Managing cash flow gaps can leave Canadian and American small business owners feeling pressed for answers, especially in fast-paced retail and construction environments. Short term loans are uniquely designed to deliver rapid funds with repayment periods ranging from a few weeks to twelve months. This funding approach allows businesses to tackle urgent expenses, purchase inventory, or seize time-sensitive opportunities. Discover how short term loans work, what options are available, and how to make informed financing choices without risking your business's financial stability.

Table of Contents

- Defining Short Term Loans and Their Purpose

- Popular Short Term Loan Types for Businesses

- How Short Term Loans Work in Practice

- Eligibility, Application, and Repayment Requirements

- Costs, Risks, and Common Pitfalls

- Short Term Loans Versus Other Financing Options

Key Takeaways

| Point | Details |

|---|---|

| Short Term Loans Provide Quick Solutions | Ideal for addressing urgent cash flow needs, these loans offer rapid funding with minimal documentation. |

| High Costs and Risks | Borrowers should be cautious of high interest rates and frequent repayments that can strain cash flow. |

| Evaluate Loan Options Carefully | Analyze various financing options to find the best fit for your business, considering costs, repayment terms, and overall financial health. |

| Prepare for the Application Process | Maintain a detailed financial portfolio to streamline the loan application and increase the likelihood of approval. |

Defining Short Term Loans and Their Purpose

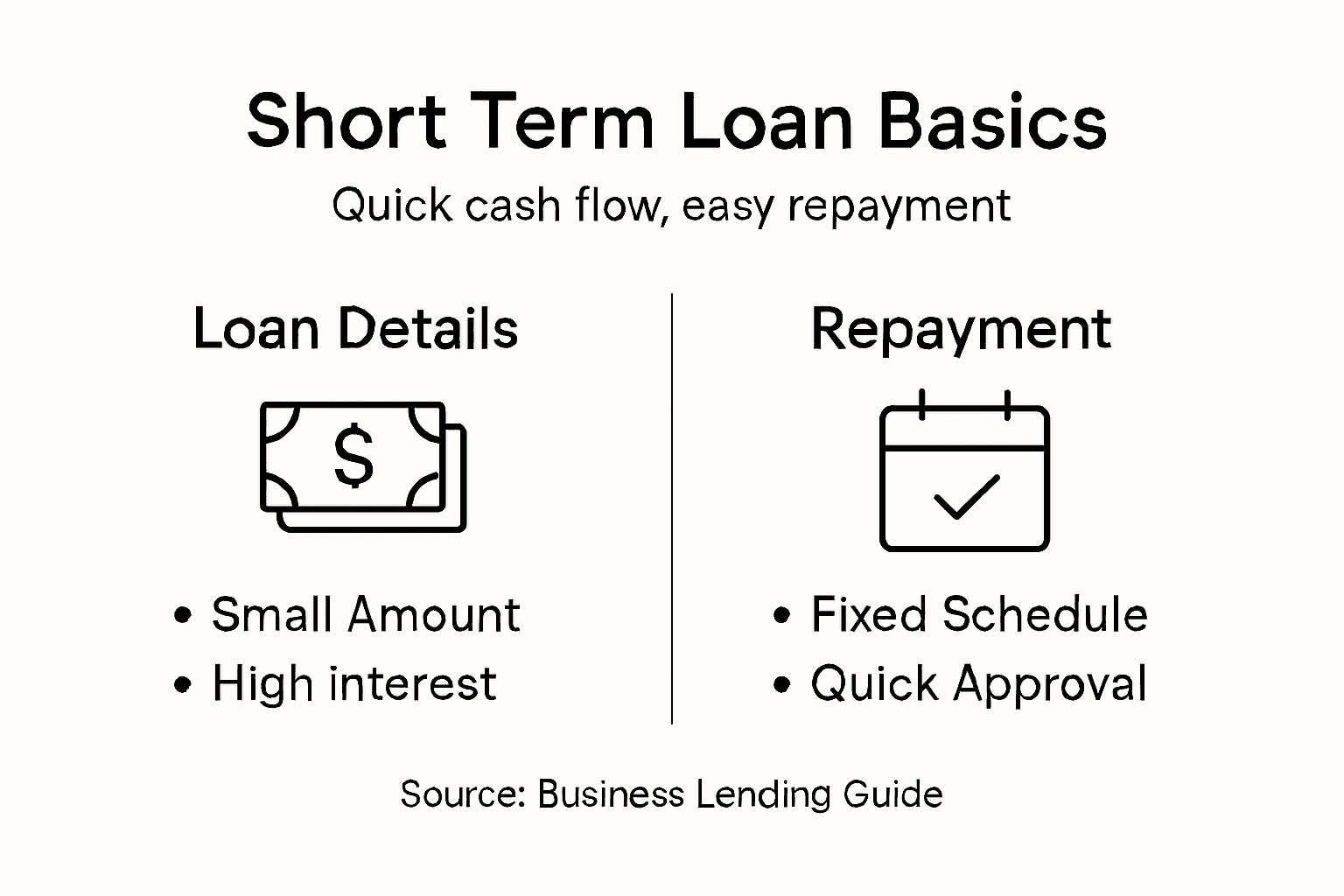

Short term loans represent a critical financial tool designed to help businesses and entrepreneurs rapidly address temporary cash flow challenges. These financial products provide quick access to funds with the explicit understanding that repayment occurs within a short timeframe, typically spanning several weeks to twelve months.

The primary purpose of short term loans centers on offering flexible funding solutions for urgent business needs. These might include:

- Purchasing critical inventory

- Covering unexpected operational expenses

- Bridging temporary revenue gaps

- Managing seasonal fluctuations in cash flow

- Seizing time-sensitive business opportunities

Unlike traditional long-term financing, short term loans are structured to provide immediate financial relief without requiring extended commitment. Business owners can access these funds quickly, often with minimal documentation and faster approval processes compared to conventional bank loans.

The mechanics of short term loans typically involve relatively smaller funding amounts, higher interest rates, and compressed repayment schedules. Lenders evaluate factors like business revenue, credit history, and financial stability to determine loan eligibility and terms. These loans are particularly valuable for small businesses experiencing temporary financial pressures or seeking rapid capital infusion.

Pro tip: Before applying for a short term loan, carefully analyze your precise funding needs and create a clear repayment strategy to maximize financial benefits and minimize potential risks.

Popular Short Term Loan Types for Businesses

Small businesses have several short-term financing options designed to address immediate financial needs and support operational flexibility. Understanding these loan types can help entrepreneurs make strategic funding decisions tailored to their specific business requirements.

The most common short-term loan types include:

- SBA 7(a) Loans: Government-backed loans offering working capital with flexible terms

- Microloans: Smaller funding amounts ideal for startups and emerging businesses

- Business Lines of Credit: Revolving credit allowing flexible fund access

- Invoice Financing: Borrowing against outstanding customer invoices

- Merchant Cash Advances: Quick funding repaid through future sales percentages

Traditional short-term loans typically range from 3 to 18 months and provide rapid access to working capital. Business lines of credit offer unique advantages by allowing entrepreneurs to draw funds as needed and pay interest only on the borrowed amount. This flexibility makes them particularly attractive for managing unpredictable cash flow fluctuations.

Merchant cash advances represent another innovative financing solution, especially for businesses with strong sales volumes. These products provide immediate funds in exchange for a predetermined percentage of future credit card sales, offering an alternative to traditional loan structures for companies that might not qualify for conventional bank financing.

Here's a snapshot of how key short-term loan types differ for small businesses:

| Loan Type | Typical Use Case | Speed of Funding | Main Cost Factor |

|---|---|---|---|

| SBA 7(a) Loans | Working capital | Moderate | Moderate interest, fees |

| Microloans | Startup costs | Fast | Lower amounts, higher rates |

| Business Line of Credit | Ongoing expenses | Very Fast | Pay interest on used funds |

| Invoice Financing | Outstanding invoices | Very Fast | Factor fee on invoice |

| Merchant Cash Advance | High volume sales needs | Instant | Highest effective cost |

Pro tip: Carefully compare the total borrowing costs, repayment terms, and qualification requirements for different short-term loan types before selecting the most appropriate option for your business.

How Short Term Loans Work in Practice

In the world of business financing, short-term loans operate through a streamlined process designed to provide quick cash with minimal barriers. These financial products are characterized by their rapid approval, minimal documentation, and flexible repayment structures that cater to immediate business needs.

The typical short-term loan process involves several key steps:

- Application: Submit basic business financial information

- Soft Credit Check: Lenders perform a non-invasive credit evaluation

- Funding Decision: Rapid approval within hours or days

- Fund Disbursement: Direct deposit into business account

- Repayment: Fixed schedule of weekly or monthly payments

Repayment terms are a critical aspect of short-term loans. Most lenders establish predetermined payment schedules, typically ranging from weekly to monthly installments. The shorter loan duration means higher interest rates, making it crucial for businesses to carefully plan their repayment strategy and ensure consistent cash flow to meet these obligations.

Unlike traditional bank loans, short-term financing often requires less stringent qualification criteria. Lenders focus more on current business performance and potential future revenue rather than extensive credit history. This approach allows newer or smaller businesses with limited credit backgrounds to access necessary funding, providing a lifeline during critical growth or operational challenge periods.

Pro tip: Always calculate the total cost of borrowing, including all fees and interest, before accepting a short-term loan to understand the true financial impact on your business.

Eligibility, Application, and Repayment Requirements

Short-term business loans have specific eligibility criteria for applicants that vary depending on the lender and loan type. These requirements are designed to assess a business's financial health, creditworthiness, and ability to repay the borrowed funds.

Key eligibility requirements typically include:

- Minimum Annual Revenue: Usually $50,000-$100,000

- Business Credit Score: Minimum score of 550-650

- Time in Business: Typically 6-12 months of operational history

- Debt-to-Income Ratio: Less than 50% preferred

- Consistent Cash Flow: Demonstrable ability to make regular payments

Application documents play a crucial role in the loan approval process. Lenders typically require comprehensive financial documentation to evaluate a business's lending risk. These documents help paint a complete picture of the business's financial standing and repayment capabilities.

Repayment structures for short-term loans are more aggressive compared to traditional long-term financing. Most loans require weekly or monthly payments, with terms ranging from 3 to 18 months. The condensed repayment timeline means higher periodic payments but lower total interest compared to extended loan periods. Businesses must carefully assess their cash flow to ensure they can meet these more frequent and potentially larger payment obligations.

Pro tip: Prepare a detailed financial portfolio in advance, including tax returns, bank statements, and cash flow projections, to streamline your short-term loan application process.

Costs, Risks, and Common Pitfalls

Short-term business loans come with complex financial implications that entrepreneurs must carefully navigate. Borrowing costs and associated risks can significantly impact a business's financial health if not thoroughly understood and strategically managed.

Key risks and potential pitfalls include:

- High Interest Rates: Often 10-25% annually

- Frequent Repayment Schedules: Weekly or monthly payments

- Potential Debt Cycle: Risk of continuous borrowing

- Cash Flow Strain: Aggressive repayment terms

- Hidden Fees: Origination, processing, and prepayment penalties

Financial risks extend beyond immediate loan terms. Businesses may encounter challenges such as liquidity mismatches and increased vulnerability during economic downturns. The condensed repayment window means less flexibility compared to traditional long-term financing, demanding precise financial planning and robust cash flow management.

Understanding the total cost of borrowing is crucial. Short-term loans often carry higher interest rates and fees, which can quickly escalate if not managed carefully. Businesses must conduct thorough cost-benefit analyses, considering not just the immediate funding need but the long-term financial implications of taking on such financing.

Compare major risks of short-term loans and possible business impacts:

| Risk | Impact on Business | How to Mitigate |

|---|---|---|

| High interest rate | Increased monthly expenses | Negotiate or shop lenders |

| Frequent repayments | Cash flow management strain | Maintain cash reserves |

| Hidden fees | Unexpected financial loss | Review all loan documents |

| Debt cycle | Long-term financial stress | Borrow only as needed |

Pro tip: Calculate the total annualized percentage rate (APR) and create a detailed repayment strategy before accepting any short-term loan to avoid unexpected financial strain.

Short Term Loans Versus Other Financing Options

Entrepreneurs must carefully evaluate multiple financing strategies to determine the most appropriate funding solution for their business needs. Comparing financing methods requires a comprehensive analysis of cost, speed, flexibility, and long-term financial implications.

Key financing alternatives include:

- Short-Term Loans:

- Quick funding

- Higher interest rates

- Shorter repayment periods

- Business Credit Cards:

- Immediate access to funds

- Revolving credit

- Higher transaction fees

- Equipment Financing:

- Asset-specific funding

- Lower interest rates

- Longer approval processes

- Business Lines of Credit:

- Flexible borrowing

- Pay interest only on used amount

- Lower ongoing costs

- Merchant Cash Advances:

- Fast approval

- Repaid through sales percentage

- Most expensive option

Comparative analysis reveals that each financing method offers unique advantages and drawbacks. Short-term loans excel in providing rapid funding with minimal documentation, making them ideal for businesses needing immediate capital infusion. However, they typically carry higher interest rates compared to traditional bank loans or equipment financing.

Business owners must conduct thorough financial assessments, considering not just immediate funding needs but also long-term repayment capabilities and overall financial health. The right financing strategy depends on specific business circumstances, cash flow projections, and strategic growth objectives.

Pro tip: Calculate the total cost of borrowing across different financing options, including hidden fees and interest rates, before making a final decision.

Unlock Fast Funding Solutions for Your Business Cash Flow Needs

If you are struggling with urgent cash flow gaps or unexpected expenses, quick and reliable financial support is essential. This article highlights the challenges of securing short term loans with tight repayment schedules and higher costs. At Capital for Business, we understand these pain points and offer a wide range of solutions tailored to your immediate working capital needs—whether it is through small business loans, merchant cash advances, or flexible business lines of credit. Our streamlined process and experienced team work quickly to get you funded so you can focus on growing your business.

Don’t let high interest rates and frequent repayment schedules hold your business back. Explore how short term loan options can provide the rapid cash infusion you need without the hassle of traditional banks. Visit us today to learn more and apply from trusted lenders who prioritize your success. Get the funding you need now to overcome cash flow challenges and seize new growth opportunities.

Frequently Asked Questions

What are short term loans?

Short term loans are financial products designed to help businesses quickly address temporary cash flow challenges by providing rapid access to funds that must be repaid within a short timeframe, typically ranging from several weeks to 12 months.

What are the common types of short term loans for businesses?

Common types of short term loans include SBA 7(a) loans, microloans, business lines of credit, invoice financing, and merchant cash advances. Each offers different benefits and suits various business needs.

How does the application process for short term loans work?

The application process usually involves submitting basic financial information, undergoing a soft credit check, receiving a funding decision within a few hours or days, and then having the funds directly deposited into the business account.

What should businesses consider before taking out a short term loan?

Before applying for a short term loan, businesses should carefully assess their funding needs, review repayment strategies, and calculate the total borrowing costs, including interest rates and any associated fees.

Recommended

- Manage Cash Flows for Timely Loan Payments

- Entrepreneurs That Often Need Short-Term Loans | Capital For Business

- What Are The Circumstances That Need A Fast Business Loan?

- How to get the best out of your short term financing goals

- Konsumrausch im Dezember. So bereitest du dich auf das Januarloch vor - Smolio