Traditional lenders often turn away startups and seasonal businesses, leaving many Canadian and American owners searching for options beyond banks. Finding reliable capital for growth can feel like a dead end when credit scores or business histories fall short. This guide explains what makes alternative funding distinct, highlights practical sources like crowdfunding and trade credit, and helps you identify the best path forward among options designed to meet real-world needs.

Table of Contents

- Defining Alternative Business Funding Options

- Popular Types and How They Differ

- Qualifying and Applying for Alternative Funding

- Weighing Costs, Risks, and Common Pitfalls

- Alternative vs. Traditional Lending Compared

Key Takeaways

| Point | Details |

|---|---|

| Alternative Funding Provides Flexibility | Unlike traditional financing, alternative funding sources cater to diverse business needs and do not heavily rely on credit scores. |

| Faster Access to Capital | Alternative lenders often approve and fund requests within days, addressing urgent financial needs quickly. |

| Variety of Funding Types | Business owners have numerous options, including debt-based, non-debt, and community-based funding, each with unique terms and considerations. |

| Consider Costs and Risks | Alternative funding generally has higher costs than traditional loans; understanding these before borrowing is crucial to avoid financial strain. |

Defining Alternative Business Funding Options

Alternative business funding is simply any money your company obtains outside traditional banking channels. Instead of walking into a bank and applying for a loan, you're finding capital through different sources entirely.

Think of traditional finance as one narrow road. Alternative funding opens up dozens of other routes to reach the same destination: growth capital for your business.

What Separates Alternative from Traditional Funding

Traditional financing means banks, credit unions, or government-backed programs. You apply, they evaluate your credit score and collateral, and they approve or deny you based on strict criteria.

Alternative sources work differently. They include family loans, peer-to-peer lending, crowdfunding, private investors, merchant cash advances, equipment financing, and trade credits. These options don't rely as heavily on your credit history or require extensive collateral.

Alternative financing methods operate through social, business, and virtual networks rather than brick-and-mortar institutions. They bridge the gap that traditional lenders leave behind.

Why Business Owners Choose Alternatives

You might choose alternative funding for several reasons:

- Banks rejected your traditional loan application

- You need capital faster than bank approval timelines allow

- Your business doesn't fit traditional lending criteria (startup, seasonal, or newer company)

- You want to avoid giving up equity to investors

- Your credit score isn't strong enough for conventional financing

- You need flexible repayment terms that match your cash flow

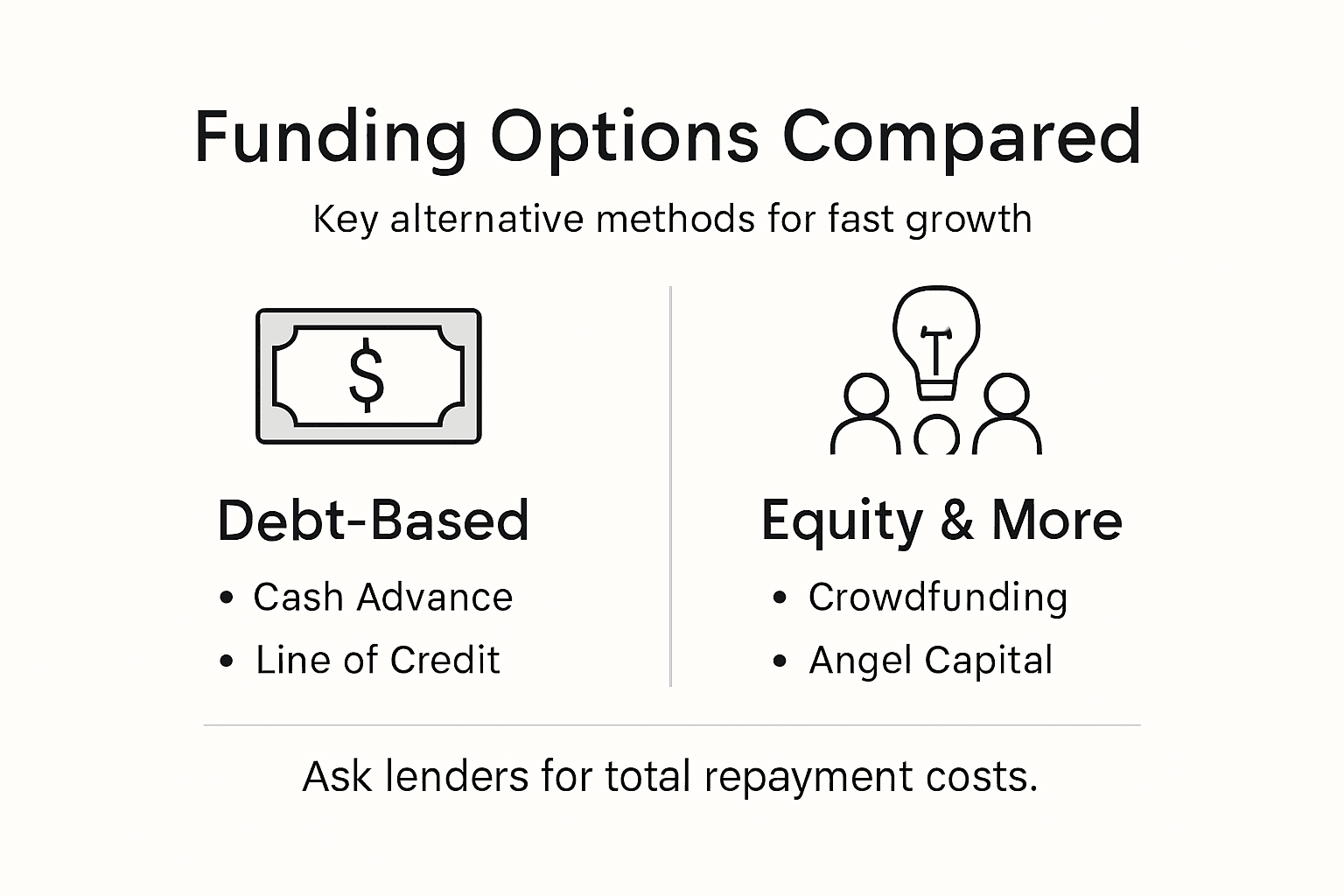

Types of Alternative Funding Available

Your options include more variety than you might realize:

Debt-based alternatives include merchant cash advances, business lines of credit, invoice financing, and equipment loans. You borrow money and repay it with interest.

Non-debt alternatives include crowdfunding, angel investors, venture capital, and grants. Some of these don't require repayment at all.

Community-based options include credit cooperatives and peer lending networks. These work at a local level where lenders know their communities.

Alternative funding sources aren't "backup" options—they're legitimate, proven strategies that thousands of successful businesses use to scale faster than traditional routes allow.

How Alternative Funding Works

The process differs from traditional lending. Alternative lenders typically evaluate your business performance rather than just your personal credit. They look at revenue, growth trajectory, customer base, and cash flow patterns.

Approval happens quickly because alternatives skip lengthy underwriting processes. Many alternative lenders can approve and fund your request within days, not months.

Repayment terms vary widely depending on the funding type. A merchant cash advance works differently than a business line of credit, which works differently than an angel investment.

Pro tip: Match your funding choice to your business timeline—if you need capital within two weeks, merchant cash advances or business lines of credit outpace traditional loans by months.

Popular Types and How They Differ

Not all alternative funding works the same way. Each type has distinct rules, timelines, costs, and requirements. Understanding these differences helps you pick the right solution for your business.

Your choice depends on how much money you need, how quickly you need it, and what you're willing to give up in return.

Merchant Cash Advances

A merchant cash advance (MCA) gives you a lump sum upfront in exchange for a percentage of your future credit card sales. You repay the advance automatically through daily or weekly deductions from your card transactions.

MCAs work fast. You can get funded within days, sometimes 24 hours. This speed comes at a cost—MCAs typically carry higher effective interest rates than traditional loans.

They're ideal if you have steady card sales but need immediate capital. Restaurants, retail stores, and service-based businesses use them frequently.

Business Lines of Credit

A business line of credit is like a credit card for your company. You get approved for a maximum amount, then draw from it whenever you need cash. You only pay interest on what you actually use.

Lines of credit offer flexibility. You might draw $5,000 one month and $15,000 the next. Once you repay borrowed amounts, that money becomes available again.

Approval timelines are shorter than traditional bank loans but longer than MCAs—typically one to two weeks.

Crowdfunding

Crowdfunding raises small amounts from many people online. You present your business idea or project on a platform, and interested backers contribute money.

There are two types: rewards-based crowdfunding (backers get products or perks) and equity crowdfunding (backers own a stake in your company). Neither requires repayment in the traditional sense.

Crowdfunding works best for products, creative ventures, or businesses with compelling stories. It's slower than other alternatives but builds customer relationships simultaneously.

Angel Investors and Venture Capital

Angel investors are individuals who invest their own money in early-stage businesses. Venture capital firms invest larger amounts in companies with high growth potential.

Both require giving up equity—a percentage ownership stake in your company. In return, you get significant capital and often business mentorship.

These suit startups or rapidly scaling businesses, not established companies looking for short-term cash. The process takes months and involves detailed pitch presentations.

Equipment Financing

Equipment financing lets you borrow money specifically to buy machinery, vehicles, or technology. The equipment itself serves as collateral.

Lenders feel confident with equipment loans because they can repossess the asset if you default. This lower risk means better interest rates than unsecured loans.

It's perfect when you need specific equipment to grow—delivery vehicles, manufacturing machinery, or point-of-sale systems.

Trade Credit

Trade credit means buying goods or services from suppliers now and paying later. Your supplier extends credit terms like "net 30" or "net 60."

This doesn't feel like borrowing because it's built into normal business operations. Yet it's powerful cash flow management—you can sell inventory before paying suppliers.

Here's a concise comparison of popular alternative business funding options and their ideal use cases:

| Funding Type | Best For | Speed to Funding |

|---|---|---|

| Merchant Cash Advance | Businesses with strong card sales | 1-3 days |

| Line of Credit | Companies with recurring needs | 7-14 days |

| Crowdfunding | Product launches, creative projects | 30+ days |

| Angel/Venture Capital | High-growth startups | 30-90 days |

| Equipment Financing | Asset-driven expansion | 3-10 days |

| Trade Credit | Inventory and supplier purchases | Depends on terms |

Quick Comparison

- Speed: MCAs win (1-3 days); lines of credit second (7-14 days); crowdfunding slowest (30+ days)

- Cost: Equipment financing cheapest; MCAs most expensive

- Equity loss: Only angel investors and venture capital require giving up ownership

- Best for: Established businesses with revenue—MCAs, lines of credit, equipment financing

- Best for startups: Crowdfunding, angel investors, personal savings

Popular alternative funding types vary dramatically in structure, risk, and accessibility—choosing the wrong type for your situation wastes time and costs more money.

Pro tip: Match the funding type to your cash flow pattern—if you have seasonal spikes, a line of credit beats a merchant cash advance because you pay interest only when you actually borrow.

Qualifying and Applying for Alternative Funding

Qualifying for alternative funding differs from traditional bank loans. Lenders evaluate different criteria and require different documentation. Understanding what each type of lender actually wants saves you time and improves your approval odds.

Alternative lenders focus on what your business does now, not just your personal credit score. They want proof of revenue, cash flow, and growth potential.

What Lenders Actually Evaluate

Alternative funding sources skip the lengthy credit evaluation process that banks use. Instead, they look at these key factors:

- Your business revenue and cash flow patterns

- How long your business has been operating

- Your industry and business model

- Personal credit score (less critical than with banks)

- Business debt and existing obligations

- Growth trajectory and customer base

Merchant cash advance lenders, for example, care most about your monthly credit card sales. Equipment lenders focus on the asset you're purchasing. Peer-to-peer lenders evaluate your business story and repayment capacity.

Preparing Your Application

Before you apply, gather essential documents. Most lenders request these materials:

- Last 2-3 years of business tax returns

- Recent bank statements (3-6 months)

- Proof of business ownership and structure

- Personal identification and personal credit history

- Business plan or description of how you'll use funds

- Financial projections for next 12 months

Organizing these documents upfront accelerates the approval process. Some lenders fund within 24 hours if your application is complete.

The Application Process

Most alternative lenders use streamlined applications. Here's the typical timeline:

- Submit your initial application online or through a loan officer

- Provide supporting documentation within 24-48 hours

- Lender reviews your application and performs due diligence (1-3 days)

- Receive approval decision and funding offer

- Sign agreement and receive funds

The entire process typically takes 3-7 days for merchant cash advances and business lines of credit. Crowdfunding and investor pitches take longer—weeks or months.

Understanding Qualification Criteria

Different funding types have different requirements. A business line of credit might require 2+ years in business and $150,000 annual revenue. A merchant cash advance needs only consistent card sales and 6 months in business.

Equipment financing focuses on the equipment value, not your personal creditworthiness. Angel investors want high-growth potential and compelling business vision.

Researching funding programs aligned with your business type and goals improves your match rate significantly.

Common Application Mistakes

Don't sabotage yourself with these errors:

- Submitting incomplete applications

- Providing inconsistent financial information

- Missing application deadlines

- Exaggerating business performance or projections

- Failing to explain how you'll use the funds

- Ignoring lender-specific requirements

Read each application carefully. Different lenders ask different questions. Generic, careless applications get rejected.

Improving Your Approval Chances

You can strengthen your application before submitting:

- Clean up your personal and business credit reports

- Build up your business savings account to show stability

- Document your revenue clearly and consistently

- Create realistic financial projections

- Prepare a clear business plan explaining growth strategy

- Gather customer testimonials or success stories

Strong applications require honest financial documentation and clear explanations of how you'll use borrowed money—lenders want confidence that you'll repay them.

Pro tip: Apply to multiple lenders simultaneously using the same documentation package; getting rejected by one lender doesn't mean you'll be rejected by others, and comparing offers takes just a few extra applications.

Weighing Costs, Risks, and Common Pitfalls

Alternative funding solves immediate cash problems, but it comes with trade-offs. Understanding the real costs and risks prevents you from making expensive mistakes that damage your business long-term.

Speed and accessibility have a price. The faster you access money, the more you typically pay for it.

Understanding the True Cost of Borrowing

Alternative funding generally costs more than traditional bank loans. A bank might offer a 7% interest rate on a small business loan. A merchant cash advance might cost the equivalent of 40% annually.

Here's why the difference matters: borrowing $50,000 at 40% effective annual rate costs you dramatically more in total repayment than borrowing at 8%. Over time, higher rates compound your financial burden.

Different funding types have different cost structures:

- Merchant cash advances: Percentage of future sales (typically 1.2% to 1.5% daily)

- Business lines of credit: Annual percentage rate, often 7% to 36%

- Equipment financing: Interest rates tied to equipment value, usually 5% to 15%

- Angel investors: Equity stake (typically 10% to 30% ownership)

- Crowdfunding: Platform fees (3% to 5% of funds raised)

Calculate the total cost before committing. Don't just look at the interest rate—examine what you'll actually repay.

Hidden Risks and Over-Leverage

Alternative financing carries risks that traditional loans don't. Many business owners borrow more than they should because the money comes so quickly.

Over-leverage happens when you owe more than your business can comfortably repay. You have a $50,000 merchant cash advance, a $30,000 line of credit, and $20,000 in equipment financing. Your monthly obligations exceed your revenue.

Then one bad month hits. A customer doesn't pay. A competitor steals your biggest client. Suddenly you can't cover your debt payments.

Protect yourself by:

This table clarifies common risks of alternative funding and mitigation tips:

| Common Risk | Potential Impact | Mitigation Strategy |

|---|---|---|

| Over-leverage | Cash flow strain, insolvency | Borrow only what's essential |

| High effective interest | Increased repayment cost | Calculate total cost upfront |

| Misaligned funding type | Operations disruption | Match with real cash flow needs |

| Equity loss to investors | Reduced control of business | Negotiate clear ownership terms |

- Only borrowing what you genuinely need

- Creating a repayment plan before accepting funds

- Projecting worst-case revenue scenarios

- Keeping credit availability as backup, not default

- Avoiding multiple funding sources simultaneously

Misalignment with Business Goals

Sometimes the funding type doesn't match your business reality. You take a merchant cash advance, but 60% of your revenue comes from invoices, not card sales. Now you're repaying advance against income that doesn't exist.

Or you accept angel investment, but the investor expects you to pivot the business toward their vision. You lose control of your company's direction.

Match your funding choice to how your business actually operates. Seasonal businesses need flexible repayment. Growth-stage businesses can handle equity investors. Established service businesses excel with lines of credit.

Common Pitfalls to Avoid

Don't fall into these traps:

- Borrowing without a specific use plan

- Ignoring fine print about fees and penalties

- Taking multiple loans without tracking total obligations

- Using borrowed money for personal expenses

- Missing repayment deadlines (damages future borrowing)

- Choosing lenders based only on speed, ignoring costs

The cheapest money isn't always the fastest money—and the fastest money isn't always the cheapest—weigh both factors against your actual business timeline and capacity to repay.

Pro tip: Create a detailed spreadsheet showing all current and potential debts with monthly payment obligations; if total debt payments exceed 30% of projected monthly revenue, you're borrowing too much regardless of funding source.

Alternative vs. Traditional Lending Compared

Traditional banks and alternative lenders operate on completely different playbooks. Understanding the differences helps you pick the right funding source for your situation.

It's not about one being "better"—it's about which fits your business right now.

Credit Standards and Qualification

Banks evaluate your creditworthiness obsessively. They pull your credit report, review your personal and business credit scores, analyze tax returns, and examine collateral extensively. A single missed payment five years ago might disqualify you.

Alternative lenders care less about credit history. They focus on current business performance. If you've recovered from past financial struggles and your business generates revenue today, alternative lenders approve you.

This fundamental difference means:

- Banks: Reject startups, seasonal businesses, and anyone with past credit problems

- Alternative lenders: Accept riskier borrowers, newer companies, and those with damaged credit

- Banks: Require 2+ years business history

- Alternative lenders: Approve businesses with 6 months of operating history

Speed and Process Complexity

Banks move slowly. Underwriting takes weeks or months. You fill out exhaustive applications, provide numerous documents, and wait through committee meetings. Even approved loans take 30+ days to fund.

Alternative lenders operate at business speed. Some fund within 24 hours. You submit an application, provide supporting documents within 1-2 days, get approved in 3-5 days, and receive funds immediately.

This speed gap matters when your business needs capital urgently. A retail store needs inventory funding before the holiday season. Waiting 60 days for a bank loan means missing your sales window entirely.

Costs and Interest Rates

Traditional bank credit typically costs less than alternative financing. Banks charge 5% to 10% interest on small business loans. Alternative lenders charge 15% to 50% or higher.

Why the difference? Alternative lenders accept higher risk, so they charge higher rates. They also operate with lower overhead and faster approval processes, which reduces cost per loan.

But sometimes paying more makes sense. A $50,000 merchant cash advance at 40% effective rate, funded in two days, might beat waiting 60 days for a $25,000 bank loan at 8%.

Collateral and Personal Guarantees

Banks require collateral—assets they can seize if you default. Your business assets, personal home, or investment accounts secure the loan. They also typically require personal guarantees from owners.

Alternative lenders vary. Merchant cash advances use future sales as collateral. Equipment loans use the equipment itself. Some require no collateral at all, instead pricing in the additional risk through higher rates.

Alternative funding offers more flexibility on collateral requirements.

Loan Terms and Repayment Structure

Bank loans have clear timelines—you borrow $50,000 and repay over 3 to 5 years with fixed monthly payments. You know exactly what you owe.

Alternative financing structures vary wildly. Merchant cash advances deduct daily or weekly from sales. Lines of credit let you draw and repay as needed. Equipment loans last only as long as the equipment stays useful.

| Factor | Traditional Banks | Alternative Lenders |

|---|---|---|

| Approval timeline | 30-60 days | 1-7 days |

| Credit score impact | Critical | Secondary |

| Typical interest rate | 5-10% | 15-50%+ |

| Business history required | 2+ years | 6+ months |

| Collateral flexibility | Strict | Flexible |

| Startup-friendly | No | Yes |

Traditional lending prioritizes stability and proven history; alternative lending prioritizes current performance and growth potential—neither approach is wrong, just different.

Pro tip: If you have strong credit and can wait 60 days, exhaust bank options first for lower costs; if your timeline is tight or credit is imperfect, alternative lenders solve problems banks won't touch.

Unlock Fast and Flexible Funding to Fuel Your Business Growth

Struggling to secure capital quickly because traditional banks rejected your loan or your business doesn't fit the typical mold Alternative business funding offers solutions that match your pace and needs. At Capital for Business, we understand that waiting weeks or months for approval can stall opportunities. Whether you need a merchant cash advance, equipment financing, or a business line of credit we provide tailored options designed for small businesses like yours.

Take control of your cash flow now and avoid costly delays. Explore how our financial services have helped businesses nationwide and in Canada grow since 2009. Visit Capital for Business to learn more and apply today. Act now to experience fast funding that supports your vision without the lengthy process traditional lenders require.

Frequently Asked Questions

What are alternative business funding options?

Alternative business funding refers to any money your business acquires outside traditional banking systems, such as loans from banks or credit unions. It includes methods like crowdfunding, peer-to-peer lending, merchant cash advances, and angel investing, providing businesses more flexibility in accessing capital.

How do alternative funding sources differ from traditional loans?

Alternative funding sources evaluate businesses based on current performance rather than strict credit scores and collateral requirements, allowing for quicker approval. While traditional loans often require extensive documentation and take weeks to process, alternative funding can be secured in days.

What types of alternative funding can I use for my business?

You can choose from various alternative funding options, including debt-based methods like business lines of credit and merchant cash advances, as well as non-debt options like crowdfunding and angel investment. Each option has unique requirements and benefits based on your business needs.

How can I improve my chances of qualifying for alternative funding?

To improve your chances, focus on documenting your business revenue and cash flow clearly, maintaining a strong business plan, and preparing your application with all necessary financial statements. Additionally, demonstrate your growth potential and clarify how you intend to use the funds effectively.