The equipment in your restaurant is not just furniture. It is the engine of your entire operation, and replacing or upgrading it can cost anywhere from $40,000 to well over $200,000. That kind of expense can either fuel serious growth or put your cash flow in a dangerous position if you approach it without a plan. Many restaurant owners know they need new equipment but feel uncertain about whether to lease, buy, or finance, and which lender to trust. This guide walks you through the 6-step financing process, compares your real options, and gives you the tools to make a confident decision.

Table of Contents

- What is restaurant equipment financing?

- Step-by-step: The restaurant equipment financing process

- What documents and requirements do I need?

- Types of lenders: Comparing your options

- Lease, buy, or finance: Which makes sense?

- Special circumstances: Startups, bad credit, and Canadian options

- Find the right restaurant equipment financing for your needs

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know your costs | Equipment financing lets you get what you need without heavy upfront spending, but requires understanding all terms and fees. |

| Prepare your paperwork | Have your financials, business plan, and vendor quotes ready to streamline the process and boost approval odds. |

| Choose the right lender | Banks and SBA give best rates for strong credit; online lenders move fastest for urgent needs. |

| Match method to goals | Leasing, buying, and loans each fit different situations—get clear on which aligns with your growth and cash flow. |

| Consider special cases | Startups and low-credit applicants can still qualify with the right lender, extra planning, and higher down payments. |

What is restaurant equipment financing?

Restaurant equipment financing is a funding arrangement that lets you acquire new or upgraded equipment without paying the full cost upfront. Instead of draining your operating capital, you spread payments over a set term, typically 12 to 84 months, while the equipment works for you from day one. This approach is especially valuable for independent restaurants, startups, and growing multi-unit operators who need to preserve cash for payroll, inventory, and daily operations.

Almost any essential piece of kitchen or front-of-house equipment qualifies. Common items include:

- Commercial ranges and ovens

- Refrigeration units and walk-in coolers

- POS systems and payment terminals

- Dishwashers and prep equipment

- Ventilation hoods and fryers

- Espresso machines and bar equipment

The costs add up fast. Equipment costs range from $3,000 to $8,000 for a commercial range and $2,500 to $6,000 for a refrigerator, with full kitchen buildouts easily reaching six figures. Financing makes these investments accessible without forcing you to choose between growth and stability. If you want a broader view of funding options, the restaurant business loan guide covers the full landscape.

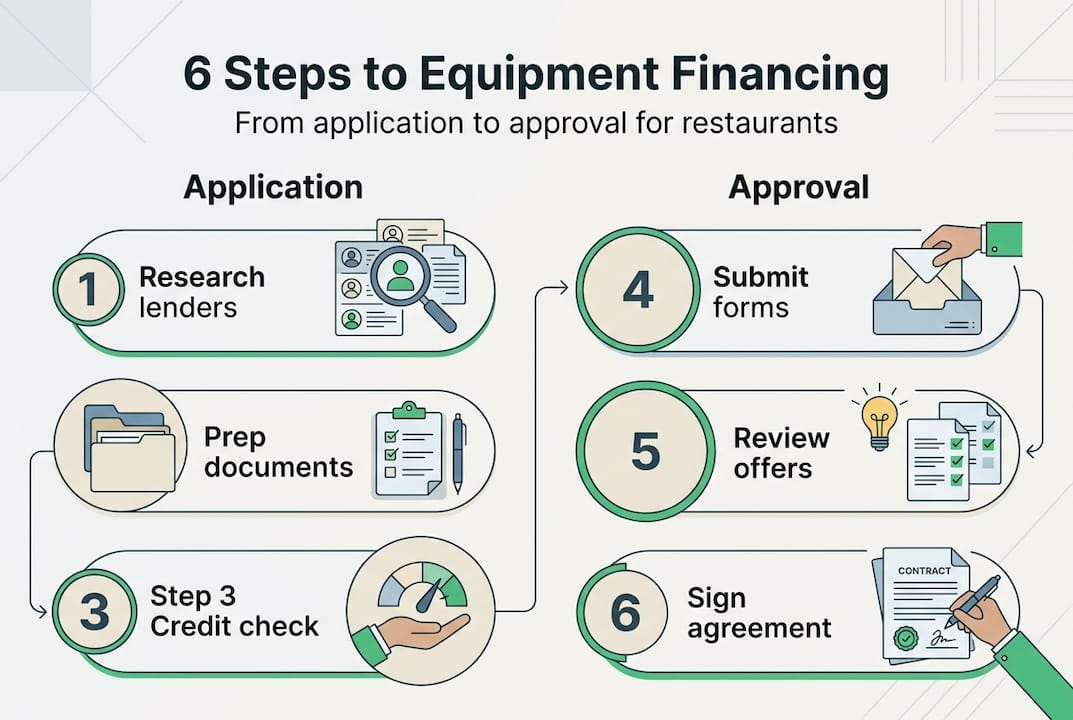

Step-by-step: The restaurant equipment financing process

Understanding the process before you start saves time and reduces stress. The 6-step financing process follows a predictable path, and knowing what comes next keeps you in control.

- Check your credit and financials. Pull your personal and business credit reports. Know your score, your debt-to-income ratio, and your revenue trends before any lender sees them.

- Gather your documents. Collect tax returns, bank statements, profit and loss statements, and equipment vendor quotes. Having these ready before you apply cuts days off the process.

- Get lender quotes. Contact at least three lenders, including online lenders and traditional banks, to compare rates, terms, and fees. Do not accept the first offer.

- Submit your application. Complete the lender's application with your documents attached. Online lenders often have streamlined portals; banks may require in-person meetings.

- Underwriting review. The lender evaluates your creditworthiness, cash flow, and the equipment's value as collateral. This is where financing options explained can help you understand what lenders are looking for.

- Closing and funding. Once approved, you sign the agreement and the lender pays the vendor directly or releases funds to you.

Pro Tip: Start collecting your required documents at least two weeks before you plan to apply. Missing paperwork is the single most common reason for delays in the equipment financing tutorial process.

| Step | Online lender timeline | Bank or SBA timeline |

|---|---|---|

| Credit check and prep | 1-2 days | 3-7 days |

| Document gathering | 2-5 days | 5-14 days |

| Application and review | 1-3 days | 7-21 days |

| Underwriting | 1-2 days | 14-45 days |

| Closing and funding | Same day to 2 days | 5-10 days |

| Total estimate | 5-14 days | 30-90 days |

What documents and requirements do I need?

Being prepared with the right paperwork is one of the most practical things you can do before applying. Lenders want to see that your business generates enough revenue to cover payments and that you have a track record of managing debt responsibly.

According to standard lender requirements, you typically need the following:

- Business and personal tax returns (last 2 years)

- Profit and loss statements (last 12 months)

- Business bank statements (last 3-6 months)

- Equipment vendor quotes or invoices

- A business plan (especially for startups)

- Business license and formation documents

On the financial side, most lenders look for a personal credit score between 620 and 680. They also evaluate your debt service coverage ratio (DSCR), which measures whether your revenue can cover loan payments. A DSCR above 1.25 is generally considered healthy. Down payments typically range from 10% to 20% of the equipment cost.

Startups and newer restaurants face additional scrutiny. If your business has less than two years of operating history, expect to provide a detailed business plan, personal financial statements, and possibly a larger down payment. Review the full list of documents for restaurant loans and equipment financing requirements to make sure nothing catches you off guard.

Types of lenders: Comparing your options

Not all lenders are built the same, and the right choice depends on your timeline, credit profile, and how much flexibility you need. Here is a clear breakdown of the four main categories.

| Lender type | Approval speed | Credit requirement | Cost | Best for |

|---|---|---|---|---|

| Traditional bank | 30-60 days | 680+ | Lowest rates | Established restaurants |

| SBA-backed lender | 45-90 days | 650+ | Low rates, fees apply | Long-term, large purchases |

| Online or alt lender | 1-5 days | 500-620+ | Higher rates | Speed, lower credit |

| Equipment lessor | 3-10 days | 600+ | Varies by structure | Flexibility, short-term |

SBA loans offer the lowest rates but come with slower approval timelines, while online lenders fund faster but typically charge more. The right fit depends on how urgently you need the equipment and how strong your financials are. For more detail on SBA and bank products, review SBA and bank loan updates or explore restaurant business loans for a broader comparison.

Pro Tip: If you need equipment within two weeks, go with an online lender. If you can wait 60 to 90 days and your credit is strong, an SBA loan will save you significantly on interest over the life of the loan.

Lease, buy, or finance: Which makes sense?

This is the question most restaurant owners wrestle with longest. Each path has real trade-offs, and the right answer depends on your growth stage, cash position, and how long you plan to use the equipment.

Cost comparison on a $100,000 equipment package:

| Method | Monthly payment (est.) | Total paid over 5 years | Equity built |

|---|---|---|---|

| Lease | $2,200 | $132,000 | None |

| Equipment loan | $1,900 | $114,000 | Full ownership |

| Purchase outright | N/A | $100,000 | Full ownership |

Statistic: Leasing costs 20-50% more over five years compared to buying, but it preserves cash and keeps monthly payments predictable.

Here is a quick breakdown of each option:

Leasing

- Pros: Lower upfront cost, easy upgrades, predictable payments

- Cons: No equity, higher total cost, restrictions on modifications

- Best for: Startups, restaurants with uncertain growth, technology-heavy equipment that becomes outdated

Equipment loan or financing

- Pros: Builds equity, lower total cost, tax deductions on depreciation

- Cons: Requires down payment, credit approval, longer commitment

- Best for: Established restaurants, stable operations, long-use equipment

Outright purchase

- Pros: No interest, full ownership immediately

- Cons: Large cash outlay, reduces working capital

- Best for: Restaurants with strong cash reserves and no immediate growth needs

For a deeper look at the trade-offs, compare equipment leasing vs. financing or use the choosing between loan or lease guide to match your situation.

Special circumstances: Startups, bad credit, and Canadian options

Not every restaurant owner walks into the financing process with two years of tax returns and a 700 credit score. These edge cases are more common than you might think, and there are real solutions available.

Startups face the steepest climb. Startups need stronger business plans and higher down payments, often 20% to 30%, because lenders cannot rely on operating history. A well-structured business plan with realistic revenue projections, a clear concept, and a defined market can offset the lack of track record. Some lenders specialize in business loans for startups and understand the unique risk profile of new restaurants.

Bad credit does not automatically disqualify you. Alternative lenders and equipment lessors often work with scores as low as 500, though you should expect higher interest rates and shorter terms. The trade-off is access now versus cost over time. Explore bad credit business loans to understand what is realistically available at different credit levels.

Canadian restaurant owners have access to flexible leasing programs through specialized lessors who apply lower credit thresholds than traditional banks. Provincial programs and equipment-specific lenders make financing accessible even for newer operations.

Key thresholds to know: Most traditional lenders require a minimum personal credit score of 620. Alternative lenders may accept 500 or above. Canadian lessors often work with scores starting at 580, and some startup-focused lenders evaluate business plans more heavily than credit history alone.

If your restaurant is in a growth phase and you need capital to support it, small business loans for restaurants can bridge the gap while you build your credit profile.

Find the right restaurant equipment financing for your needs

You now have a clear picture of the process, the documents, the lender types, and the real costs involved. The next step is finding a financing partner who understands the restaurant industry and can move at your pace.

At Capital for Business, we have worked with restaurant owners across North America since 2009, connecting them with equipment financing options that fit their actual situation, not just their credit score. Whether you are weighing equipment leasing vs. financing or need to understand the types of small business loans available to you, our team can help you move from research to funding quickly. We work with startups, established operators, and everyone in between. Reach out today and get matched with a solution that supports your goals.

Frequently asked questions

How long does restaurant equipment financing approval take?

Online lenders typically approve applications in 1 to 5 days, while SBA or bank loans can take 30 to 90 days depending on the complexity of your application and documentation.

What credit score do I need to finance restaurant equipment?

Most lenders require a personal credit score between 620 and 680, but alternative lenders accept scores as low as 500, usually with higher rates and stricter terms.

What equipment can I finance for my restaurant?

Most essential items qualify, including ranges, refrigerators, and POS systems, as well as ovens, dishwashers, fryers, ventilation hoods, and espresso machines.

Is it better to lease or buy restaurant equipment?

Leasing costs 20 to 50% more over five years but keeps monthly costs lower and preserves cash. Buying or financing builds equity and reduces total cost over time.

Can startups get equipment financing?

Yes. Startups require strong plans and higher down payments, but several lenders specialize in startup restaurant financing and weigh business plans heavily in their approval decisions.