Getting denied for a small business loan is frustrating, especially when the rejection comes down to something fixable. Many owners apply without fully understanding what lenders need, and a missing document or weak cash flow statement can stop funding cold. The good news is that most loan denials are avoidable. Whether you're applying for an SBA 7(a) loan in the U.S. or a Canada Small Business Financing Program (CSBFP) loan north of the border, the path to approval follows a clear set of steps. This guide walks you through exactly what to prepare, how to present it, and what to avoid so you can turn a potential denial into an approval.

Table of Contents

- Understand lender expectations and program requirements

- Gather and organize essential documents

- Craft a compelling business plan with strong financials

- Tailor your approach for your business type and situation

- Review, submit, and avoid common mistakes

- Our perspective: What actually moves the needle in loan approvals

- Ready to apply? Resources and solutions for your next step

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Align with program rules | Know your lender’s requirements before starting your application to maximize success. |

| Prepare thorough documentation | Organize all required documents, including business plans and financials, before applying. |

| Focus on cash flow | Strong, realistic cash flow statements are the single most important factor for loan approval. |

| Adjust for your business type | Startups, growing businesses, and restricted industries must tailor their approach to fit program eligibility. |

| Double-check before submitting | Review your application for errors and completeness to avoid common reasons for denial. |

Understand lender expectations and program requirements

Now that you're aware that many loan rejections come down to avoidable issues, let's start by breaking down what lenders want to see. Understanding the specific requirements of each program is the first step toward a stronger application. Lenders are not just evaluating your idea. They're evaluating your risk profile, your financial history, and your ability to repay.

For U.S. applicants, the SBA 7(a) loan is the most widely used government-backed option. To qualify, you generally need a personal FICO score of 650+, at least two years in business, demonstrated cash flow, a detailed business plan with financial projections, and complete documentation. Canadian applicants can access the CSBFP, which offers up to $1.15M for businesses with under $10M in annual revenue. Eligible uses include equipment, real estate, and working capital, and applications go through banks or credit unions.

Here's a quick comparison of the two programs:

| Feature | SBA 7(a) (U.S.) | CSBFP (Canada) |

|---|---|---|

| Max loan amount | $5M | $1.15M |

| Min credit score | 650 (FICO) | Varies by lender |

| Years in business | 2+ preferred | Startups eligible |

| Application via | SBA-approved lenders | Banks/credit unions |

| Key use cases | Working capital, equipment | Equipment, real estate |

Common dealbreakers lenders flag include:

- Insufficient cash flow or inconsistent revenue

- Operating in an ineligible industry (e.g., gambling, speculative real estate)

- Missing or outdated financial documents

- No clear repayment plan in the business plan

Familiarizing yourself with lender considerations before you apply can save you significant time. Also, reviewing common approval obstacles helps you spot gaps in your application early. For a broader view of lender options, a business loan provider guide can help you compare choices.

Pro Tip: Always confirm your industry is eligible for the specific loan program before investing time in the full application. Some industries are automatically excluded, and finding out late wastes everyone's time.

Gather and organize essential documents

Knowing exactly what lenders expect, your next step is to ensure you have the right documents ready, fast and organized. Incomplete paperwork is one of the most common reasons applications stall or get denied outright. Lenders need to verify your financial health quickly, and disorganized submissions signal poor management.

Full documentation is required for approval on both sides of the border. Here's what you'll typically need:

For U.S. SBA applicants:

- Personal and business tax returns (last 2-3 years)

- Profit and loss statements (current year, year-to-date)

- Balance sheets

- Business plan with financial projections

- Business licenses and legal documents

- Bank statements (last 3-6 months)

For Canadian CSBFP applicants:

- Business plan with revenue projections

- Recent financial statements

- Vendor quotes for asset purchases

- Business registration documents

- Personal financial statements of owners

- Bank statements (last 3-6 months)

Here's a side-by-side look at key documentation differences:

| Document | U.S. (SBA 7a) | Canada (CSBFP) |

|---|---|---|

| Tax returns | Required (2-3 years) | Not always required |

| Vendor quotes | Not standard | Required for assets |

| Business plan | Required | Required |

| Financial projections | Required | Required |

| Legal/registration docs | Required | Required |

Reviewing business loan tips before you compile your package can highlight gaps you might overlook. It's also worth reading about documentation mistakes that commonly delay or derail applications.

Pro Tip: Scan every document and organize them into clearly labeled digital folders before your first lender meeting. Lenders who receive clean, complete digital packages process applications faster, and that speed can work in your favor.

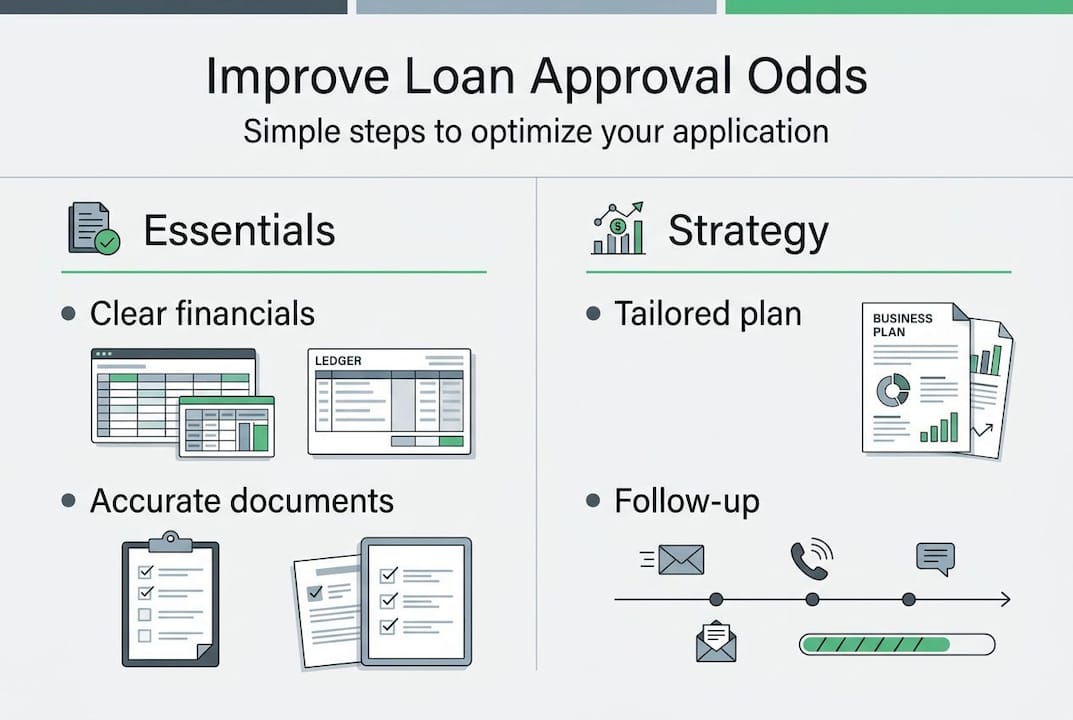

Craft a compelling business plan with strong financials

Proper documents are the foundation. Next, it's time to build a business plan that stands out and convinces lenders you're set for success. A business plan is not just a formality. It's your primary tool for demonstrating that you understand your market, your numbers, and your path to repayment.

A loan-ready business plan includes these core elements:

- Executive summary: A concise overview of your business, its purpose, and the funding request

- Market analysis: Data-backed research on your target customers, competitors, and industry trends

- Revenue projections: Month-by-month forecasts for at least 12-24 months, tied to real assumptions

- Cash flow statements: Showing that income will consistently cover operating costs and loan payments

- Supporting financials: Historical profit and loss statements, balance sheets, and tax returns

Strong cash flow and detailed projections are among the most critical factors lenders evaluate. Projections that are not grounded in real data raise red flags immediately. Use your actual sales history, industry benchmarks, and confirmed contracts to build credible numbers.

"Weak cash flow is the most common reason lenders deny small business loan applications, accounting for 41% of CSBFP denials in Canada alone."

This statistic matters because it points to something fixable. If your cash flow looks thin on paper, address it directly in your plan. Explain seasonal patterns, upcoming contracts, or cost reductions that will improve the picture. Lenders appreciate transparency over optimism.

To increase approval odds, make sure every projection connects back to a real data point. Avoid round numbers that look estimated. If you're unsure what's causing concern, reviewing reasons for denial can help you identify and fix weak spots before submission.

Tailor your approach for your business type and situation

Not every business fits the typical profile. Let's cover how to navigate special cases and adjust your strategy based on your specific situation. Your loan strategy should match where your business actually is, not where you hope it will be.

Startups vs. established businesses:

- Startups with limited history should target SBA Express or microloans, which have more flexible requirements

- Established businesses with two or more years of financials are better positioned for standard SBA 7(a) or CSBFP loans

- In Canada, most CSBFP loans go to newer businesses, but denial rates rise with loan size or weak cash flow

- If you've been in business less than a year, focus on building a strong business plan and demonstrating early revenue traction

If your industry is high risk or excluded:

- Confirm eligibility before applying. Gambling, certain financial services, and speculative real estate are typically excluded from SBA programs

- Explore alternative lenders or industry-specific programs if government-backed options are unavailable

- Consider a merchant cash advance or business line of credit as a bridge while you build your profile

Collateral and personal guarantees:

- Large loans almost always require collateral, such as equipment, real estate, or inventory

- Personal guarantees are standard for most SBA loans and many CSBFP applications

- If you lack collateral, look into unsecured microloan programs or online lenders with revenue-based underwriting

Reviewing loan fit considerations can help you match your situation to the right product before you apply.

Pro Tip: If your FICO score falls between 500 and 650, don't give up. Microloans and online lenders often have more flexible credit requirements and can help you build the track record needed for larger loans later.

Review, submit, and avoid common mistakes

With your strategy in place, it's time to finalize, review, and make sure you avoid the issues that cause most denials. A strong application can still fail at the last step if you rush the submission or overlook a key detail.

Use this checklist before you hit submit:

- Verify that all financial documents are current and match across every form

- Confirm your industry is eligible for the specific loan program you're applying to

- Check that your cash flow projections are realistic and supported by actual data

- Ensure your business plan includes a clear repayment strategy

- Review all personal financial statements for accuracy

- Confirm that collateral or personal guarantee documentation is included if required

Weak cash flow details and incomplete paperwork are the top two causes of denial across both U.S. and Canadian programs. Don't let either one derail your application at the finish line.

For U.S. applicants, note that personal guarantees are required for loans over $50,000 in most cases. Make sure your guarantor documentation is complete and accurate before submission.

Avoiding financing mistakes at this stage is just as important as the preparation work you've already done. Once approved, understanding how to use loan funds strategically will help you maximize the impact of your funding.

Pro Tip: After submitting, follow up with your lender within five to seven business days. A brief, professional check-in shows initiative and keeps your application top of mind during the review process.

Our perspective: What actually moves the needle in loan approvals

After working with small business owners across hundreds of industries since 2009, we've seen a clear pattern. The applications that succeed are not always the ones with the best numbers. They're the ones that tell the most credible story.

Lenders read dozens of applications every week. They can spot a business plan that was inflated to look good versus one built on honest assumptions. Conservative forecasting, where you show you've planned for slower months and unexpected costs, signals maturity and builds trust. Optimistic projections with no downside planning often do the opposite.

Financial storytelling matters. Your numbers need to make sense as a narrative. Revenue goes up because of a new contract. Costs increase because you're hiring. Repayment is feasible because your margins are stable. When the story holds together, lenders feel confident.

We also see many owners underestimate the value of post-submission follow-up. A short, professional email a week after submitting can keep your file active and signal that you're serious. Understanding why banks reject business funding often comes down to perception as much as paperwork. Make sure yours sends the right message.

Ready to apply? Resources and solutions for your next step

Armed with proven tips and pitfalls to avoid, you're now ready for the next step toward securing business funding. Capital for Business has helped thousands of small business owners across the U.S. and Canada find the right funding solution, even when traditional banks said no.

Whether you're comparing easy business loan options or want to understand how a merchant cash advance workflow fits your cash flow cycle, we have the resources to guide your decision. Our team works quickly and efficiently to match you with funding that fits your industry, your timeline, and your goals. Explore our full range of business funding solutions and take the next step with confidence. We've been doing this since 2009, and we're ready to help you move forward.

Frequently asked questions

What credit score do I need to optimize my small business loan application?

For most SBA loans, a FICO score of 650 or higher is recommended. However, SBA Express and microloans may accept scores as low as 500 for qualified applicants.

What is the most common reason business loan applications are denied?

Weak cash flow is the leading cause of denial for both U.S. and Canadian applicants. In Canada, 41% of CSBFP denials are directly tied to insufficient cash flow documentation.

What documents do I need for a small business loan in the U.S. and Canada?

Key documents include recent tax returns, a detailed business plan with projections, profit and loss statements, and balance sheets. Canadian applicants also need vendor quotes for assets when purchasing equipment or real estate.

Are startups eligible for government-backed loans?

Yes. In the U.S., startups can apply for SBA Express or microloans. In Canada, most CSBFP loans are actually granted to businesses less than one year old.

Do I need collateral for a small business loan?

For loans over $50,000 in the U.S., personal guarantees and collateral are typically required. Larger loans in Canada also carry higher scrutiny and denial rates without sufficient assets to back the request.

Recommended

- Master Business Loan Application Workflow for Success

- Considerations before signing up for a Small Business Loan

- 7 Ways You Can Use Your Business Loan | Capital for Business

- How to Apply for Business Loans in Canada 2026: Boost Approval 40%

- Leading Business Loan Provider l Loan Applications in Less Than 3 Days