Navigating the world of small business lending can feel like learning a foreign language. Terms like collateral, amortization, and debt service coverage ratio often confuse entrepreneurs seeking funding, creating barriers to accessing capital. This confusion can lead to missed opportunities, unfavorable loan terms, or even rejected applications. Understanding the terminology used by lenders transforms you from an uncertain applicant into a confident borrower who can evaluate options, negotiate terms, and secure the right funding for your business needs.

Table of Contents

- Understanding Core Lending Terms Every Small Business Owner Should Know

- Types Of Small Business Loans And Their Specific Terminology

- Decoding Loan Application And Approval Terminology To Boost Your Funding Chances

- How Understanding Lending Jargon Can Optimize Your Business Loan Use And Repayment

- Explore Tailored Small Business Loan Options With Capital For Business

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Terminology knowledge improves approval odds | Understanding lending terms helps you present accurate information and demonstrate preparedness to lenders |

| Different loan types use specific vocabulary | Each funding option from unsecured loans to merchant cash advances has unique terminology you should master |

| Application terms directly impact your experience | Familiarity with credit scores, collateral valuation, and financial ratios streamlines the approval process |

| Repayment vocabulary prevents costly mistakes | Knowing amortization schedules, prepayment penalties, and APR variations helps optimize loan management |

| Industry language builds lender confidence | Speaking the same terminology as financial institutions positions you as a serious, informed business owner |

Understanding core lending terms every small business owner should know

Every lending conversation revolves around a handful of fundamental concepts that shape how loans work. Mastering these core terms gives you the foundation to understand more complex financing structures and make smart financial decisions for your business.

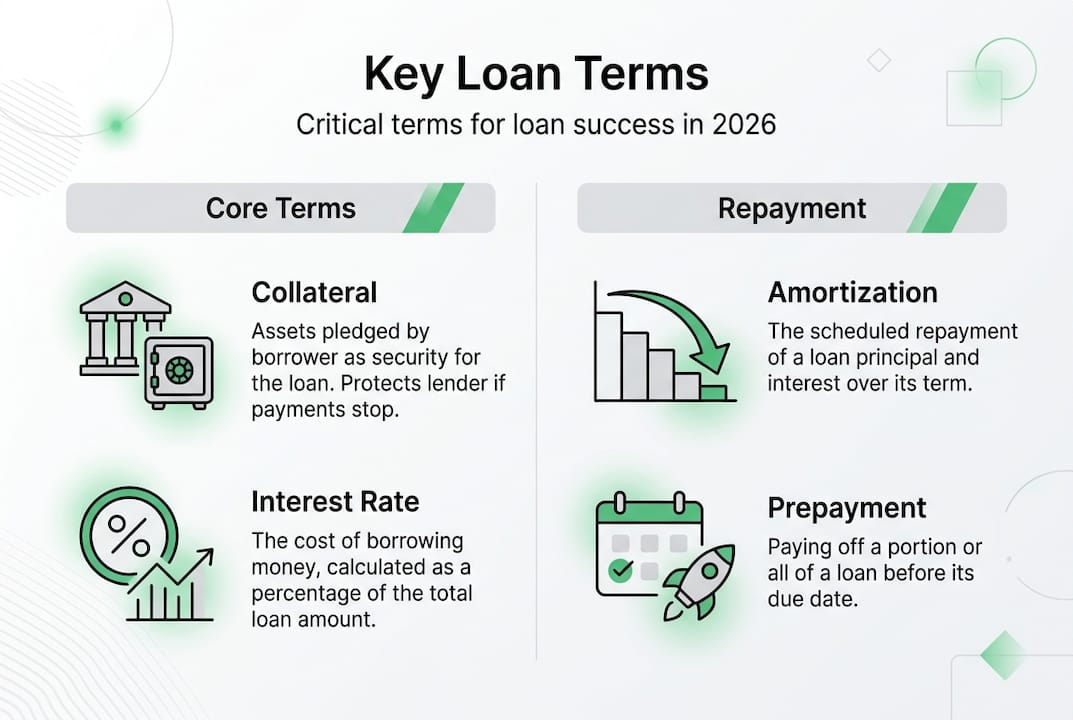

Collateral refers to assets you pledge as security for a loan. If you default on payments, the lender can seize these assets to recover their money. Common collateral includes real estate, equipment, inventory, or accounts receivable. Unsecured loans, by contrast, require no collateral but typically come with higher interest rates to offset the lender's increased risk.

The interest rate represents the cost of borrowing money, expressed as a percentage of the principal. Your principal is the original loan amount before interest accrues. Together, these determine your total repayment obligation. Term length specifies how long you have to repay the loan, ranging from a few months for short term working capital to several years for equipment financing.

Here are essential terms you will encounter repeatedly:

- Principal: The base loan amount you borrow before any interest or fees

- Interest rate: The percentage charged on your outstanding balance, either fixed or variable

- Term: The duration of your loan agreement, affecting both payment size and total interest paid

- Collateral: Physical or financial assets securing the loan against default

- Unsecured loan: Financing that requires no collateral but relies on creditworthiness alone

- APR (Annual Percentage Rate): The true cost of borrowing including interest and fees, expressed annually

- Default: Failure to meet loan obligations, triggering penalties or collateral seizure

Small business loan applicants benefit from understanding terms such as collateral, interest rate, and term. This knowledge helps you compare offers accurately and avoid surprises during repayment. When a lender quotes a 12% APR on a 36 month term with monthly payments, you should immediately understand the total cost structure and repayment schedule.

Pro Tip: Ask lenders to define any unfamiliar terms in plain language before signing up for small business loan agreements. A reputable lender welcomes questions and provides clear explanations, while evasiveness might signal unfavorable terms hidden in jargon.

Types of small business loans and their specific terminology

Different financing products come with specialized vocabulary that reflects their unique structures and purposes. Understanding these distinctions helps you identify which funding type aligns with your business situation and communicate effectively with potential lenders.

Knowing the distinctions between loans like unsecured loans and equipment financing is vital. Each loan category serves specific business needs and carries terminology that reflects its structure. Working capital loans provide short term cash flow support, often using terms like factor rate instead of traditional interest rates. Equipment financing uses the purchased equipment as collateral, introducing terms like residual value and depreciation schedules.

Merchant cash advances represent a unique funding model where businesses receive upfront capital in exchange for a percentage of future credit card sales. This structure uses terminology like holdback percentage (the portion of daily sales remitted) and factor rate (the multiplier determining total repayment). Unlike traditional loans, merchant cash advances do not have fixed payment schedules, making them flexible but potentially expensive.

Here is how common loan types differ in purpose and key terminology:

| Loan Type | Typical Use | Key Terminology |

|---|---|---|

| Unsecured business loan | General business expenses without collateral | Credit score, personal guarantee, debt to income ratio |

| Equipment financing | Purchasing machinery or vehicles | Residual value, depreciation, secured interest |

| Merchant cash advance | Quick cash flow based on card sales | Factor rate, holdback percentage, remittance |

| Working capital loan | Short term operational expenses | Revolving credit, draw period, factor rate |

| Business line of credit | Flexible access to funds as needed | Draw period, credit limit, utilization rate |

Each loan type has advantages tied to specific business scenarios. Unsecured loans offer speed and simplicity for established businesses with strong credit profiles. Equipment financing spreads costs over the asset's useful life while building equity. Merchant cash advances provide rapid funding when traditional lenders decline applications, though at premium costs.

The terminology differences matter when comparing offers. A merchant cash advance quoting a 1.3 factor rate might seem cheaper than a loan at 15% APR, but the factor rate applies to the entire advance amount regardless of repayment speed. Understanding this distinction prevents costly misunderstandings. Explore equipment leasing vs financing to grasp how these options differ in ownership, tax treatment, and long term costs.

Pro Tip: Match loan terminology to your business model. If you process significant credit card volume, understanding merchant cash advance terms gives you access to funding that traditional lenders might not offer.

Decoding loan application and approval terminology to boost your funding chances

The application process introduces its own vocabulary that directly affects approval odds and loan terms. Lenders use specific metrics to evaluate risk, and understanding these measurements helps you present your business in the strongest possible light.

Familiarity with approval terms like credit score, debt service coverage ratio, and financial statements improves application success. Your personal and business credit scores quantify creditworthiness on numerical scales, with higher scores unlocking better rates and terms. Lenders typically require scores above 650 for favorable consideration, though alternative lenders may accept lower scores with adjusted terms.

Debt service coverage ratio (DSCR) measures your ability to service debt from operating income. Calculate it by dividing net operating income by total debt obligations. A DSCR above 1.25 indicates healthy cash flow to cover loan payments with cushion for fluctuations. Lenders view this metric as a primary indicator of repayment capacity, often weighing it more heavily than credit scores for established businesses.

Collateral valuation determines how much lenders will advance against pledged assets. Most lenders apply loan to value (LTV) ratios between 70% and 85%, meaning they will lend 70 to 85 cents per dollar of appraised collateral value. This protects them against value depreciation and liquidation costs if they must seize assets. Understanding LTV helps you estimate available funding before applying.

A personal guarantee makes you personally liable for business debt if the company cannot repay. This common requirement for small business loans means lenders can pursue your personal assets if the business defaults. While this increases your risk, it also demonstrates commitment to lenders and often secures better terms than purely corporate guarantees.

Here are the typical steps in the loan application process with key terminology at each stage:

- Pre qualification: Initial assessment using basic financials to estimate approval odds and potential terms without affecting credit scores

- Application submission: Formal request including detailed financial statements, tax returns, and business plans with specific funding requests

- Underwriting: Lender's detailed analysis of creditworthiness, collateral, cash flow, and risk factors using standardized criteria

- Approval or conditional approval: Positive lending decision, potentially requiring additional documentation or conditions before funding

- Closing: Final signing of loan documents, pledge of collateral, and disbursement of funds to your business account

- Servicing: Ongoing loan management including payment processing, account maintenance, and communication about any changes

Pro Tip: Prepare your documents and understand lender requirements before applying to streamline approval. Having organized financial statements, tax returns, and business plans ready demonstrates professionalism and speeds up underwriting. Review small business loan options to identify which documentation each loan type typically requires.

How understanding lending jargon can optimize your business loan use and repayment

Once you secure funding, terminology knowledge continues delivering value by helping you manage the loan efficiently and avoid expensive mistakes. The repayment phase introduces concepts that affect your total costs and financial flexibility.

Clarity on terms like amortization, prepayment penalties, and interest compounding helps manage repayments effectively. Amortization refers to the gradual reduction of loan principal through scheduled payments that include both interest and principal portions. Early payments consist mostly of interest, with principal reduction accelerating over time. Understanding your amortization schedule shows exactly when you will achieve significant principal paydown.

Prepayment penalties charge fees if you repay a loan before its scheduled maturity. Lenders impose these to recoup lost interest income when borrowers refinance or pay off loans early. Some loans allow partial prepayments without penalty up to a certain percentage annually. Always clarify prepayment terms before signing, especially if you anticipate strong cash flow that could enable early payoff.

Fixed APR remains constant throughout the loan term, providing predictable payments that simplify budgeting. Variable APR fluctuates based on market indices like the prime rate, potentially lowering costs when rates fall but increasing payments when rates rise. Your risk tolerance and market outlook should guide this choice.

Interest compounding frequency affects total costs significantly. Daily compounding accrues interest on previously charged interest more frequently than monthly compounding, increasing total payments. Simple interest, calculated only on the principal balance, costs less than compound interest over identical terms.

Here are best practices informed by terminology comprehension:

- Review your amortization schedule quarterly to track principal reduction and ensure payments apply correctly

- Calculate the true cost of prepayment penalties before refinancing to confirm savings exceed fees

- Monitor variable rate loans monthly and consider refinancing to fixed rates if market trends suggest rising costs

- Request simple interest structures when possible to minimize total interest paid over the loan term

- Understand your payment allocation between principal and interest to optimize tax deductions and equity building

- Track accounting standards for loans to ensure proper financial statement treatment

This table illustrates cost differences between loan conditions:

| Loan Feature | Option A | Option B | Cost Difference |

|---|---|---|---|

| $50,000 loan at 10% APR | 36 month term | 60 month term | $2,340 more interest for longer term |

| Prepayment penalty | 3% of balance | None | $1,500 penalty on early payoff of $50,000 |

| Interest type | Compound daily | Simple interest | $890 more over 36 months with compounding |

| Rate structure | Fixed 12% APR | Variable starting 10% | Potential $3,200 increase if rates rise 2% |

These differences add up quickly, making terminology knowledge financially valuable. A business owner who understands these concepts can negotiate best loan conditions and select products that minimize total costs while meeting operational needs.

Explore tailored small business loan options with capital for business

Now that you understand the terminology that shapes lending decisions, you can confidently explore funding options that match your business needs. Capital For Business has served small business owners since 2009, offering diverse loan products designed for real world business challenges.

Whether you need working capital to manage seasonal fluctuations, equipment financing to upgrade operations, or a merchant cash advance for rapid access to funds, having the vocabulary to discuss these options positions you for success. Our team speaks your language and works with businesses across hundreds of industries nationwide and in Canada.

We understand that banks and credit unions often fail small businesses with rigid requirements and slow processes. That is why we have built a platform that delivers funding quickly, efficiently, and at prices you can afford. Explore easy small business loans to see how different products address specific business scenarios, from expansion to cash flow management.

Our comprehensive business funding solutions include small business loans, working capital, merchant cash advance, credit card processing, equipment financing, and business lines of credit. Armed with the terminology knowledge from this guide, you can evaluate which solution fits your situation and communicate your needs effectively to our lending specialists.

FAQ

What are some common small business lending terms I should memorize?

Prioritize understanding collateral (assets securing loans), interest rate (borrowing cost percentage), unsecured loan (no collateral required), and amortization (gradual principal reduction through payments). These terms appear in virtually every lending conversation. Additional important concepts include APR (total borrowing cost), term length (repayment duration), and principal (original loan amount). Mastering these basics prepares you for more complex discussions about specific loan products and structures.

How does understanding loan terminology affect my chances of approval?

Clear understanding helps you provide accurate information and demonstrate preparedness to lenders, who perceive informed borrowers as lower risk. When you speak confidently about debt service coverage ratios, collateral valuation, and financial metrics, you signal business sophistication that increases lender comfort. This knowledge also helps you present your business in the strongest light by emphasizing metrics that matter most to underwriters. Lenders approve applications from prepared borrowers more frequently and often offer better terms.

Can I negotiate loan terms if I understand the terminology?

Yes, knowing terms like APR, prepayment penalties, and amortization gives you leverage to negotiate better conditions. Understanding the difference between fixed and variable rates helps you request structures that match your risk tolerance. When you can calculate how prepayment penalties affect total costs, you can negotiate their removal or reduction. This knowledge enables meaningful discussions about loan covenants, collateral requirements, and fee structures that less informed borrowers simply accept as presented.

Where can I learn more about specific loan types and processes?

Explore detailed guides on small business loan options to understand different funding products and their ideal use cases. The comprehensive business loan terminology explained resource provides deeper definitions and practical examples. Review considerations for small business loans before applying to ensure you have evaluated all factors affecting your decision. These resources build on the foundation established in this guide and prepare you for confident lending conversations.