Many small business owners believe securing funding for commercial real estate is out of reach, reserved only for established corporations with deep pockets. In reality, Canadian entrepreneurs have access to multiple government-backed and private financing options specifically designed to support property acquisition and expansion. This guide breaks down the most accessible real estate funding sources available in 2026, from federal loan programs to flexible private solutions. You'll learn eligibility requirements, loan structures, interest rates, and practical strategies to help you choose the right financing path for your business growth.

Table of Contents

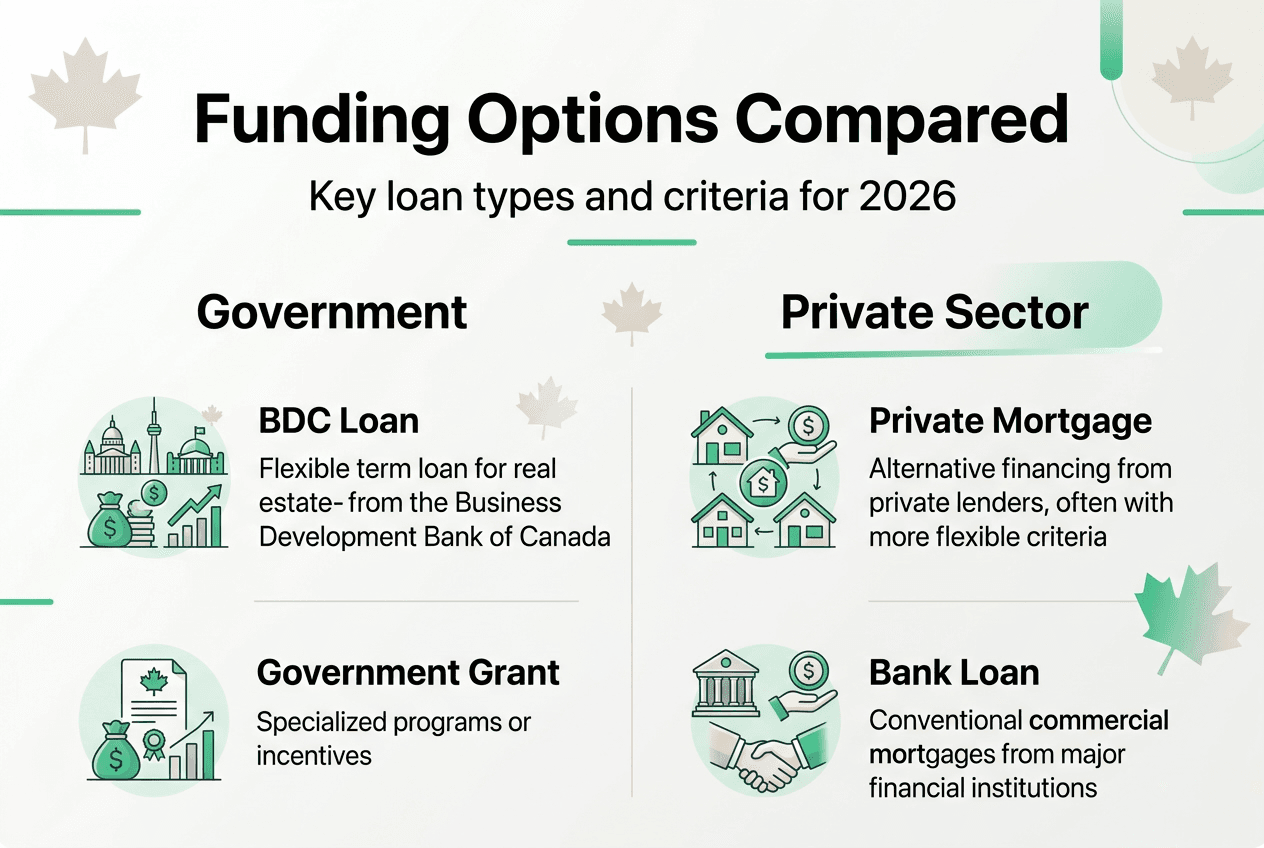

- Government-Backed Funding Options For Commercial Real Estate

- BDC Financing For Commercial Real Estate: Flexible And High-Value Option

- Private Mortgages: Short-Term Solutions With Distinct Considerations

- Comparing Real Estate Funding Options And Choosing The Right Fit

- Explore Tailored Business Funding Solutions For Your Real Estate Goals

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Government programs provide accessible funding | Federal programs like CSBFL offer loans up to $1.15 million with government backing for eligible small businesses. |

| BDC offers exceptional flexibility | Business Development Bank of Canada provides up to 100% financing with 25-year terms and principal payment deferrals. |

| Private mortgages suit urgent needs | Short-term private financing works for quick closings but carries higher rates between 8% and 15%. |

| Eligibility varies significantly | Each funding source has distinct requirements for revenue, credit history, and property type. |

| Strategic planning improves success | Matching your business goals with the right funding type and preparing thorough documentation increases approval odds. |

Government-backed funding options for commercial real estate

Federal programs form the foundation of accessible real estate financing for Canadian small businesses. The Canada Small Business Financing Loan (CSBFL) provides government-backed funding for equipment, commercial real estate, and leasehold improvements. Similarly, the Canada Small Business Financing Program (CSBFP) offers both term loans and lines of credit specifically designed to help entrepreneurs invest in property.

Eligible businesses typically operate as for-profit entities with gross annual revenues under $10 million. You must be registered and operating under Canadian law, which excludes non-profit organizations and most farming operations. Maximum loan amounts reach $1 million for CSBFL and up to $1.15 million under CSBFP, depending on your specific needs and qualifications.

Loan terms extend up to 15 years for term loans, providing manageable monthly payments that align with long-term business planning. Lines of credit offer shorter repayment periods but greater flexibility for ongoing projects. Interest rates fluctuate based on market conditions and lender policies, with a standard 2% registration fee applied at loan origination.

These programs specifically exclude certain expenses from eligible use. You cannot use government-backed loans for working capital, purchasing goodwill, or paying franchise fees. The focus remains squarely on tangible assets like real property, equipment, and physical improvements that enhance business operations.

For entrepreneurs with limited credit history, government backing significantly improves approval chances compared to conventional bank loans. Lenders view these programs as lower risk, making them more willing to work with newer businesses. Understanding the nuances between applying for business loans in Canada helps you navigate the application process more effectively.

| Program Feature | CSBFL | CSBFP |

|---|---|---|

| Maximum loan amount | $1 million | $1.15 million |

| Loan types | Term loans | Term loans and lines of credit |

| Maximum term length | 15 years | 15 years (term loans) |

| Registration fee | 2% | 2% |

| Eligible uses | Equipment, real estate, improvements | Property acquisition, expansion |

| Revenue limit | Under $10 million | Under $10 million |

Pro Tip: Prepare a comprehensive business plan and current financial statements before approaching lenders. Government-backed programs require detailed documentation, and having everything organized demonstrates professionalism and increases your approval likelihood significantly.

Exploring various business funding options Canada 2026 reveals additional paths beyond federal programs. Understanding how a business line of credit works complements your knowledge of term loans, giving you flexibility to structure financing around cash flow patterns.

BDC financing for commercial real estate: flexible and high-value option

The Business Development Bank of Canada (BDC) stands apart from traditional lenders by offering exceptionally flexible terms tailored to entrepreneurial growth. BDC provides up to 100% financing for commercial real estate projects, eliminating the substantial down payment barrier that stops many small business owners from pursuing property investments.

Loan durations can extend up to 25 years, significantly longer than typical bank mortgages. This extended timeline reduces monthly payment obligations, freeing up cash flow for operations and growth initiatives. Additionally, BDC may offer principal payment deferrals lasting up to 36 months, allowing you to establish revenue streams before major repayment obligations begin.

Eligible uses include acquiring existing commercial properties, constructing new facilities, or renovating current spaces to better serve business needs. BDC focuses exclusively on commercial applications, excluding residential developments and non-commercial facilities. This specialization means loan officers understand the unique challenges entrepreneurs face when expanding physical operations.

The application process emphasizes business viability and growth potential rather than relying solely on credit scores. BDC evaluates your business plan, market opportunity, management experience, and projected cash flows. This holistic approach benefits entrepreneurs who may have limited credit history but possess solid business fundamentals and clear growth strategies.

Beyond financing, BDC provides advisory services that help you refine project plans and develop sustainable financing strategies. Their consultants bring deep expertise in commercial real estate and small business growth, offering insights that improve project success rates. This combination of capital and knowledge creates a partnership rather than a simple lender-borrower relationship.

Key benefits of BDC financing include:

- Coverage of 100% of project costs without requiring personal equity contributions

- Extended 25-year repayment terms that reduce monthly obligations

- Principal payment deferrals up to 36 months for new projects

- Focus on business potential rather than strict credit score requirements

- Access to expert advisory services throughout the financing process

- Specialized understanding of entrepreneurial real estate needs

Pro Tip: Leverage BDC's advisory services even before applying for financing. Their consultants can help you identify potential weaknesses in your project plan and strengthen your application, significantly improving approval odds and potentially securing better terms.

Understanding different commercial business loan types helps you compare BDC offerings against other financing structures. Each loan type serves specific business scenarios, and matching your needs to the right product determines long-term success.

Private mortgages: short-term solutions with distinct considerations

Private mortgages fill a specific niche in Canadian real estate financing, serving as bridge solutions when traditional funding proves unavailable or timing demands quick action. These loans typically operate as interest-only arrangements with terms spanning 6 to 24 months, designed explicitly for temporary financing needs rather than long-term holds.

Interest rates reflect the higher risk private lenders assume. Rates typically range from 8% to 15%, substantially higher than conventional mortgages hovering between 4% and 6%. This premium compensates lenders for accepting borrowers who may have credit challenges, unique properties, or urgent timing requirements that traditional banks cannot accommodate.

Private lenders prioritize property value and loan-to-value ratios over borrower credit scores. If your property appraises well and you're requesting 65% to 75% of its value, approval becomes significantly more likely regardless of past credit issues. This asset-based approach opens doors for entrepreneurs recovering from bankruptcy, managing temporary credit problems, or dealing with properties that don't fit conventional lending criteria.

However, private mortgages carry distinct risks that demand careful evaluation. The unregulated nature of some private lenders means fewer consumer protections compared to federally regulated institutions. Without proper due diligence, you might encounter predatory terms, excessive fees, or lenders lacking proper licensing and oversight.

Scenarios where private mortgages prove valuable:

- Recent bankruptcy or consumer proposal preventing traditional bank approval

- Self-employed income that's difficult to document through conventional verification methods

- Unique or non-standard properties that banks consider too risky

- Urgent closing timelines requiring funding within days rather than weeks

- Bridge financing while waiting for traditional loan approval or property sale proceeds

- Poor credit scores below 600 that automatically disqualify conventional applications

Critical risks to watch:

- Significantly higher interest costs eating into investment returns

- Unregulated lenders operating without proper oversight or consumer protections

- Foreclosure risk if you cannot secure refinancing before term expiration

- Rollover traps where lenders charge excessive fees to extend short-term loans

- Hidden costs and penalties not clearly disclosed during initial negotiations

- Difficulty transitioning to traditional financing if property or credit issues persist

Pro Tip: Develop a clear exit strategy before signing any private mortgage agreement. Know exactly how you'll refinance or repay the loan when it matures, whether through property sale, traditional refinancing, or business revenue. Without this plan, you risk getting trapped in expensive rollover cycles that drain equity and threaten foreclosure.

Building strong business credit helps you transition from private to conventional financing more quickly. Understanding the trade-offs between a small business loan vs equipment leasing also reveals alternative strategies for conserving capital while growing operations.

Comparing real estate funding options and choosing the right fit

Selecting the optimal financing source requires understanding how each option stacks up across critical decision factors. The table below compares government-backed loans, BDC financing, and private mortgages on dimensions that matter most to small business owners.

| Feature | Government Loans (CSBFL/CSBFP) | BDC Financing | Private Mortgages |

|---|---|---|---|

| Maximum loan amount | $1 million to $1.15 million | Up to 100% of project cost | Varies by lender and property |

| Interest rates | Variable, competitive | Competitive, flexible | 8% to 15% |

| Loan terms | Up to 15 years | Up to 25 years | 6 to 24 months |

| Approval timeline | Several weeks | Moderate, flexible | Days to 2 weeks |

| Credit requirements | Moderate, government-backed | Flexible, business-focused | Minimal, asset-based |

| Down payment | Typically required | Potentially 0% | 25% to 35% |

| Eligible properties | Commercial only | Commercial only | Commercial and some unique properties |

| Best for | Established businesses with solid credit | Growth-focused entrepreneurs | Quick needs or credit challenges |

When evaluating which funding path aligns with your business needs, consider these essential factors:

- Your current creditworthiness and financial history determine which lenders will consider your application

- Timeline urgency influences whether you can wait weeks for traditional approval or need funding within days

- Project scale and total capital requirements help identify programs with sufficient lending capacity

- Risk tolerance affects your comfort with higher interest rates versus stricter approval criteria

- Long-term business strategy determines whether short-term bridge financing or extended repayment terms serve you better

- Cash flow projections reveal which monthly payment structures your business can sustain comfortably

Pro Tip: Align your funding choice directly with business goals and realistic cash flow projections. The lowest interest rate means nothing if payment obligations strain operations and prevent growth. Similarly, easy approval loses value if you cannot refinance before a short-term loan matures, triggering expensive penalties or foreclosure.

Securing the right financing proves especially critical for businesses with limited credit history or unconventional situations. Professional guidance helps you navigate complex requirements and present applications that highlight strengths while addressing potential concerns proactively.

Documentation quality significantly impacts approval success across all funding types. Gather current financial statements, detailed business plans, property appraisals, and market analysis before approaching any lender. This preparation demonstrates professionalism and allows lenders to make informed decisions quickly.

Consider consulting with financial advisors or mortgage brokers who specialize in commercial real estate. Their expertise helps you identify programs you might overlook and structure applications to maximize approval probability. The modest cost of professional advice often pays for itself through better terms, faster approval, or access to more suitable programs.

Reviewing comprehensive Canadian business funding options 2026 ensures you're not missing opportunities that perfectly match your situation. Following proven business loan application tips improves your presentation and increases the likelihood of favorable terms.

Explore tailored business funding solutions for your real estate goals

Navigating multiple funding options becomes simpler when you work with specialists who understand small business real estate financing. Capital For Business offers diverse funding solutions designed specifically for entrepreneurs pursuing commercial property investments across Canada. Our platform connects you with loan products ranging from traditional term loans to flexible lines of credit, each structured to match different business profiles and investment strategies.

We recognize that every business faces unique challenges and opportunities. Our team provides personalized guidance to help you identify which funding types align with your credit situation, timeline requirements, and growth objectives. Whether you need quick bridge financing or long-term acquisition capital, we simplify the application process and accelerate approval timelines compared to traditional bank procedures. Explore our range of easy small business loans, comprehensive funding solutions, and flexible business line of credit options to find the perfect fit for your real estate investment plans.

Frequently asked questions

What is the eligibility criteria for government-backed real estate loans?

Canadian small businesses operating for profit with gross annual revenue under $10 million generally qualify for government-backed programs like CSBFL and CSBFP. Applicants must be registered and operate under Canadian laws, which excludes non-profit organizations and most farming businesses.

How do private mortgages differ from traditional bank loans for real estate?

Private mortgages operate as short-term solutions with higher interest rates, typically 8% to 15%, and focus primarily on property value rather than borrower credit scores. Traditional bank loans offer lower rates, extended terms up to 25 years, and require stronger credit profiles with comprehensive income documentation.

What are the risks associated with private mortgages?

Major risks include significantly higher interest costs, potential exposure to unregulated lenders, foreclosure if refinancing fails, and rollover traps where lenders charge excessive fees for extensions. Developing a clear exit strategy and conducting thorough due diligence on lenders mitigates these dangers substantially.

Can I use government-backed loans for residential real estate or rental properties?

Government-backed programs like CSBFL and CSBFP specifically exclude residential developments and rental property investments from eligible uses. These loans focus exclusively on commercial real estate that directly supports business operations and growth.