Small business financing has shifted dramatically. In 2026, 74% of small businesses prefer non-bank lenders over traditional banks, prioritizing speed and accessibility. Fintech and alternative lenders now dominate the landscape, while government programs and AI adoption reshape how businesses secure capital. Understanding these evolving trends helps you navigate financing options strategically, whether you're seeking working capital, equipment funding, or expansion loans. This guide clarifies key borrower profiles, approval patterns, and practical strategies for financing success in 2026.

Table of Contents

- Fintech And Alternative Lenders Reshaping Small Business Financing

- Understanding Borrower Profiles And Loan Approval Trends In 2026

- Canadian Market Spotlight: Government-Backed Loans And Alternative Lending Growth

- Top Challenges And The Role Of Technology For Business Financing Growth

- Explore Tailored Financing Solutions For Your Business

- Frequently Asked Questions About Business Financing Trends 2026

Key takeaways

| Point | Details |

|---|---|

| Non-bank preference | 74% of small businesses choose alternative lenders for faster funding over traditional banks. |

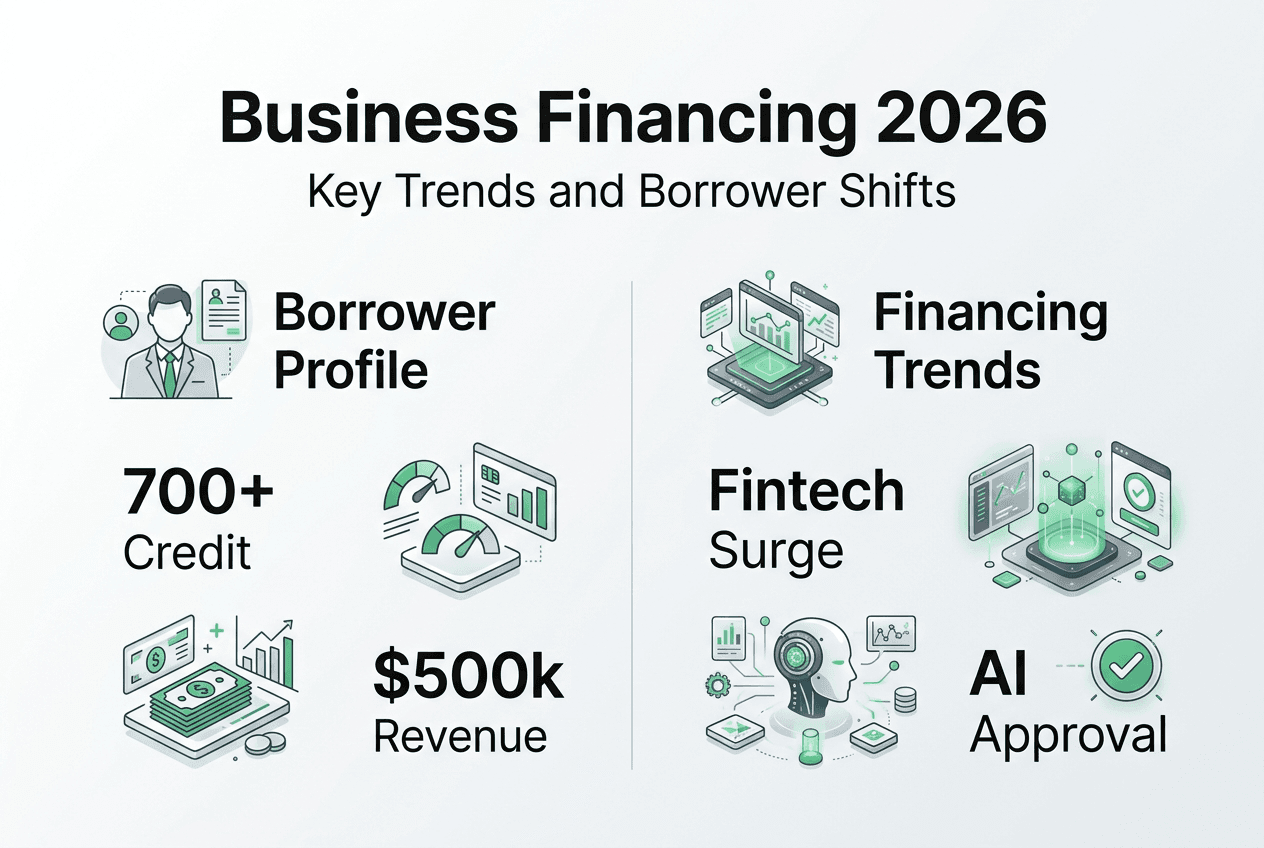

| Borrower profile | Approved applicants typically have 700+ credit scores and at least 7 years in business. |

| Primary loan use | Working capital accounts for 65% of funded loans in 2026. |

| Canadian growth | Alternative lending expanded 200% as banks maintain conservative lending standards. |

| AI influence | 56% of US small businesses use AI technology, impacting financing strategies. |

Fintech and alternative lenders reshaping small business financing

Fintech platforms have fundamentally changed how small businesses access capital. Non-bank lenders are preferred by 74% of businesses specifically for their speed advantage over traditional banks. These platforms leverage artificial intelligence and automated underwriting to process applications in hours rather than weeks, dramatically reducing the friction that historically plagued business lending.

Traditional banks continue operating with conservative lending standards, requiring extensive documentation and lengthy approval processes. Their risk assessment models often exclude newer businesses or those with non-traditional revenue patterns. Meanwhile, fintech lenders analyze alternative data sources like cash flow patterns, online sales metrics, and customer reviews to evaluate creditworthiness more holistically.

The advantages fintech lenders offer include:

- Approval decisions within 24 to 48 hours instead of weeks

- Flexible qualification criteria beyond traditional credit scores

- Minimal paperwork through digital document uploads

- Broader acceptance of diverse business models and industries

- Transparent fee structures displayed upfront

Pro Tip: Maintain organized digital financial records including bank statements, invoices, and tax returns in cloud storage. AI-based underwriting systems can access and analyze these documents instantly, accelerating your approval timeline significantly.

"The technology in small business lending ecosystem has matured beyond simple automation. Machine learning algorithms now predict repayment likelihood with greater accuracy than traditional models, enabling lenders to serve previously underserved markets."

This transformation doesn't mean traditional banks have disappeared. They still serve businesses with established credit histories and substantial collateral. However, the competitive landscape now offers entrepreneurs multiple pathways to capital. Understanding which lender type aligns with your business profile and timeline needs becomes crucial for business financing tips 2026 success.

The speed advantage extends beyond initial approval. Fintech platforms typically disburse funds within 48 hours of approval, while banks may require additional weeks for final documentation and fund transfer. For businesses facing immediate opportunities or cash flow gaps, this timing difference can determine success or failure. Exploring financing alternatives insights reveals how various industries adapt these solutions to their specific needs.

Understanding borrower profiles and loan approval trends in 2026

Successful loan applicants in 2026 share distinct characteristics. Approved borrowers typically have personal credit scores of 700+, with a median of 7 years in business operation. These benchmarks reflect lender risk tolerance, though alternative lenders show more flexibility than traditional banks. Understanding these profiles helps you assess your readiness and identify areas for improvement before applying.

The median approval covers approximately 75% of the requested funding amount. This gap between request and approval means you should apply for slightly more than your minimum need, anticipating potential reductions. Working capital remains the primary use for 65% of funded loans, followed by equipment purchases, expansion projects, and inventory management.

Interestingly, 22% of approvals go to businesses generating under $500,000 in annual revenue. This statistic challenges the assumption that only established, high-revenue businesses qualify for financing. Alternative lenders particularly serve this segment, evaluating growth potential and cash flow patterns rather than solely historical revenue.

| Metric | Traditional Banks | Alternative Lenders | | --- | --- | | Minimum credit score | 680-720 | 600-650 | | Years in business | 2-3 years | 6-12 months | | Approval rate | 25-30% | 45-55% | | Average funding amount | $50,000-$250,000 | $10,000-$150,000 | | Time to funding | 30-90 days | 1-7 days |

Several factors influence approval likelihood beyond credit scores and business age:

- Consistent monthly revenue demonstrating stable cash flow

- Debt-to-income ratio below 40% showing manageable existing obligations

- Industry risk profile with some sectors considered higher risk

- Collateral availability for secured loan products

- Clear business plan articulating how funds will generate returns

Pro Tip: Build your years-in-business metric strategically. Even if you restructured or rebranded, maintaining the same tax identification number preserves your operational history. Additionally, focus on improving personal credit scores through timely payments and reducing credit utilization below 30%.

The small business loan borrower criteria landscape rewards preparation. Businesses that proactively address weak areas like inconsistent revenue or limited credit history position themselves for better terms and higher approval rates. Many successful applicants spend 3 to 6 months strengthening their financial profile before formally applying.

Working capital loans dominate because they address universal business needs: managing seasonal fluctuations, covering payroll during slow periods, and seizing time-sensitive opportunities. Lenders view working capital requests favorably when applicants demonstrate clear cash flow cycles and realistic repayment projections tied to revenue patterns.

Canadian market spotlight: government-backed loans and alternative lending growth

Canada's financing landscape presents unique opportunities through government programs and rapidly expanding alternative lending. The Canada Small Business Financing Program (CSBFP) provides government-backed loans fostering economic growth, reducing lender risk and improving access for businesses that might not qualify through conventional channels. This program has supported thousands of businesses across diverse industries since its inception.

Alternative lending has grown 200% in Canada as traditional banks maintain conservative lending standards. This explosive growth reflects both demand and supply factors. Banks tightened requirements following economic uncertainty, while fintech platforms recognized underserved market segments and deployed technology to serve them profitably. Approximately 40% of Canadian loan applications face rejection from traditional institutions, creating substantial opportunity for alternative providers.

The CSBFP and alternative lenders offer distinct benefits:

- CSBFP provides government guarantees reducing lender risk and interest rates

- Alternative lenders accept lower credit scores and shorter business histories

- CSBFP caps loan amounts at $1 million with favorable terms

- Alternative platforms offer faster approval and funding timelines

- Both options serve businesses excluded from traditional bank lending

To successfully apply for government-backed loans, follow these steps:

- Verify your business qualifies under CSBFP eligibility criteria including revenue limits and industry classifications

- Prepare comprehensive financial statements covering at least two years of operation

- Develop a detailed business plan explaining loan purpose and repayment strategy

- Gather required documentation including tax returns, bank statements, and ownership verification

- Approach participating lenders who administer CSBFP on behalf of the government

- Compare terms from multiple lenders as rates and fees vary despite government backing

| Feature | Traditional Banks | Alternative Lenders | CSBFP | | --- | --- | --- | | Interest rates | 6-9% | 12-30% | 5-8% | | Approval speed | 4-12 weeks | 1-5 days | 2-6 weeks | | Credit requirements | 680+ | 600+ | 650+ | | Maximum amount | $500k+ | $250k | $1M | | Collateral needed | High | Low to Medium | Medium | | Best for | Established businesses | Quick funding needs | Equipment/property |

The business loan applications canada 2026 process varies significantly by lender type. Traditional banks require extensive documentation and multiple meetings, while alternative lenders streamline applications through online portals. CSBFP applications involve additional government paperwork but offer superior terms for qualifying businesses.

Canadian entrepreneurs should evaluate all three channels based on their specific circumstances. A business seeking equipment financing might prioritize CSBFP's favorable rates and terms. One needing immediate working capital for a time-sensitive opportunity might choose alternative lenders despite higher costs. Understanding small business funding options canada helps match financing sources to business needs strategically.

Top challenges and the role of technology for business financing growth

Small business optimism remains strong with 94% projecting growth in 2026, yet significant challenges temper this outlook. Inflation ranks as the top concern for 31% of businesses, directly impacting operating costs, pricing strategies, and profit margins. Cash flow management troubles 29% of owners, often stemming from delayed customer payments, seasonal revenue fluctuations, or rapid growth straining working capital.

These challenges directly influence financing needs and strategies. Businesses facing inflation-driven cost increases seek working capital to bridge gaps between expense timing and revenue collection. Those managing cash flow volatility pursue lines of credit offering flexible access to funds during lean periods. Understanding how economic pressures translate into specific financing requirements helps you select appropriate products and structure applications effectively.

The top three challenges and their financing impact include:

- Inflation increasing operating costs requires working capital loans to maintain inventory levels and cover higher supplier prices without raising customer prices immediately

- Cash flow gaps from payment timing mismatches demand revolving credit lines providing flexible access during shortfalls

- Labor shortages and wage pressure necessitate equipment financing to automate processes and reduce dependence on scarce workers

Technology adoption accelerates as businesses seek competitive advantages. 56% of US small businesses use AI, primarily for marketing automation, customer service chatbots, and data analysis. This technological shift impacts financing in multiple ways. AI-driven insights help businesses forecast cash flow more accurately, strengthening loan applications with data-backed projections. Automated financial management reduces bookkeeping costs while maintaining the organized records lenders require.

Pro Tip: Leverage AI-powered accounting and cash flow forecasting tools before applying for financing. Lenders increasingly value data-driven financial projections over generic estimates. Present detailed monthly cash flow forecasts showing exactly how loan proceeds will generate sufficient revenue to cover repayment obligations.

The financing role in business growth extends beyond simply accessing capital. Strategic financing enables businesses to overcome challenges that would otherwise limit growth. A company facing cash flow issues might use a line of credit to accept larger orders requiring upfront material purchases. One combating labor shortages could finance automation equipment reducing headcount needs while increasing productivity.

Businesses successfully navigating 2026's challenges combine multiple strategies. They adopt technology improving operational efficiency, secure appropriate financing supporting growth initiatives, and maintain financial discipline ensuring sustainable expansion. The integration of smart financing strategies 2026 with broader business planning separates thriving companies from those merely surviving.

Understanding that challenges create financing opportunities rather than obstacles shifts your perspective. Each business challenge represents a specific problem that appropriate financing can help solve. Inflation squeezing margins might justify equipment loans enabling production efficiency gains. Cash flow volatility could warrant establishing a line of credit before emergencies arise. Framing financing as a strategic tool for overcoming challenges rather than a desperate measure improves both application success and fund utilization effectiveness.

Explore tailored financing solutions for your business

Navigating 2026's financing landscape requires understanding both trends and practical options suited to your specific needs. The insights covered demonstrate how financing sources, borrower expectations, and approval criteria have evolved. Now consider how these trends translate into actionable solutions for your business.

Capital for Business offers financing products designed for the realities small businesses face:

- Types of easy small business loans providing term financing for expansion, equipment, or major purchases with predictable repayment schedules

- Working capital loans addressing cash flow gaps, seasonal fluctuations, and growth opportunities requiring immediate funding

- Merchant cash advance options offering flexible repayment tied to daily sales, ideal for businesses with variable revenue patterns

Whether you're managing inflation pressures, seizing growth opportunities, or bridging cash flow gaps, exploring financing solutions aligned with your business profile and timeline needs positions you for success in 2026's competitive environment.

Frequently asked questions about business financing trends 2026

How can small businesses improve loan approval chances in 2026?

Focus on building personal credit above 700, maintaining at least 6 to 12 months of consistent revenue, and organizing financial documentation digitally. Lenders increasingly use AI to analyze cash flow patterns, so demonstrate stable monthly income and manageable debt levels. Review 2026 financing tips for detailed strategies.

What are the best alternative lenders for quick business funding?

Fintech platforms specializing in small business loans typically approve applications within 24 to 48 hours and disburse funds within a week. Look for lenders offering transparent fee structures, flexible qualification criteria, and positive reviews from businesses in your industry. Speed advantages make alternative lenders ideal for time-sensitive opportunities.

How is AI changing business loan applications?

AI analyzes alternative data sources beyond credit scores, including cash flow patterns, online reviews, and sales trends. This technology enables faster decisions, often within hours, and expands approval rates for businesses with limited credit history but strong operational metrics. Maintain organized digital financial records to benefit from AI-driven underwriting.

What government-backed loans are available to Canadian businesses in 2026?

The Canada Small Business Financing Program offers government-guaranteed loans up to $1 million for equipment, property, and leasehold improvements. Interest rates typically range from 5% to 8%, significantly lower than alternative lenders. Visit apply for business loans canada for application guidance.

What are the main challenges small businesses face when seeking financing this year?

Inflation-driven cost increases and cash flow volatility top the list, affecting 31% and 29% of businesses respectively. These challenges increase working capital needs while potentially weakening financial metrics lenders evaluate. Addressing these issues through improved cash flow forecasting and cost management strengthens loan applications significantly.