TL;DR:

- A cash advance fee is an upfront charge applied when you withdraw cash against your credit line. The total cost of such advances includes high interest, additional transaction fees, ATM surcharges, and foreign transaction fees, making them expensive. Small business owners should consider alternatives like a business line of credit or merchant cash advance to reduce borrowing costs.

A cash advance fee is an upfront charge your credit card issuer applies the moment you withdraw cash against your credit line. Explaining cash advance fees matters because these costs stack quickly. You pay a transaction fee, then interest starts accruing immediately at a rate higher than your regular purchase APR, with no grace period to pay it off before charges begin. The Consumer Financial Protection Bureau classifies cash advances as a distinct borrowing category, separate from standard purchases. Capitalforbusiness works with small business owners every day who are surprised by how much a cash advance actually costs once all the layers are added up.

What fees and interest rates apply to credit card cash advances?

Credit card cash advances carry two primary costs: a transaction fee and an ongoing interest charge. Cash advance fees average 4.03% of the amount withdrawn, with most issuers charging between 3% and 5%. A minimum flat fee of $5 to $10 applies when the percentage calculation falls below that floor.

The interest rate on a cash advance is almost always higher than your card's purchase APR. Cash advance APRs average 24.48%, compared to the lower rates most cardholders see on regular purchases. That gap matters because the interest clock starts the second the transaction posts.

Unlike standard credit card purchases, cash advances carry no grace period. With a regular purchase, you can pay your balance in full by the due date and owe zero interest. With a cash advance, interest accrues from day one regardless of when you pay. A $5,000 cash advance at 24.48% APR costs roughly $102 in interest for the first month alone, before you factor in the upfront fee.

Here is a breakdown of the typical fee structure:

| Fee Type | Typical Range | Notes |

|---|---|---|

| Transaction fee | 3%–5% of amount | Minimum $5–$10 applies |

| Cash advance APR | ~24.48% average | Starts accruing immediately |

| ATM owner fee | $2–$5 per transaction | Charged by the ATM operator |

| Foreign transaction fee | 1%–3% of amount | Applies to international withdrawals |

Pro Tip: If your cash need is small, the flat minimum fee can actually cost you more on a percentage basis than the stated rate. A $50 withdrawal with a $10 minimum fee equals a 20% upfront cost before interest.

Most business owners focus on the percentage fee and miss the ATM surcharge. Non-affiliated ATM fees range from $2 to $5, and foreign transaction fees add another 1% to 3% on top of the advance amount. These charges are separate from your card issuer's fees and show up as distinct line items on your statement.

How do cash advance costs compare to other short-term financing?

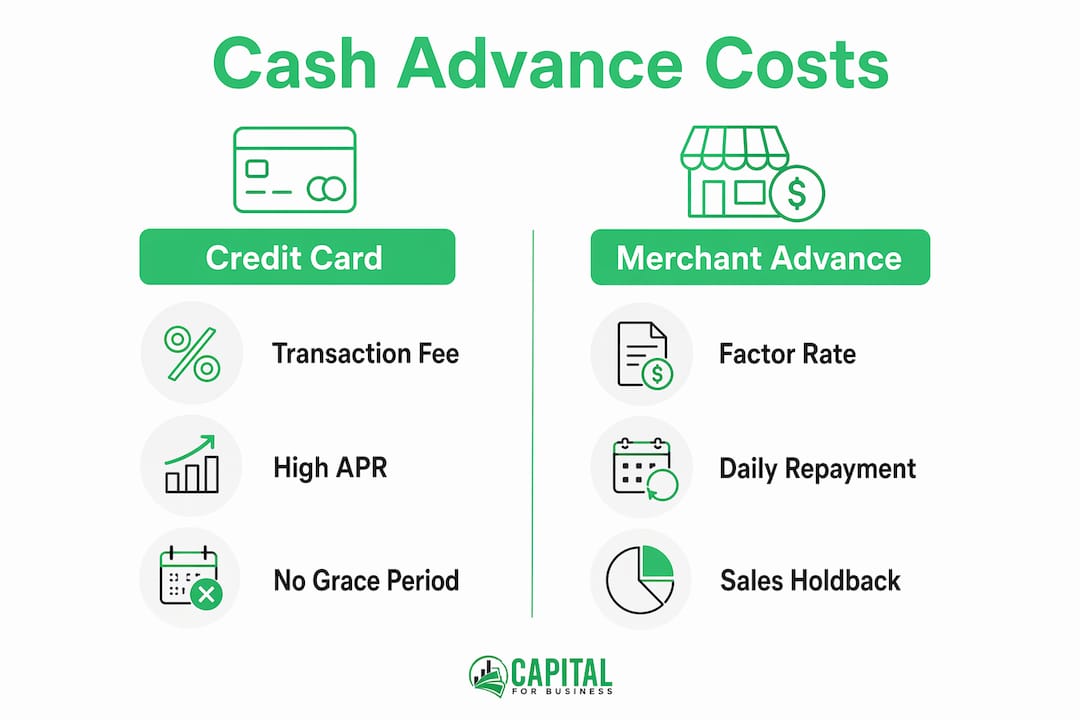

A credit card cash advance and a merchant cash advance share a name but operate very differently. Understanding the distinction helps you choose the right tool for your situation.

A credit card cash advance pulls money from your revolving credit line. You pay a transaction fee upfront, then interest at a high APR with no grace period. The total cost grows every day the balance stays unpaid. A merchant cash advance works differently. The provider advances a lump sum against your future sales, and repayment comes as a fixed percentage of daily card receipts.

Merchant cash advances use a factor rate instead of APR. A factor rate of 1.3 means you repay $1.30 for every $1.00 borrowed, regardless of how quickly you pay. That structure means paying off the balance early does not reduce your total cost the way it would with an interest-bearing loan. For a business with steady daily sales, the predictable repayment schedule can be easier to manage than a revolving credit card balance.

Here is a side-by-side comparison of key financing characteristics:

| Feature | Credit card cash advance | Merchant cash advance | Business line of credit |

|---|---|---|---|

| Cost structure | Fee + APR | Factor rate | Interest on drawn amount |

| Grace period | None | Not applicable | Varies by lender |

| Repayment | Monthly minimum | Daily sales holdback | Flexible draws |

| Early payoff benefit | Yes, reduces interest | No | Yes |

| Approval speed | Instant | Fast | Moderate |

Traditional small business loans carry lower interest rates than either cash advance type, but they require more documentation and take longer to fund. A business line of credit sits in the middle. You draw only what you need, pay interest only on the drawn balance, and repay on a schedule that fits your cash flow.

The core issue with credit card cash advances is compounding cost. You pay a fee on day one, then interest on the fee plus the principal from day one forward. A $10,000 advance with a 4% fee and a 24.48% APR costs $400 upfront, then roughly $204 in interest per month if you carry the full balance. Over three months, that totals more than $1,000 in financing costs on a $10,000 draw.

What hidden costs can increase the total expense of a cash advance?

The headline fee and APR are only part of the story. Several less obvious costs can push the true expense of a cash advance well above what the initial numbers suggest.

-

Interest on the fee itself. Fees are added to your principal balance immediately, so you pay interest on the fee from day one. A $400 fee on a $10,000 advance means your interest-bearing balance starts at $10,400, not $10,000.

-

ATM surcharges. Using an out-of-network ATM adds a $2 to $5 charge from the ATM operator. This is separate from your card issuer's fee and does not count toward your advance limit.

-

Foreign transaction fees. Withdrawing cash abroad triggers a 1% to 3% foreign transaction fee on top of the standard cash advance fee. A $2,000 withdrawal overseas could carry $40 to $60 in foreign transaction charges alone.

-

Convenience check and balance transfer classifications. Convenience checks and balance transfers can be classified as cash advances, triggering the same high fees and APR. Many business owners write a convenience check thinking it works like a regular purchase, then find a cash advance fee on their next statement.

-

Late fees on carried balances. Carrying a cash advance balance increases your minimum payment. Missing that payment adds a late fee, typically $25 to $40, and can trigger a penalty APR on the entire account.

-

Effective APR versus stated APR. Financial calculators reveal that layered fees and immediate interest push the effective APR far above the stated rate. A 24.48% stated APR combined with a 4% upfront fee and no grace period can translate to an effective annual cost well above 30% on short-term draws.

Pro Tip: Read your cardholder agreement before taking a cash advance. Look specifically for the section on "cash-equivalent transactions." Many issuers classify money orders, lottery tickets, and cryptocurrency purchases as cash advances, triggering fees you did not expect.

The practical takeaway is that the true cost of a cash advance is almost always higher than the stated APR suggests. Using an effective APR calculator before you borrow gives you a realistic picture of what you will actually pay.

How can small business owners manage or minimize cash advance costs?

Managing cash advance costs starts with borrowing intentionally. A few specific practices can meaningfully reduce what you pay.

-

Borrow only what you need. The transaction fee is percentage-based above the minimum threshold. Borrowing $500 instead of $1,000 cuts your fee in half and reduces the interest-bearing balance from day one.

-

Consolidate your cash needs into one transaction. Each separate cash advance triggers a new transaction fee. Taking one $2,000 advance costs less in fees than four separate $500 withdrawals.

-

Pay the balance as fast as possible. Because interest accrues daily with no grace period, every day you carry the balance adds cost. Paying off the advance within the first billing cycle dramatically reduces total interest paid.

-

Compare cards before you borrow. Cash advance fees and APRs vary by issuer. Some business credit cards charge lower cash advance APRs or waive the minimum fee for existing customers. Reviewing your card terms before you need cash gives you time to switch if your current card is expensive.

-

Explore alternatives before committing. A merchant cash advance may cost less for a business with consistent card sales. A business line of credit offers flexible access to funds at lower rates than most cash advances. Equipment financing covers specific asset purchases without touching your credit line.

Pro Tip: If you regularly need short-term cash for operations, a business line of credit is almost always cheaper than repeated credit card cash advances. The interest rate is lower, there is a grace period on draws, and you only pay for what you use.

The cost differences between merchant cash advances and credit card advances are significant enough to justify a direct comparison before you decide. A factor rate of 1.2 to 1.5 on a merchant cash advance may look expensive, but the absence of compounding daily interest can make it cheaper over a 6-month repayment window than a credit card advance at 24.48% APR.

Key Takeaways

Cash advance fees are a layered cost structure that combines upfront transaction fees, immediate high-APR interest, and additional charges that together make credit card cash advances one of the most expensive short-term borrowing options available to small business owners.

| Point | Details |

|---|---|

| Transaction fee range | Cash advance fees average 4.03%, with a minimum flat fee of $5–$10 per transaction. |

| No grace period | Interest at an average APR of 24.48% starts accruing the day the advance posts. |

| Hidden cost layers | ATM fees, foreign transaction fees, and interest on the fee itself all add to the true cost. |

| Effective APR is higher | Layered fees push the real annualized cost above the stated APR on short draws. |

| Alternatives exist | Business lines of credit and merchant cash advances often cost less than repeated cash advances. |

What I have learned from watching business owners use cash advances

Most business owners who take a credit card cash advance do not realize they are borrowing money at a rate that rivals some payday loan products. They see the credit limit, they see the ATM, and they assume the cost is roughly the same as carrying a balance on a purchase. It is not.

The detail that catches people most off guard is the fee-on-fee structure. The fee becomes part of your principal, so you pay interest on it from day one. On a $10,000 advance, that means your interest meter starts at $10,400. Over 90 days at 24.48% APR, the difference is not trivial.

The second thing I have seen consistently is that business owners treat cash advances as a quick fix without a repayment plan. They take the advance, cover the immediate need, and then carry the balance for months because cash flow stays tight. That is when the cost becomes genuinely damaging. A $5,000 advance carried for six months at 24.48% APR costs over $600 in interest alone, plus the upfront fee.

My honest recommendation is this: use a cash advance only when you have a clear, short repayment window and no cheaper option available. If you need cash regularly, build a business line of credit or explore a merchant cash advance before you reach for the ATM. The difference in total financing cost over a year can be substantial.

— Capital

Capitalforbusiness funding options worth knowing about

Credit card cash advances solve an immediate problem, but they are rarely the most cost-effective path for a small business. Capitalforbusiness has worked with business owners across hundreds of industries since 2009, and the pattern is consistent: owners who plan their financing ahead of time pay far less than those who rely on emergency cash advances.

Capitalforbusiness offers small business loans and funding solutions designed for the way small businesses actually operate. From merchant cash advances to business lines of credit and equipment financing, the options are structured to fit your cash flow rather than strain it. Rates are competitive, repayment terms are clear, and the application process is built for speed. If you want to understand which funding solution fits your business, Capitalforbusiness is ready to help you find it.

FAQ

What is a cash advance fee on a credit card?

A cash advance fee is an upfront charge applied when you withdraw cash from your credit line, typically 3% to 5% of the amount or a minimum flat fee of $5 to $10, whichever is greater.

Does interest on a cash advance start immediately?

Yes. Cash advance interest accrues from the transaction date with no grace period, unlike regular credit card purchases where you can avoid interest by paying in full each month.

Are convenience checks considered cash advances?

Convenience checks are classified as cash advances by most card issuers, triggering the same transaction fees and higher APR as an ATM withdrawal.

How is a merchant cash advance different from a credit card cash advance?

A merchant cash advance uses a fixed factor rate and repays through daily sales holdbacks, while a credit card cash advance charges a percentage fee plus compounding daily interest at a high APR.

What is the most cost-effective alternative to a credit card cash advance for a small business?

A business line of credit or a merchant cash advance typically costs less than a credit card cash advance for most small business needs, because both offer lower effective rates and more predictable repayment structures.