TL;DR:

- Construction financing provides the capital necessary to start and complete projects while shaping risk and contract terms.

- Effective management of draw schedules and capital structures prevents cash flow gaps that can delay or derail projects.

Financing in construction is defined as the structured capital that enables project managers and contractors to initiate, sustain, and complete builds without exhausting their own cash reserves. The role of financing in construction goes far beyond simply borrowing money. It determines how risk is shared among stakeholders, how contracts are written, and whether a project survives a cash flow gap between a draw disbursement and a subcontractor payment. Understanding construction project funding at this level separates contractors who consistently deliver on time from those who stall mid-project. The capital stack, the draw schedule, and the lender relationship all shape project outcomes before a single foundation is poured.

What are the primary financing options for construction projects?

Construction project funding is built on a layered capital structure, commonly called a capital stack. Each layer carries a different cost and level of risk. Senior debt sits at the lowest cost and risk, followed by mezzanine debt, and then equity at the highest cost and risk. Knowing where your project sits in that stack tells you exactly how much your financing will cost and what lenders will demand in return.

Commercial construction loans are the most common senior debt product. Commercial loans typically cover 60–75% of total project costs, funded through monthly draws verified by project monitors. That means you are responsible for sourcing the remaining 25–40% through equity contributions or subordinate debt.

The main financing options for construction break down as follows:

- Senior construction loans: Short-term, typically 12–36 months, covering the majority of hard costs. These require strong credit, project documentation, and often a personal guarantee.

- Mezzanine debt: Fills the gap between senior debt and equity. It carries higher interest rates and may include equity participation rights for the lender.

- Equity financing: Capital contributed by project owners or investors. It carries the highest cost in terms of return expectations but does not require debt service during construction.

- Business lines of credit: Revolving credit facilities that contractors use to cover payroll, materials, and subcontractor payments between draw disbursements.

- Nonbank loans and private debt funds: Faster to close than bank loans, with more flexible underwriting, but at a meaningfully higher interest rate.

Alternative financing sources, including equity crowdfunding platforms, have also grown as a channel for smaller construction ventures. Platforms that specialize in equity crowdfunding for projects give developers access to a broader pool of investors outside traditional bank relationships.

Pro Tip: Map your full capital stack before approaching any lender. Lenders want to see that every dollar of project cost is accounted for, including your equity contribution, before they commit senior debt.

The right mix of financing options for construction depends on project size, timeline, and your firm's credit profile. A small commercial renovation may need only a business line of credit. A ground-up multifamily development will require a full capital stack with senior debt, mezzanine, and equity working together.

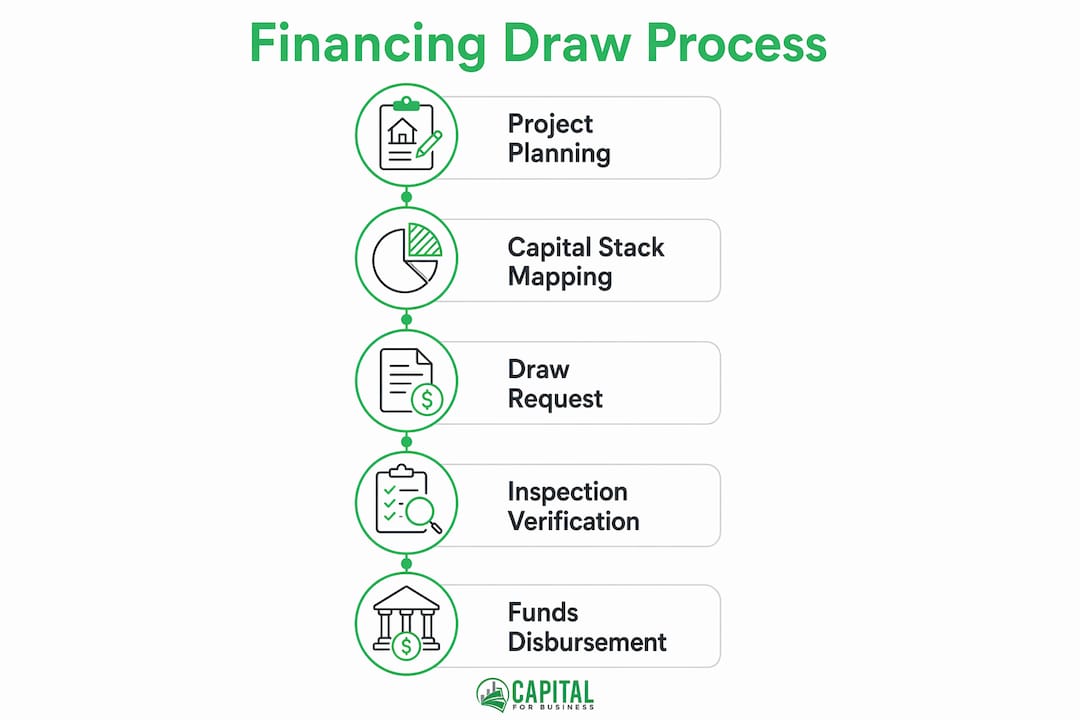

How does the financing draw and disbursement process work?

The draw process is the mechanism that releases loan funds to contractors in stages as construction progresses. Understanding it prevents the cash flow problems that derail otherwise well-funded projects.

Here is how a standard draw process works:

- Submit a draw request. The contractor submits a draw request tied to a detailed schedule of values, showing the percentage of work completed for each line item.

- Third-party inspection. An independent inspector or project monitor visits the site to verify that the claimed work is actually complete. Draw disbursements require verification against an approved schedule of values by third-party inspectors before funds are released.

- Lender review and approval. The lender reviews the inspector's report and approves the draw amount. This process typically takes 5–15 business days.

- Funds disbursement. Approved funds are wired to the borrower or placed in a controlled disbursement account.

- Interest accrual on drawn funds only. Interest on construction loans is paid monthly only on funds drawn to date, often from a pre-funded interest reserve. This keeps your carrying cost low in the early stages of a project when draws are small.

The critical problem contractors face is the timing lag. You pay subcontractors and suppliers before the draw is approved and funded. That gap can run two to four weeks, and it creates real cash pressure on your operating account.

Pro Tip: Build a 30-day working capital buffer into your project budget before construction starts. This buffer covers payroll and material costs while your draw request moves through the inspection and approval cycle.

Coordinating draw requests with project milestones is not optional. If your draw request does not align with verifiable progress, the inspector will reduce the approved amount. That shortfall comes directly out of your operating cash. Contractors who treat the draw schedule as a financial planning tool, not just a paperwork requirement, consistently avoid the cash crunches that slow projects down.

How does financing influence risk allocation and contract negotiations?

Financing does not just fund a project. It shapes every major contract provision that governs how risk is distributed among the developer, contractor, engineer, and lender.

Project financing focuses on using future project revenues and contracts to secure loans rather than relying on the sponsor's credit alone. That structure forces lenders to care deeply about project-level risk, which flows directly into the contracts you sign.

When a lender's capital is at stake, they require the project to meet what is called "bankability" standards. Those standards show up in construction contracts in specific ways:

- Completion guarantees: Lenders often require the developer to guarantee project completion, which the developer then passes down to the general contractor through the construction agreement.

- Liquidated damages clauses: Project financing contracts include rigorous provisions on schedule, testing, and damages to protect lender interests. Liquidated damages for schedule delays are a direct result of lender requirements.

- Performance testing requirements: For infrastructure and energy projects, lenders require performance tests before final loan disbursement. The contractor must meet those tests or face financial penalties.

- Step-in rights: Lenders may negotiate the right to step in and take over project management if the contractor defaults. This provision appears in the construction contract as a direct result of the financing structure.

"Financing is not just liquidity. It is a key driver of risk allocation, shaping contract specifics among all stakeholders. The contractor who understands the lender's requirements before signing a construction agreement holds a significant negotiating advantage."

Project managers who understand the importance of construction financing at this level negotiate better contracts. They know which provisions come from lender requirements and which are developer preferences. That knowledge creates room to push back on terms that transfer excessive risk to the contractor without corresponding compensation.

What trends are shaping construction financing in 2026?

The lending market for construction has shifted significantly. Traditional banks have tightened underwriting standards, and nonbank lenders are filling the gaps with faster approvals and more flexible structures, but at a higher cost.

60% of firms rate traditional bank financing as very inaccessible due to complex requirements and rigid cash flow alignment standards. That figure reflects a structural reality: banks require extensive documentation, long approval timelines, and borrower profiles that many growing construction firms cannot meet.

| Financing source | Approval speed | Flexibility | Typical cost | Best suited for |

|---|---|---|---|---|

| Traditional bank | 60–90 days | Low | Lowest | Established firms with strong credit |

| Credit union | 45–75 days | Moderate | Low | Small to mid-size contractors |

| Nonbank lender | 5–15 days | High | Higher | Firms needing speed or with complex profiles |

| Private debt fund | 10–30 days | High | Highest | Large or complex projects |

| Business line of credit | 3–10 days | Very high | Moderate | Ongoing working capital needs |

Structural changes in lending markets have increased reliance on nonbank debt funds and finance companies. This shift raises project funding costs and reduces the regulatory transparency that comes with bank lending. Contractors need to read nonbank loan agreements carefully, paying particular attention to prepayment penalties, draw control provisions, and default triggers.

The practical response for contractors is to diversify their financing relationships. Relying on a single lender for all project capital creates concentration risk. Firms that maintain a bank relationship for lower-cost senior debt and a nonbank relationship for fast-access working capital are better positioned to keep projects moving regardless of market conditions.

How can project managers control budgets through effective financing management?

Budget control in construction starts with financing management, not cost tracking. The two are inseparable. A project that runs out of accessible capital stops, regardless of how well costs are managed on paper.

These steps give project managers direct control over financing costs and cash flow:

- Integrate your financing plan into the project schedule from day one. Map each draw request date to a project milestone. Know exactly when funds will arrive and what expenses fall due in the same window.

- Use a working capital line of credit to bridge draw timing gaps. Aligning financing plans tightly with project milestones prevents cash flow gaps. A working capital loan covers payroll and materials in the weeks between draw requests and disbursements.

- Monitor interest expense monthly. Interest accrues only on drawn funds, so drawing more than you need at any given stage increases your financing cost unnecessarily. Draw what you need, when you need it.

- Maintain a contingency reserve separate from your draw schedule. Lenders build contingency into loan budgets, but that contingency is not always accessible quickly. Keep a separate liquid reserve for unexpected costs that cannot wait for a draw cycle.

- Review your financing structure at each project phase. The financing that works for the foundation phase may not be the right tool for the fit-out phase. Contractors who manage cash flow proactively adjust their financing mix as project needs change.

The impact of financing on construction projects is most visible in the cash flow statement, not the income statement. A project can show a healthy projected profit and still fail if the contractor cannot cover expenses during the gap between work completed and payment received. Financing management is the discipline that closes that gap.

Pro Tip: Ask your lender for a controlled disbursement account that releases funds directly to subcontractors and suppliers. This eliminates the float period between your draw receipt and vendor payment, and it often satisfies lender requirements for funds control.

Contractors who treat financing as a project management tool, not just a funding source, consistently deliver projects on budget. They know their draw schedule as well as they know their construction schedule. They monitor interest costs the same way they monitor labor costs. That level of attention to financing is what separates firms that grow from firms that stall.

Key Takeaways

Effective construction financing requires aligning capital structure, draw timing, and risk allocation before a project breaks ground, not after problems arise.

| Point | Details |

|---|---|

| Capital stack structure | Senior debt, mezzanine, and equity each carry different costs; know your stack before approaching lenders. |

| Draw timing management | Contractors must bridge the gap between work completed and draw disbursement using working capital tools. |

| Financing shapes contracts | Lender requirements drive liquidated damages, completion guarantees, and performance testing provisions in construction agreements. |

| Nonbank lenders fill gaps | Nonbank lenders offer faster approvals but higher costs; diversifying lender relationships reduces concentration risk. |

| Budget control starts with financing | Integrating the financing plan into the project schedule is the most direct way to prevent cash flow gaps and cost overruns. |

What I've learned about financing after years in construction lending

Most contractors treat financing as something they figure out once and then forget. That approach costs them money on every project. The draw process, the capital stack, the lender relationship: these are not one-time decisions. They are ongoing management responsibilities that affect every week of a project's life.

The contractors who consistently deliver on budget are the ones who understand that project financing is a risk management tool, not just a funding mechanism. They read their loan agreements the way they read their construction contracts. They know exactly what triggers a default, what their lender's inspection rights are, and how much contingency they can access without a formal draw request.

The shift toward nonbank lenders is real, and it is not going away. Faster approvals and flexible structures are genuinely useful for contractors who need capital quickly. But the higher cost and lower regulatory oversight require more discipline on the borrower's side. I have seen firms take nonbank loans without fully understanding the prepayment terms, then get hit with penalties when they refinanced at project completion.

My honest recommendation: build your financing knowledge the same way you build your technical expertise. Understand the capital stack. Know your draw schedule cold. Read every covenant in your loan agreement. Contractors who do this do not just survive financing challenges. They use financing as a competitive advantage, moving faster and taking on larger projects than their less-informed competitors.

— Capital

Capitalforbusiness offers construction financing built for real projects

Construction projects move fast, and your financing needs to keep pace. Capitalforbusiness has worked with contractors and project managers across hundreds of industries since 2009, providing small business loans and working capital solutions that fit the realities of construction cash flow.

Whether you need a working capital line to bridge draw timing gaps, equipment financing for a new project, or a fast-approval loan to cover subcontractor payments, Capitalforbusiness delivers funding when banks move too slowly. Explore construction funding options up to $500,000 with terms built around how construction projects actually work. Apply today and get a decision without the 90-day bank timeline.

FAQ

What is the role of financing in construction?

Financing in construction provides the capital required to start, sustain, and complete projects. It also shapes risk allocation, contract terms, and cash flow management across every project phase.

How do construction loan draws work?

Lenders release funds in stages through a draw process, where a third-party inspector verifies completed work against a schedule of values before each disbursement. Contractors must cover expenses during the lag between work completion and draw approval.

What is a construction capital stack?

A capital stack is the layered structure of funding sources for a project, typically combining senior debt, mezzanine debt, and equity. Senior debt carries the lowest cost, while equity carries the highest expected return.

Why are nonbank lenders growing in construction financing?

Traditional bank financing is rated as very inaccessible by a majority of construction firms due to complex requirements and rigid underwriting. Nonbank lenders fill that gap with faster approvals and flexible terms, though at higher interest rates.

How can contractors manage cash flow between draw disbursements?

Contractors use working capital lines of credit or short-term business loans to cover payroll and material costs while draw requests move through the inspection and approval cycle. Aligning draw request dates with project milestones reduces the size and frequency of those gaps.