TL;DR:

- Business term loans provide a fixed lump sum repaid over a set schedule, aiding growth projects.

- There are various options including bank, online, and SBA loans, each with different costs and requirements.

- Suitable for specific investments like equipment or expansion, but not ideal for fluctuating operational expenses.

Half of small businesses use term loans regularly, yet many owners assume this type of financing is reserved for large corporations or businesses with perfect credit. That assumption leaves real growth opportunities on the table. A business term loan is one of the most straightforward funding tools available: you receive a lump sum, repay it on a fixed schedule, and know exactly when you'll be done. This guide covers everything you need to know, from how term loans work and what they cost, to how to qualify and when to use one strategically. Whether you're planning an expansion, buying equipment, or shoring up working capital, understanding term loans gives you a clear advantage.

Table of Contents

- What is a term loan for business and how does it work?

- Term loan types: Bank, online, and SBA options explained

- Qualifying for a term loan: Requirements and how to improve your chances

- Costs, terms, and repayment: What to expect (and avoid surprises)

- When (and when not) to use a term loan for business growth

- What most business owners get wrong about term loans (and how to get it right)

- Explore business loan solutions tailored to your needs

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Understand your options | There are multiple types of business term loans with different pros, cons, and qualification criteria. |

| Compare true costs | Look closely at interest rates, fees, and prepayment penalties before agreeing to a loan. |

| Qualify strategically | Improve your approval odds by prepping documentation and understanding what lenders want. |

| Use loans wisely | Match loan type and structure to your business needs—avoid borrowing more than necessary. |

| Plan for repayment | Predictable payments are valuable, but always have a strategy for using the funds and repaying the loan. |

What is a term loan for business and how does it work?

A business term loan is a fixed amount of money borrowed from a lender and repaid over a set period through regular installments. Think of it as the opposite of a revolving credit line. You get the full amount upfront, and your repayment schedule is locked in from day one.

According to business development terminology, a term loan is one of the foundational instruments in business finance. What makes it distinct is the structure: you know your payment amount, your interest rate (fixed or variable), and your payoff date before you sign.

How repayment works

A business term loan provides a lump sum repaid over a fixed period with interest, typically via amortized payments where early payments cover more interest and later payments cover more principal. This is called amortization. In the early months of your loan, a larger share of each payment goes toward interest. As time passes, more of each payment chips away at the principal balance.

Here's a simplified example: if you borrow $100,000 at 8% APR over five years, your monthly payment stays constant, but the split between interest and principal shifts every month. By year four, most of each payment is reducing your balance directly.

Key components of a business term loan:

- Loan amount: Typically ranges from $5,000 to $5 million

- Repayment term: Usually 6 months to 7 years, depending on lender and loan type

- Interest rate: Fixed or variable, ranging from about 6% to 99% APR

- Payment frequency: Monthly is standard; some lenders require weekly or daily payments

- Collateral: May or may not be required depending on loan size and lender

"Predictable payments are one of the biggest advantages of a term loan. When you know exactly what you owe each month, budgeting becomes significantly easier."

One common point of confusion is the difference between a term loan and a business line of credit. A line of credit lets you borrow, repay, and borrow again up to a set limit. A term loan is a one-time disbursement. If you're planning using a loan to grow your business through a specific project or purchase, a term loan is usually the better fit.

For the latest updates on how banks and government-backed programs are structuring these products, reviewing SBA and bank loan updates can help you stay current.

Pro Tip: Ask your lender for a full amortization schedule before signing. This shows you exactly how much interest you'll pay over the life of the loan and helps you compare offers side by side.

Term loan types: Bank, online, and SBA options explained

With a firm understanding of what a term loan is, it's crucial to examine which type best fits your business's needs. The three main categories are traditional bank loans, online lender loans, and SBA-backed loans. Each comes with different rates, timelines, and requirements.

Comparison of term loan types

| Feature | Bank loans | Online lenders | SBA loans |

|---|---|---|---|

| Interest rate | 6.3% to 11.5% | 14% to 99% | Prime + 2.25% to 4.75% |

| Approval time | Weeks to months | 1 to 5 business days | Several weeks to months |

| Loan amount | Up to $1M+ | $5,000 to $500K | Up to $5M |

| Term length | 1 to 10 years | 3 months to 5 years | Up to 25 years |

| Credit requirement | 680+ FICO | 550+ FICO | 650+ FICO |

| Documentation | Extensive | Moderate | Very extensive |

Bank term loans offer the lowest rates. Bank term loans average 6.3% to 11.5% based on Q3 2025 Federal Reserve data. However, banks are the most selective. They want established businesses with strong financials, high credit scores, and often require collateral.

Online lenders move fast. Approval can come within 24 hours, and funding often follows within days. The tradeoff is cost: online lender rates can reach up to 99% APR. That's a significant expense, so online loans make the most sense when you need speed and have a clear, short-term return on investment.

SBA loans are government-backed and designed to support small businesses that might not qualify for conventional bank financing. SBA 7(a) term loans offer up to $5 million, with terms up to 10 years for working capital and up to 25 years for real estate, at variable rates of Prime plus 2.25% to 4.75%. The catch is paperwork. SBA applications are thorough and time-consuming, but the terms are hard to beat.

Which type is right for you?

- Strong credit, established business: Bank loan or SBA loan

- Need funds quickly: Online lender

- Large loan with long repayment window: SBA loan

- Newer business or lower credit score: Online lender or alternative lender

For more detail on government-backed options, reviewing SBA loan details gives you a practical breakdown of current programs.

Pro Tip: Don't apply to just one lender. If your business profile is strong, you have negotiating power. Getting multiple offers lets you compare total costs, not just interest rates, and potentially negotiate better terms.

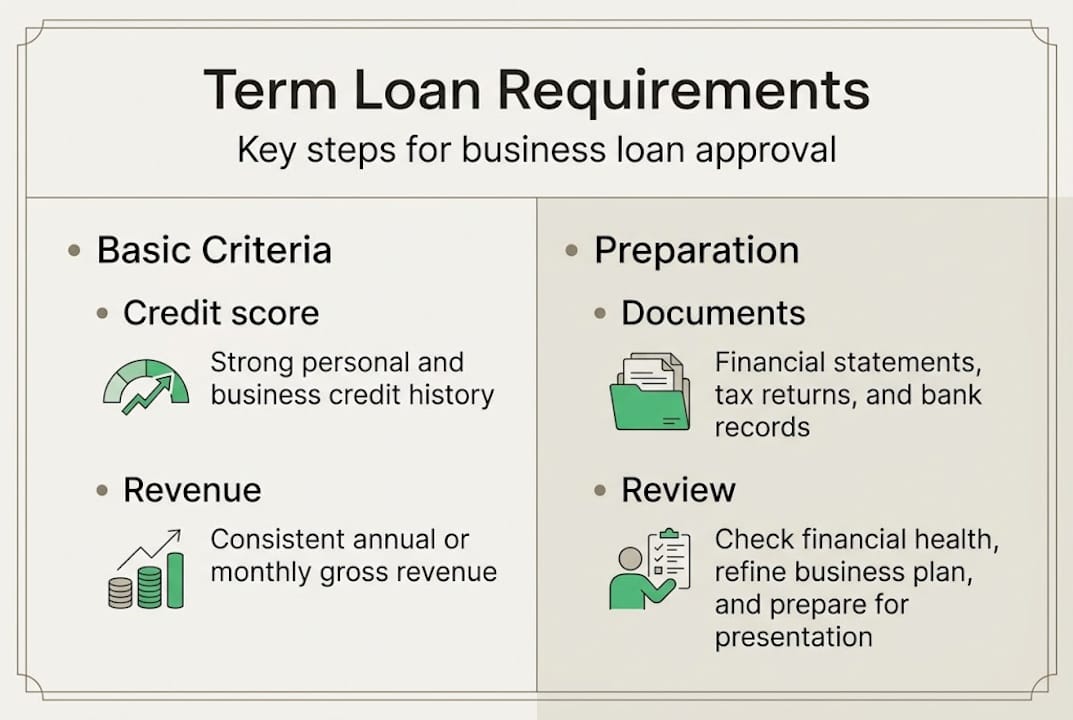

Qualifying for a term loan: Requirements and how to improve your chances

Once you've selected a loan type, the next crucial step is knowing how to qualify and improve your approval odds. Lenders evaluate several factors before approving a term loan, and understanding what they look for helps you prepare a stronger application.

Standard eligibility requirements:

- Time in business: Most lenders require at least 2 years of operating history. Some online lenders will consider businesses as young as 6 months.

- Annual revenue: A minimum of $100,000 in annual revenue is the standard benchmark for most lenders.

- Credit score: A 680+ FICO score is preferred by banks and SBA lenders. Online lenders may approve scores as low as 550.

- Business plan: Lenders want to see how you plan to use the funds and how repayment fits your cash flow.

- Financial documents: Expect to provide tax returns (2 to 3 years), bank statements, profit and loss statements, and a balance sheet.

- Debt-to-income ratio: Lenders assess your existing debt load relative to revenue to ensure you can handle additional payments.

What to expect from the approval process:

Approved borrowers typically receive about 75% of the requested loan amount. Short-term loans see the highest approval rates, while SBA and medium-term loans tend to result in the largest approved amounts. This means it's worth requesting slightly more than your minimum need, within reason.

If your credit score is below 680:

Don't assume you're out of options. Alternative lenders and online platforms often prioritize revenue and cash flow over credit scores. Explore bad credit loan options or read the guide to bad credit business loans to understand what's available. Some lenders also use bank statement analysis instead of traditional credit checks, which can work in your favor if your revenue is consistent.

| Credit score range | Best lender option | Typical APR range |

|---|---|---|

| 720+ | Bank or SBA | 6% to 12% |

| 680 to 719 | Bank, SBA, or online | 8% to 25% |

| 600 to 679 | Online or alternative lenders | 20% to 60% |

| Below 600 | Specialized alternative lenders | 40% to 99% |

Before submitting any application, review your credit report for errors and resolve any outstanding issues. Incomplete financials or unexplained gaps in revenue are red flags that can delay or derail approval. Reviewing business loan considerations before you apply can help you spot and address those issues early.

Pro Tip: Prepare your financial documents at least 30 days before applying. Lenders move faster when your paperwork is clean and complete, and you'll be in a stronger position to respond to any follow-up requests quickly.

Costs, terms, and repayment: What to expect (and avoid surprises)

Understanding qualifying is only part of the equation. Next comes understanding what you'll pay and how to protect your business's finances over the life of the loan.

Breaking down the real cost of a term loan:

Typical loan ranges run from $5,000 to $5 million, with terms from 6 months to 7 years and APRs from 6% to 99% depending on the lender. But the interest rate is only part of the picture. Here's what else affects your total cost:

- Origination fee: Usually 1% to 5% of the loan amount, charged upfront

- Application fee: Some lenders charge a flat fee just to process your application

- Late payment fee: Typically a percentage of the missed payment or a flat dollar amount

- Prepayment penalty: A charge for paying off your loan ahead of schedule

- Annual fee: Less common but present with some lenders

Understanding amortization in practice:

On a $50,000 loan at 10% APR over 3 years, your monthly payment would be approximately $1,613. In month one, roughly $417 goes to interest and $1,196 to principal. By month 30, only about $40 goes to interest. The total interest paid over the full term would be around $5,067. That number changes dramatically with a higher rate or longer term.

"Always calculate the total cost of the loan, not just the monthly payment. A lower monthly payment with a longer term often means you pay significantly more overall."

Prepayment penalties: Know before you sign

Prepayment penalties are common on long-term loans, typically ranging from 1% to 5% of the remaining balance. For SBA loans, prepayment penalties only apply to loans with terms of 15 years or more, and only during the first three years. If you plan to pay off your loan early, this clause can cost you thousands.

To minimize total interest paid, consider grow your business with a loan strategies that align your loan term with the useful life of whatever you're financing. Financing a piece of equipment that will last 5 years on a 7-year loan means you're paying for something past its peak value.

For guidance on negotiating loan terms before you sign, comparing multiple offers is the single most effective strategy.

Pro Tip: Always ask your lender directly: "Is there a prepayment penalty, and how is it calculated?" Get the answer in writing. This one question can save you thousands if your business grows faster than expected.

When (and when not) to use a term loan for business growth

Knowing costs and terms, the final step is making sure a term loan aligns with your unique business goals and situation. Not every financial need calls for a term loan, and using the wrong tool can create unnecessary strain.

When a term loan makes strong sense:

Term loans are ideal for one-time, defined needs with predictable returns. Common use cases include:

- Equipment purchases: Buying machinery, vehicles, or technology that will generate revenue over time

- Business expansion: Opening a new location, renovating an existing space, or entering a new market

- Inventory bulk purchases: Securing a large order at a discount when you have a confirmed buyer

- Hiring and training: Funding a significant staffing expansion tied to a new contract or project

- Debt consolidation: Replacing multiple high-rate obligations with one lower-rate term loan

For growth strategies for SMEs, term loans work best when the investment has a clear, measurable return and a defined timeline.

When a term loan is the wrong choice:

If your cash flow is seasonal or unpredictable, locking into fixed monthly payments can create pressure during slow periods. For ongoing operational expenses, payroll gaps, or fluctuating inventory needs, a business line of credit is a better fit. Understanding the advantages and disadvantages of unsecured business line of credit helps you see where each product fits.

Also avoid using a term loan for expenses that don't generate a return. Funding a marketing experiment or covering a short-term cash gap with a multi-year loan means you're paying interest long after the need has passed.

Using both tools together:

Many successful small businesses use a term loan for capital investments and a line of credit for day-to-day flexibility. This combination gives you stability and agility. Explore business line of credit options and what is a business line of credit to understand how to structure both products effectively.

Pro Tip: Before applying for a term loan, map out exactly how the funds will generate revenue or reduce costs. If you can't build a basic projection showing how the loan pays for itself, reconsider the timing.

What most business owners get wrong about term loans (and how to get it right)

After working with small business owners across hundreds of industries since 2009, we've seen the same mistakes repeat. The most common one: borrowing the maximum amount you qualify for simply because you can.

Lenders approve you based on their risk tolerance, not your business's actual capacity. Borrowing more than your cash flow can comfortably support creates stress during slow months, even when the business is otherwise healthy. The most successful borrowers we've worked with match the loan structure to their cash flow cycle, not the other way around.

Another overlooked area is negotiation. Most business owners focus entirely on the interest rate, but the real savings often come from negotiating origination fees, repayment flexibility, or prepayment terms. A lender who won't budge on rate may still offer a fee waiver or a grace period that saves you more in practice.

Here's the contrarian view: sometimes the smartest move is not taking the loan right now. If your business is six months away from stronger revenue or a better credit profile, waiting can unlock significantly better terms. A smaller loan used well and repaid cleanly also builds your lending history, which positions you for larger capital at better rates later.

Reviewing borrowing considerations before you commit is one of the most practical steps you can take. The goal isn't just approval. It's using capital in a way that genuinely moves your business forward.

Explore business loan solutions tailored to your needs

Understanding term loans is the first step. Taking action is what drives real growth. Whether you're ready to apply or still comparing your options, Capital for Business has the resources and products to support your next move.

Explore types of small business loans to find the right fit for your goals, timeline, and financial profile. If your credit history isn't perfect, don't let that stop you. Our bad credit business loans guide walks you through options specifically designed for business owners who've faced financial challenges. Since 2009, we've helped thousands of small businesses access funding quickly and affordably, even when traditional banks said no. Reach out today and let us help you find a loan structure that works for your business, not against it.

Frequently asked questions

What is a business term loan?

A business term loan delivers a lump sum upfront, which you repay in fixed installments with interest over a set period. Payments are typically amortized, meaning early payments cover more interest while later payments reduce more of the principal balance.

How much can I borrow with a term loan?

Business term loans typically range from $5,000 to $5 million, though the amount depends on the lender, your credit history, and your business's financials.

What are common requirements to qualify for a term loan?

You'll usually need 2+ years in business, $100,000 or more in annual revenue, and a minimum 680 FICO score for most traditional lenders, though alternative lenders may accept lower scores.

Are there penalties for repaying a term loan early?

Prepayment penalties are common on long-term loans, typically 1% to 5% of the remaining balance. SBA loans only apply this penalty to loans with 15-year-plus terms during the first three years.

When doesn't it make sense to use a business term loan?

Term loans are usually not ideal for ongoing, unpredictable expenses or seasonal cash flow gaps. Lines of credit are better suited for those needs because they offer flexible access to funds without locking you into fixed payments.