TL;DR:

- A structured financing workflow involves equipment selection, document prep, lender submission, approval, funding, and repayment.

- Proper preparation and multiple lender applications speed approval and secure better terms for construction contractors.

- Choosing between loans and leases depends on equipment usage, finances, and tax strategies to maximize ROI.

Construction businesses lose bids and stall projects every year because their equipment financing process is unclear, slow, or disorganized. When a contractor needs a new excavator or fleet of work trucks, the difference between landing the job and losing it often comes down to how fast and efficiently they can secure funding. Cash flow constraints make this even harder for small firms. A well-structured financing workflow solves that. This guide walks you through every key step, from document preparation to final approval, while covering loan versus lease decisions, tax advantages, and practical tips to keep the process moving without costly delays.

Table of Contents

- Understanding the contractor equipment financing workflow

- What you need before applying: Preparation and prerequisites

- Step-by-step application and funding: How the process works

- Troubleshooting and optimization: Common mistakes, edge cases, and workflow upgrades

- Tax and financial benefits: Make your workflow work harder

- A fresh perspective on contractor equipment financing workflow

- Next steps: Find the right financing for your business

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Master the workflow | Understanding and preparing for each step speeds up equipment financing and avoids costly delays. |

| Prep documents early | Having all required documents ready before applying boosts approval chances and simplifies lender comparisons. |

| Match solution to needs | Consider loans for long-term use and equity; leases for flexibility, cash flow, and short-term projects. |

| Leverage tax advantages | Section 179 deductions and bonus depreciation can make financing far more profitable for your business. |

| Strategic optimization boosts ROI | Optimizing financing structures based on project cycles and utilization rates maximizes your return on investment. |

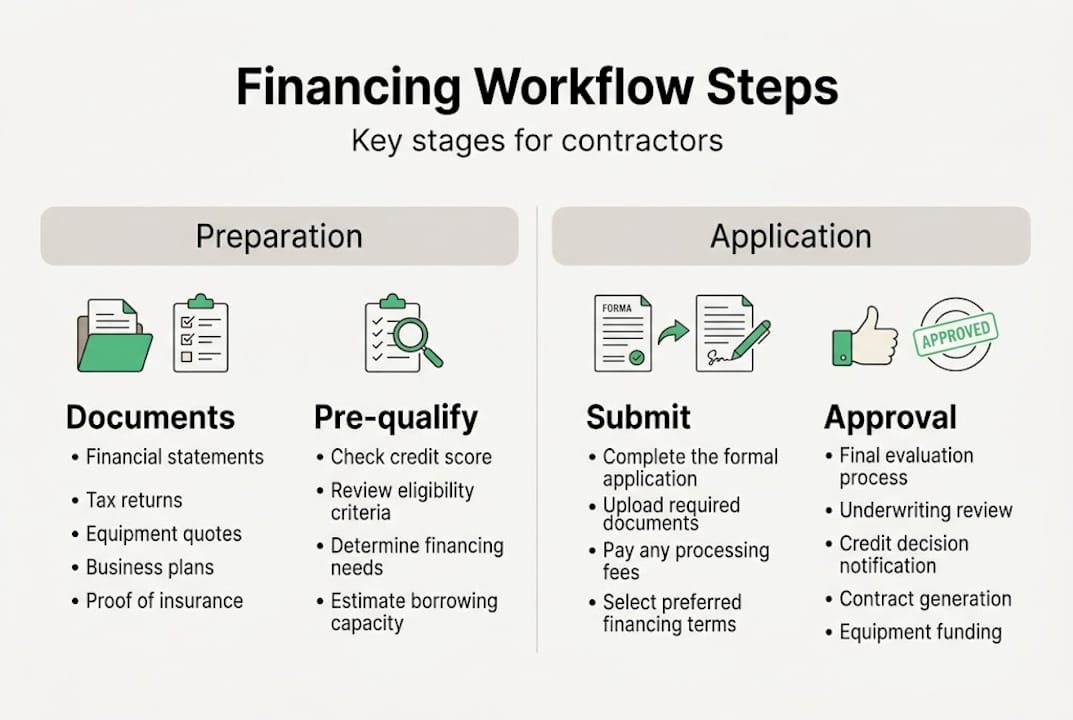

Understanding the contractor equipment financing workflow

Before you apply for a single dollar in equipment financing, it helps to see the full picture. The standard workflow for contractor equipment financing involves 4 to 6 clear stages: equipment selection, document preparation, lender submission, approval and terms review, funding, and repayment. Each stage builds on the last, and skipping steps or rushing through them is one of the most common causes of delays.

Here is how the typical process flows from start to finish:

- Equipment identification: Determine exactly what you need, its cost, and whether new or used fits your budget and project timeline.

- Document preparation: Gather all financial records, business formation documents, and equipment invoices before approaching any lender.

- Multi-lender submission: Submit applications to multiple lenders at the same time to compare rates, terms, and flexibility.

- Approval and terms review: Lenders assess your credit, revenue, and equipment value, then return an offer, often within 24 to 48 hours.

- Funding: Once you accept terms and sign the agreement, the lender sends payment directly to the vendor or seller.

- Repayment: Fixed monthly payments begin according to your loan or lease schedule.

This equipment financing tutorial provides a closer look at how each stage works in practice, especially for contractors new to the process.

Typical timeline expectations:

| Stage | Estimated time |

|---|---|

| Document preparation | 1 to 3 days |

| Application submission | Same day |

| Approval decision | 24 to 48 hours |

| Funding after approval | 1 to 3 business days |

| First repayment begins | 30 days post-funding |

Many contractors underestimate how much preparation time affects the entire timeline. Missing a single document, such as a tax return or equipment invoice, can push your approval back by several days. That kind of delay is costly when a project start date is locked in.

Common process pitfalls include submitting incomplete applications, approaching only one lender (which limits your negotiating power), and failing to match your financing term to actual equipment usage needs. If you are just getting started, this beginner's equipment financing guide covers the basics without the technical jargon.

Pro Tip: Use this equipment financing checklist to prepare all your documents before submitting a single application. Lenders move faster when your file is complete on the first submission.

Understanding the workflow sets a solid foundation, so let's examine the key steps in detail, starting with what you will need before you apply.

What you need before applying: Preparation and prerequisites

The fastest way to slow down your financing is to show up unprepared. Lenders evaluate your application based on specific financial documents, and any gap in that file creates friction. Before you contact a single lender, gather everything on this list:

- Business tax returns: Most lenders want the last 2 years of filed returns.

- Profit and loss statement: A current P&L shows your income versus expenses clearly.

- Bank statements: Typically the last 3 to 6 months of business account activity.

- Equipment invoice or quote: A direct seller invoice speeds up the lender's collateral evaluation.

- Business formation documents: Articles of incorporation, LLC operating agreement, or equivalent.

- Owner identification: A government-issued ID and often a personal credit pull.

The detailed prerequisites vary by lender and deal size, but this list covers the core requirements for most construction equipment applications in 2026.

Credit scores matter significantly. Your score affects both your approval odds and the interest rate you receive. Here is a practical breakdown:

| Credit score range | Likely rate range | Down payment range |

|---|---|---|

| 720 and above | 6% to 9% | 10% to 15% |

| 680 to 719 | 9% to 14% | 10% to 20% |

| 630 to 679 | 14% to 18% | 15% to 25% |

| Below 630 | 16% to 22%+ | 20% to 30% |

Startups and contractors with lower credit scores can still qualify, but they should prepare for higher rates and larger upfront down payments. Having a strong revenue history or co-signer can offset a weaker score in some cases.

Pre-quoting multiple lenders before committing is one of the most overlooked strategies in this process. Different lenders specialize in different deal sizes, equipment types, and credit profiles. A bank may decline your application while a specialty equipment lender approves it the same day. Applying broadly gives you options and leverage when reviewing offers.

For startups, the equation is different. Lenders will focus more on your business plan, personal credit, and any available collateral when traditional financial history is thin. Knowing this in advance lets you position your application more effectively.

Pro Tip: Organize digital copies of every document in a single shared folder before you apply. Request a direct seller invoice with the VIN or serial number included. Lenders move significantly faster when they can confirm collateral value without asking follow-up questions. Review the full equipment financing checklist to make sure nothing is missing.

Once you know what is expected, accurate preparation sets the stage for an efficient application. Next, let's follow the action: executing your financing application effectively.

Step-by-step application and funding: How the process works

With your documents ready, the application process moves quickly. Here is the practical sequence from submission to funded:

- Submit to 1 to 5 lenders simultaneously. Parallel applications save days. Use application process stats and an expert application tips source to benchmark what strong applicants include.

- Wait for approval decisions. Most lenders respond within 24 to 48 hours for standard deals.

- Review and compare offers. Look at interest rate, term length, early payoff penalties, and lender flexibility during slow seasons.

- Negotiate if possible. Competing offers give you real leverage to ask for better terms.

- Sign the agreement. Read every line, especially buyout clauses in leases and balloon payment terms in loans.

- Lender pays vendor directly. Funds rarely come to you first; the lender wires payment directly to the equipment seller.

- Take delivery and start repayments. Your monthly schedule begins 30 days after funding in most cases.

"The industry approval rate for equipment financing sits at 78%, with funding typically completed within 1 to 3 business days after signing."

One of the most important choices in this stage is whether to pursue a loan or a lease. Each has real trade-offs:

| Factor | Equipment loan | Equipment lease |

|---|---|---|

| Monthly payment | Higher | Lower |

| Ownership | Yes, after payoff | No (unless buyout clause) |

| Equity built | Yes | No |

| Flexibility | Lower | Higher |

| Best for | Long-term core assets | Short-term or upgrade-focused use |

| Tax treatment | Depreciation + interest deduction | Payments may be fully deductible |

Loans make the most sense for equipment you will use consistently for 5 or more years. Leases are better suited for projects where technology or usage requirements change frequently. The step-by-step financing tutorial covers both paths with real examples.

After the lender pays the vendor, delivery is arranged directly between you and the seller. Most contractors see their equipment on-site within a week of signing. Repayments are typically fixed, making cash flow planning straightforward.

With the process underway, the right steps and choices can get your equipment on the job fast. Next, let's cover real-world challenges: troubleshooting, edge cases, and maximizing your workflow.

Troubleshooting and optimization: Common mistakes, edge cases, and workflow upgrades

Even experienced contractors run into friction in the financing process. Knowing where things go wrong, and how to fix them, gives you a major advantage.

Common mistakes to avoid:

- Incomplete document submissions: A missing bank statement or outdated tax return can stall your application for days.

- Overestimating equipment needs: Buying more capacity than your projects require ties up capital and increases idle costs.

- Ignoring total cost of ownership (TCO): Monthly payment is only one number. Maintenance, insurance, fuel, and resale value all affect your true cost. The true cost breakdown is worth reviewing before any purchase.

- Neglecting seasonal cash flow: Many construction businesses have slower winter months. A fixed payment that works in summer can create stress in January.

Edge cases worth planning for:

- Bad credit or startup situations: Startups and those with credit scores above 600 can still qualify, though expect higher rates and a down payment of 20% to 30%. Explore your options through bad credit business loans if traditional equipment lenders decline your file.

- Used equipment financing: Lenders will typically require a condition inspection and may cap financing on equipment older than 10 to 15 years.

- High down payment requirements: If a lender asks for 25% or more upfront, evaluate whether your working capital can absorb that without hurting project operations.

Workflow optimization strategies:

The most effective contractors do not treat every piece of equipment the same way. They blend loan and lease strategies depending on equipment type and project duration. Core fleet assets like excavators or dump trucks are usually financed with loans to build equity. Specialty or short-term equipment is leased to maintain flexibility. The loan or lease choice guide walks through this decision with practical scenarios.

Some contractors are also using telematics data to track actual equipment utilization before committing to a purchase or financing term. This prevents the costly mistake of buying capacity you do not actually use.

According to industry utilization data, the average equipment utilization rate in construction is 65% to 70%. Avoid overbuying based on peak-season demand alone.

Pro Tip: Match your financing term length to the realistic lifecycle of each piece of equipment on your project schedule. A 7-year loan on equipment you will replace in 4 years creates unnecessary financial drag.

As you refine your workflow, the final key to ROI is maximizing the tax and financial advantages of your equipment financing choices.

Tax and financial benefits: Make your workflow work harder

Financing your equipment is not just a cash flow strategy. It is also a tax strategy, and most contractors leave money on the table by not planning this part carefully.

Key tax advantages of equipment financing in 2026:

- Section 179 deduction: The IRS allows businesses to deduct the full purchase price of qualifying financed equipment, up to $2.5M in deductions in a single tax year. This applies to both new and used equipment.

- 100% bonus depreciation: For assets placed in service in 2026, 100% bonus depreciation may apply depending on legislative updates. Confirm current rules with your CPA.

- Interest deduction: The interest portion of your loan payments is tax deductible, reducing your effective financing cost.

- Capital lease treatment: If your lease is structured as a capital lease, you may also capture depreciation benefits similar to ownership.

These advantages are generally stronger with loans than with operating leases, since ownership is required to claim depreciation. However, lease payment structures can also offer full deductibility as a business operating expense, depending on how the lease is classified.

Stat callout: 80% of U.S. businesses use some form of equipment financing, and delinquency rates remain low at approximately 2%, reflecting how manageable structured payments tend to be for businesses that plan ahead.

Construction is consistently ranked among the top five asset classes financed in the country, which means lenders are familiar with the industry's cash flow patterns and seasonal variables. That familiarity often translates to more flexible terms for experienced contractors.

Learn how to maximize your return by saving with Section 179 and structuring your purchase timing strategically before year-end.

Pro Tip: Always consult your CPA before finalizing any equipment financing deal. The tax impact of loan versus lease, timing of the purchase, and your current depreciation schedule can significantly affect how much you actually save.

Now that you understand both the process and benefits, let's look at how these insights reshape your entire approach to contractor equipment financing.

A fresh perspective on contractor equipment financing workflow

Most contractors focus on one number: the monthly payment. That instinct is understandable. Cash flow is real, and keeping payments manageable protects the business month to month. But limiting your analysis to that single figure is one of the most expensive habits in the industry.

The contractors who consistently win better projects and grow their fleets think differently. They analyze total cost of ownership, factoring in depreciation curves, real utilization rates, maintenance costs, and projected resale value. A piece of equipment with a lower payment but poor resale value and high maintenance can cost more over three years than a better-built machine financed at a slightly higher rate.

A dynamic workflow also adapts to business conditions. During a short-term boom in commercial work, leasing gives you capacity without long-term commitment. When core fleet assets are central to your business model, loans build equity and tax advantages over time. The smartest firms compare loan and lease strategies regularly and adjust their approach as the project mix shifts.

"Equipment financing is a growth accelerator when treated with strategic rigor, not just speed."

Strong preparation, multi-lender competition, and smart financial structuring give contractors a real edge. The firms that treat financing as a strategic tool consistently outperform those that treat it as a necessary inconvenience.

Pro Tip: Before approving any equipment purchase, ask: what is the lifecycle value of this asset relative to the financing cost? Think beyond affordability and toward ROI.

Next steps: Find the right financing for your business

You now have a clear map of the contractor equipment financing workflow, from preparation through funding and tax planning. The next step is putting that knowledge to work with the right financing partner.

Capital for Business has been helping construction businesses access equipment funding since 2009. We work with contractors who need fast approvals, flexible terms, and lenders who understand the seasonal realities of project-based work. Whether you need a straightforward loan, a lease structure, or working capital to bridge a cash gap, we have solutions designed for your industry. Explore easy small business loan options and compare available equipment financing offers to find the right fit. Visit our business funding solutions page to get started today.

Frequently asked questions

How long does contractor equipment financing take from application to funding?

Most contractors receive approval within 24 to 48 hours, and funds are typically disbursed within 1 to 3 business days after the agreement is signed.

What credit score is needed for equipment financing approval?

Scores of 630 and above are often workable, with the best rates going to applicants at 720 or higher. Startups and lower-credit applicants may still qualify, typically with higher rates between 16% and 22% and down payments of 20% to 30%.

Can I finance used construction equipment?

Yes, most lenders will finance used equipment up to 10 to 15 years old. A condition inspection on used equipment is typically required, and a larger down payment may apply depending on age and condition.

How does Section 179 impact equipment financing?

Financed equipment purchases may qualify for a Section 179 deduction up to $2.5M plus 100% bonus depreciation in qualifying years, which can significantly improve your after-tax return on the investment.

Is it better to lease or finance equipment for contractors?

Leasing offers lower monthly payments and greater flexibility, while loans build ownership and maximize tax benefits through depreciation. The right choice depends on how long you will use the equipment and your current financial goals.