business owner needs to know

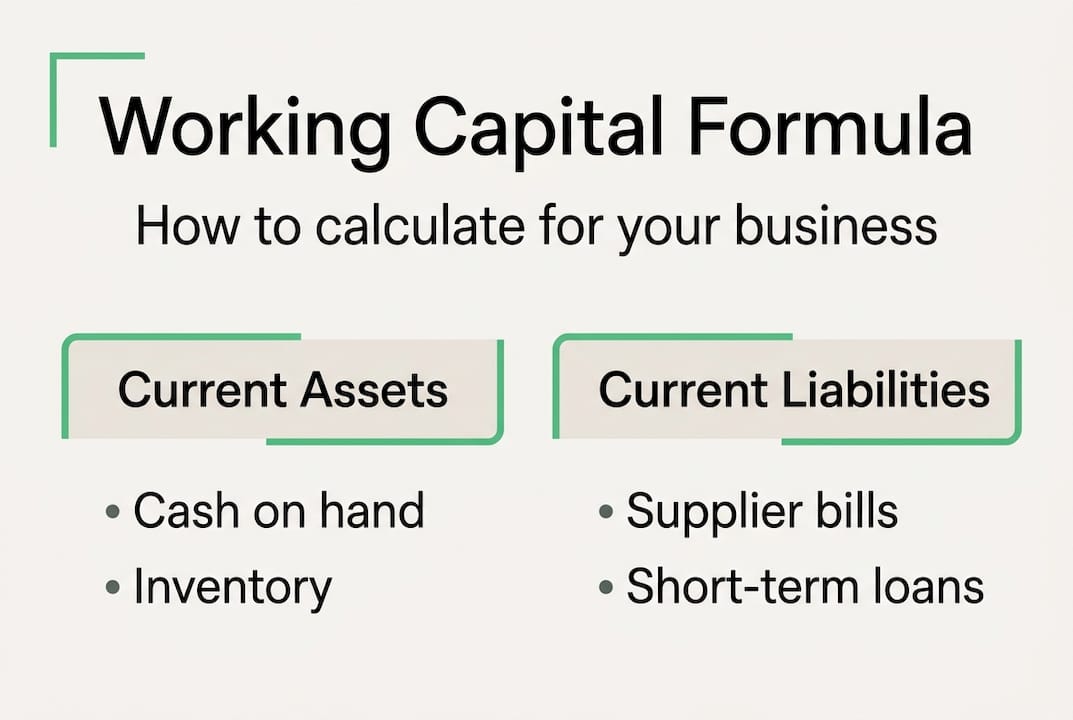

Working capital is not just the cash sitting in your checking account. It is the difference between what your business owns in the short term and what it owes in the short term. Understanding why working capital matters starts with knowing exactly what goes into that calculation.

The formula is straightforward:

Working Capital = Current Assets minus Current Liabilities

Current assets are things your business expects to convert into cash within the next 12 months. Current liabilities are obligations your business must pay within the same window.

| Current assets | Current liabilities |

|---|---|

| Cash and cash equivalents | Accounts payable (bills owed to suppliers) |

| Accounts receivable (invoices owed to you) | Short-term loans or credit lines due |

| Inventory | Accrued wages and payroll taxes |

| Prepaid expenses | Current portion of long-term debt |

When current assets exceed current liabilities, you have positive working capital. That generally signals your business can cover its short-term obligations. When liabilities exceed assets, you have negative working capital.

Here is where many owners get tripped up:

- Positive working capital does not automatically mean your business is thriving. You could have a large accounts receivable balance that customers are slow to pay, leaving you technically "positive" but cash-starved.

- Negative working capital is not always a crisis. Fast-turnover retailers, like supermarkets, often collect cash from customers before they pay their suppliers, creating a deliberate and efficient negative position.

- Holding too much working capital can actually slow growth by tying up funds that could be reinvested.

Pro Tip: Before you label your working capital position "good" or "bad," ask how quickly your assets actually convert to cash. A $200,000 receivable that takes 90 days to collect is very different from $200,000 in cash.

Good managing working capital practice means reviewing these numbers monthly, not just at tax time. The formula is simple, but the story behind the numbers requires attention.

How working capital impacts cash flow and business operations

With the building blocks established, let's connect working capital to what owners care about most: daily cash flow and making payroll.

The best tool for this connection is the Cash Conversion Cycle (CCC). The CCC measures how long it takes your business to turn its investments in inventory and other resources into actual cash from sales. The shorter the cycle, the faster cash flows back into your business.

Here is a simple example. Imagine you run a small manufacturing company. You purchase raw materials on Day 1. You hold that inventory for 30 days before it becomes a finished product. You sell the product on Day 30 and issue an invoice. Your customer pays 60 days later. Your CCC is 90 days. That means you waited 90 days to recover the cash you spent on Day 1.

Now consider how working capital and cash flow interact when that cycle stretches:

- Slow inventory turnover ties up cash in goods sitting on shelves.

- Late invoice collection delays cash coming in while bills keep arriving.

- Short supplier payment terms force you to pay out before cash arrives.

- Rapid growth can actually worsen cash flow if sales outpace your ability to collect.

- Seasonal demand creates peaks and valleys that strain even well-managed businesses.

"For US small companies with revenues under $300 million, the median CCC was 120 days in 2024, compared to 100 days for medium firms and just 65 days for large firms. The US overall median CCC stood at approximately 89 days."

This data is striking. Small businesses are operating with cash cycles that are nearly twice as long as large corporations. That means a small business owner waits twice as long to recover invested cash, all while facing the same monthly rent, payroll, and supplier bills.

| Company size | Median CCC (2024) |

|---|---|

| Small (under $300M revenue) | 120 days |

| Medium | 100 days |

| Large | 65 days |

| US overall | ~89 days |

Improving working capital management strategies means actively working to shorten this cycle wherever possible. Even cutting your CCC by 15 to 20 days can free up meaningful cash without borrowing a single dollar.

Positive vs. negative working capital: What it really means for small business survival

Understanding these cycles sets up a bigger question: is positive or negative working capital actually better for your business model?

The honest answer is that it depends entirely on how your business generates and uses cash. Here is a clearer breakdown.

When positive working capital signals strength:

- Your business has a buffer to handle unexpected expenses.

- You can negotiate better terms with suppliers because you pay reliably.

- Lenders and investors view you as lower risk.

- You have room to invest in growth without immediately needing outside funding.

When negative working capital is a strategic choice:

- Subscription-based businesses collect payment upfront before delivering services.

- Large retailers receive goods on credit and sell them for cash before supplier invoices are due.

- Fast-food franchises and similar models operate efficiently with negative positions because cash comes in daily.

When negative working capital is a danger signal for small businesses:

- Your inventory moves slowly and invoices take weeks or months to collect.

- You rely on short-term debt to cover routine operating expenses.

- Suppliers are tightening your payment terms because of late payments.

- You cannot meet payroll without drawing on a credit line every cycle.

The key insight from negative working capital analysis is that context determines meaning. A negative number is only efficient when your Days Inventory Outstanding (DIO) and Days Sales Outstanding (DSO) are low, and your Days Payable Outstanding (DPO) is high. In plain terms: you sell fast, collect fast, and pay suppliers slowly.

Pro Tip: Calculate your CCC before drawing conclusions from your working capital number. If your CCC is long and your working capital is negative, that is a real warning sign. If your CCC is short and your negative position is driven by favorable supplier terms, you may be running an efficient operation.

There is also a risk on the other side. Holding excessive positive working capital means cash is sitting idle instead of being invested in equipment, marketing, or staff. Explore funding options for working capital and working capital funding to understand how to deploy capital strategically rather than just accumulate it.

Optimizing working capital for growth: Tools, tips, and real-world strategies

It is one thing to know your numbers. It is another to actually improve them. Let's get practical.

Start by calculating your working capital and CCC every month. You do not need a finance degree to do this. A basic spreadsheet, a simple accounting app like QuickBooks or Wave, or a quarterly check-in with your accountant can keep you informed. Consistency matters more than complexity.

Tactics to shorten your cash conversion cycle:

- Send invoices immediately after delivery, not at the end of the month.

- Offer small early-payment discounts (1 to 2 percent) to encourage faster collections.

- Review inventory regularly and reduce slow-moving stock.

- Negotiate longer payment terms with suppliers, even 15 extra days helps.

- Use inventory management software to avoid over-ordering.

- Set up automated payment reminders for outstanding invoices.

When internal improvements are not enough, external working capital solutions become valuable. 85% of mid-market US firms with revenues between $50 million and $1 billion use external working capital solutions, and Canadian firms in this category often generate higher returns from them. Even smaller businesses benefit from the same tools at the right stage of growth.

Simple action plan for assessing your working capital:

- Pull your most recent balance sheet and identify all current assets and current liabilities.

- Calculate your working capital using the formula above.

- Calculate your CCC by adding your DIO and DSO, then subtracting your DPO.

- Compare your CCC to your industry average to see where you stand.

- Identify the single biggest drag on your cycle (slow collections, excess inventory, or short supplier terms) and address it first.

- Revisit the numbers monthly and track your progress.

If you are working on repaying business loans on time, improving your working capital position directly supports that goal by keeping cash available. Similarly, a stronger working capital position can help you qualify for better rates, which is relevant if you are focused on reducing loan interest. And if cash flow has already become a crisis, knowing your working capital numbers is the first step in surviving finance crises.

For US and Canadian small business owners alike, the goal is not to chase a perfect number. It is to understand your cycle, spot problems early, and use the right tools to keep operations running smoothly.

The surprising truth about working capital most business guides miss

Most articles about working capital tell you to maximize it. Keep it positive, keep it growing, and you will be safe. That advice is well-intentioned but incomplete, and for many small businesses, it can actually work against you.

Here is what years of working with small business owners across hundreds of industries has taught us: the businesses that thrive are not the ones with the highest working capital. They are the ones who understand their own cash flow model well enough to use working capital strategically.

A retail business that deliberately runs negative working capital because it collects cash before paying suppliers is not in trouble. It is operating efficiently. Conversely, a service business with strong positive working capital but a 90-day collection cycle may be sitting on a ticking clock. The number looks fine until a few big clients pay late at the same time.

As research confirms, positive working capital shows stability but excess ties up cash, while negative can actually boost return on equity in efficient models. The problem is that most small business owners never get to this level of nuance. They either panic at a negative number or feel falsely secure with a positive one.

The real skill is managing working capital wisely in a way that fits your specific business model. Stop comparing your working capital ratio to a generic benchmark. Instead, compare your CCC to your own historical performance and to direct competitors in your industry. That comparison tells you far more about whether you are improving or drifting toward trouble.

The businesses that grow consistently treat working capital as a dynamic tool, not a static score to maintain.

Get the support your small business needs to master working capital

Understanding working capital is a genuine advantage. It helps you spot cash flow problems before they become emergencies, make smarter decisions about growth, and communicate more confidently with lenders and advisors.

At Capital for Business, we have helped small business owners across the US and Canada access the funding they need to keep operations running and seize growth opportunities since 2009. Whether you need working capital loans to bridge a cash flow gap, want to explore options for supporting working capital through a small business loan, or are just starting to research your small business loan options, we are ready to help. Our team works quickly, efficiently, and at terms that make sense for your business. Reach out today and take the next step toward stronger cash flow.

Frequently asked questions

What is the working capital formula?

Working capital is calculated as current assets minus current liabilities. Current assets include cash, receivables, and inventory, while current liabilities include accounts payable and short-term debt.

Why is working capital important for small businesses?

It measures whether a business can pay its short-term bills, manage daily cash flow, and avoid dangerous cash shortages. Negative working capital can signal financial distress in small businesses that lack fast inventory turnover.

What does negative working capital mean?

Negative working capital means your current liabilities exceed your current assets. It can signal either financial distress or efficiency depending on whether your business collects cash quickly and pays suppliers slowly.

How can small businesses improve working capital?

Speeding up invoice collection, negotiating longer supplier payment terms, and reducing excess inventory are effective starting points. 85% of mid-market firms also use external working capital solutions to support growth and smooth out cash flow gaps.