TL;DR:

- Many small businesses believe flawless credit, experience, or bank connections are necessary for funding, but government programs aim to bridge the traditional lender gap. Understanding different financing types, lender evaluation criteria, and preparing a clear financial narrative increases approval chances. Proper preparation, systematic documentation, and a partner mindset are key to unlocking business funding opportunities.

Many small business owners in Canada and the U.S. believe that securing business funding requires flawless credit, years of operating history, or connections to the right bank manager. That belief keeps real opportunities on the table. Government risk-sharing programs, working capital financing, and equipment loans exist specifically to bridge the gap between what traditional lenders offer and what small businesses actually need. This article cuts through the confusion by explaining how the major financial service categories work, what lenders really look for, how to measure your financial health, and the practical steps you can take right now to position your business for approval.

Table of Contents

- Understanding business financial services: Core concepts and options

- How lenders evaluate your business: Risk, repayment, and documentation

- Working capital: What it is, how it's measured, and why it matters

- Accessing business financial services: Step-by-step application and practical tips

- Why most small businesses miss out on funding: Our take

- Unlock business funding with expert guidance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Loan programs share risk | Government-backed programs like CSBFP help small businesses but lenders still require repayment proof. |

| Documentation drives approval | Proper financial statements, business plans, and projections are essential for securing funding. |

| Working capital is critical | Understanding and managing your cash conversion cycle gives you an edge in both operations and loan applications. |

| Step-by-step approach helps | Following a clear application process and checklist increases your chance of approval. |

| Treat lenders as partners | A well-prepared narrative and transparency open doors to reliable financial services. |

Understanding business financial services: Core concepts and options

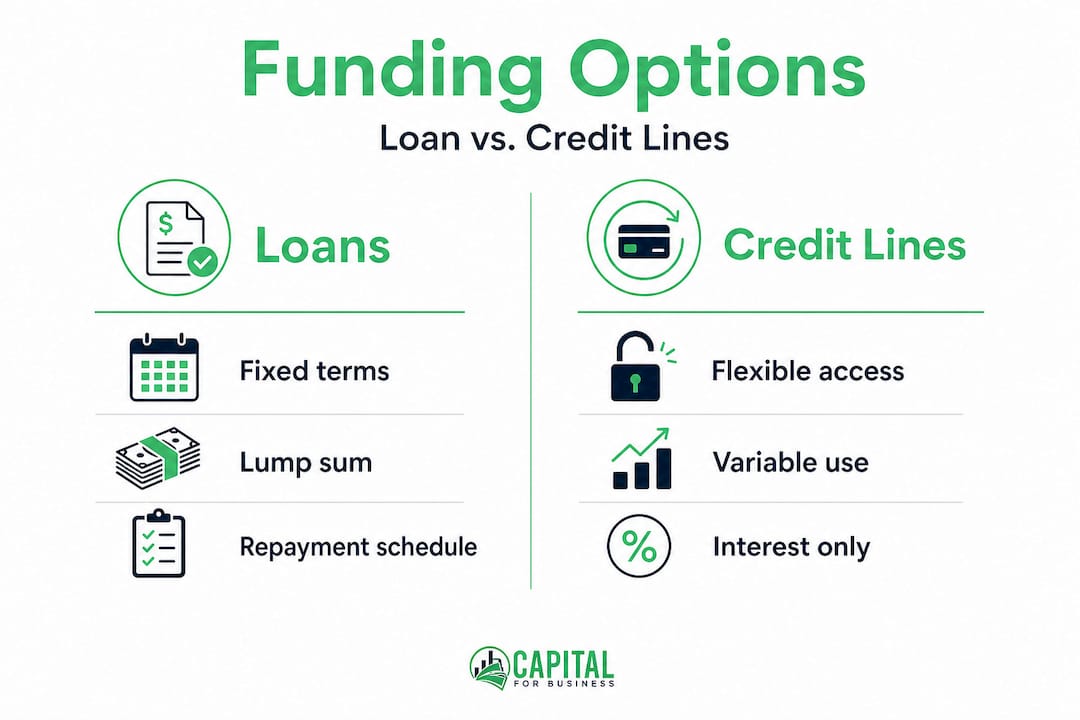

Before you fill out a single application, it helps to understand what you are actually applying for. Business financial services is a broad term that covers everything from term loans and lines of credit to government-backed loan programs, merchant cash advances, and equipment financing. Each product is designed for a different need, and choosing the wrong one can cost you time and money.

Loans, lines of credit, and risk-sharing programs are the three most common categories small business owners encounter. A term loan delivers a fixed lump sum that you repay over a set period with interest. A business line of credit works more like a credit card: you draw funds when you need them, repay them, and draw again. Risk-sharing programs are different from both. They are not grants, and they do not give you free money. They encourage private lenders to approve loans they might otherwise decline by having a government entity absorb part of the loss if a borrower defaults.

One of the most misunderstood programs in Canada is the Canada Small Business Financing Program (CSBFP), which is a government risk-sharing arrangement that helps small businesses access loans through financial institutions, with the federal government sharing the lender's risk rather than eliminating it entirely. Many owners apply expecting grant-like treatment. They are surprised when they still face full credit underwriting. Understanding this distinction from the start saves significant frustration.

In the U.S., the Small Business Administration (SBA) operates a similar model. The SBA does not lend money directly to most small businesses. Instead, it guarantees a portion of loans made by approved lenders, which reduces the lender's exposure and makes approval more accessible for businesses that lack extensive collateral or long credit histories.

Financing options: Canada vs. U.S.

| Feature | Canada (CSBFP model) | U.S. (SBA model) |

|---|---|---|

| Program type | Government risk-sharing loan | Government-backed loan guarantee |

| Who lends the money | Banks and credit unions | SBA-approved private lenders |

| Eligible uses | Equipment, leasehold improvements, working capital | Working capital, equipment, real estate, expansion |

| Loan limits | Up to $1.15 million CAD | Up to $5 million USD (varies by program) |

| Borrower responsibility | Full repayment required | Full repayment required |

| Credit underwriting | Yes, by the lending institution | Yes, by the participating lender |

The uses of proceeds matter as much as the type of program you select. Common eligible uses include purchasing or upgrading equipment, covering working capital gaps during slow seasons, funding leasehold improvements, buying commercial vehicles, or financing business expansion into new markets. Our business loan guide breaks down these use cases in greater detail for owners who want to match the right product to the right business goal.

Typical funding categories small businesses access include:

- Working capital: Covers day-to-day operational expenses such as payroll, inventory, and vendor payments

- Equipment financing: Used to purchase or lease specific business equipment with the asset often serving as collateral

- Business lines of credit: Flexible revolving credit for short-term or variable cash needs

- Merchant cash advances: Advances based on future credit card sales, typically repaid as a percentage of daily transactions

- Term loans: Fixed loan amounts for defined projects with structured repayment schedules

Understanding which category fits your current situation is the first step in the application process. If you are already planning a loan application, reviewing the full process for applying for business loans can help you avoid common early mistakes.

How lenders evaluate your business: Risk, repayment, and documentation

Once you understand what financial products exist, the next question is: how does a lender decide whether to approve you? Lenders follow a structured underwriting process that evaluates your business's ability to repay, not just your intent to repay.

A critical point that risk-sharing programs confirm is that even when a government entity shares the lender's risk, the lender still conducts full underwriting of the borrower's repayment ability, and the borrower remains fully responsible for repayment. Government backing does not substitute for a strong financial story. It simply makes lenders slightly more willing to look at businesses they might have otherwise passed on.

"Lenders are not looking for reasons to approve you. They are looking for evidence that you can and will repay. Your job is to make that evidence as clear and organized as possible."

The CSBFP's evaluation methodology uses structured data sources including borrower databases, quantitative performance reports, and interviews, which tells you something important: program administrators and lenders track data systematically. Your financial story needs to be equally systematic to hold up under that level of scrutiny.

What lenders want to see

Here is the standard documentation most lenders expect before they review any application:

- Business financial statements: At minimum two years of income statements and balance sheets, showing revenue trends, profitability, and liabilities

- Cash flow projections: A 12-month forward-looking projection that demonstrates how you will generate enough cash to service the new debt

- Use of proceeds statement: A clear, specific explanation of exactly how the loan funds will be used, down to dollar amounts and timelines

- Business plan or executive summary: For newer businesses especially, a written plan that outlines the market, competitive position, and revenue model

- Personal financial statements: Many lenders require owners with a significant equity stake to show personal assets and liabilities

- Tax returns: Both personal and business returns for the past two to three years

- Legal documents: Business registration, licenses, lease agreements, and any franchise agreements if applicable

- Collateral documentation: Appraisals or asset listings if the loan requires secured collateral

Pro Tip: The most common reason loan applications stall or get declined is not poor credit. It is an incomplete or inconsistent financial story. If your cash flow projection assumes 20% revenue growth with no supporting market data, a lender will question every other number in your file. Ground every assumption in verifiable facts.

Before you submit, review the loan approval considerations that experienced lenders weigh most heavily. You can also work through a step-by-step application guide to make sure nothing is missing. If equipment is part of your loan request, the equipment financing checklist provides a detailed breakdown of what to prepare specifically for asset-based loans.

Working capital: What it is, how it's measured, and why it matters

Working capital is one of those terms that business owners hear constantly but often cannot define precisely when asked. Simply put, working capital is the difference between your current assets (cash, accounts receivable, and inventory) and your current liabilities (accounts payable, short-term debt, and accrued expenses). A positive working capital number means your business can cover its short-term obligations. A negative number is a warning sign.

Working capital is not just an accounting concept. It is a daily operational reality. A business with solid sales but slow-paying customers can run out of cash entirely while waiting for receivables to clear. That gap between when you pay suppliers and when customers pay you is exactly the kind of problem working capital financing is designed to solve.

![]()

Cash conversion cycle benchmarks

The cash conversion cycle (CCC) is the most practical metric for measuring working capital efficiency. It measures the number of days it takes a business to convert investments in inventory and other resources into cash from sales. A shorter cycle means faster cash recovery. According to KPMG's 2025 working capital research, the average cash conversion cycle across all U.S. companies increased from 83 days in 2020 to 90 days in 2023, then improved slightly to 89 days in 2024, with notable variation by company size.

| Segment | 2020 CCC (days) | 2023 CCC (days) | 2024 CCC (days) |

|---|---|---|---|

| All companies | 83 | 90 | 89 |

| Small businesses | Higher than average | Higher than average | Typically 95 to 110+ |

| Large corporations | Below average | Below average | Often 60 to 75 |

Small businesses consistently carry longer cash conversion cycles than larger companies because they have less leverage with suppliers, fewer resources for credit management, and smaller cash reserves to absorb delays. This is why understanding your own CCC before approaching a lender is so valuable. It shows you know your business's financial mechanics, and it helps you frame how the loan will improve your cycle.

Several factors directly influence how long your cash conversion cycle runs:

- Accounts receivable days: How long customers take to pay invoices; shorter is better

- Inventory turnover rate: How quickly you sell through stock; slow-moving inventory ties up cash

- Accounts payable terms: How long your suppliers give you to pay; longer terms improve your position

- Seasonal revenue patterns: Industries with strong seasonal swings often see dramatic CCC changes by quarter

- Customer payment behavior: B2B businesses often face longer cycles than B2C businesses by default

Pro Tip: Before applying for any loan or line of credit, run your cash conversion cycle for the most recent 12-month period and compare it to industry benchmarks. If your CCC is significantly longer than your competitors', that is a red flag lenders will notice. Address it in your application by explaining your receivables management strategy and how the funding will help close the gap.

The essential working capital tips resource walks through practical steps for improving your cycle before you approach lenders. If you want to understand how a small business loan can directly support working capital needs, or see real-world examples of working capital solutions across different industries, both resources are worth your time before submitting any application.

Accessing business financial services: Step-by-step application and practical tips

You now have the foundational knowledge. You understand the types of financing available, what lenders look for, and how to measure your working capital health. The next step is translating all of that into an actual application. Here is a practical, step-by-step process to guide you through.

-

Clarify your funding purpose: Define exactly why you need the capital, how much you need, and what measurable outcome you expect. Vague purposes like "general business needs" weaken every application.

-

Assess your current financial position: Pull together your most recent income statements, balance sheets, and bank statements. Calculate your working capital ratio and your cash conversion cycle. Know your numbers before a lender asks.

-

Choose the right product: Match your need to the right financing product. Equipment purchases fit equipment financing. Seasonal cash gaps fit a line of credit. Long-term investments fit term loans. Refer back to the comparison table in section two if you need a reminder.

-

Research available programs: In Canada, check whether you qualify for the CSBFP through your bank. In the U.S., ask lenders about SBA guarantee programs. These programs exist to make approval more accessible, but you still need to qualify under standard underwriting criteria.

-

Gather your documentation: Use the numbered list from section three as your checklist. Do not submit an application until every document on that list is ready, organized, and consistent with your financial narrative.

-

Build your financial narrative: Write a short, clear summary of your business, your funding need, your use of proceeds, and your repayment plan. This narrative is what connects all your supporting documents into a coherent story.

-

Submit and follow up: Submit your complete application to your lender of choice. Follow up within a week to confirm receipt and ask about timeline. Prompt, professional follow-through signals that you are organized and serious.

-

Review your loan offer carefully: When you receive a term sheet or offer, compare interest rates, fees, repayment schedule, and covenants before signing. Do not let urgency push you into terms you have not fully analyzed.

Practical tips to strengthen each step:

- Use accounting software to generate clean, consistent financial statements rather than manually compiled spreadsheets

- Have a professional review your cash flow projection before submission

- If your credit score is below lender thresholds, address it before applying rather than hoping the application compensates

- Apply to multiple lenders simultaneously to preserve your negotiating position

- Keep a record of all communications and document versions you submit

The step-by-step loan application guide and our working capital tips resource provide further tactical support for each stage of this process.

Why most small businesses miss out on funding: Our take

After working with small business owners across hundreds of industries since 2009, we have seen the same patterns repeat. The businesses that struggle to secure funding are not always the ones with weak financials. Often, they are businesses with real potential that have never been taught how to present themselves to a lender.

The biggest misconception we encounter is the belief that a government guarantee program like the CSBFP or the SBA model eliminates lender scrutiny. It does not. As confirmed by the CSBFP program structure, lenders still evaluate borrower repayment ability fully, and the borrower remains entirely responsible for the debt. Government backing lowers the lender's risk exposure; it does not lower the documentation standard.

The second pattern is treating lenders as gatekeepers rather than partners. When a business owner approaches a lender with a defensive mindset, expecting to be interrogated, they often present information reactively and incompletely. The more effective approach is to walk in as a partner presenting an opportunity. You are giving this lender the chance to earn interest on a well-managed loan. Your job is to make that case clearly and confidently.

The third and most correctable issue is the absence of a prepared financial narrative. Many owners hand over financial statements and assume the numbers speak for themselves. They do not. Lenders see hundreds of applications. A well-organized summary that connects your revenue trends, your working capital position, your use of proceeds, and your repayment capacity in one clear document stands out immediately.

Working through a step-by-step loan application guide before your first lender conversation can dramatically change the quality of that conversation. It is not about gaming the system. It is about showing up prepared with the same professionalism you bring to your best customers.

Pro Tip: A strong financial narrative does not require perfect numbers. It requires honest, organized numbers with a clear explanation of what they mean and where they are headed. Lenders appreciate transparency about challenges far more than they appreciate numbers that look too clean to be credible.

The businesses that consistently secure funding treat every application as a presentation, not a form. They prepare, they organize, they anticipate questions, and they follow through. That discipline, more than credit score or collateral alone, is what separates funded businesses from unfunded ones.

Unlock business funding with expert guidance

Capital for Business has spent more than 15 years helping small business owners across Canada and the U.S. access the funding they need to grow, expand, and compete. Whether you are navigating your first loan application or looking for a faster path to working capital, our team works quickly, transparently, and at terms that work for your business.

If you are ready to explore your options, start by reviewing the types of easy small business loans available through our platform. If working capital is your immediate priority, our dedicated working capital funding solutions can help bridge the gap fast. For businesses that need machinery, vehicles, or technology to move forward, our equipment financing programs offer flexible terms designed for real-world business needs. We are here when banks say no, and we make the process as straightforward as possible.

Frequently asked questions

Is the CSBFP a grant or a loan guarantee?

The CSBFP is a government risk-sharing program that backs loans made by financial institutions, not a grant, meaning you borrow and repay the full loan amount through your lender.

What documents do lenders usually require for business loans?

Lenders typically require financial statements, tax returns, a business plan, cash flow projections, and a specific use of proceeds statement. Even with risk-sharing programs backing your loan, these documents remain mandatory because lenders still underwrite your repayment ability independently.

How do I measure working capital in my business?

Working capital equals current assets minus current liabilities, and the cash conversion cycle measures how efficiently your business converts activity into cash. KPMG's working capital benchmarks show the U.S. average at 89 days in 2024, giving you a useful starting point for comparison.

Are government guarantees enough to secure loan approval?

No. Government programs reduce the lender's loss exposure if you default, but they do not replace the standard underwriting process. Lenders still assess repayment ability and require complete, credible documentation before approving any loan.

How long does it take to get funding for working capital?

Timelines vary depending on the lender, the loan type, and how complete your documentation is. Small businesses that arrive with organized financials and a clear use of proceeds statement can often secure funding within a few weeks, while incomplete applications can extend the process by months.