Merchant cash advances promise fast money when your business needs it most, but effective APRs can exceed 350% in 2026. Many small business owners rush into these agreements without fully grasping how they work or the financial risks they carry. This guide cuts through the confusion to reveal what merchant cash advances actually are, their true costs, and when they might make sense for your business. You'll learn how to evaluate these financing options against traditional loans and protect yourself from predatory terms that could trap your business in a debt spiral.

Table of Contents

- What Is A Merchant Cash Advance And How Does It Work?

- The Hidden Costs And Financial Risks Of Merchant Cash Advances

- Comparing Merchant Cash Advances With Traditional Business Loans

- Best Practices And Legal Considerations When Using Merchant Cash Advances

- Explore Reliable Financing Options For Your Small Business

Key takeaways

| Point | Details |

|---|---|

| High cost structure | MCAs can carry effective APRs from 50% to over 300%, far exceeding traditional loan rates. |

| Not a loan | MCAs are structured as sales of future receivables, avoiding many lending regulations. |

| Cash flow pressure | Daily or weekly repayments based on sales percentages can strain your operating budget. |

| Default risks | Aggressive collection terms and debt accumulation can create financial traps for struggling businesses. |

| Careful evaluation needed | Understanding true costs and exploring alternatives is essential before signing any MCA agreement. |

What is a merchant cash advance and how does it work?

A merchant cash advance provides immediate capital by purchasing a portion of your future credit card sales or receivables. Unlike traditional loans, MCAs are structured as sales rather than debt instruments, which allows providers to sidestep many banking regulations. This distinction matters because it affects your rights, costs, and legal protections.

Here's how the process typically works:

- You receive a lump sum payment upfront, usually ranging from $5,000 to $500,000

- The provider collects repayment through a fixed percentage of your daily or weekly card sales

- Repayment continues until you've paid back the advance plus fees

- The total amount owed is calculated using a factor rate, not an interest rate

Factor rates usually range from 1.1 to 1.5, meaning you repay $1.10 to $1.50 for every dollar advanced. A $50,000 advance with a 1.3 factor rate costs you $65,000 total. The provider deducts payments automatically from your merchant account or bank account, often daily. This automatic collection happens whether your business is profitable that day or not.

The speed and accessibility make MCAs attractive when traditional lenders say no. Most providers approve applications within 24 to 48 hours, requiring minimal documentation compared to bank loans. You don't need perfect credit, extensive collateral, or years of financial statements. If your business processes card payments regularly, you likely qualify.

Pro Tip: Calculate the true annual percentage rate before signing. Divide the total fee by the advance amount, then multiply by 365 and divide by the estimated repayment period in days. This reveals the actual cost you're paying.

The repayment structure creates unique cash flow dynamics. During strong sales periods, you pay more. During slow periods, you pay less. This flexibility sounds appealing, but it also means the MCA provider gets paid first, before you cover rent, payroll, or inventory. Many business owners discover too late that this arrangement leaves insufficient funds for essential operations.

The hidden costs and financial risks of merchant cash advances

The factor rate system deliberately obscures the true cost of MCAs. When you see a 1.3 factor rate, it looks reasonable compared to a 30% interest rate. The reality is far different. MCAs typically carry APRs between 50% and 350%, making them among the most expensive financing options available in 2026.

Consider a real example. You receive $30,000 with a 1.4 factor rate, repaying $42,000 total over six months. That $12,000 fee represents a 40% return over six months, which translates to roughly 80% APR. If repayment happens faster due to strong sales, the APR climbs even higher. A three-month repayment period on the same terms pushes the APR above 160%.

Daily or weekly payment schedules create relentless pressure on your cash flow:

- Payments hit your account before you can allocate funds to other expenses

- Seasonal businesses face the same payment obligations during slow periods

- Multiple MCAs compound the drain, with some businesses paying 30% to 50% of daily revenue to MCA providers

- Operating capital shrinks, forcing difficult choices between paying suppliers or meeting payroll

The debt spiral risk is real and devastating. When daily payments consume too much revenue, businesses often take out additional MCAs to cover the shortfall. Each new advance adds another daily deduction, accelerating the cash flow crisis. This cycle continues until the business collapses or seeks bankruptcy protection.

"Many small businesses enter MCA agreements without fully understanding the repayment obligations and financial strain they create. The lack of regulatory oversight allows some providers to impose terms that would be illegal for traditional lenders."

Predatory practices flourish in the loosely regulated MCA industry. Some providers include confession of judgment clauses, allowing them to obtain court judgments against you without a trial. Others charge stacking fees if you take multiple advances or impose harsh penalties for early repayment. The absence of truth-in-lending requirements means providers don't have to disclose APR or use standardized cost metrics.

Pro Tip: Review financing mistakes to avoid before committing to any high-cost financing. Understanding common pitfalls helps you recognize warning signs in MCA agreements.

Certain business situations amplify MCA risks. Restaurants, retail stores, and seasonal businesses with fluctuating revenue face particular danger. A strong month might suggest you can handle the payments, but three slow months can quickly deplete reserves. Before signing, stress test your cash flow projections against worst-case scenarios, not average performance.

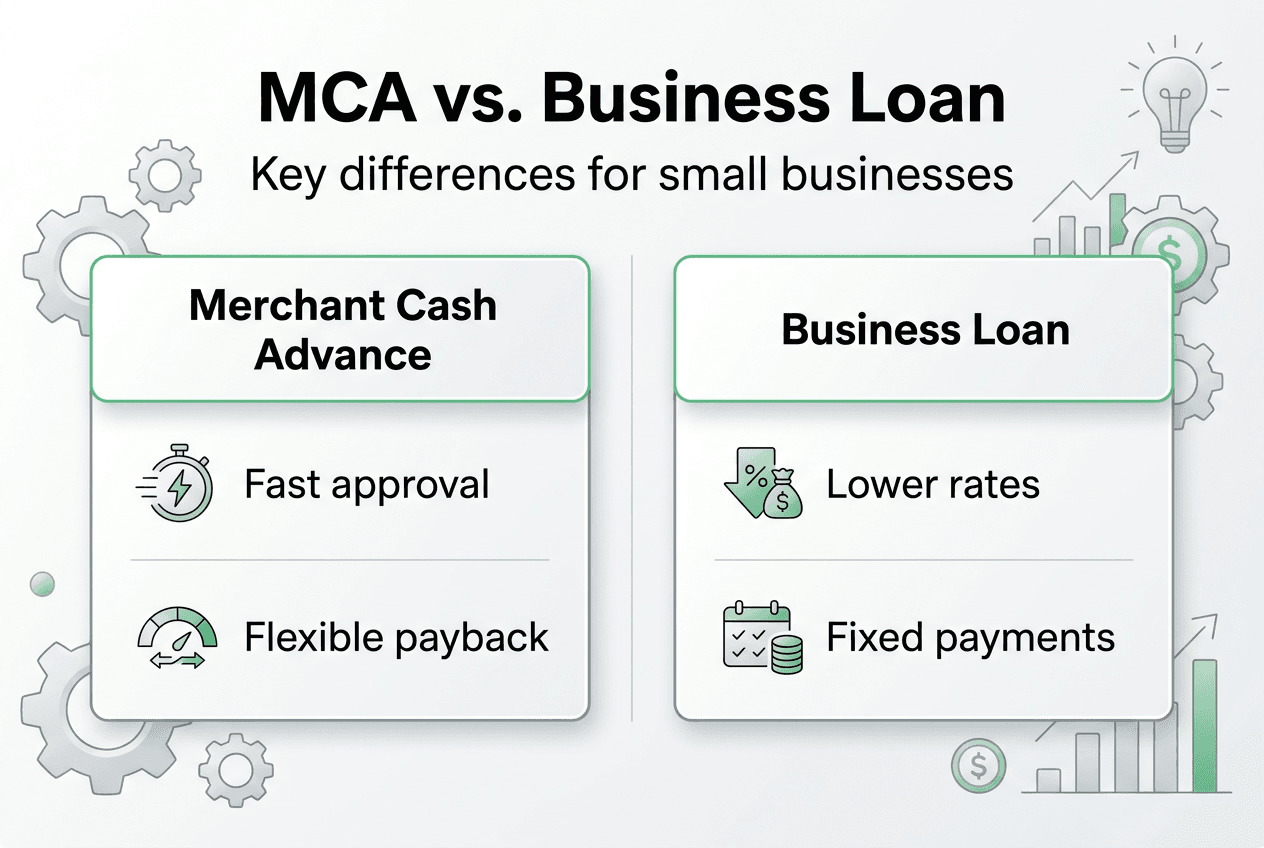

Comparing merchant cash advances with traditional business loans

The fundamental difference between MCAs and loans lies in their legal structure and regulatory oversight. MCAs bypass many regulations that govern traditional lending, including interest rate caps and disclosure requirements. This distinction creates stark contrasts in cost, terms, and borrower protections.

| Feature | Merchant Cash Advance | Traditional Business Loan |

|---|---|---|

| Approval speed | 24 to 48 hours | 2 to 8 weeks |

| Cost (APR) | 50% to 350%+ | 6% to 30% |

| Repayment structure | Percentage of daily sales | Fixed monthly payments |

| Credit requirements | Minimal | Moderate to strong |

| Regulatory oversight | Limited | Extensive |

| Early repayment | Often penalized | Usually allowed |

Traditional loans offer predictable monthly payments that make budgeting straightforward. You know exactly what you owe and when. MCAs tie payments to revenue, which sounds flexible but makes financial planning difficult. You can't predict exact payment amounts or the final repayment date.

The cost difference deserves emphasis. A $50,000 business loan at 12% APR over three years costs roughly $9,700 in interest. The same amount as an MCA with a 1.35 factor rate costs $17,500 in fees, and that's before considering the compressed repayment timeline that drives the effective APR much higher.

Key factors to consider when choosing between options:

- Time sensitivity: Do you need funds within days, or can you wait weeks?

- Cost tolerance: Can your business margins support APRs above 50%?

- Credit profile: Will traditional lenders approve your application?

- Cash flow stability: Can you handle fixed payments or do you need flexibility?

- Long-term impact: How will this financing affect your business 12 to 24 months from now?

Traditional lenders require more documentation, including tax returns, financial statements, and business plans. The approval process involves credit checks, collateral evaluation, and sometimes personal guarantees. This scrutiny protects both parties by ensuring you can realistically repay the debt. MCA providers skip most of this analysis, focusing primarily on your card sales volume.

For businesses with decent credit and time to spare, exploring different types of small business loans usually yields better terms than MCAs. SBA loans, equipment financing, and business lines of credit all offer lower costs and more favorable structures. Even alternative lenders with faster approval processes typically charge less than MCA providers.

The MCA versus business loan decision often comes down to urgency versus cost. If you're facing an immediate crisis like equipment failure or a time-sensitive opportunity, an MCA might be your only option. For planned expansions or less urgent needs, the extra time required for traditional financing saves substantial money.

Best practices and legal considerations when using merchant cash advances

Protecting your business starts with thorough due diligence before signing any MCA agreement. Request complete disclosure of all costs, including the factor rate, origination fees, and any additional charges. Calculate the effective APR yourself using multiple repayment scenarios to understand the true cost.

Essential steps for evaluating MCA offers:

- Compare at least three providers to understand market rates and terms

- Review the entire contract with a lawyer familiar with commercial financing

- Verify the provider's reputation through online reviews and Better Business Bureau ratings

- Confirm exact repayment percentages and how they're calculated from your sales

- Identify any confession of judgment clauses or unusual legal provisions

Cash flow projections become critical when considering MCAs. Model your business finances with the MCA payment deducted daily or weekly. Include seasonal variations and potential downturns. If the projections show tight margins even in good months, the MCA will likely create problems. Understanding key considerations before signing helps you avoid agreements that seem manageable on paper but prove crushing in practice.

Legal protections for MCA borrowers remain limited but are evolving in 2026. Some states have begun regulating MCAs more strictly, requiring clearer disclosures or capping effective interest rates. Understanding your legal rights and remedies before problems arise gives you options if disputes occur. Consult with a business attorney in your jurisdiction to understand what protections apply.

Pro Tip: Maintain detailed records of all payments, correspondence, and account statements related to your MCA. If disputes arise about payment amounts or contract terms, thorough documentation strengthens your position significantly.

Alternatives to MCAs often provide better solutions:

- Business lines of credit offer flexible access to funds with lower costs

- Invoice factoring converts receivables to cash without the high MCA fees

- Equipment financing spreads costs over time while acquiring necessary assets

- Peer-to-peer lending platforms sometimes approve businesses traditional banks reject

- Revenue-based financing provides similar flexibility with more transparent pricing

If you're already in an MCA and struggling with payments, don't ignore the problem. Contact the provider immediately to discuss options. Some will restructure terms or temporarily reduce payment percentages. Defaulting triggers aggressive collection actions and potential legal consequences. Seeking help from a business financial advisor or attorney early provides more options than waiting until you're in crisis.

The MCA workflow and step-by-step guide at Capital for Business walks you through the entire process, helping you understand what to expect at each stage. This transparency allows you to make informed decisions rather than rushing into agreements you don't fully understand.

Explore reliable financing options for your small business

Navigating small business financing requires understanding all your options, from merchant cash advances to traditional loans. Capital for Business has supported small business owners since 2009, offering transparent guidance and access to multiple financing solutions. Whether you need quick funding through a merchant cash advance or prefer exploring different types of easy small business loans, we help you compare terms and find the right fit for your situation.

Our team understands that banks and credit unions don't always meet the needs of growing businesses. We work with business owners across hundreds of industries, providing working capital, equipment financing, and credit solutions when you need them most. Visit our funding solutions page to explore options tailored to your business goals and cash flow requirements.

FAQ

What is the difference between a merchant cash advance and a business loan?

A merchant cash advance purchases your future receivables and repays through a percentage of daily sales, while a business loan provides debt capital repaid through fixed installments. MCAs avoid lending regulations because they're structured as sales, not loans. This means different legal protections, typically higher costs, and flexible repayment tied to your revenue. Traditional loans offer regulated interest rates, predictable payments, and stronger borrower protections under lending laws.

Are merchant cash advances a good option for managing cash flow?

MCAs provide immediate capital but often worsen cash flow problems due to high costs and aggressive repayment schedules. The daily or weekly deductions can consume 10% to 30% of your revenue, leaving less for operations. They work best for short-term emergencies or time-sensitive opportunities where the return exceeds the high cost. For ongoing cash flow management, using merchant cash advances strategically requires careful planning to avoid creating bigger financial problems.

How quickly can I get funding through a merchant cash advance?

Most MCA providers approve applications and fund accounts within 24 to 48 hours. Some offer same-day funding if you apply early and provide required documentation immediately. The speed comes from minimal underwriting focused on your card sales volume rather than extensive financial analysis. You'll typically need recent bank statements, processing statements showing card sales, and basic business information. This rapid access makes MCAs attractive for urgent needs but shouldn't rush you into accepting unfavorable terms.

What legal protections do small businesses have against unfair MCA terms?

Legal protections vary by jurisdiction but remain limited compared to traditional lending. Businesses have evolving legal remedies against predatory MCA practices, including challenges to confession of judgment clauses and unconscionable terms. Some states now require clearer disclosures or regulate collection practices. Consulting a business attorney helps you understand rights specific to your location and situation. Document all interactions and contract terms carefully, as this evidence supports any legal action if disputes arise. Review common financing mistakes to recognize warning signs before signing.

Recommended

- Using Merchant Cash Advance for Growth | Capital For Business

- Merchant Cash Advance - up to $500k | Capital For Business

- Merchant Cash Advance Workflow 2026: Step-by-Step Funding

- How a Merchant Cash Advance streamlines your operations

- DO YOU NEED CASH FOR YOUR BUSINESS NOW? @RetailFinanceNI - LoveBelfast

- Smart Financial Decisions for Your Business