Getting turned down by a traditional bank can stall your ambitions, but it does not have to be the end of your growth story. Many small business owners across the United States and Canada are discovering diverse loan options, from SBA-backed programs to flexible credit lines, that cater to a wider range of needs and credit backgrounds. This guide uncovers practical financing solutions, helping you find the right capital path to fuel your next expansion or resolve cash flow challenges quickly.

Table of Contents

- Defining Small Business Loan Options Today

- Comparing Major Loan Types and Variations

- Eligibility Requirements and Application Process

- Costs, Repayment Terms, and Potential Risks

- Alternatives to Traditional Loans Explained

Key Takeaways

| Point | Details |

|---|---|

| Diverse Loan Options | Small businesses can choose from various loan types such as Term Loans, SBA Loans, and Lines of Credit, each tailored to specific funding needs. |

| Eligibility Criteria | Qualification often hinges on credit history, business performance, and financial documentation, requiring meticulous preparation. |

| Understanding Costs | Loan costs vary widely, with interest rates and associated fees important to consider to ensure affordability and financial viability. |

| Alternative Funding | Entrepreneurs should explore alternative funding options, including crowdfunding and angel investors, to diversify financing sources beyond traditional loans. |

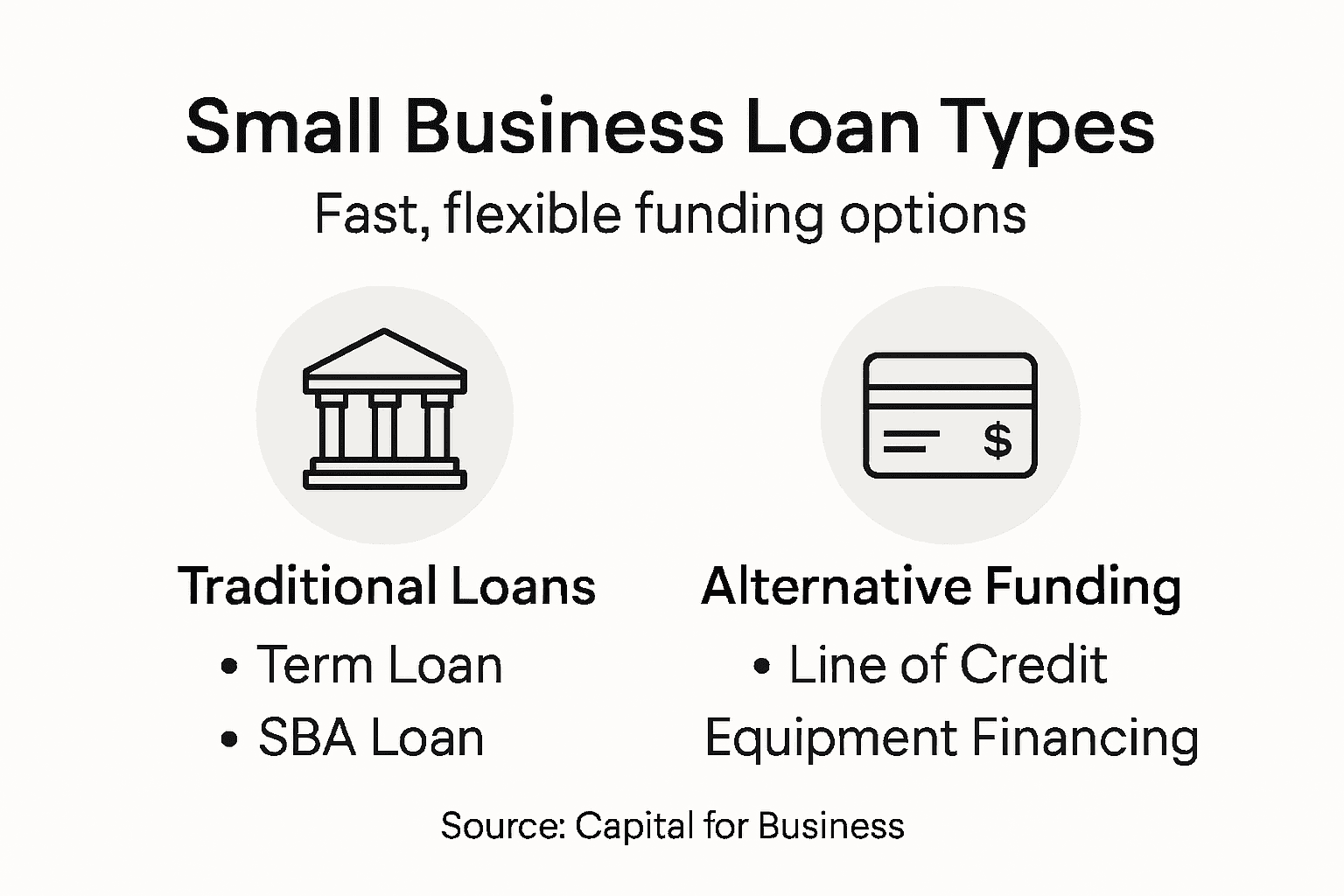

Defining Small Business Loan Options Today

Small business loans represent critical financial instruments designed to support entrepreneurial growth and operational needs. Understanding these financing options requires navigating a complex landscape of lending opportunities tailored to different business contexts. Small business funding encompasses multiple loan types, each with unique characteristics and application requirements.

The primary loan categories for small businesses include:

- Term Loans: Traditional financing with fixed repayment schedules

- Lines of Credit: Flexible funding allowing businesses to draw funds as needed

- Equipment Financing: Specialized loans for purchasing business machinery

- SBA Loans: Government-backed options with favorable terms

- Merchant Cash Advances: Alternative funding based on future revenue

Small businesses typically qualify for loans based on several critical factors. Credit score, business history, annual revenue, and collateral availability serve as primary evaluation metrics for lenders. The Small Business Administration facilitates access by guaranteeing loans and reducing institutional risk, enabling more businesses to secure necessary capital.

Loan amounts can range dramatically, from microloans under $50,000 to substantial investments reaching $5.5 million. This diversity ensures that businesses across different scales and industries can find appropriate financing solutions. Entrepreneurs must carefully assess their specific financial needs, projected growth, and repayment capabilities when selecting a loan product.

Here's a concise look at how the main small business loan types compare on key features:

| Loan Type | Typical Purpose | Loan Amount Range | Repayment Terms |

|---|---|---|---|

| Term Loan | General expansion, purchases | $25,000–$5.5 million | 1–10 years, fixed rate |

| Line of Credit | Working capital needs | $10,000–$500,000 | Revolving, ongoing use |

| SBA 7(a) Loan | Broad business funding | Up to $5 million | Up to 25 years |

| Equipment Financing | Machinery and vehicles | Up to 100% equipment | 3–7 years, asset-backed |

| Merchant Advance | Short-term cash flow gaps | $5,000–$250,000 | 3–18 months, variable |

Pro tip: Before applying, compile a comprehensive financial portfolio including tax returns, business plans, and cash flow projections to improve your loan approval chances.

Comparing Major Loan Types and Variations

Navigating the landscape of small business loans requires understanding the nuanced differences between various financing options. SBA loan programs offer distinct financing pathways designed to meet diverse business needs, each with unique characteristics and strategic advantages.

The primary SBA loan categories include:

- 7(a) Loans: Most popular general-purpose business financing

- 504 Loans: Long-term financing for major fixed assets

- Microloan Program: Small capital investments under $50,000

- CAPLine Program: Short-term working capital solutions

- Export Loan Program: Specialized financing for export-focused businesses

Each loan type serves different strategic purposes with varying requirements. Term lengths, interest rates, and qualification criteria differ significantly across these programs. The 7(a) loan program provides maximum flexibility, allowing funds for working capital, equipment purchases, and business expansion, with loan amounts reaching up to $5 million.

504 loans specifically target long-term investments in real estate and heavy equipment, offering fixed-rate financing that helps businesses make substantial infrastructure investments. These loans typically involve collaboration between local development companies, private sector lenders, and the Small Business Administration to provide comprehensive financing solutions.

Pro tip: Consult with a financial advisor to match your specific business growth strategy with the most appropriate loan type and funding structure.

Eligibility Requirements and Application Process

Small business loan applications involve a comprehensive evaluation process that requires careful preparation and strategic documentation. Loan qualification involves multiple assessment criteria designed to verify business viability and financial stability.

Key eligibility requirements typically include:

- Business Type: For-profit enterprises located in the United States

- Credit History: Demonstrated creditworthiness and financial responsibility

- Business Age: Minimum operational history (usually 2+ years)

- Revenue Thresholds: Consistent annual income meeting lender standards

- Debt Service Coverage: Ability to manage additional financial obligations

The application process demands meticulous documentation and financial transparency. Creditworthiness, business performance, and repayment capacity serve as primary evaluation metrics for most lenders. Entrepreneurs must prepare comprehensive financial statements, including tax returns, profit and loss statements, and detailed business plans that demonstrate potential for sustainable growth.

Most lenders require a structured application package containing specific supporting documents. This typically includes personal and business tax returns for the past three years, financial statements, business licenses, lease agreements, and a detailed explanation of the loan's intended purpose. Credit scores above 680 significantly improve approval chances, though some specialized loan programs accommodate lower credit ranges.

Pro tip: Organize your financial documentation systematically and consider obtaining a professional credit report before applying to identify and address potential weaknesses.

Costs, Repayment Terms, and Potential Risks

Small business loans represent complex financial instruments with nuanced cost structures and potential implications for entrepreneurs. Loan costs vary significantly across different lending platforms, requiring careful analysis and strategic planning.

Key financial considerations include:

- Interest Rates: Ranging from 6% to 25% depending on loan type

- Origination Fees: Typically 1-6% of total loan amount

- Prepayment Penalties: Potential additional charges for early repayment

- Closing Costs: Administrative expenses associated with loan processing

- Collateral Requirements: Assets potentially at risk for loan default

Repayment terms create significant variation in overall loan affordability. Most small business loans offer monthly payment structures, with terms ranging from short-term (6-24 months) to long-term (5-10 years) financing options. Variable interest rates can introduce additional complexity, potentially increasing total repayment amounts during the loan lifecycle.

Potential risks extend beyond simple financial calculations. Entrepreneurs must consider the broader implications of business debt, including potential personal credit impact, potential asset seizure, and long-term financial obligations. Defaulting on a business loan can create substantial challenges, potentially limiting future financing opportunities and damaging business creditworthiness.

Pro tip: Create a comprehensive financial contingency plan that includes multiple repayment scenarios to mitigate potential loan-related risks.

Alternatives to Traditional Loans Explained

Entrepreneurs facing challenges securing conventional bank financing have multiple innovative funding alternatives to explore. Government funding options provide diverse pathways for small businesses seeking financial support beyond traditional lending models.

Alternative funding strategies include:

- Crowdfunding Platforms: Raising capital through online investor networks

- Government Grants: Non-repayable funds for specific business initiatives

- Angel Investors: Private equity investments from high-net-worth individuals

- Merchant Cash Advances: Financing based on future credit card sales

- Equipment Financing: Specialized loans secured against business equipment

- Peer-to-Peer Lending: Online platforms connecting borrowers and investors

Crowdfunding and angel investing represent particularly dynamic alternatives for entrepreneurs with innovative business concepts. These methods not only provide financial resources but can also offer strategic guidance, networking opportunities, and potential mentorship from experienced investors. Unlike traditional loans, these funding sources often require demonstrating unique value propositions and strong growth potential.

Each alternative funding method carries distinct advantages and potential limitations. Factors such as business stage, industry, credit history, and specific financial needs will determine the most appropriate funding strategy. Careful evaluation of repayment terms, equity dilution, and long-term financial implications remains crucial when exploring non-traditional financing options.

Below is a summary of traditional loans and alternative funding methods with their typical strengths and ideal use cases:

| Funding Source | Main Advantage | Best For |

|---|---|---|

| Term Loan | Fixed payments, predictability | Stable, mature businesses |

| SBA Loan | Lower rates, longer terms | Strong credit, documentation |

| Equipment Financing | Secures required tools | Asset-dependent firms |

| Merchant Cash Advance | Quick access, flexible | High-volume retail/services |

| Crowdfunding | Community engagement | Innovative startups |

| Angel Investor | Industry expertise, capital | High-growth potential firms |

| Government Grant | No repayment required | Specialized, qualifying projects |

| Peer-to-Peer Lending | Fast online approval | Thinner credit histories |

Pro tip: Develop a comprehensive funding strategy that combines multiple financing sources to maximize financial flexibility and minimize individual funding constraints.

Discover Fast, Flexible Funding Tailored for Your Small Business Needs

Navigating the complex world of small business loans can be overwhelming. The article highlights key challenges such as finding the right loan type, understanding eligibility criteria, and managing repayment risks. If you are looking for quick access to working capital, equipment financing, or a flexible business line of credit that meets your unique business needs, your solution is right here. Capital for Business understands the pain points of stringent bank requirements and slow processes and offers fast, reliable funding options designed for entrepreneurs like you.

Boost your business growth today with funding options that align with your goals. Visit Capital for Business to explore a wide range of financial services including small business loans and merchant cash advances. Don’t let paperwork or long wait times hold you back. Learn more about our working capital solutions or get started now to secure the funds you need to expand, upgrade, and thrive.

Frequently Asked Questions

What are the main types of small business loans available?

Small business loans primarily include term loans, lines of credit, equipment financing, SBA loans, and merchant cash advances, each designed to meet different financial needs.

How do I qualify for a small business loan?

Eligibility for a small business loan typically requires a good credit history, consistent annual revenue, a minimum operational history of two years, and the ability to manage additional debt obligations.

What are the typical repayment terms for small business loans?

Repayment terms can vary significantly; term loans typically range from 1 to 10 years, while lines of credit offer ongoing access to funds. SBA loans can have terms up to 25 years depending on the program.

What should I include in my application for a small business loan?

Your application should include comprehensive financial documentation such as tax returns, profit and loss statements, a business plan, and a detailed explanation of the loan's purpose to improve approval chances.