TL;DR:

- Alternative lending provides small businesses with faster, more accessible financing options outside traditional banks, often using digital processes and broader data. These products include merchant cash advances, equipment financing, and lines of credit, tailored to specific business needs and cash flow profiles. When properly managed, alternative loans can accelerate growth; however, understanding their costs and repayment impacts is essential for sound financial decision-making.

A bank rejection does not have to stop your business growth. Millions of small business owners across the United States and Canada face that exact situation every year, only to discover that alternative lending has quietly matured into a reliable, fast, and accessible pathway to capital. Whether you need funds for new equipment, working capital to cover payroll, or a cash advance tied to your sales volume, the alternative lending market now offers a broad range of structured products built specifically for businesses that banks overlook. This article walks you through what alternative lending is, which options fit your situation, how the pros and cons stack up, and exactly how to apply.

Table of Contents

- What is alternative lending and how does it work?

- Types of alternative lending solutions for small businesses

- Pros and cons: Alternative lending vs. bank loans

- How to qualify and apply for alternative small business loans

- The overlooked realities of alternative lending for small businesses

- How Capital For Business connects you to funding options

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Accessible financing | Alternative lending offers funding paths when banks say no, opening doors for more small businesses. |

| Fast approval | Most alternative lenders approve loans within hours or days using digital tools and new criteria. |

| Flexible options | A variety of loan types lets businesses choose the solution best matched to their needs. |

| Balanced decision-making | Comparing pros and cons helps you avoid pitfalls and pick the right financing option for your situation. |

What is alternative lending and how does it work?

Traditional bank loans follow a familiar formula: strong credit score, years of operating history, substantial collateral, and months of underwriting. That formula works for an established business with a clean financial record, but it leaves a significant portion of small businesses without access to the capital they actually need. Alternative lending was built to solve that problem.

Alternative lending refers to any financing product offered outside of a traditional bank or credit union. This includes online lenders, fintech platforms, direct capital providers, peer-to-peer networks, and specialty finance companies. These lenders evaluate your business using a wider set of data points and, critically, they do it much faster. Alternative lenders assess risk using different data and faster technology than traditional banks, which means your cash flow patterns, transaction history, and even your industry performance can count as much as your credit score.

The core difference comes down to access and speed. Traditional banks underwrite loans over weeks or months. Alternative lenders often complete the same process in hours or days. They use digital applications, automated verification, and real-time financial data to make faster decisions without sacrificing accuracy.

Key features you will typically find with alternative lenders:

- Fully digital application process, often completable in under 30 minutes

- Decisions based on cash flow and revenue, not just credit scores

- Flexible collateral requirements, sometimes with no collateral at all

- Funding timelines ranging from same-day to a few business days

- Loan amounts ranging from a few thousand dollars to several million

- Repayment structures tied to revenue, daily sales, or fixed schedules

- Open eligibility for newer businesses, sometimes as little as six months in operation

The comparison below shows how these two lending worlds differ when measured on the factors that matter most to a small business owner.

| Feature | Traditional bank | Alternative lender |

|---|---|---|

| Application process | Paper-heavy, branch visits | Fully digital, online |

| Approval time | Weeks to months | Hours to a few days |

| Minimum credit score | Typically 680+ | Often 500 to 600+ |

| Time in business required | Usually 2+ years | Sometimes 6 months |

| Collateral requirements | Usually required | Often flexible or none |

| Funding speed | Slow | Fast |

| Accessibility for small businesses | Limited | High |

"The shift to technology-driven underwriting has fundamentally changed who can access business credit. Small businesses now have options that simply did not exist a decade ago." This reality is one of the most important changes in small business financing over the past several years.

Understanding how tech in small business lending has evolved helps explain why alternative lenders can serve customers that banks routinely turn away, and why so many business owners are now choosing this path voluntarily, not just out of necessity.

Types of alternative lending solutions for small businesses

Now that the basics are clear, let's explore the range of alternative lending tools available for your business. Each product is designed for a specific type of capital need, so matching the right tool to the right situation is essential.

There are several major categories of alternative lending: merchant cash advance, equipment financing, working capital loans, and peer-to-peer lending, among others. Each carries its own structure, repayment terms, and ideal use case.

| Loan type | Best use case | Typical amounts | Approval time |

|---|---|---|---|

| Merchant cash advance | Businesses with high card sales volume | $5,000 to $500,000 | 24 to 48 hours |

| Equipment financing | Purchasing or leasing specific equipment | $10,000 to $5 million | 1 to 5 days |

| Working capital loan | Daily operations, payroll, inventory | $5,000 to $500,000 | 1 to 3 days |

| Business line of credit | Ongoing flexible access to funds | $10,000 to $250,000 | 1 to 5 days |

| Invoice factoring | Businesses waiting on unpaid invoices | Varies by receivables | 1 to 3 days |

| Peer-to-peer lending | Lower loan amounts, flexible criteria | $5,000 to $300,000 | 3 to 7 days |

When to consider each type:

- Merchant cash advance: Your business processes a strong volume of credit and debit card transactions. Repayment comes as a percentage of daily card sales, so it naturally adjusts to slower periods.

- Equipment financing: You need a specific piece of machinery, vehicle, or technology. The equipment itself serves as collateral, which improves approval odds significantly.

- Working capital loan: Your business faces a temporary cash shortfall or seasonal gap. These working capital loan basics are ideal for keeping operations running smoothly without disrupting growth.

- Business line of credit: You want flexible, reusable access to funds rather than a single lump sum. Draw what you need, repay it, and draw again.

- Invoice factoring: Your business carries significant accounts receivable (money owed by customers) and cannot wait 30 to 90 days for payment.

- Peer-to-peer lending: You want a competitive rate and are comfortable working through an online lending platform that connects businesses with individual investors.

The equipment financing guide available from Capital for Business walks through how asset-based financing works in detail, including how the equipment's value affects your loan terms and approval likelihood.

Pro Tip: Before you apply anywhere, write down exactly what the funds will be used for and how long you need access to the money. A short-term operational need calls for a different product than a multi-year equipment purchase. Matching your capital need to the right product saves time and reduces total borrowing cost.

If you are unsure whether a merchant cash advance or a term loan fits your situation, the merchant cash advance overview breaks down how repayment works for card-heavy businesses and helps you decide whether this structure suits your cash flow model.

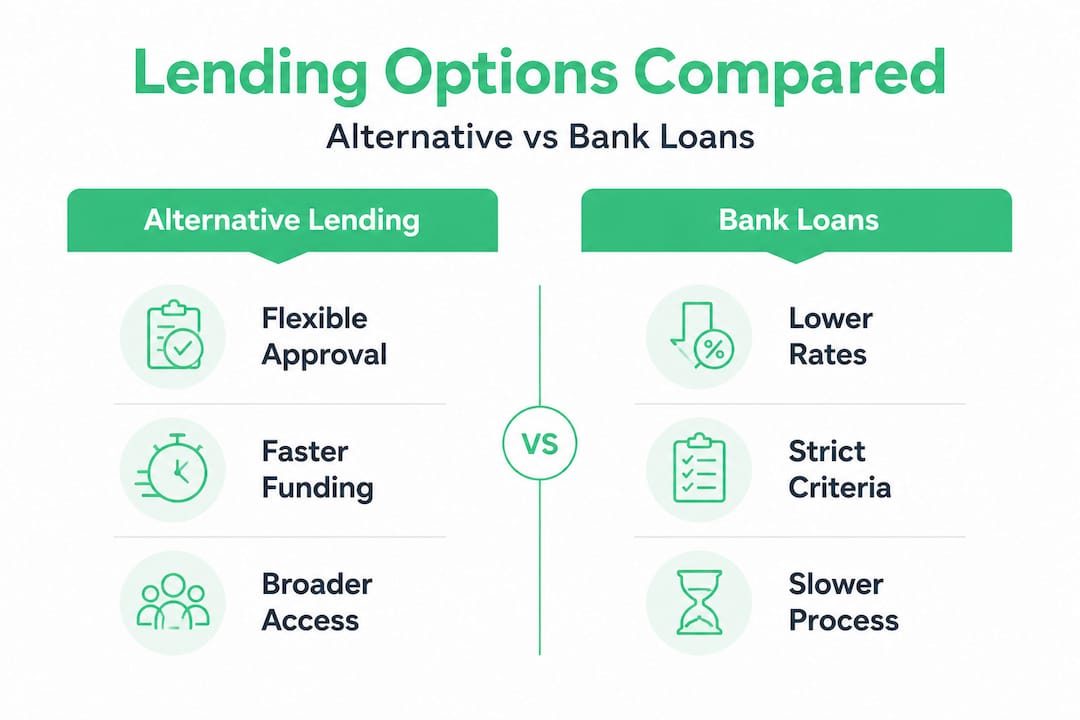

Pros and cons: Alternative lending vs. bank loans

With these lending types in mind, it's crucial to weigh their strengths and weaknesses next to bank lending. No financing product is perfect. Understanding both sides of the equation helps you make a decision you can manage confidently over the life of the loan.

Alternative lenders are faster, more accessible, but can have higher costs compared to banks. That single truth shapes almost every comparison you will make between the two options.

Advantages of alternative lending:

- Speed: Funding can arrive in 24 to 72 hours, which is critical when payroll is due or an opportunity has a short window.

- Flexible qualifications: Revenue, cash flow, and business performance matter more than a perfect credit score.

- Broader eligibility: Newer businesses and those with past credit challenges can qualify for products that banks would never approve.

- Simpler process: Digital applications, fewer documents, and no branch visits make the experience far less stressful.

- Product variety: From merchant cash advances to invoice factoring, the range of options matches a wider variety of business needs.

- Transparent terms: Many alternative lenders offer clear, upfront pricing without hidden fees buried in loan documents.

Disadvantages of alternative lending:

- Higher rates: Annual percentage rates (APRs) can run significantly higher than bank loan rates, particularly for short-term products.

- Shorter repayment periods: Many alternative loans run 3 to 18 months, which raises your periodic payment compared to a 5-year bank term.

- Less regulation: The alternative lending space is less uniformly regulated, so borrower protections vary by lender and product type.

- Smaller loan amounts: While some alternative lenders fund millions, others cap products at amounts that may not meet larger capital needs.

- Factor rate structures: Products like merchant cash advances use factor rates rather than APRs, which can make true cost comparisons harder to calculate.

Understanding why banks decline small business loans puts the disadvantages of alternative lending in context. If a bank would not approve you anyway, the higher cost of an alternative loan is the actual market rate for your current risk profile, not a penalty.

Pro Tip: To evaluate whether an alternative loan makes financial sense, estimate the revenue you expect to generate with the borrowed funds and compare it to the total repayment amount. If the return clearly exceeds the cost of borrowing, the loan is likely a good business decision even if the rate looks high on paper. For additional context, alternative funding solutions offers a breakdown of how to assess total cost across different product types.

How to qualify and apply for alternative small business loans

Once you know which lending route fits, taking action means understanding exactly how to qualify and apply. The process is faster than a bank loan, but being prepared still makes a real difference in your outcome.

Alternative lenders often look at cash flow, time in business, and digital transaction history, sometimes extending credit even if your bank says no. This broader lens means you need to present your business accurately and completely, not just your credit score.

Typical eligibility requirements for alternative lenders:

- Minimum 6 to 12 months in business (some lenders require 2 years)

- Annual revenue between $50,000 and $250,000, depending on the product

- A credit score of 500 or above (requirements vary widely by lender)

- Active business checking account with regular transaction activity

- No active bankruptcies or significant unresolved tax liens

Steps to apply for alternative small business financing:

- Identify your need and loan type. Be specific about the dollar amount, the purpose, and the repayment timeline you can realistically manage.

- Research lenders that match your profile. Look for lenders who specialize in your industry, business age, or revenue level. Not every alternative lender serves every business type.

- Gather your documents in advance. Having everything ready before you start an application speeds up the process and reduces back-and-forth with the lender.

- Complete the online application. Most alternative lenders use streamlined digital forms. Be accurate and complete. Missing information causes delays.

- Review your offer carefully. Read the repayment terms, total repayment amount, and any fees before signing. Ask questions if anything is unclear.

- Respond quickly to follow-up requests. If the lender asks for additional information, respond the same day. Speed is a two-way street in alternative lending.

- Receive your funds and track your use. Keep a clear record of how borrowed funds are used so you can measure the return on that investment.

Documents most alternative lenders will request:

- Three to six months of business bank statements

- Most recent business tax return (and personal, in some cases)

- Proof of business ownership and legal registration

- Government-issued photo identification

- Profit and loss statement or financial summary

- A brief description of how you plan to use the funds

Learning how the alternative loan approval process works can help you avoid common delays and improve your chances of getting funded the first time. And if your cash needs fall outside a single loan product, understanding how to fill funding gaps with multiple solutions gives you a more complete financial strategy.

The overlooked realities of alternative lending for small businesses

Most guides on alternative lending focus on the mechanics: what products exist, how to qualify, and what rates look like. That information matters. But after working with business owners across hundreds of industries since 2009, we have seen a consistent set of mistakes and misunderstandings that rarely appear in standard financing articles.

The most common mistake is choosing the cheapest-looking option without considering the repayment structure. A lower factor rate on a merchant cash advance can still cost more in absolute dollars than a slightly higher-rate term loan with a longer repayment period. The total cost of capital, not the rate alone, is the number that should drive your decision.

Business owners also tend to underestimate how short funding cycles affect their cash flow. A 90-day loan with daily repayment sounds manageable until you realize that every single business day, money is leaving your account before you have a chance to use it for operations. That daily draw changes your working capital picture in ways that monthly-payment borrowers rarely face.

We also see businesses borrow for the right reason but the wrong amount. Underborrowing is as risky as overborrowing. If you take $30,000 when you actually need $50,000 to complete a project or purchase, you may find yourself back in the application process two months later, this time from a weaker financial position. Borrowing enough to fully execute your plan is almost always smarter than taking a smaller amount to feel conservative.

Common pitfalls we see businesses fall into with alternative lending:

- Applying for multiple loans simultaneously, which can trigger multiple hard credit inquiries

- Ignoring the daily or weekly repayment impact on operational cash flow

- Choosing a lender based on a single advertised rate without reviewing full terms

- Failing to account for prepayment policies, which vary significantly by lender

- Using short-term capital for long-term investments, creating a repayment mismatch

- Not asking about renewal or refinancing options before the original loan matures

The best borrowing decision is the one that fits your specific business cycle, not the one that looks best in a brochure. Understand your cash flow before you commit to any repayment structure.

Staying current on 2026 financing trends is also worth your time. The alternative lending market evolves quickly, and products that were expensive or unavailable two years ago may now be well-priced and accessible for your industry. Business owners who revisit their financing options annually often find better terms as their revenue and credit profile improve.

The honest truth is that alternative lending is a tool, not a solution on its own. Used strategically, with clear purpose and realistic repayment expectations, it accelerates growth. Used carelessly, it can add financial strain at exactly the wrong moment. The difference almost always comes down to preparation and honesty about your actual cash flow.

How Capital For Business connects you to funding options

Understanding your alternative lending options is a strong first step. Taking action is what creates results. Capital for Business has served small business owners across the United States and Canada since 2009, offering a wide range of financing solutions built for businesses that banks overlook or underserve.

Whether you are looking to explore loan types that fit your business model, need to apply for working capital to cover an immediate operational need, or want to speak with a funding specialist about the best path forward, Capital for Business offers the products and guidance to move quickly. Our team works with businesses across hundreds of industries, including those with imperfect credit, limited history, or urgent timelines. The application process is straightforward, the decisions are fast, and the funding is real. When you are ready to take the next step, get started with fast funding through a simple online inquiry that connects you to the right solution for your situation.

Frequently asked questions

What documents do I need to apply for alternative business loans?

You generally need three to six months of business bank statements, your most recent business tax return, proof of business ownership, a government-issued ID, and a brief summary of how you plan to use the funds.

Is alternative lending more expensive than traditional bank loans?

Alternative lenders are often more accessible but can charge higher costs than traditional banks, though the faster funding and easier qualification often justify the difference for businesses that cannot meet bank standards.

How quickly can I get approved for alternative lending?

Approvals may come within hours or days since alternative lenders use fast, technology-driven evaluation methods that bypass the slow manual underwriting common at traditional banks.

Can I get alternative funding with bad credit?

Yes, some alternative lenders focus on cash flow and overall business performance rather than credit scores alone, making it possible to qualify for financing even if your bank has already said no.