Banks turn down business funding requests every day, and the reasons often surprise small business owners who believe their applications are solid. Many assume rejection stems solely from poor credit, but the reality involves multiple factors ranging from incomplete documentation to industry risk perception. Understanding these reasons empowers you to address weaknesses in your application and explore alternative financing routes that can keep your business moving forward. This guide breaks down why banks say no and reveals practical funding options available to small businesses across the U.S. and Canada.

Table of Contents

- Key takeaways

- Common reasons banks reject business funding

- How to identify and address your rejection causes

- Comparing bank loans with alternative small business funding options

- Best practices for increasing approval odds for future funding

- Explore flexible small business funding solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Rejection triggers | Common causes include weak credit, poor cash flow, incomplete documentation, industry risk, and insufficient collateral. |

| Documentation quality matters | Incomplete or inaccurate paperwork dramatically reduces approval odds and can stall underwriting. |

| Prepare financials in advance | Gather at least two years of financial statements, tax returns, and bank statements and organize them chronologically to avoid delays. |

| Alternative financing options | Beyond banks, consider equipment leasing, lines of credit, government programs, and other funding routes to keep growth moving. |

Common reasons banks reject business funding

Banks evaluate business funding applications through multiple lenses, and poor credit history remains a leading cause for rejection. Your credit score signals repayment reliability, but it's just one piece of the puzzle. Banks dig deeper into your financial health by examining cash flow statements, profit and loss reports, and balance sheets to determine whether your business generates enough revenue to service debt. Weak or inconsistent cash flow raises red flags about your ability to make regular payments.

Documentation quality makes or breaks applications. Incomplete or inaccurate applications significantly reduce approval chances, forcing underwriters to reject requests they cannot properly evaluate. Missing tax returns, outdated financial statements, or unclear business plans leave banks with insufficient information to assess risk. Many small business owners underestimate how thoroughly banks scrutinize every document, from bank statements to vendor contracts.

Beyond paperwork, banks consider industry risk and market conditions. Businesses in sectors experiencing volatility or decline face higher rejection rates regardless of individual financial strength. Insufficient collateral poses another barrier, particularly for larger loan amounts where banks require tangible assets to secure their investment. Timing matters too. Applying during periods of business instability or right after major financial setbacks typically results in denial.

Pro Tip: Before applying, gather at least two years of financial statements, tax returns, and bank statements. Organize them chronologically and ensure all figures match across documents to avoid raising concerns about accuracy.

Common rejection triggers include:

- Credit scores below 650 for most traditional bank products

- Debt-to-income ratios exceeding 40%, indicating over-leverage

- Less than two years in business, viewed as high risk

- Negative cash flow in recent quarters

- Outstanding tax liens or legal judgments

- Unclear explanation of how loan funds will be used

Understanding these factors helps you evaluate your application objectively. Review important loan considerations and assess where your business stands before submitting paperwork. Strengthening weak areas before applying dramatically improves your odds, while rushing an unprepared application wastes time and potentially damages your credit through unnecessary hard inquiries. Taking time to address vulnerabilities demonstrates the financial discipline banks seek in borrowers, positioning you for better outcomes when increasing loan approval chances.

How to identify and address your rejection causes

Receiving a rejection letter stings, but it provides valuable intelligence for your next attempt. Request specific feedback from the lender explaining why they declined your application. Federal regulations require lenders to provide adverse action notices detailing rejection reasons, giving you concrete areas to improve. Don't settle for vague responses. Push for clarity on whether credit, financials, documentation, or other factors drove the decision.

Once you identify weaknesses, create an action plan:

- Audit your financial records for accuracy and completeness. Hire a bookkeeper or accountant if your records contain gaps or inconsistencies that undermine credibility.

- Address credit issues systematically by paying down high-balance accounts, disputing errors on credit reports, and establishing positive payment history over several months.

- Strengthen your business plan with detailed financial projections, clear market analysis, and specific explanations of how borrowed funds will generate revenue or reduce costs.

- Gather missing documentation proactively, including updated tax returns, business licenses, lease agreements, and any contracts supporting revenue claims.

- Consider working with a financial advisor or small business development center counselor who can review your application objectively and identify blind spots you might miss.

Improving your application takes time, but preparation tips before applying demonstrate that correcting application errors increases funding likelihood. Rushing a reapplication before addressing core issues typically produces the same result. Give yourself adequate time to implement changes and document improvements.

Pro Tip: Create a loan application checklist based on your rejection feedback. Check off each item as you address it, and don't reapply until every box is marked complete. This systematic approach prevents overlooking critical fixes.

Monitor your progress through measurable improvements. Track your credit score monthly to verify it's climbing. Review updated financial statements quarterly to confirm cash flow is strengthening. Document every step you take to remedy identified weaknesses, as this paper trail demonstrates commitment to financial responsibility when you reapply. Some business owners benefit from starting with smaller loan amounts to establish a track record before pursuing larger funding requests. Following loan application improvement tips positions you for success whether you return to traditional banks or explore alternative lenders.

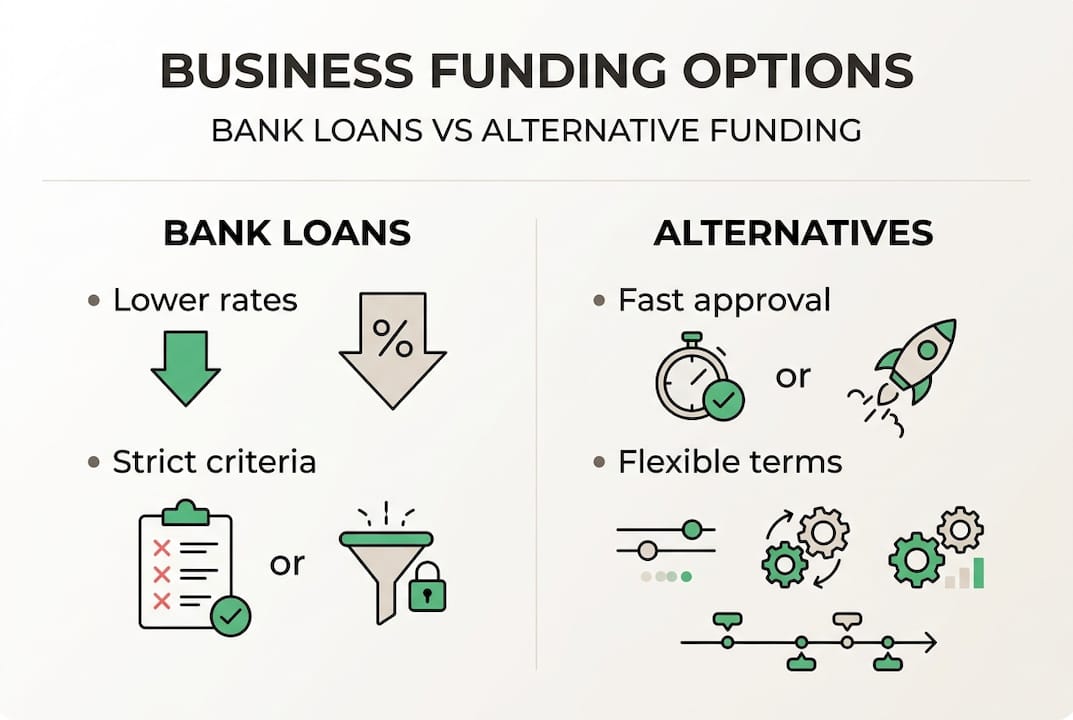

Comparing bank loans with alternative small business funding options

When banks reject your application, alternative lenders offer viable paths to capital. These options differ significantly in structure, requirements, and costs, making comparison essential for informed decisions. Alternative lenders offer faster approvals with less stringent credit requirements, opening doors for businesses banks turn away.

| Funding Type | Approval Speed | Credit Requirement | Typical Amount | Key Advantage |

|---|---|---|---|---|

| Bank Loan | 4-8 weeks | 680+ score | $50k-$5M | Lowest rates |

| Online Business Loan | 1-5 days | 600+ score | $5k-$500k | Fast funding |

| Merchant Cash Advance | 1-3 days | 550+ score | $5k-$250k | Revenue-based repayment |

| Equipment Financing | 3-7 days | 600+ score | Up to equipment value | Equipment serves as collateral |

| Business Line of Credit | 1-2 weeks | 620+ score | $10k-$250k | Flexible draw and repayment |

Online business loans provide quick access to capital with streamlined applications and automated underwriting. Lenders evaluate your business differently than banks, often prioritizing revenue and cash flow over credit scores alone. Approval happens within days rather than weeks, and funds typically arrive within a week of approval. However, interest rates run higher than traditional bank loans, reflecting the increased risk lenders assume.

Merchant cash advances suit businesses with strong credit card sales. Providers advance a lump sum in exchange for a percentage of future credit card receipts. Repayment fluctuates with sales volume, providing breathing room during slow periods. This flexibility comes at a cost, as factor rates often translate to annual percentage rates exceeding 40%.

Equipment financing allows you to purchase necessary equipment while spreading payments over time. The equipment itself serves as collateral, reducing lender risk and making approval easier for businesses with credit challenges. This targeted approach works well when you need specific assets but lack cash reserves.

Business lines of credit offer ongoing access to funds up to a predetermined limit. Draw what you need when you need it, and pay interest only on the outstanding balance. This revolving structure provides flexibility for managing cash flow gaps, seasonal inventory purchases, or unexpected expenses. Approval requirements fall between traditional bank loans and merchant cash advances.

Key advantages of alternative business financing options:

- Faster funding timelines keep business operations moving

- More flexible credit requirements expand access

- Specialized products match specific business needs

- Less documentation burden simplifies applications

- Relationship-based underwriting considers full business picture

Limitations include higher costs, shorter repayment terms, and potentially smaller funding amounts compared to bank loans. Evaluate the total cost of capital, not just monthly payments. A merchant cash advance might offer quick cash but could cost significantly more over time than waiting to improve your application for a bank loan. Match the funding type to your specific situation, considering urgency, amount needed, and your ability to handle repayment terms.

Best practices for increasing approval odds for future funding

Securing business funding requires ongoing financial discipline, not last-minute scrambling before applications. Maintain organized, up-to-date financial records throughout the year. Use accounting software to track income and expenses accurately, reconcile accounts monthly, and generate financial statements quarterly. This habit ensures you can produce required documentation quickly and demonstrates operational competence to lenders.

Build and protect your credit profile actively. Monitor personal and business credit reports regularly for errors or fraudulent activity. Pay all obligations on time, as payment history carries the most weight in credit scoring. Keep credit utilization below 30% of available limits, and maintain a mix of credit types when possible. Establishing trade credit with suppliers and reporting those payments to business credit bureaus strengthens your business credit profile independently of personal credit.

Understand specific lender requirements before applying. Each lender maintains unique criteria for approval, from minimum time in business to acceptable debt-to-income ratios. Research these requirements thoroughly and apply only to lenders whose criteria you meet or exceed. Shotgun applications to multiple lenders waste time and generate hard inquiries that temporarily lower your credit score.

Pro Tip: Create a funding readiness folder containing all documents lenders typically request. Update it quarterly so you're always prepared to apply when opportunities arise or needs emerge.

Work with financial professionals to strengthen your applications. Accountants ensure financial statements follow proper formatting and accurately represent your business. Business consultants help craft compelling business plans that address lender concerns proactively. Some small business development centers offer free application review services, providing expert feedback before you submit to lenders.

Preparedness and proper documentation drive higher approval rates. Present clear, detailed explanations of how you'll use borrowed funds and how those investments will generate returns. Lenders want to see thoughtful planning, not vague statements about growth or expansion. Quantify expected outcomes with realistic projections based on market research and historical performance.

Implement these ongoing practices:

- Schedule quarterly financial reviews to catch issues early

- Maintain separate business and personal finances

- Document major business decisions and their financial impacts

- Build cash reserves to demonstrate financial stability

- Establish relationships with lenders before you need funding

- Keep business licenses, insurance, and registrations current

Following loan application best practices and maintaining a structured business loan application workflow transforms funding from a stressful scramble into a manageable process. The businesses that secure funding most reliably treat financial readiness as an ongoing operational priority, not a project that starts when cash runs low. This proactive approach positions you to capitalize on opportunities quickly and weather challenges without desperate funding searches.

Explore flexible small business funding solutions

Capital For Business specializes in helping small businesses secure funding when traditional banks say no. Since 2009, we've worked with business owners across hundreds of industries throughout the U.S. and Canada, providing accessible financing solutions tailored to real-world business needs. Whether you're managing credit challenges, need fast funding, or require specialized financing products, our range of options helps you find the right fit.

We offer easy small business loan options including working capital, merchant cash advances, equipment financing, and business lines of credit up to $500,000. Our streamlined application process delivers decisions quickly, often within 24 hours, and funding can reach your account in as little as two business days. Even businesses with imperfect credit histories qualify for bad credit business loans designed specifically for your situation. Explore our complete range of business funding solutions to find the product that matches your needs and timeline.

Frequently asked questions

Why do banks reject business funding even with good credit?

Banks evaluate multiple factors beyond credit scores when assessing loan applications. Strong credit helps, but insufficient cash flow, weak business plans, or incomplete documentation can still trigger rejection. Banks also consider industry risk, time in business, and collateral availability as critical decision factors. Even profitable businesses face rejection if they cannot demonstrate stable, predictable revenue streams that support debt service. Understanding these bank loan rejection reasons helps you address vulnerabilities before applying.

Can I reapply for a bank loan after being rejected?

Yes, you can reapply after addressing the specific issues that caused rejection. Request detailed feedback from the lender explaining their decision, then systematically fix identified problems before resubmitting. Most experts recommend waiting at least three to six months between applications to allow time for meaningful improvements to credit, financials, or documentation. Reapplying too quickly without addressing core issues typically produces the same result while generating additional hard inquiries on your credit report. Consider increasing chances on reapplication by working with financial advisors who can objectively assess your readiness.

What are the best alternative funding options if banks say no?

Online business loans, merchant cash advances, and equipment financing represent the most accessible alternatives for businesses banks reject. These options feature faster approval timelines, more flexible credit requirements, and specialized structures matching specific business needs. Online lenders often approve businesses with credit scores in the 600s, while merchant cash advances work well for businesses with strong credit card sales but credit challenges. Equipment financing uses the purchased equipment as collateral, reducing approval barriers. Evaluate costs carefully, as alternative financing options typically carry higher rates than bank loans but provide faster access to capital when you need it most.

How long should I wait before reapplying after rejection?

Wait at least 90 days before reapplying to the same lender, giving yourself time to address rejection causes meaningfully. Use this period to improve credit scores, strengthen financial statements, complete missing documentation, or refine your business plan. Some situations require longer waiting periods, particularly if you need to demonstrate sustained revenue growth or resolve legal issues. Applying to different lenders during this time is acceptable if you've addressed the core issues that caused initial rejection. Focus on quality improvements rather than rushing reapplications that face the same obstacles.

Do alternative lenders report to business credit bureaus?

Many alternative lenders report payment activity to business credit bureaus, helping you build credit history through successful repayment. However, practices vary by lender and product type. Ask potential lenders directly about their reporting policies before accepting funding. Merchant cash advance providers typically don't report to credit bureaus since advances aren't structured as traditional loans. Equipment financing companies and online business lenders more commonly report payment history. Successfully managing alternative financing and demonstrating reliable repayment can strengthen your credit profile for future traditional bank loan applications.